dTAO replaced Bittensor's validator voting with alpha token markets. Learn how emissions, staking, and subnet pricing work one year after the February 2025 launch.

Author: Kritika Gupta

Dynamic TAO, or dTAO, is the February 2025 Bittensor upgrade that replaced validator-controlled emission voting with an open market system built around subnet-specific alpha tokens. Before dTAO, a small group of root network validators decided which Bittensor subnets received the largest share of daily TAO emissions. After the upgrade, the market took over that role. Every subnet now issues its own alpha token, which trades against TAO inside an automated market maker (AMM) liquidity pool. An AMM is an on-chain system that prices assets automatically through supply and demand. When users stake TAO into a subnet, they buy that subnet’s alpha token. The alpha price then determines the subnet’s share of network emissions. Higher demand for a subnet leads to a higher alpha price and a larger share of daily TAO rewards.

Key facts

The system turned Bittensor into a market-driven AI economy where capital allocation happens through real-time price discovery instead of committee voting.

Parent guide: Bittensor (TAO) Guide

Before dTAO launched in February 2025, Bittensor used a governance system centered around the root subnet, also known as SN0. Roughly 64 validators with large amounts of root stake voted on how the network distributed daily TAO emissions across subnets. In theory, the system rewarded the best-performing AI networks. In practice, however, it created growing structural problems as Bittensor expanded.

The first issue was scale.

As the Bittensor subnet ecosystem grew, the validator layer struggled to keep up. A relatively small group of validators suddenly had to evaluate dozens, then hundreds, of competing subnets. As a result, emission allocation became a bottleneck. Decision-making slowed, and smaller subnets struggled to gain attention regardless of product quality.

The second issue was conflict of interest.

Many validators also operated subnets or held economic exposure to them. Because of that, they had strong incentives to favor their own projects during emission voting. Over time, subnet founders increasingly focused on building relationships with validators instead of improving products or attracting users. Capital allocation became political.

The third issue was council fatigue.

A small group controlled a large share of network emissions, but participation quality varied widely. Some validators actively shaped emissions. Others voted passively or followed existing power structures. Gradually, the system started resembling a closed council rather than an open market.

The underlying flaw was simple.

Human coordination struggled to scale alongside a rapidly growing decentralized AI network. Therefore, dTAO emerged as Bittensor’s answer to that problem. Instead of asking validators to decide which subnets deserved emissions, the protocol shifted that responsibility to markets. Alpha token demand became the new signal.

dTAO replaced Bittensor’s validator-controlled emission model with a market-driven system built around alpha tokens and automated liquidity pools.

First, every subnet now issues its own alpha token. That token trades directly against TAO inside a constant-product automated market maker, or AMM. An AMM is an on-chain liquidity pool that prices assets automatically through supply and demand rather than order books.

When a user stakes TAO into a subnet, they effectively swap TAO for that subnet’s alpha token through the AMM pool. As demand rises, the subnet’s alpha price climbs relative to TAO.

That price now determines emissions.

In simple terms, the alpha market acts as a real-time voting system. Stronger demand for a subnet increases its alpha price. In turn, higher alpha prices increase that subnet’s share of daily TAO emissions.

As a result, the mechanism changed how capital flows across Bittensor. Under the old model, subnet founders needed validator support to secure emissions. Under dTAO, they need market demand. Builders now compete for liquidity, users, revenue, and long-term conviction instead of political influence inside the root network.

The easiest analogy is subnet equity. Buying alpha gives users economic exposure to a subnet’s success. If a subnet attracts real usage, generates revenue, or becomes strategically important inside the decentralized AI economy, demand for its alpha token can rise sharply.

In addition, the AMM creates continuous liquidity. Users can enter or exit subnet exposure at market prices without relying on centralized coordination.

Finally, the model behaves similarly to a bonding curve. Early buyers can accumulate alpha cheaply. If the subnet proves useful and attracts sustained demand, the alpha price appreciates, which pulls in a larger share of network emissions.

