Bittensor Failed Subnets reveal what subnet deaths teach investors about dTAO, alpha speculation, and Bittensor’s real health.

Author: Kritika Gupta

Bittensor Failed Subnets tell a more honest story about the network than its winners alone. Most subnets fail. Many were never serious attempts at building decentralized AI infrastructure. Instead, their collapse through market decay, incentive gaming, or direct intervention reveals more about Bittensor’s real condition than any highlight reel of top emitters.

This article does not attack the network. It also does not defend every weak subnet. Instead, it examines the cull mechanism itself: the deregistration process active since late 2025, the data on what the network prunes, and the uncomfortable lessons for investors, builders, and anyone still buying the clean “decentralized intelligence marketplace” pitch.

Everyone studies the winning subnets, but the real education in Bittensor comes from the dead ones. That is the central argument of this piece. Most subnets fail. Many were never serious attempts at building decentralized AI infrastructure. And the pattern of how they die reveals more about Bittensor’s actual health than any success story does.

The top emitters show what the network wants to become. The failed subnets show what the network really tolerates, rewards, rejects, and sometimes has to forcibly correct. That distinction matters for anyone trying to understand TAO beyond the clean pitch.

Bittensor sells a powerful idea: an open market for machine intelligence, where miners compete, validators score useful work, and capital flows toward productive subnets. However, the graveyard tells a messier story. It shows speculative alpha games, weak product-market fit, abandoned experiments, incentive loops, and occasional foundation-level intervention.

That does not make Bittensor a scam. It also does not make every failed subnet a victim. The point is not to dunk on the network or whitewash the failure rate. The point is to catalogue what actually breaks, why it breaks, and what those failures teach investors, builders, and researchers.

For broader context on the base thesis, read our Bittensor (TAO) Guide. But this section starts with the harder truth: if you only study the trophy case, you miss the mechanism. In Bittensor, the obituaries are not side notes. They are market data.

Before we talk about failed subnets, we need to understand how Bittensor actually removes them.

