Bittensor (TAO) uses subnets, miners, validators, and a 21M fixed supply to decentralize AI. Learn how dTAO, halvings, and 128+ subnets shape TAO in 2026.

Author: Kritika Gupta

Bittensor (TAO) is one of crypto’s most ambitious attempts to decentralize artificial intelligence. Instead of relying on closed models controlled by a few companies, Bittensor uses subnets, miners, validators, and TAO incentives to create an open marketplace for machine intelligence. This guide explains how Bittensor works, why its 21 million token supply matters, what dTAO changed, which subnets are gaining traction, and what risks investors should watch in 2026.

To understand TAO’s halving you first need to understand how Bittensor works as a network.

Bittensor is a decentralized AI network that turns machine intelligence into an open market. Miners produce AI outputs, validators score their quality, and the network pays rewards in TAO to the participants that deliver the most useful work.

Bittensor does not operate like a single AI app, chatbot, or foundation model. It works as a blockchain-based coordination layer for AI markets. Each subnet focuses on a specific task, such as inference, training, data, agents, prediction models, or compute-related services. Therefore, miners compete inside those subnets, validators judge performance, and TAO emissions flow toward the strongest contributors.

TAO vs RNDR vs AKT vs FET

This structure makes Bittensor one of crypto’s clearest attempts to decentralize AI production. Instead of letting a few companies control model access, pricing, and infrastructure, Bittensor gives developers, GPU operators, researchers, and validators a permissionless way to compete in machine intelligence markets.

As of May 2026, CoinGecko listed Bittensor near a $2.7 billion market cap with about 9.6 million Bittensor TAO circulating, while CoinMarketCap showed roughly 10.9 million TAO in circulation and a market cap above $3 billion. Grayscale reported 129 active subnets, while April 2026 ecosystem coverage cited 128 active subnets. Daily emissions fell to about 3,600 TAO after the December 2025 halving.