Legacy root-vote model vs dTAO market model

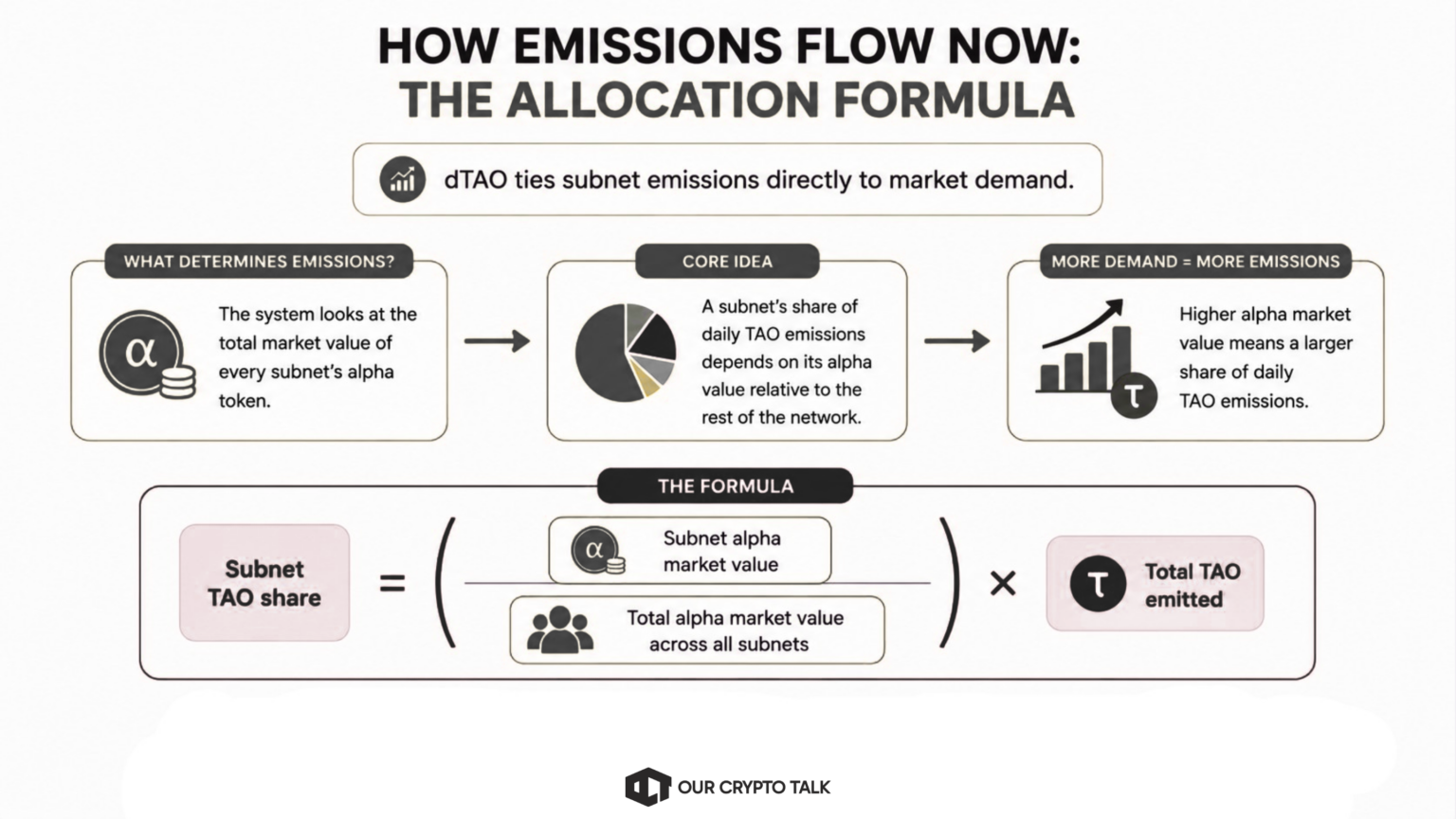

dTAO ties subnet emissions directly to market demand.

The Bittensor system looks at the total market value of every subnet’s alpha token. A subnet’s share of daily TAO emissions depends on how large its alpha value is relative to the rest of the network.

The formula is straightforward:

In practice, this means alpha price controls emissions.

If a subnet attracts more staking demand, its alpha token price rises inside the AMM pool. A higher alpha price increases that subnet’s percentage of total network value, which increases its share of TAO rewards.

After the December 2025 halving, Bittensor emits roughly 3,600 TAO per day across the network.

Here is a simple example.

Assume all subnet alpha tokens combined are worth 10,000 TAO-equivalent. One subnet controls 1,000 TAO of that value. That subnet therefore represents 10% of the total alpha market.

Because it controls 10% of network alpha value, it receives roughly 10% of daily emissions. With daily issuance near 3,600 TAO, the subnet would receive approximately 360 TAO per day. The process does not stop there.

The protocol also injects newly minted alpha back into the subnet’s liquidity pool. This mechanism helps maintain liquidity between TAO and the subnet’s alpha token. The system caps those injections to reduce runaway inflation and limit excessive dilution.