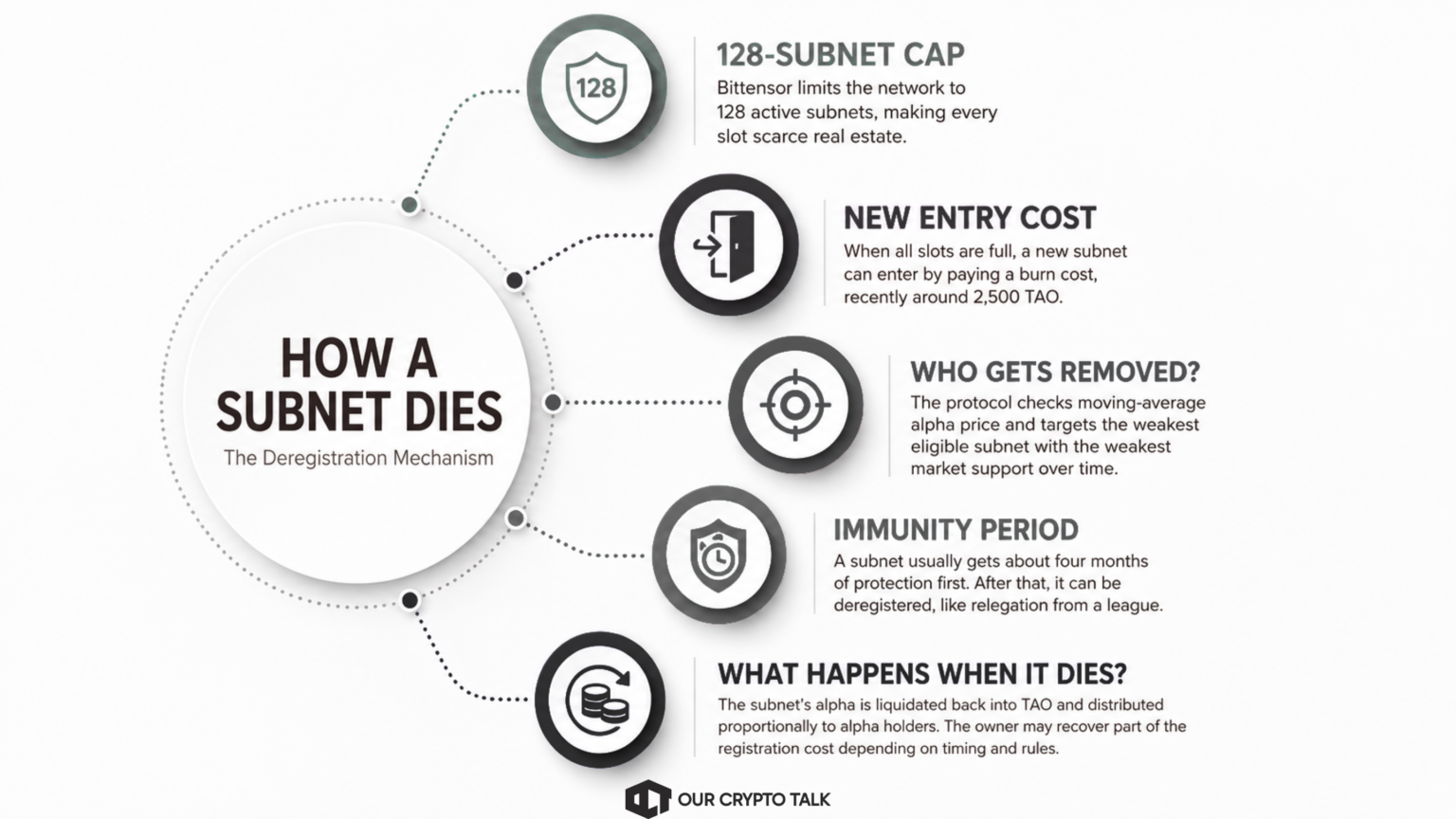

Bittensor caps the network at 128 active subnets. That cap matters because it turns every subnet slot into scarce real estate. When all 128 slots are full and a new subnet registers, the network must make room. The new entrant pays a burn cost, recently around 2,500 TAO, and the protocol then looks for the weakest eligible subnet already inside the system.

The key metric is the subnet’s moving-average alpha price. In simple terms, the network tracks which subnet alpha has the weakest market support over time. If that subnet has already passed its roughly four-month immunity period, it becomes eligible for removal. The protocol then deregisters that subnet and gives the slot to the new entrant.

To understand Bittensor Failed Subnets, readers first need to understand the deregistration mechanism. Think of it as relegation. Bittensor does not let every team stay in the league forever. New subnets can enter, but someone at the bottom must go down. The system cuts underperformers to make room for fresh attempts.

When a subnet dies, its alpha token does not simply vanish. The protocol liquidates the subnet’s alpha back into TAO and distributes that TAO proportionally to alpha holders. Meanwhile, the subnet owner may recover part of the original registration cost depending on when they registered and which registration mechanics applied at the time.

This system became especially important after dTAO changed the role of subnet alphas and market demand. For a deeper breakdown of that shift, read our dTAO explainer.

Importantly, deregistration did not run continuously through every phase of Bittensor’s development. The network paused or disabled it during the early dTAO rollout, then re-enabled it in late 2025. Since then, subnet death has become a live mechanism again, not just a theoretical threat.

The failed subnet list matters because it turns a vague criticism into a testable pattern. Bittensor does not just have “some weak subnets.” It has several distinct ways a subnet can die or approach death.

This Bittensor Failed Subnets list separates verified named cases from live at-risk entries. Some fail quietly because their alpha price decays and they slide into the pruning zone. Some fail loudly because the incentive design rewards token demand more than useful AI work and others collapse after disputes with core actors. Others simply never find real product-market fit.

