Is Bittensor a Ponzi scheme? Explore the Bittensor Ponzi debate, tokenomics, revenue gap, and whether AI can sustain long-term growth.

Author: Chirag Sharma

The crypto market thrives on narratives, but some narratives demand deeper scrutiny than others. One of the most debated topics in 2026 is whether Bittensor, one of the most ambitious AI-crypto projects, operates like a Ponzi scheme or represents a legitimate technological breakthrough.

The term “Bittensor Ponzi” has gained traction following criticism from prominent analysts who argue that the protocol’s economics rely heavily on token emissions rather than real revenue. At the same time, supporters claim Bittensor is simply in its early growth phase, similar to Bitcoin or Ethereum in their formative years.

So what is the truth?

To answer this properly, we need to separate facts from narratives and examine how Bittensor actually works, where the criticism comes from, and whether the Ponzi label holds up under scrutiny.

Before addressing whether Bittensor is a Ponzi, it is important to understand what the protocol is trying to achieve. Bittensor is a decentralized network designed to coordinate artificial intelligence development across multiple participants.

Instead of relying on centralized AI companies, Bittensor allows miners, validators, and subnet operators to contribute compute, models, and services. These participants are rewarded in TAO tokens based on the value they provide to the network.

The architecture revolves around subnets, which are specialized environments where different AI tasks are performed. As of 2026, there are more than 100 active subnets, each focused on areas such as inference, training, data processing, or specific enterprise use cases.

The system is designed to create an open marketplace for intelligence, where contributors are incentivized through token rewards. This model is fundamentally different from traditional AI companies that rely on centralized ownership and closed systems.

However, this structure also introduces complexity, especially when it comes to evaluating its economic sustainability.

The argument that Bittensor resembles a Ponzi scheme does not come from nowhere. It is rooted in the relationship between token emissions and actual revenue generated by the network.

Following the December 2025 halving, Bittensor reduced its daily emissions from approximately 7,200 TAO to around 3,600 TAO. At current market prices, this translates to hundreds of millions of dollars in annualized token issuance.

In contrast, estimates of real external revenue generated by the network range between $3 million and $15 million annually. Even optimistic estimates place revenue significantly below emission levels.

This creates a clear imbalance.

The network distributes far more value through token emissions than it generates through actual usage. Critics argue that this resembles a Ponzi-like structure, where new token issuance sustains the system rather than organic demand.

Several key concerns emerge from this argument:

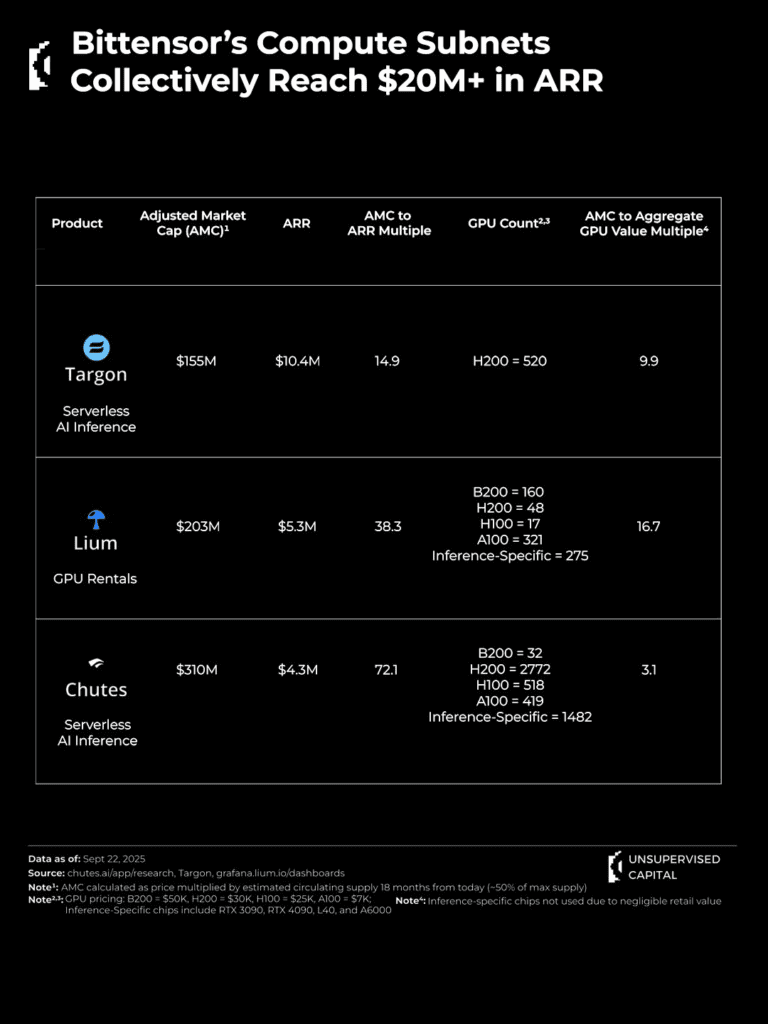

One commonly cited example is the Chutes subnet, which reportedly captures a large portion of emissions while generating only a fraction of that value in actual revenue. This highlights the gap between subsidy-driven activity and real economic demand.