The newly emitted alpha is then distributed across subnet participants. The subnet owner receives roughly 18% of emissions. Validators receive around 41%. Miners also receive around 41%. That reward structure creates a direct economic loop.

Useful subnets attract staking demand. Higher demand pushes alpha prices higher. Higher alpha prices increase emissions. Increased emissions attract more miners, validators, and infrastructure around the subnet.

The result is a live capital allocation system where emissions constantly adjust to market conviction.

One of the biggest misconceptions about dTAO is that Bittensor fully switched to market-driven emissions overnight. In reality, that never happened.

Instead, the network introduced dTAO gradually through a parameter called tao_weight. This variable controls how much influence still belongs to the legacy root-stake system versus the new alpha-token market structure. Today, the current tao_weight sits around 0.18.

At launch in February 2025, the value was significantly higher. As a result, root validators still carried meaningful influence over emissions while alpha markets slowly gained control. The system worked more like a dial than a switch.

Over time, as tao_weight declined, subnet alpha prices became increasingly important in determining emission allocation. The protocol deliberately slowed the transition to avoid sudden liquidity shocks or violent capital rotation between subnets.

That stability mattered.

For example, a full handover on day one could have triggered extreme volatility across newly launched alpha markets. Many subnet liquidity pools were still thin during the early rollout period. Because of that, smaller pools were easier to manipulate and more vulnerable to sharp price swings.

The gradual transition gave markets time to mature. Then, around May 2025, one of the key milestones arrived when alpha-based emissions overtook emissions controlled through root stake for the first time. That marked a major structural shift inside the network.

At the same time, the change also reduced persistent sales pressure from root validators.

Under the old model, validators frequently received emissions from subnets they did not strongly support economically. In many cases, they sold those rewards immediately. As alpha markets took over, emissions increasingly flowed toward subnets with actual market demand and active staking participation.

Finally, the remaining root influence also served another purpose.

dTAO changed how TAO holders interact with the network. Under the old system, most users focused primarily on staking through the root network. After dTAO launched, staking became far more targeted. Holders now allocate capital toward individual subnets through their associated alpha tokens.

The process starts with validators.

Validators act as the operational access point into a subnet. When users stake TAO through a validator tied to a subnet, their TAO is swapped through the subnet’s AMM pool, and they receive exposure to that subnet’s alpha token.

As a result, two very different staking postures emerged.

The first is root staking.

Root staking still offers relatively stable exposure to the broader Bittensor network. However, its influence continues to decline as tao_weight falls and alpha-driven emissions gradually take over. Because of that, many holders now view root staking as the lower-volatility option rather than the network’s primary growth engine.

The second posture is subnet staking.

Unlike root staking, subnet staking gives users direct exposure to a specific alpha token and the economic performance of that subnet. If a subnet attracts real demand, usage, or revenue, the alpha token can appreciate significantly. In addition, strong subnet performance can increase emissions flowing into that ecosystem.

Naturally, the upside is higher, but so is the risk.

Alpha tokens can lose value quickly if a subnet fails to attract users or liquidity dries up. Moreover, exit liquidity depends entirely on the depth of the subnet’s TAO-alpha pool. Thin liquidity can amplify volatility during sharp market moves.

As a result, dTAO is fundamentally conviction-driven.

Holders now make active decisions about which parts of the decentralized AI economy deserve capital. The market can reward strong subnet performance aggressively, but poor allocations can still lead to permanent losses

For a broader analysis of Bittensor’s ecosystem and long-term outlook, read Bittensor Crypto Review.