The table below does not pretend to be a complete historical graveyard. Bittensor does not present every past deregistration in one clean public page for casual readers. So this list separates verified named cases from live at-risk entries visible in pruning data.

Bittensor failed subnets taxonomy

The pattern is the point. Bittensor’s graveyard does not show one single failure mode. It shows a market where weak narratives decay, reflexive token games can hijack emissions, governance disputes can damage even major subnets, and ordinary product-market fit still decides survival. For a broader primer on how subnets are supposed to create value, read our guide to Bittensor subnets and decentralized AI.

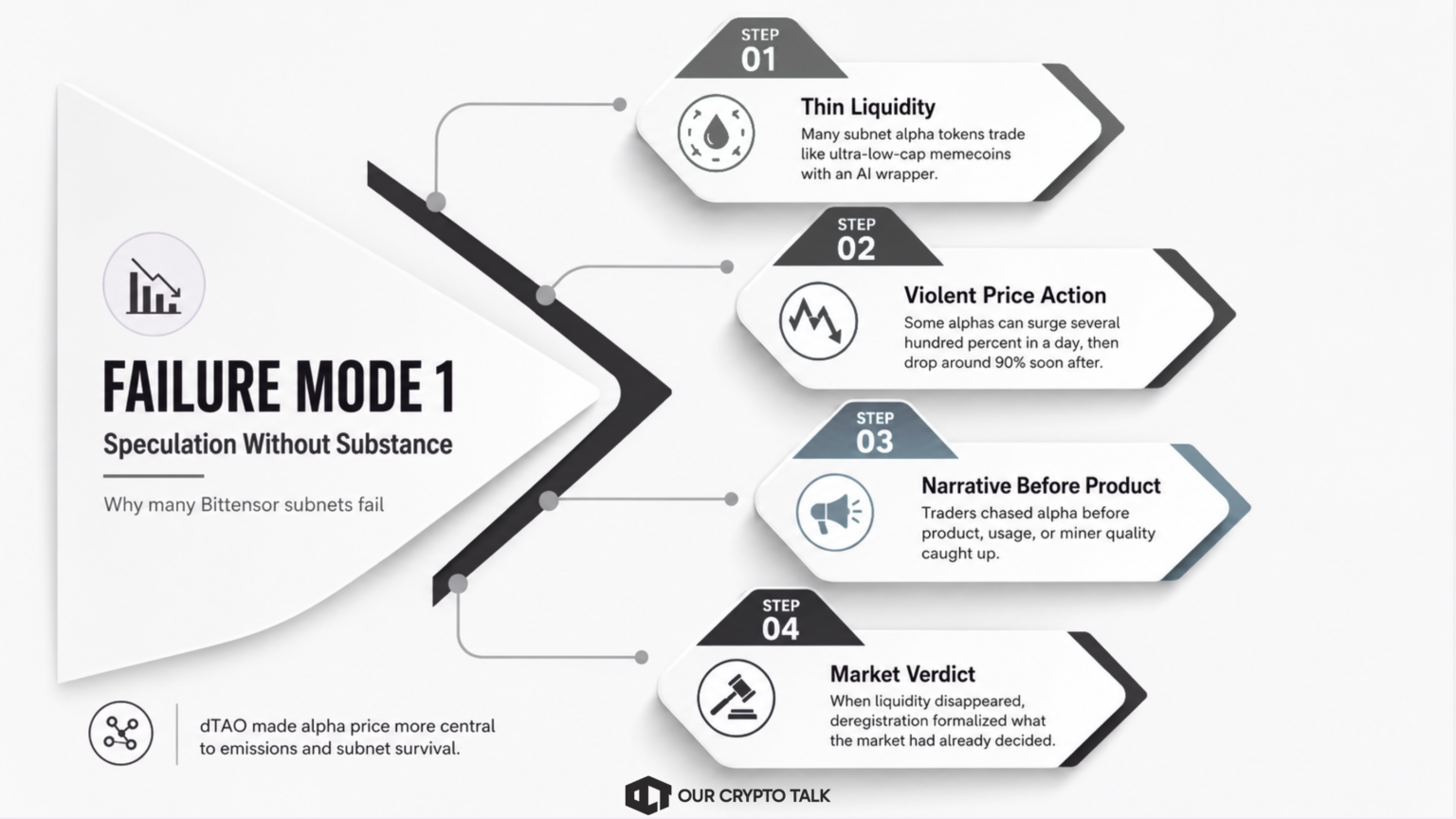

The largest failure category in Bittensor is also the one the bull case usually treats as background noise: speculation without substance.

This does not describe the best subnets. It describes the long tail. Many subnet alpha tokens trade like ultra-low-cap memecoins with an AI wrapper. They have thin liquidity, aggressive emissions, small float, and violent price action. Some alphas can gain several hundred percent in a single day, then lose around 90% shortly after. That kind of movement rarely proves that a subnet has found real demand for machine intelligence. More often, it proves that a tiny market found a narrative and then ran out of buyers.