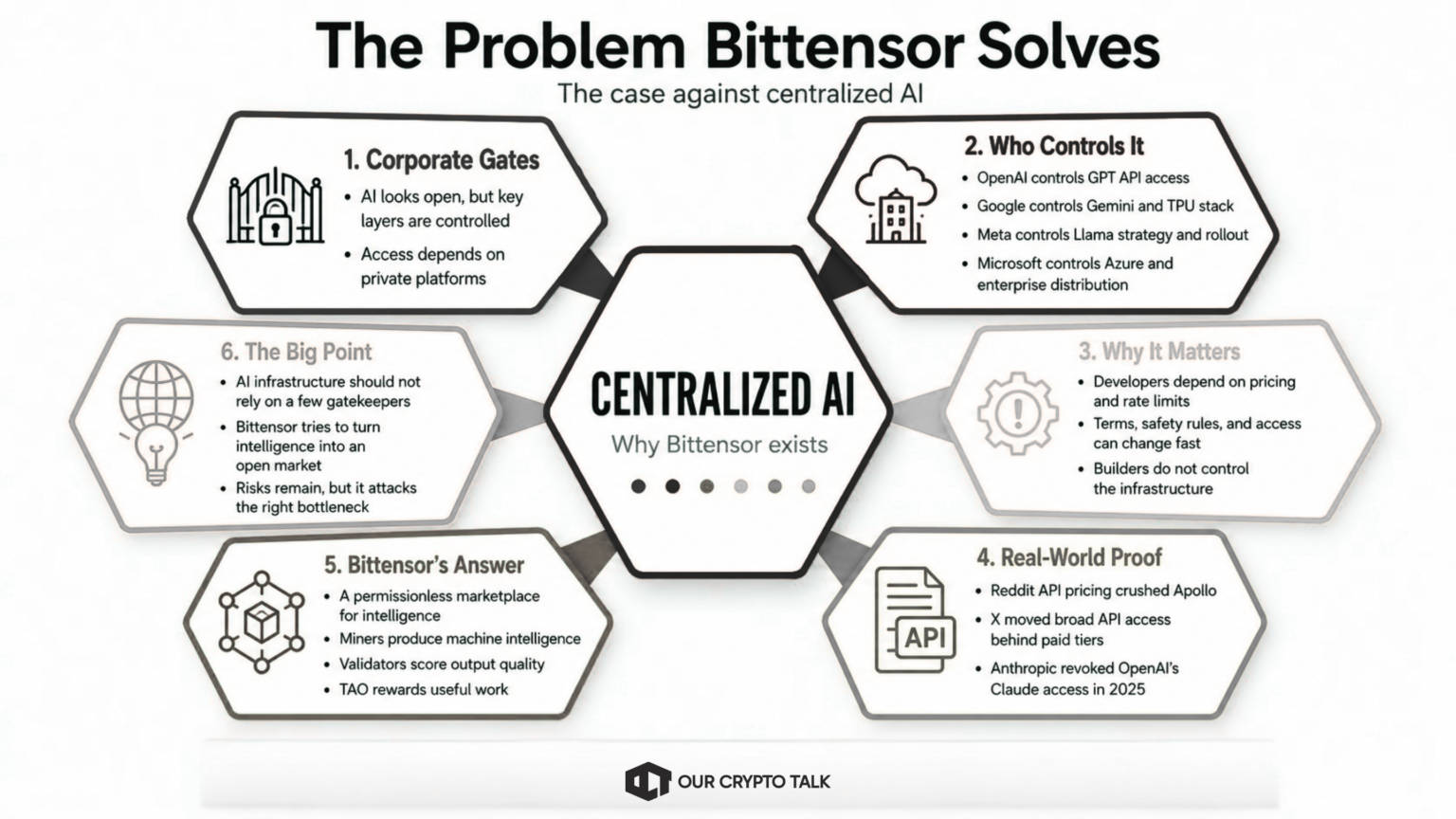

AI looks open from the outside. In practice, its most valuable layers sit behind corporate gates.

OpenAI controls access to GPT models through its API. Google controls Gemini, DeepMind research, TPU infrastructure, and a large share of AI distribution through Search, Android, and Workspace. Meta releases some open-weight models, but it still controls the infrastructure, licensing choices, and product roadmap around its AI stack. Microsoft sits across the cloud and distribution layer through Azure, OpenAI access, GitHub, Windows, and enterprise software.

That concentration matters. Developers do not just depend on models. Additionally, they depend on pricing, rate limits, account access, safety policies, licensing terms, and API availability set by companies they do not control. A startup can build on a model API for months, then face a pricing change, model deprecation, stricter usage policy, or revoked access with limited recourse.

This is not theoretical. Reddit’s 2023 API pricing changes forced Apollo, one of the most popular third-party Reddit apps, to shut down after its developer said the new terms could cost about $20 million per year. X also removed broad free API access in 2023 and introduced paid tiers, with researchers later documenting how the change damaged academic access to public social data. Anthropic revoked OpenAI’s access to Claude in 2025 after alleging a terms-of-service violation, showing that even the biggest AI companies can lose access to rival models when the platform owner decides the line has been crossed.

Bittensor TAO exists as a direct counterpoint to that model. It does not ask builders to trust one lab, one cloud provider, or one API gatekeeper. It creates a permissionless marketplace where miners produce machine intelligence, validators judge output quality, and TAO emissions reward useful work.

The point is simple. If AI becomes the core infrastructure of the internet, access cannot depend entirely on private companies changing terms from the top down. Bittensor tries to move intelligence production into an open market.

That does not make Bittensor risk-free. It still has validator incentives, subnet quality issues, and token-driven speculation to prove out. But it attacks the right bottleneck. Centralized AI controls access. Bittensor tries to make intelligence a market.

Bittensor works through a simple loop: miners produce machine intelligence, validators judge its quality, and the network pays TAO to the participants that perform best.

The easiest way to understand Bittensor TAO is to think of it as a marketplace for AI work. Miners are the suppliers. They run models, serve outputs, train systems, provide data, or complete other machine-learning tasks depending on the subnet. Validators are the buyers, reviewers, and quality-control layer. They send tasks to miners, compare responses, score performance, and report those scores back to the network.

Each subnet defines its own market. One subnet may reward text inference. Another may focus on distributed training. Another may measure data quality, prediction accuracy, or compute performance. This makes Bittensor more flexible than a single AI protocol. Therefore, it can support many different machine-intelligence markets under one economic system.

The miner-validator loop creates constant competition. Miners must improve their outputs because validators test them repeatedly. Validators must score accurately because their own rewards and influence depend on useful evaluation. If a miner performs poorly, it earns less TAO. If it performs well, it can attract more emissions and more attention from validators.

Yuma Consensus sits behind this process. It aggregates validator scores and turns them into network-wide reward signals. In plain terms, Yuma helps decide which miners and validators contributed the most value, then routes TAO emissions toward them.

A useful analogy is academic peer review with financial consequences. Miners submit work. Validators review it. Yuma aggregates the reviews. TAO emissions act as the prize pool. The difference is that Bittensor runs this process continuously, across live markets, with crypto incentives attached.

Another analogy is marketplace bidding. Miners compete to offer the best intelligence for a given task. Validators decide which suppliers are most reliable. Altogether, the protocol then rewards the suppliers and evaluators that help the market function best.

This design gives Bittensor its core advantage. It does not try to pick one winning AI model. It creates conditions where many models, services, datasets, and AI workflows can compete. The network rewards measured performance rather than brand name, corporate access, or closed infrastructure control.