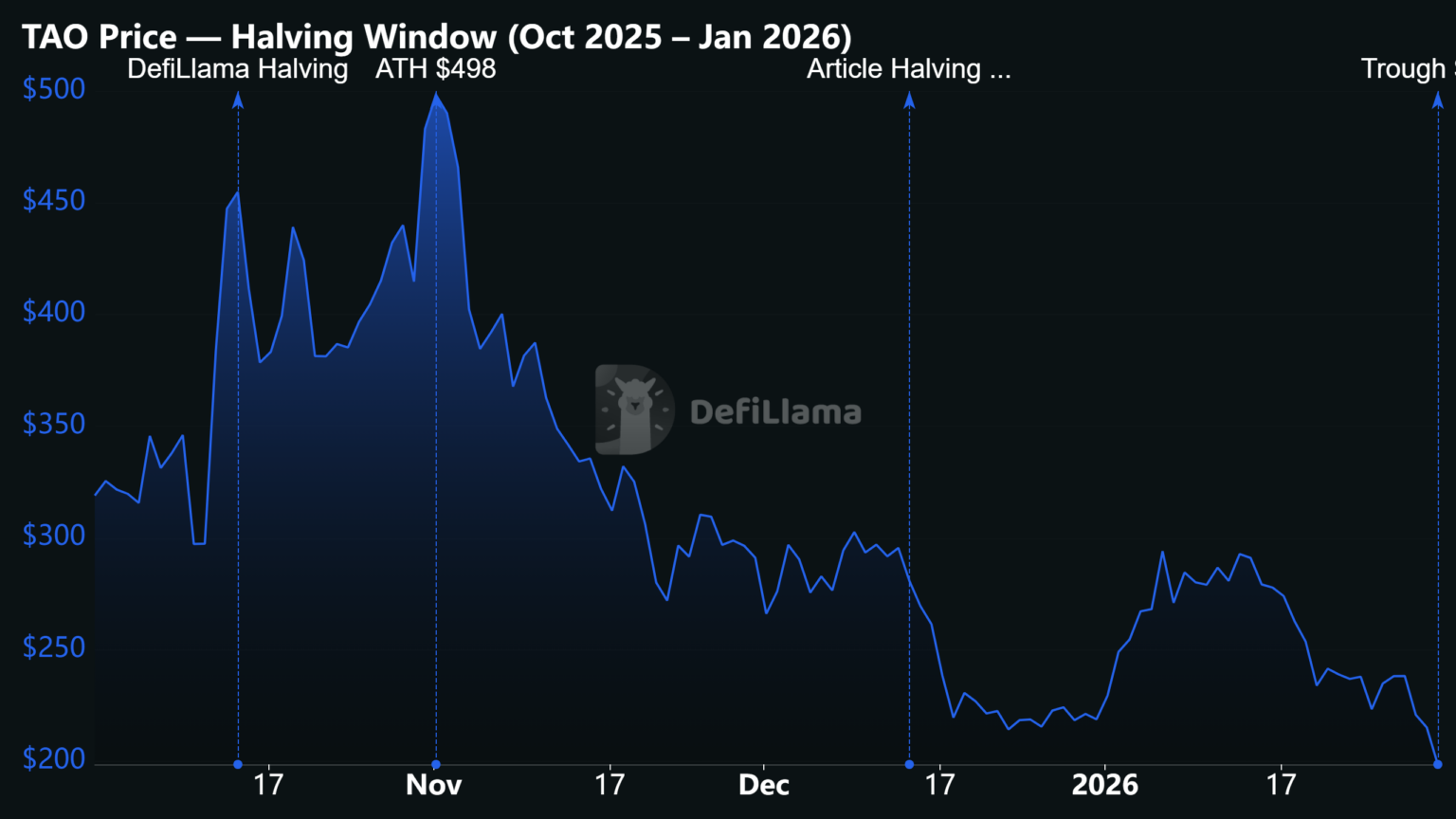

dTAO did not just change how Bittensor allocates emissions. It also changed how scarcity flows through the network. Both TAO and subnet alpha tokens follow synchronized halving schedules tied to supply thresholds. Each asset ultimately targets a maximum supply of 21 million tokens.

The first major milestone arrived on December 14, 2025. That day, Bittensor completed its first TAO halving. Daily TAO issuance dropped from roughly 7,200 TAO to around 3,600 TAO across the network.

Alpha emissions also tightened at the same time. The rate of new alpha injections flowing into subnet liquidity pools was cut in half alongside base-layer TAO issuance. That meant fewer rewards entering both the root economy and subnet-level markets simultaneously.

The result was a dual supply shock. Scarcity increased across the entire decentralized AI ecosystem, not just the TAO token itself. Subnets suddenly competed for a smaller pool of emissions while also operating with tighter alpha distribution schedules.

That shift amplified the importance of market demand under dTAO. Before the halving, weaker subnets could still survive on relatively loose emissions. After the halving, capital became far more selective. Subnets with real usage, revenue generation, or sustained staking demand gained a stronger position as emissions tightened network-wide.

The mechanism also reinforced dTAO’s core feedback loop. Higher-conviction subnets continued attracting liquidity and maintaining stronger alpha prices, while weaker projects faced faster capital outflows and declining emissions.

The post-halving environment turned Bittensor into a more competitive market for decentralized AI capital allocation.

dTAO solved one problem, but it also exposed another.