This matters because dTAO made alpha price more central to subnet survival and emissions. In theory, market demand should help route TAO toward useful subnets. In practice, it also created a speculative layer where traders could chase subnet alphas before the underlying product, usage, or miner quality caught up.

For the long tail, Bittensor Failed Subnets often started as tokens with narratives rather than products with users. This matters because dTAO made alpha price more central to subnet survival and emissions. In theory, market demand should help route TAO toward useful subnets. In practice, it also created a speculative layer where traders could chase subnet alphas before the underlying product, usage, or miner quality caught up.

That does not mean every failed subnet was fraudulent. Some builders likely had serious ideas but failed to reach users. Others underestimated how hard it is to turn a subnet into a durable market for intelligence. However, many never looked like production systems in the first place. They looked like tokens searching for a reason to exist.

That distinction is crucial. The critique does not indict Bittensor’s genuine builders or the stronger subnets producing inference, agents, data, or training work. It indicts the speculative long tail that used the subnet model as a launchpad for narrative liquidity. When that liquidity disappeared, deregistration simply formalized what the market had already decided.

For a broader comparison of Bittensor’s subnet model against other AI crypto networks, read our Bittensor vs Render breakdown. For market-side context, see our Bittensor price prediction.

Speculation is one problem. Gaming the emissions system is worse.