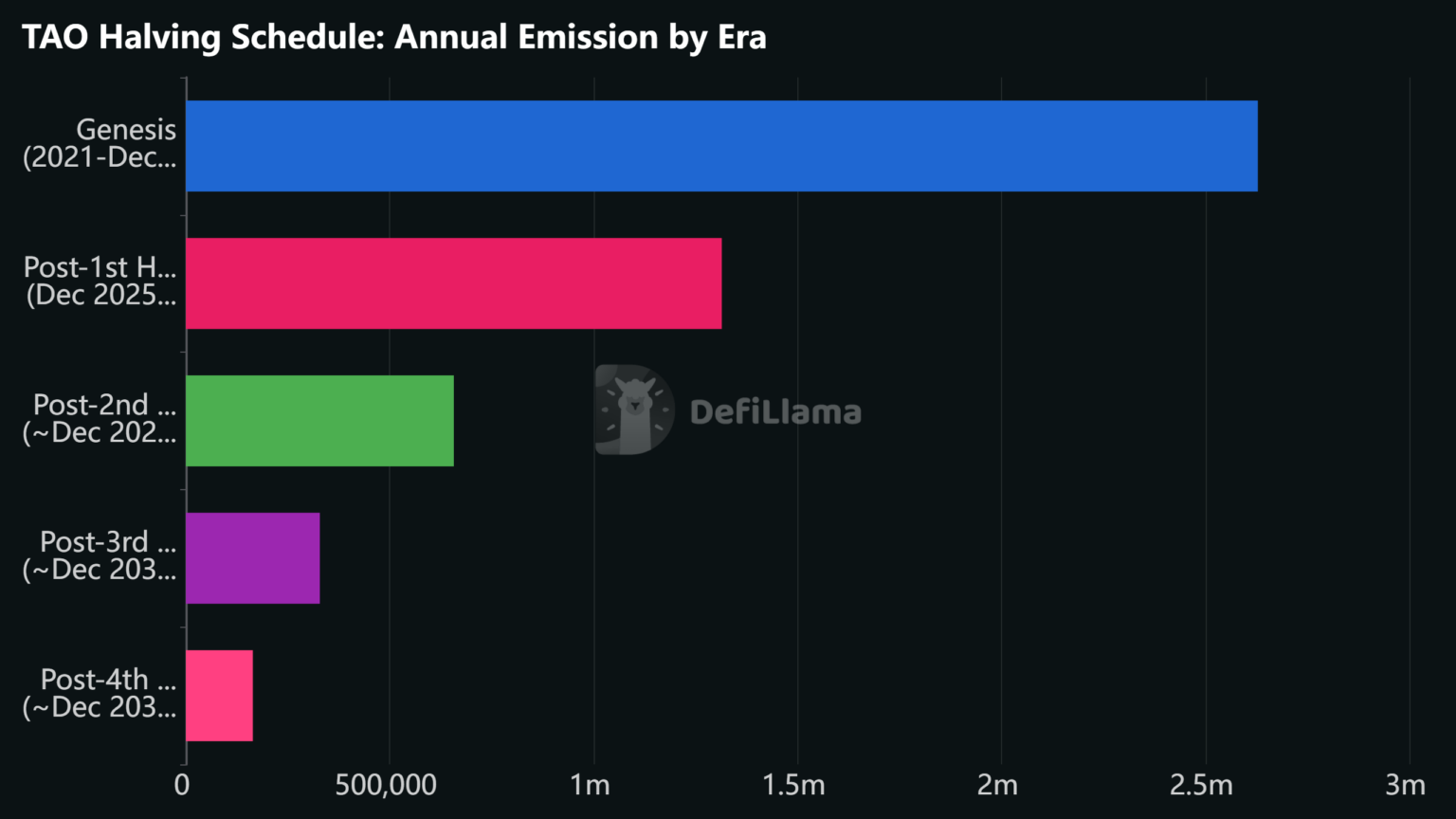

TAO is Bittensor’s native token and the economic unit that powers the network. It has a fixed maximum supply of 21 million TAO, matching Bitcoin’s hard-cap supply model. That design is intentional. Bitcoin uses programmed scarcity to secure a monetary network. Bittensor uses programmed scarcity to coordinate a market for machine intelligence.

The supply schedule also borrows from Bitcoin. TAO emissions fall through halving events, which reduce the rate of new token issuance. Bittensor completed its first halving in December 2025, cutting daily emissions from about 7,200 TAO to 3,600 TAO. Grayscale flagged this reduction ahead of the event, and TAOStats now lists the next halving around December 2029, with the exact timing tied to total issuance rather than a simple calendar date.

This makes TAO’s monetary policy easy to understand. There is a fixed cap, a declining issuance rate, and a long-term scarcity curve. As of May 2026, TAOStats showed roughly 10.9 million TAO in circulation, or about 52% of the full 21 million supply.

Bittensor adds one important twist: recycling. TAO used for subnet registration and related network activity can be burned back into the unissued supply. TAOStats notes that this can lengthen the halving timeline because the protocol uses total issued supply to determine when halvings occur.