The system assumes market pricing reflects real subnet value. In practice, crypto markets often reward hype faster than utility. As a result, a rising alpha price does not automatically mean a subnet delivers meaningful AI work, sustainable revenue, or long-term demand.

That tension surfaced almost immediately after launch. Several early subnets discovered they could aggressively pump alpha prices through speculation and coordinated buying activity. Since dTAO ties emissions directly to alpha market value, those inflated prices translated into larger shares of daily TAO rewards.

The SN28 episode became one of the clearest examples.

Speculators pushed the subnet’s alpha price sharply higher despite weak evidence of real economic activity or AI output. In turn, the higher price mechanically increased emissions flowing into the subnet, which created even more attention and speculative demand.

Soon, the loop became self-reinforcing. SN281, often referred to as the “LOL-subnet,” followed a similar pattern. Traders treated the subnet more like a momentum token than productive AI infrastructure. As alpha appreciated, emissions rose, even though the subnet itself contributed little meaningful utility to the broader network.

Together, the episodes exposed a core weakness inside dTAO. Markets can allocate capital efficiently over long timeframes, but short-term crypto markets can remain deeply irrational. Under dTAO, hype itself can temporarily become an emission strategy.

Eventually, the Opentensor Foundation intervened.

Using remaining root stake influence during the transition period, validators applied pressure against manipulated alpha pools and reduced the impact of speculative subnet emissions. This intervention helped collapse several distorted alpha markets before they absorbed even larger portions of network rewards.

However, that solution introduced another contradiction. The intervention was only possible because Bittensor had not fully decentralized emissions yet. In other words, the same root influence dTAO aimed to replace became the emergency brake that stabilized the system.

That tension still exists today.

If the network eventually removes root influence entirely, future manipulative cycles may become harder to stop. On the other hand, if governance intervention remains possible, critics can argue the system never became fully market-driven in the first place. For now, Bittensor has not fully resolved that contradiction. The network is still testing where decentralization ends and protocol defense begins.

One year after launch, the strongest argument for dTAO is visible directly on-chain.

Subnets that built real products and attracted actual users generally captured stronger staking inflows, higher alpha prices, and larger emission shares. The market did not reward every subnet equally, but it increasingly rewarded measurable demand instead of validator relationships.