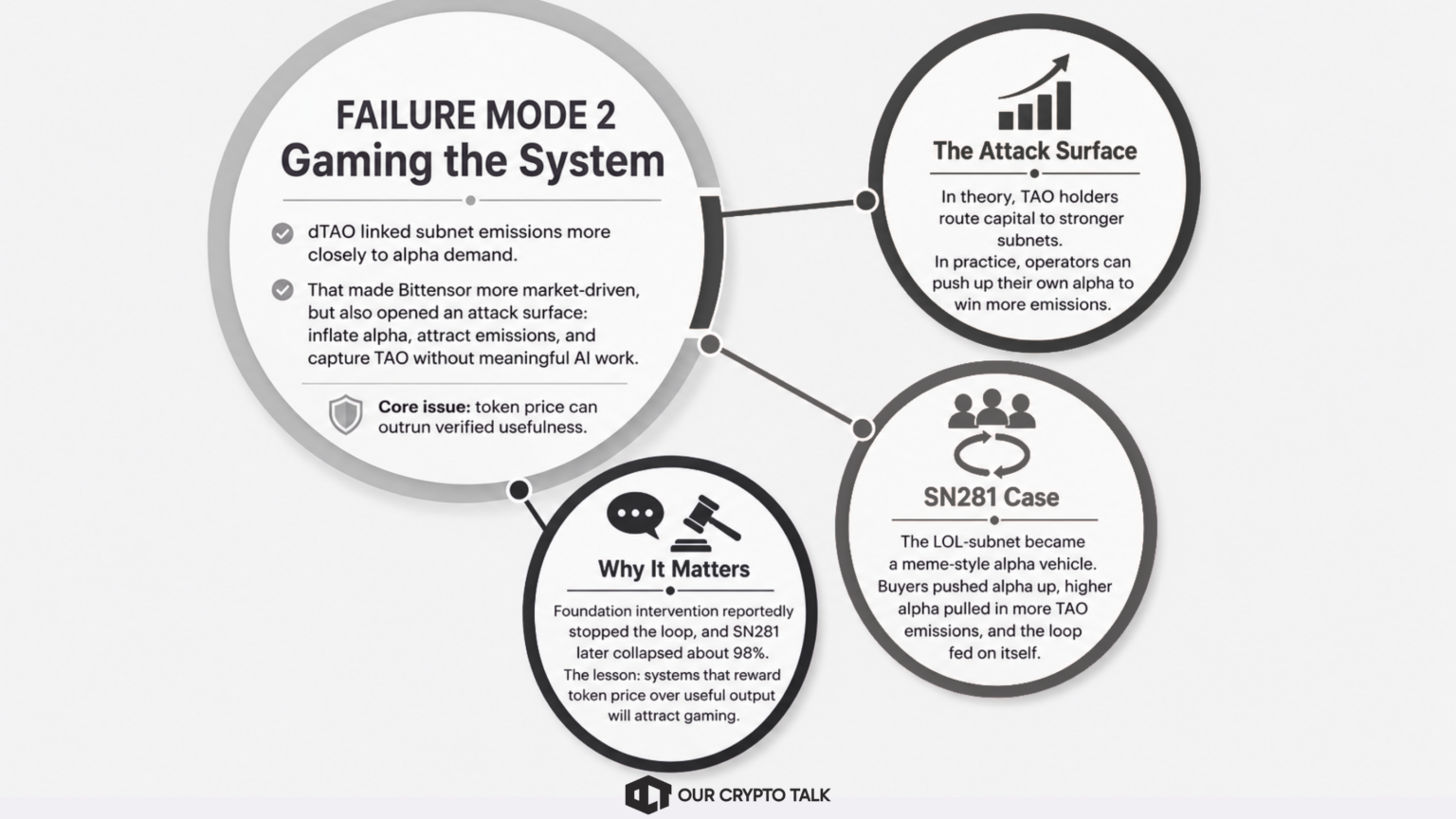

dTAO tried to make Bittensor more market-driven by tying subnet emissions to alpha demand. In theory, that gives TAO holders more power to decide which subnets deserve capital. In practice, it also created an obvious attack surface: inflate your own alpha, attract more emissions, and capture TAO without producing meaningful AI work.

Subnet 281, the so-called LOL-subnet, exposed that weakness early. An anonymous operator took control of the subnet and turned it into “TAO Accumulation Corporation,” a meme-style alpha vehicle with no serious connection to decentralized AI. Its logic was brutally simple. Hold the subnet alpha, receive a better score, capture more emissions, and encourage more people to buy the same alpha.

The SN281 case shows why Bittensor Failed Subnets cannot only be explained as weak execution. That subnet turned into a reflexive emissions loop. Buyers pushed up the alpha price. A higher alpha price helped the subnet attract more TAO emissions. Those emissions made the trade look more attractive. Then more buyers entered. The system rewarded balance-sheet demand, not useful output.

This was not a subtle edge case. The subnet openly encouraged holders to buy its alpha to inflate its share of emissions. Reports described miners needing no real work, with scoring linked to token holdings instead of computational contribution. Eventually, the Opentensor Foundation intervened through its root stake and custom validator logic, and the subnet’s alpha reportedly collapsed by roughly 98%.

That intervention protected the network in the short term. However, it also revealed the deeper design tension. If Bittensor needs centralized correction to stop a subnet from converting emissions into a token game, then the market mechanism alone does not fully enforce useful AI production.