The 2025 dTAO upgrade also changed how emissions move through the network. Before dTAO, subnet rewards depended more heavily on root network allocation. After dTAO, every subnet has its own Alpha token, and emissions are increasingly shaped by TAO staking flows into subnet markets. Bittensor documentation describes the current system as flow-based emissions, or Taoflow, where capital flows help determine which subnets receive more rewards.

That is the core Bitcoin parallel and the core difference. Bitcoin rewards hashpower. Bittensor rewards machine intelligence. TAO keeps Bitcoin’s scarcity logic, but applies it to miners, validators, subnets, and AI markets.

Subnets are the core operating layer of Bittensor. Each subnet is a specialized market for a specific type of machine intelligence or digital service. One subnet may focus on inference. Another may focus on training, data, agents, prediction markets, or compute. Therefore, the broader Bittensor network provides the shared incentive system, while each subnet defines what work matters and how miners get evaluated.

The structure is simple at a high level. A subnet owner registers a subnet on Bittensor. Miners then join that subnet to produce outputs. Validators test those outputs, score their quality, and submit weights. Yuma Consensus turns those scores into reward signals. TAO emissions then flow toward the subnet participants that perform best.

As of May 2026, TAOStats showed 128 active subnets, with each subnet listed by emissions, ownership, registration data, immunity status, and recycle volume. CoinGecko’s April 2026 subnet review also described 128 active subnets, with possible expansion to 256 later in 2026.

Subnets compete for emissions. That competition became more market-driven after dTAO. Under the post-dTAO model, each active subnet has its own Alpha token, and emissions increasingly depend on TAO staking flows into subnet markets. Bittensor’s documentation describes this as a flow-based emissions system, where validator, miner, and staker rewards come through subnet-specific allocation mechanics.

This is why subnets matter. They turn Bittensor from one AI network into a portfolio of competing AI markets. Additionally, the strongest subnets can attract miners, validators, stake, emissions, users, and eventually revenue. The weakest subnets risk losing attention as capital and emissions move elsewhere.

Dynamic TAO, or dTAO, turned Bittensor from a mostly root-directed emissions system into a market-driven subnet economy. More importantly, it changed who decides where TAO flows.

Before dTAO, emission allocation depended more heavily on the root network. High-stake validators and root-level voting influenced which subnets received rewards. That gave Bittensor a working coordination model, but it also created a bottleneck. In practice, subnet funding depended on a relatively narrow allocation process, not a broad market signal from TAO holders.

That changed in February 2025. After the dTAO upgrade, each subnet received its own subnet-specific token, usually called an Alpha token. TAOStats describes Alpha as the generic name for subnet tokens, with each subnet having its own staking token after the dTAO launch.

As a result, Bittensor moved into a clear before-and-after era. Before dTAO, the network looked more like one system allocating rewards from the top. After dTAO, it became a network of competing subnet markets. TAO holders could stake into specific subnets, gain exposure to their Alpha tokens, and express conviction in the AI markets they believed could attract miners, validators, usage, and future emissions.

That is why dTAO mattered. It created price discovery at the subnet level. Instead of treating all subnet activity as one broad category, the market could begin to separate strong subnets from weak ones. For example, a subnet with real demand, credible builders, strong validator participation, and useful AI output could attract more TAO flows. By contrast, a weaker subnet could lose attention, liquidity, and emissions.

The model also kept evolving after launch. By November 2025, Bittensor documentation says the network had transitioned to a flow-based emissions model known as Taoflow. Under that system, subnet emissions depend on net TAO inflows from staking activity rather than only token prices.

Conviction locks add another layer. They allow stakers to signal longer-term commitment rather than short-term rotation. In practice, this gives the network a way to separate fast speculative flows from deeper conviction in a subnet’s future. This matters because Alpha tokens can be volatile, and shallow liquidity can distort short-term signals.

By 2026, dTAO had become the center of the Bittensor investment case. CoinGecko reported that the network supported 128 active subnets and that Alpha token market capitalization reached about $1.12 billion by March 2026, equal to roughly 27% of TAO’s own market cap.

Still, the upgrade did not remove risk. It introduced new ones, including Alpha volatility, subnet speculation, liquidity fragmentation, and reflexive staking flows. Even so, it made Bittensor more dynamic. TAO became the base asset for a live market of AI subnets, while Alpha tokens became the mechanism for choosing where network incentives should concentrate.

The best way to understand Bittensor in 2026 is to look at its subnets. This is where the network moves from theory to execution. Each subnet targets a specific AI market, competes for miners and validators, and tries to prove that TAO emissions can fund useful machine intelligence rather than empty activity.