Despite these concerns, labeling Bittensor as a Ponzi scheme is not entirely accurate. A traditional Ponzi scheme involves a centralized operator who secretly uses new investor funds to pay earlier participants, with no underlying business or transparency.

Bittensor does not fit this definition. The protocol is fully on-chain, transparent, and auditable. All emissions, rewards, and transactions can be verified publicly. There is no hidden operator controlling payouts, and participants are aware of how the system distributes incentives.

More importantly, there is real activity taking place within the network. Subnets are actively processing AI workloads, handling API requests, and building infrastructure for decentralized intelligence. While much of this activity is subsidized, it still represents genuine usage rather than purely fabricated demand.

This distinction is critical.

Bittensor may have economic inefficiencies, but it is not a fraudulent system designed to deceive participants. It is an experimental model attempting to bootstrap a new category of decentralized infrastructure.

The more accurate way to frame the Bittensor Ponzi debate is not whether it is a scam, but whether its current economic model is sustainable.

Like many early crypto networks, Bittensor relies heavily on token emissions to incentivize participation. This is similar to how Bitcoin used block rewards or how Ethereum funded early network growth.

However, the scale of the imbalance in Bittensor raises legitimate concerns.

A large portion of the network’s activity is effectively subsidized, meaning users are benefiting from artificially low costs supported by token emissions. For example, certain AI services offered through subnets appear cheaper than centralized alternatives, but this pricing is not sustainable without continued subsidies.

This leads to a critical question.

What happens when subsidies decline or when token demand weakens?

If the network cannot generate sufficient external revenue to replace emissions, it risks entering a cycle where value extraction outweighs value creation. In such a scenario, token holders may bear the cost while operators continue to benefit.

This dynamic is what critics refer to when they use the term “ponzinomics.”

Despite the criticisms, there is a strong and vocal community that believes Bittensor represents the future of decentralized AI.

Their argument is based on the idea that early-stage networks always look inefficient before achieving scale. Bitcoin, in its early years, had minimal transaction volume relative to its block rewards. Ethereum went through similar phases before DeFi and NFTs drove real usage.

Supporters highlight several key points:

Recent updates to the protocol, such as changes to emission distribution based on staking inflows, aim to better align incentives with actual demand. These adjustments suggest that the system is evolving rather than remaining static.

There is also a broader philosophical argument.

Decentralized AI offers benefits that centralized systems cannot easily replicate, including censorship resistance, open access, and global collaboration. These features may justify higher costs in certain use cases, especially where trust and transparency are critical.

While the long-term vision is compelling, the risks cannot be ignored.

The biggest concern is that decentralized AI may struggle to compete with centralized providers on efficiency, latency, and cost. Large AI companies benefit from economies of scale that decentralized networks find difficult to match.

Additionally, the current incentive structure may create misaligned priorities.

Subnet operators are incentivized to maximize rewards, which may not always align with creating sustainable or high-quality services. If emissions remain the primary driver of participation, the network could face challenges in transitioning to a revenue-driven model.

Another risk is market perception.

If the narrative around “Bittensor Ponzi” continues to spread, it could impact investor confidence and reduce demand for the token. In crypto, perception often plays a significant role in determining outcomes.

So, is Bittensor a Ponzi scheme? The answer is no, but the concerns are not without merit.

Bittensor is a transparent, decentralized protocol with real activity and a clear technological vision. It does not fit the definition of a Ponzi scheme, as there is no hidden operator or fraudulent structure.

However, its current economic model relies heavily on token emissions, creating a dependency on continued demand and growth. This makes it a high-risk, high-reward experiment rather than a proven system.

The term “Bittensor Ponzi” oversimplifies a complex situation. A more accurate description would be that Bittensor is in a subsidy-driven growth phase, where long-term sustainability has yet to be fully demonstrated.

The next 12 to 24 months will be critical.

If the network can convert subsidized activity into real revenue and demand, it could become a foundational layer for decentralized AI. If not, the concerns raised by critics may prove justified.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.