The lesson is not simply “bad actors exist.” Crypto already knows that. The sharper lesson is this: any incentive model that pays for token price instead of verified usefulness will attract actors who optimize for token price. SN281 did not break the thesis by itself. It exposed the part of the thesis that still needs hard proof.

For the macro version of this critique, read our Bittensor Ponzi analysis.

Not every subnet death comes from the market. Sometimes, the market watches core power step in first.

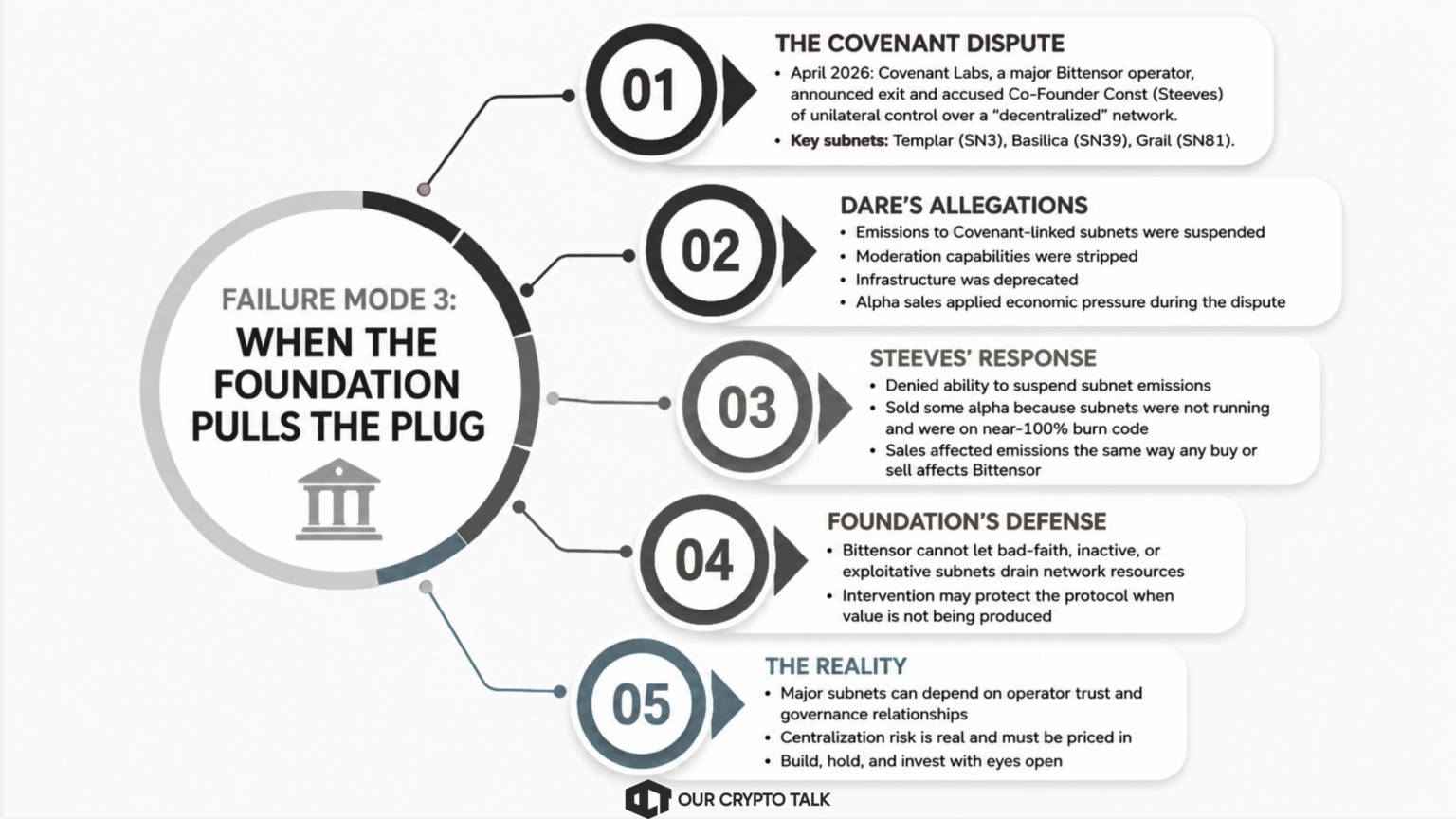

The April 2026 Covenant Labs dispute is the clearest example, and it deserves careful treatment. Covenant was not a minor builder. It operated several of Bittensor’s most visible subnets, including Templar SN3, Basilica SN39, and Grail SN81. Templar, in particular, had become central to the Bittensor bull case after the Covenant-72B training milestone.

Then the relationship broke.

Covenant founder Sam Dare publicly announced the team’s exit and accused Bittensor co-founder Jacob Steeves, known as Const, of exercising unilateral control over a network marketed as decentralized. Dare alleged that emissions to Covenant-linked subnets had been suspended, moderation capabilities had been stripped, infrastructure had been deprecated, and visible alpha sales had applied economic pressure during the dispute.

Those are serious claims, but they remain claims. Steeves denied the core allegation that he could suspend subnet emissions. His response argued that he sold some alpha holdings because the subnets were not running and were on near-100% burn code. He said those sales affected emissions in the same way any buy or sell affects Bittensor, not through special privilege.

That distinction matters. If Dare’s version is right, Bittensor has a direct centralization problem. If Steeves’ version is right, the dispute still shows a different problem: major subnets can depend heavily on operator trust, operational continuity, and governance relationships.

The foundation also has a legitimate defense in principle. Bittensor cannot let bad-faith subnets, inactive systems, or emissions games drain network resources forever. Intervention may protect the protocol when a subnet stops producing value or actively exploits the incentive layer.

However, the honest takeaway is not a verdict on who acted correctly in April 2026. It is simpler and more uncomfortable. A network marketed as decentralized still appears to have a hand that can materially weaken or end a subnet’s future. Builders and alpha holders need to price that risk.