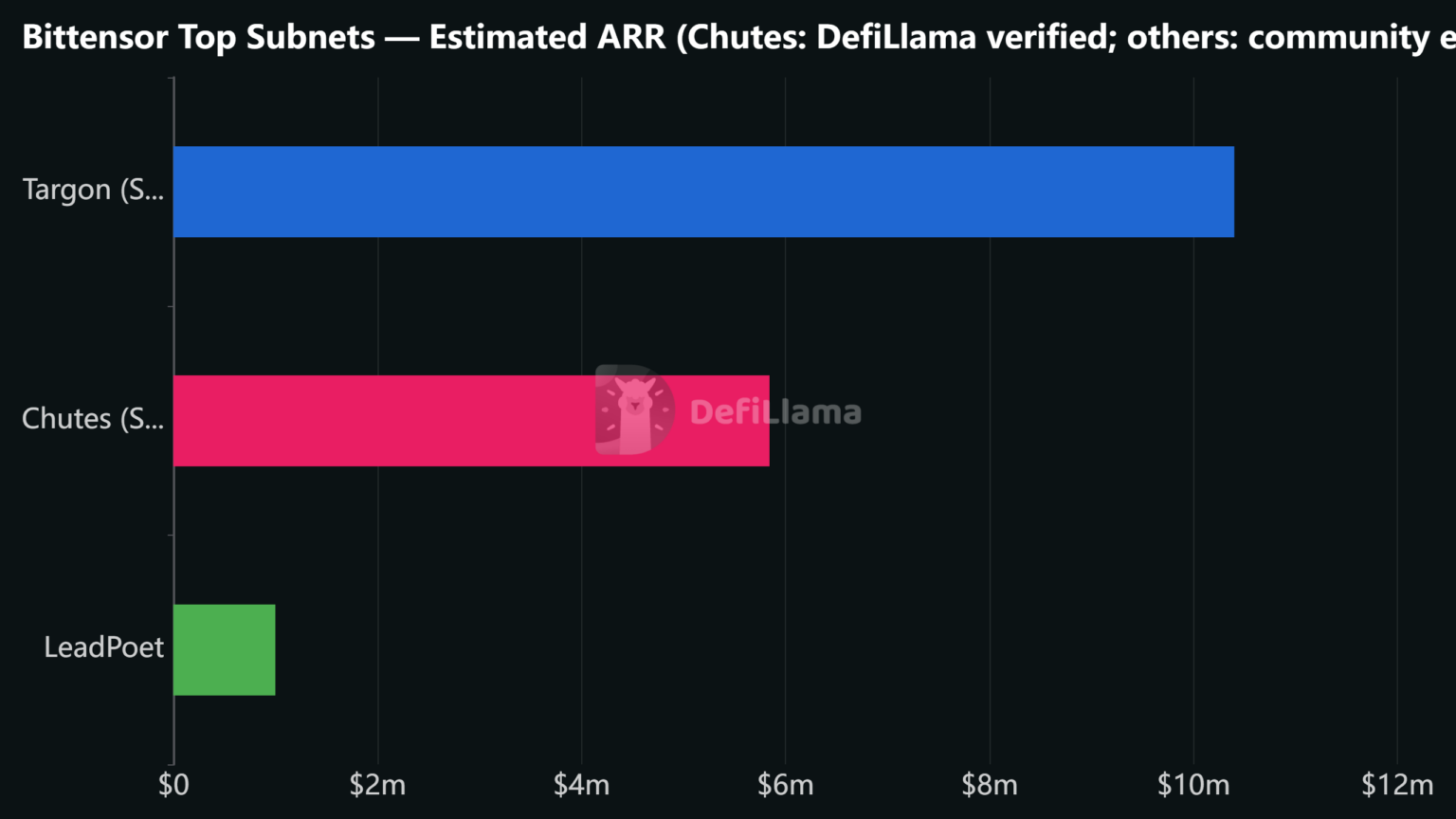

First, Templar, or SN3, is the clearest proof point so far. It focuses on distributed training and became the subnet behind Covenant-72B, a 72-billion-parameter model trained through a globally distributed, permissionless pre-training run. The Covenant-72B paper says the model trained on about 1.1 trillion tokens and performed competitively with centralized models trained on similar or higher compute budgets. That matters because it shows subnet coordination can produce foundation-model work, not just reward small inference tasks.

Next, Chutes, or SN64, targets serverless GPU inference. Its pitch is straightforward: give developers access to open-source AI models through scalable, API-style infrastructure without depending fully on centralized cloud providers. Chutes describes its platform as serverless AI compute for open-source models, including LLM, image, speech, and video workloads. This matters because inference is where AI moves from research to user-facing demand.

Meanwhile, Lium, or SN51, focuses on the data and compute layer. It positions itself around decentralized GPU infrastructure for training and inference, which makes it part of Bittensor’s attempt to turn scattered compute supply into useful AI capacity. Its traction matters because Bittensor needs more than model outputs. It also needs reliable infrastructure around data, compute, and execution if subnets are going to serve real users.