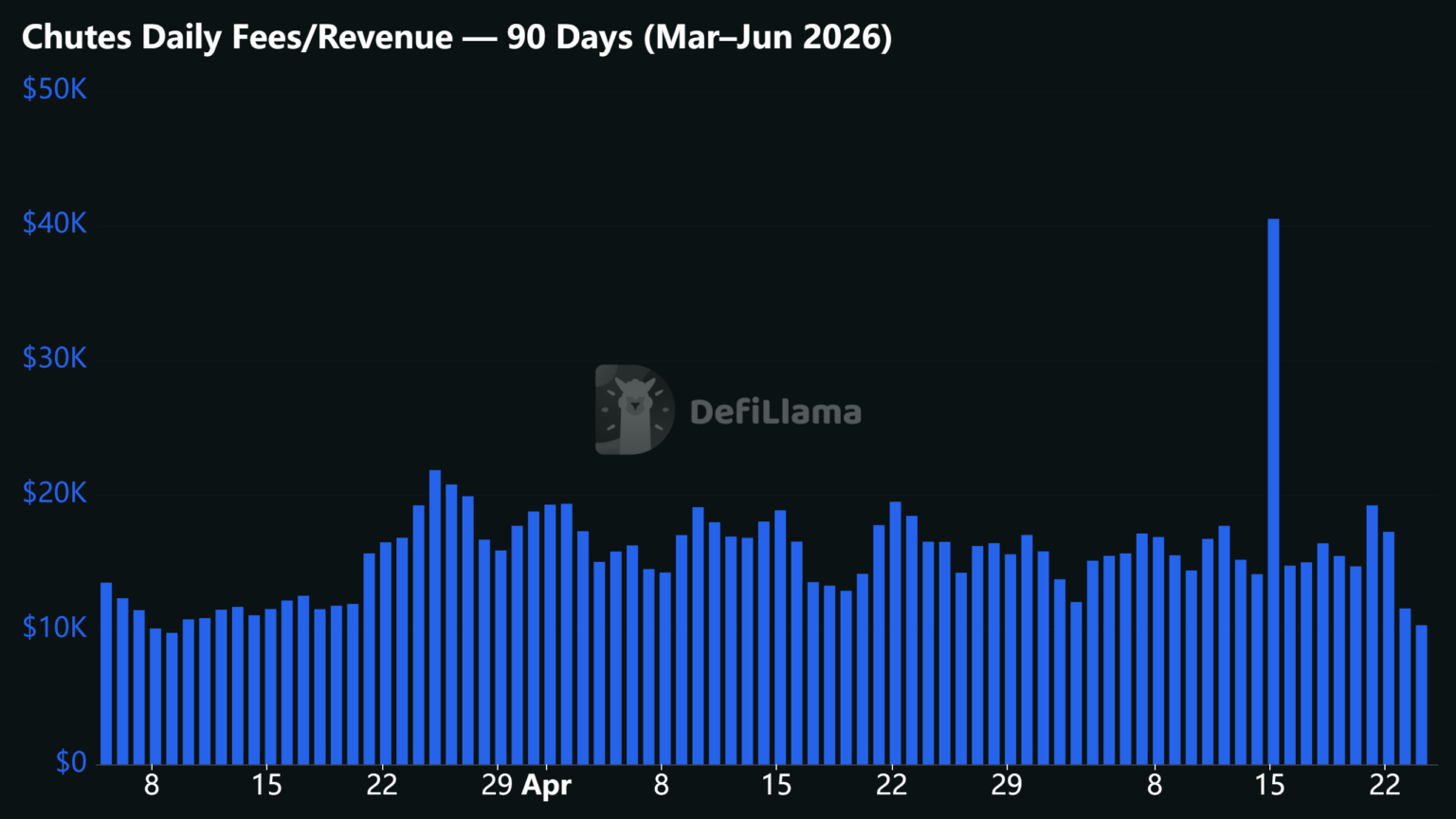

SN64, better known as Chutes, became one of the clearest examples. The subnet focused on decentralized serverless inference and compute infrastructure. As usage expanded, staking demand followed. Chutes also introduced revenue-funded alpha buybacks, which tied subnet economics more closely to real activity instead of pure speculation.

That distinction mattered. The subnet sustained high emissions because users and capital continued flowing into the ecosystem, not because validators manually favored it through governance. At the same time, weaker projects struggled to survive.

Several subnets that failed to establish product-market fit lost liquidity, saw alpha prices collapse, and eventually disappeared from the network entirely. The Tiger Alpha and KDN-1 deregistration wave in early 2026 became one of the most visible examples of the market removing underperforming projects from the emission system.

Under the old root-voting structure, weaker subnets could sometimes maintain emissions through political alignment or validator support. Under dTAO, sustained demand became harder to fake over long periods.

That self-correcting behavior is arguably the system’s biggest success. Capital now rotates toward subnets with stronger usage metrics, better infrastructure, deeper liquidity, or clearer revenue models. Emissions adjust continuously through market activity instead of periodic committee decisions.

The process is not perfectly efficient. Speculative cycles still exist, and manipulation risks remain real. But one year later, the broader pattern is difficult to ignore. Bittensor’s emission system now behaves more like an open capital market and less like a closed allocation council.

dTAO turned Bittensor into a live market for decentralized AI capital allocation.

The easiest way to observe that market is through dashboards like Taostats, which track alpha prices, subnet rankings, emission share percentages, staking flows, validator activity, and liquidity depth across the network.

Three metrics matter most. First, watch alpha price trends. Sustained appreciation backed by liquidity and network activity usually signals growing conviction around a subnet. Sharp vertical moves with thin volume often signal speculation instead of organic demand.

Second, track emission share. A subnet steadily gaining percentage share over time usually indicates persistent staking inflows and stronger market positioning. Sudden spikes followed by rapid reversals often point to unstable capital rotation.

Third, monitor liquidity and participation. Maturing subnets generally attract broader validator participation, deeper liquidity pools, more stable staking flows, and visible product usage. Strong subnets increasingly show signs of real economic activity rather than purely narrative-driven momentum.

The distinction matters. Under dTAO, markets reward attention quickly, but they also punish weak fundamentals over time. Alpha prices can collapse fast when demand disappears or liquidity dries up.

That creates both opportunity and risk for TAO holders. dTAO effectively turned every TAO holder into a voter on the future of decentralized AI infrastructure. Capital now acts as the network’s decision-making layer. Strong subnets attract emissions, liquidity, and builders. Weak subnets lose all three.

The upside can be significant, especially in a post-halving environment with tighter emissions. The risks are equally real when speculation outruns utility.

For the full network overview, read the Bittensor (TAO) Guide.

This article is for informational purposes only and does not constitute financial advice