For more context on the subnet itself, read our Templar SN3 deep dive. For the broader base thesis, start with our Bittensor TAO Guide.

The strongest defense of Bittensor’s failed subnets is also the simplest: death is the point.

A permissionless network cannot let every subnet live forever. If Bittensor wants to support an open market for machine intelligence, it needs a way to remove weak experiments, abandoned projects, and speculative shells. The 128-subnet cap forces that discipline. When a new entrant arrives, the weakest eligible subnet risks losing its slot. That pressure makes the system harsher, but also more honest.

The bull case argues that Bittensor Failed Subnets prove the network’s selection pressure works. In this view, deregistration works like natural selection. It concentrates TAO emissions, validator attention, miner effort, and market interest on subnets that can actually defend their existence. It also raises the bar for new entrants. A builder cannot simply launch a subnet, collect emissions, and coast forever. After the immunity window ends, the market can challenge the slot.

Deregistration also has a practical benefit. When a subnet dies, the protocol liquidates its alpha back into TAO and distributes value to alpha holders. That prevents capital from sitting indefinitely inside dead pools with no productive future. In crypto, where zombie protocols often survive for years through inertia, that matters.

A high failure rate should not shock anyone. Most startups fail. Most tokens fail and most open-source experiments fail. A permissionless AI market will naturally produce many bad ideas, weak teams, and failed attempts. The question is not whether subnets fail. The question is whether the system removes enough weak ones to let stronger ones compound.

And Bittensor does have real winners. Some subnets have shown credible traction in serverless compute, inference, agent work, data markets, and distributed training before the Covenant dispute. That matters. It proves the filter can work, even if it works imperfectly.

So the fair bull case is clear: failed subnets do not automatically discredit Bittensor. They may prove that the network enforces scarcity, competition, and accountability better than most crypto ecosystems. For a fuller review of the base thesis, read our Bittensor crypto review.