Alongside that, Gradients is another important subnet category because it targets model-training workflows rather than simple output generation. In plain terms, it sits closer to the machinery of AI improvement. That makes it relevant for builders watching whether Bittensor can support deeper model development, not only inference markets. However, its value will depend on validator quality, miner performance, and whether the subnet can show sustained usefulness beyond emissions.

Finally, Sportstensor shows the other side of the network: specialized intelligence markets. Instead of training foundation models or serving inference, it applies Bittensor-style incentives to sports prediction and information discovery. That matters because it demonstrates the subnet model’s flexibility. Bittensor can host technical AI infrastructure, but it can also host narrower markets where participants compete to produce better signals.

Together, these subnets show how broad the Bittensor economy has become. Still, they do not all carry the same weight. Templar has the cleanest headline because Covenant-72B gives Bittensor a hard proof point. Chutes has one of the clearest product-market bridges because developers already understand serverless inference. Lium and Gradients point toward deeper infrastructure. Sportstensor shows that subnet markets can stretch into prediction and domain-specific intelligence.

Institutional interest in Bittensor has grown, but it still needs to be separated from actual institutional usage of the network.

Grayscale is the clearest example. Its Decentralized AI Fund gives accredited investors exposure to a basket of AI-linked crypto assets, including Bittensor. Grayscale describes the fund as an investment vehicle tied to native tokens of decentralized AI protocols, not as direct usage of those networks. In 2024, Grayscale also launched the Grayscale Bittensor Trust, a single-asset product holding TAO for eligible investors. By 2026, Grayscale’s Bittensor Trust had public trading infrastructure under the ticker GTAO, and its S-1/A filing described the Trust as a Delaware statutory trust that holds TAO.

DCG is the other major institutional name around Bittensor. Therefore, the Wall Street Journal reported in 2024 that DCG had accumulated more than $100 million in TAO and that Barry Silbert launched Yuma to support entrepreneurs building on Bittensor. Yuma later expanded into subnet-focused asset management, with The Block reporting in March 2026 that subnet tokens had reached a record 27% of TAO’s market capitalization.

NVIDIA’s role is more indirect. Bittensor benefits from the broader AI compute narrative, and NVIDIA CEO Jensen Huang’s comments around decentralized training milestones helped market attention around TAO in 2026. However, as of May 2026, there is no strong public evidence that NVIDIA itself uses Bittensor in production or holds TAO through a verified “Digital Currency Fund” structure. Treat NVIDIA as a narrative and infrastructure reference point, not confirmed network adoption.

ETF speculation is also active. Grayscale’s amended S-1 for the Bittensor Trust creates a clearer path toward broader public-market access, but it does not equal ETF approval. The filing shows product ambition. It does not prove regulatory certainty or institutional demand at scale.

That distinction matters. Bittensor has institutional exposure through funds, trusts, staking infrastructure, and DCG-linked ecosystem vehicles. What remains less proven is institutional usage of Bittensor subnets for live AI workloads. Until that changes, the institutional case for TAO is still mostly financial exposure, not enterprise adoption.

Bittensor has one of the strongest narratives in crypto AI, but the risks are not minor. The biggest criticism is that the network can look circular: TAO emissions reward miners, validators, subnet owners, and stakers; those rewards attract more capital; that capital then chases more emissions. If outside demand does not grow, the system risks becoming an incentive loop rather than a productive AI economy.

That is the core of the Ponzi allegation. It does not mean Bittensor is automatically a Ponzi scheme. Additonally, a real Ponzi requires deceptive promises, centralized fraud, and payouts funded by new entrants rather than productive activity. Bittensor is open-source, market-based, and transparent on-chain. Still, the criticism matters because emissions alone do not prove value. The network must show that subnets can produce useful AI services, attract paying users, and generate demand beyond TAO speculation.

Miner-validator gaming is the second major risk. Bittensor depends on validators to score miner outputs honestly and accurately. If miners learn how to optimize for validator tests rather than real usefulness, emissions can reward gaming instead of intelligence. Likewise, if validators collude, run weak evaluation methods, or favor familiar miners, subnet quality can degrade fast. Yuma Consensus can aggregate scores, but it cannot magically guarantee good judgment.

In addition, subnet quality variance adds another problem. Bittensor has more than 100 active subnets, but they are not equal. Some target real infrastructure, such as distributed training, inference, data, or prediction markets. Others may remain experimental, thinly used, or mostly incentive-driven. As a result, weak subnets can still attract attention before they prove durable value, especially in a market where emissions create financial rewards.

There is also concentration risk around Yuma Rao and other large ecosystem actors. Barry Silbert’s Yuma has helped build, fund, and promote Bittensor activity, but influence can cut both ways. If too much stake, infrastructure, subnet ownership, or narrative control concentrates around a small group, Bittensor’s decentralization story becomes harder to defend. For that reason, the network needs open competition, not just influential backers.

Regulatory uncertainty remains unresolved as well. TAO, Alpha tokens, staking products, subnet assets, and AI marketplaces may face different treatment across jurisdictions. Regulators could examine whether certain products resemble securities, whether staking yields require disclosure, or whether AI-related outputs create compliance obligations.

Ultimately, the honest view is this: Bittensor is not proven because it has emissions, subnets, or a strong token chart. It becomes proven only if useful AI work creates demand outside the reward loop. That is the line readers should watch.

Getting started with TAO has four steps: buy the token, move it to a supported wallet, choose how to stake, then use TAOStats to track validators and subnets.

First, buy TAO on a centralized exchange that supports it in your region. Major TAO markets have appeared on platforms such as Binance, Kraken, MEXC, Gate.io, Bitget, KuCoin, and others, though availability depends on country rules and exchange listings. CoinMarketCap and Messari both track active TAO trading markets, while Binance lists live TAO price and trading data for supported users.

Second, move TAO off the exchange if you want self-custody or staking control. Bittensor’s wallet page lists TAO.com Wallet, Nova Wallet, SubWallet, and Polkadot.js among supported options. TAO.com Wallet and Nova Wallet are better suited for everyday use. Polkadot.js is more technical and better suited for advanced users who already understand Substrate-style wallets. Bittensor also supports Ledger hardware wallets for users who want cold-storage security.

Third, decide whether you want to stake. In Bittensor, staking usually means delegation. You delegate TAO to a validator, and that validator’s stake helps determine its consensus power and share of emissions. After the validator takes its fee, remaining rewards are distributed back to delegators based on their stake. Bittensor’s official documentation says TAO holders can stake any amount to a validator, while TAOStats provides staking interfaces and validator data for users who want to compare options.

Fourth, explore subnets before touching Alpha exposure. TAOStats is the main Bittensor dashboard for subnet discovery, staking, portfolio tracking, validator analytics, and historical on-chain data. Use it to compare subnet emissions, validator activity, yield estimates, and Alpha markets before making decisions.

The practical rule is simple: buy on a reputable exchange, withdraw to a supported wallet, start with validator delegation if you are new, and study subnets before taking higher-risk Alpha exposure. Staking can generate rewards, but it also carries validator risk, liquidity risk, slippage risk, and opportunity cost.

For exchange-by-exchange instructions, read NEW: How to Buy TAO. For delegation, validators, subnet staking, and Alpha exposure, read NEW: How to Stake TAO in Pillar 2.

Bittensor vs Other AI Crypto such as Render, Akash, and Fetch.ai all sit inside the AI crypto category, but they do not solve the same problem. TAO focuses on markets for machine intelligence. However, Render focuses on GPU rendering and compute. Akash focuses on decentralized cloud infrastructure. In addition, Fetch.ai, now part of the Artificial Superintelligence Alliance branding, focuses on autonomous agents and agent-based coordination. Fetch.ai’s own merger guide said self-custodied FET on mainnet would convert to ASI once the network upgrade completed.