The failed subnet list matters because it turns Bittensor from a pitch into a system investors can judge. The lessons are different for each audience, but they all point to the same conclusion: subnet death is not noise. It is the clearest stress test of the model. For investors and builders, Bittensor Failed Subnets are not background noise. They are risk signals.

They are thin, speculative assets with reflexive price action, weak liquidity, and limited visibility into real demand. The four-month immunity period can also become an exit trap. A new subnet may pump while it remains protected, but once immunity expires, the market starts pricing the risk of deregistration more aggressively.

If the subnet has no users, no sticky miner network, and no reason for validators to keep supporting it, the alpha can decay fast. Meanwhile, emissions remain highly concentrated in a small group of stronger subnets, which leaves the long tail fighting over scraps. In practice, most alpha exposure looks closer to venture-style risk than productive cash-flow ownership.

For builders, the lesson is even simpler: product-market fit or perish. A subnet cannot survive forever on a ticker, a Discord, and an AI narrative. The registration cost, recently around 2,500 TAO, represents real capital. Builders must treat it like a burn-risk investment, not a marketing fee. They need useful work, reliable operations, validator trust, and a clear reason for demand to persist after the launch hype fades. The Covenant dispute also teaches a more uncomfortable lesson. Foundation alignment and core governance relationships matter more than the decentralization pitch often implies.

For the Bittensor thesis, the deaths force maturity. Decentralized AI is not a clean machine that automatically routes capital to intelligence. It is messier, more political, more speculative, and more gameable than the pitch decks suggest. That does not kill the thesis. It makes the thesis harder, narrower, and more dependent on execution.

The failed subnet list does not give one simple answer. It supports two serious readings of Bittensor, and both deserve attention.

The bullish reading says the graveyard proves the model works. Bittensor is an open market for machine intelligence, so most experiments should fail. That is how startup ecosystems work. That is how venture portfolios work. The point is not to make every subnet succeed. The point is to create enough competition that weak projects lose their slots and stronger ones compound. From this angle, deregistration looks healthy. It removes dead weight, recycles capital, and forces builders to prove demand instead of hiding behind a permanent allocation of emissions.

The bearish reading sees the same evidence differently. If a large share of subnets are speculative alpha vehicles, if token price can matter more than verified usefulness, if emissions remain concentrated in a small winner set, and if the foundation can still materially influence outcomes, then the harder question becomes unavoidable: how decentralized and productive is this system in practice? A market that needs frequent correction from core actors is still a market, but it is not the clean permissionless machine that the simplest Bittensor pitch suggests.

OurCryptoTalk’s view sits between those extremes. The deaths do not kill the Bittensor thesis. The idea of incentivizing useful intelligence through open competition still matters, and the network has produced real subnets worth studying. However, the deaths do puncture the marketing version of Bittensor. They show that the system is more speculative, more political, and more fragile than the bull case usually admits.

That is why serious investors should study the graveyard as carefully as the trophy case. The winners show what Bittensor could become. The failures show what it actually is today.

The failed subnets are not a clean reason to write off Bittensor. They are a reason to distrust anyone who only shows you the winners.

That includes bullish threads, dashboard screenshots, alpha showcase posts, and even OCT’s own past coverage when it focused too heavily on the trophy case. A serious view of Bittensor must include both sides: the subnets that prove the model can work and the subnets that show where the model breaks.

The next phase of the thesis will depend less on how many new subnets launch and more on what happens after they enter the arena. Watch the subnet death rate as registrations and deregistrations cycle through the 128-slot cap. Watch whether emissions keep concentrating in a small group of dominant subnets or spread toward a broader base of useful networks. Most importantly, watch how often the foundation or core actors intervene directly compared with how often the market mechanism decides outcomes on its own.

That is the real test. If weak subnets die because better ones replace them, Bittensor’s Darwinian model looks stronger. If weak subnets survive through hype, or strong subnets can still fall through politics, the decentralization pitch needs a much bigger discount. In a network built on competition, the obituaries are not a bug in the story. They are the story.