Bittensor vs Render vs Akash vs Fetch.ai

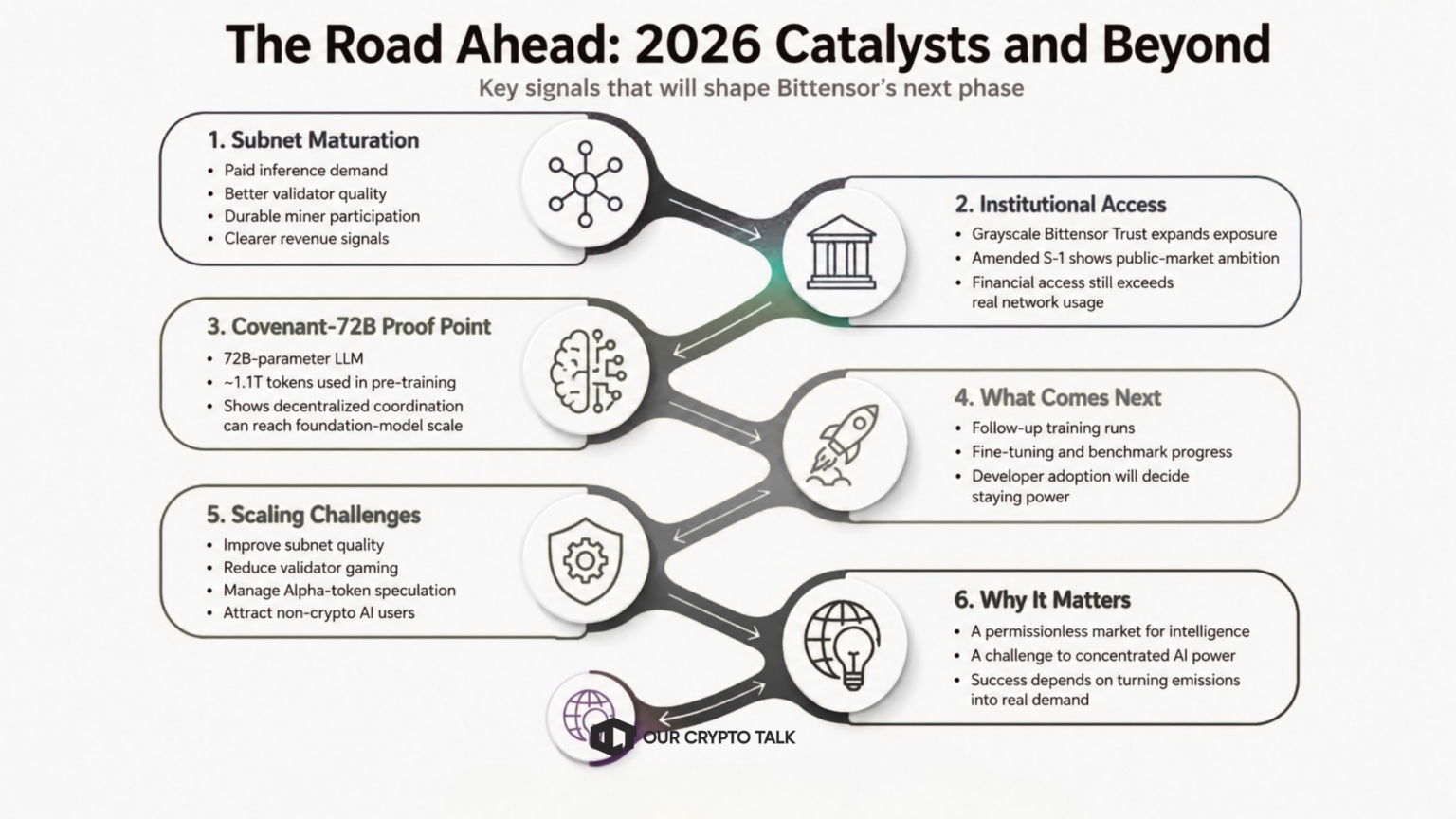

Bittensor’s next phase will depend less on narrative and more on execution. The network already has the AI story, the fixed-supply token model, the subnet economy, and the post-halving scarcity setup. In 2026, the real question is whether subnets can mature into useful infrastructure with users outside the TAO reward loop.

Subnet maturation is the first catalyst. Stronger subnets need to show paid inference demand, better validator quality, durable miner participation, and cleaner revenue signals. Chutes-style inference, Templar-style distributed training, and data-focused subnets give Bittensor credible directions, but the market will need proof that activity can survive beyond emissions.

The second catalyst is institutional access. Grayscale’s Bittensor Trust gives investors a regulated wrapper for TAO exposure, and the amended S-1 shows continued public-market ambition. That still does not mean ETF approval is guaranteed. It means TAO has moved from a purely crypto-native asset into the institutional product pipeline. The gap between financial exposure and real enterprise usage remains important. For readers comparing TAO’s 2026 upside case against other high-momentum crypto assets, see our full breakdown: TAO vs HYPE: Which Crypto Can Move Faster in 2026?

Covenant-72B is the third signal to watch. The March 2026 paper described it as a 72-billion-parameter LLM trained through open, permissionless, globally distributed participation, with about 1.1 trillion tokens used in pre-training. The model matters because it gives Bittensor a concrete proof point for decentralized coordination at foundation-model scale. Follow-up runs, fine-tuning, benchmarks, and developer adoption will decide whether it becomes a milestone or a one-off headline.

Scaling will be the hard part. In addition, Bittensor must improve subnet quality, reduce validator gaming, manage Alpha-token speculation, expand useful capacity, and attract non-crypto AI users. It also needs clearer enterprise signals, not just token products and ecosystem funds.

That is why Bittensor matters. It is not simply another AI coin chasing the sector trend. It is an attempt to build a permissionless market for intelligence at a time when AI power is concentrating inside a few companies. If Bittensor can turn emissions into useful work, and useful work into real demand, it becomes one of crypto’s most important experiments.

This article is for educational purposes only and does not constitute financial advice.

Subscribe to OurCryptoTalk for deep-dive crypto analysis

Crypto Projects Shut Down 2026: 10 Failures, $87M Lost

AI Needs Trusted Data. Can The DATA Foundation Deliver?

Crypto Bridges & DEX Aggregators in 2026: The Full Landscape

Ondo Perps vs Hyperliquid: Stock Collateral vs Speed

Crypto Projects Shut Down 2026: 10 Failures, $87M Lost

AI Needs Trusted Data. Can The DATA Foundation Deliver?

Crypto Bridges & DEX Aggregators in 2026: The Full Landscape

Ondo Perps vs Hyperliquid: Stock Collateral vs Speed