Bittensor vs Render compared for 2026: TAO and RENDER on real usage, tokenomics, catalysts, and risk, so you can decide which AI crypto fits your portfolio.

Author: Kritika Gupta

There is no single winner in the Bittensor vs Render debate. Render is the cleaner bet for investors who want decentralized GPU compute with real, measurable usage today. It already shows traction through frames processed, node activity, and token burns tied to completed work. Bittensor is the bigger vision bet. It gives investors exposure to a decentralized market for machine intelligence, where subnets compete to produce valuable AI outputs. However, that upside comes with more complexity, more volatility, and a higher reliance on future adoption. In simple terms, choose Render if you want clearer infrastructure proof points. Choose Bittensor if you want higher-risk exposure to the coordination layer of decentralized AI.

Relative positioning across the AI crypto stack

A direct Bittensor vs Render comparison can mislead readers because the two projects do not sell the same thing. They both sit inside the AI crypto narrative, but they operate at different layers of the stack.

Render sits at the compute and infrastructure layer. It aggregates GPU power and sells it to users who need rendering capacity or AI compute. In practical terms, Render gives the market a decentralized way to access raw GPU supply. That makes it closer to the picks-and-shovels side of AI. If demand for rendering, inference, and training workloads grows, Render wants to capture that demand through job activity, node participation, and token burns.

Bittensor sits at the intelligence and coordination layer. It does not simply rent out compute. Instead, it runs a marketplace where subnets compete to produce useful machine intelligence. These subnets can focus on models, data, inference, agents, search, and other AI services. Validators score the work, and the network rewards the participants that produce the most valuable outputs. In other words, Bittensor tries to coordinate the AI economy itself.

That difference matters for investors. Render offers a more concrete infrastructure thesis with easier proof points. You can track usage, burns, nodes, and workload growth. Bittensor offers a broader but more complex thesis. You must judge subnet quality, incentive design, external demand, and whether decentralized intelligence markets can capture real value over time.

Therefore, these projects can both succeed. They can both fail. They can also trade market leadership depending on which layer investors value more in a given cycle. In fact, they may prove more complementary than competitive. A Bittensor subnet could use decentralized GPU supply, while Render could benefit from the same AI demand that strengthens Bittensor’s narrative.

So the rest of this article compares two investment theses, not two products doing the same job.

For a deeper breakdown of subnets and Bittensor’s AI market design, read our Bittensor (TAO) Guide.

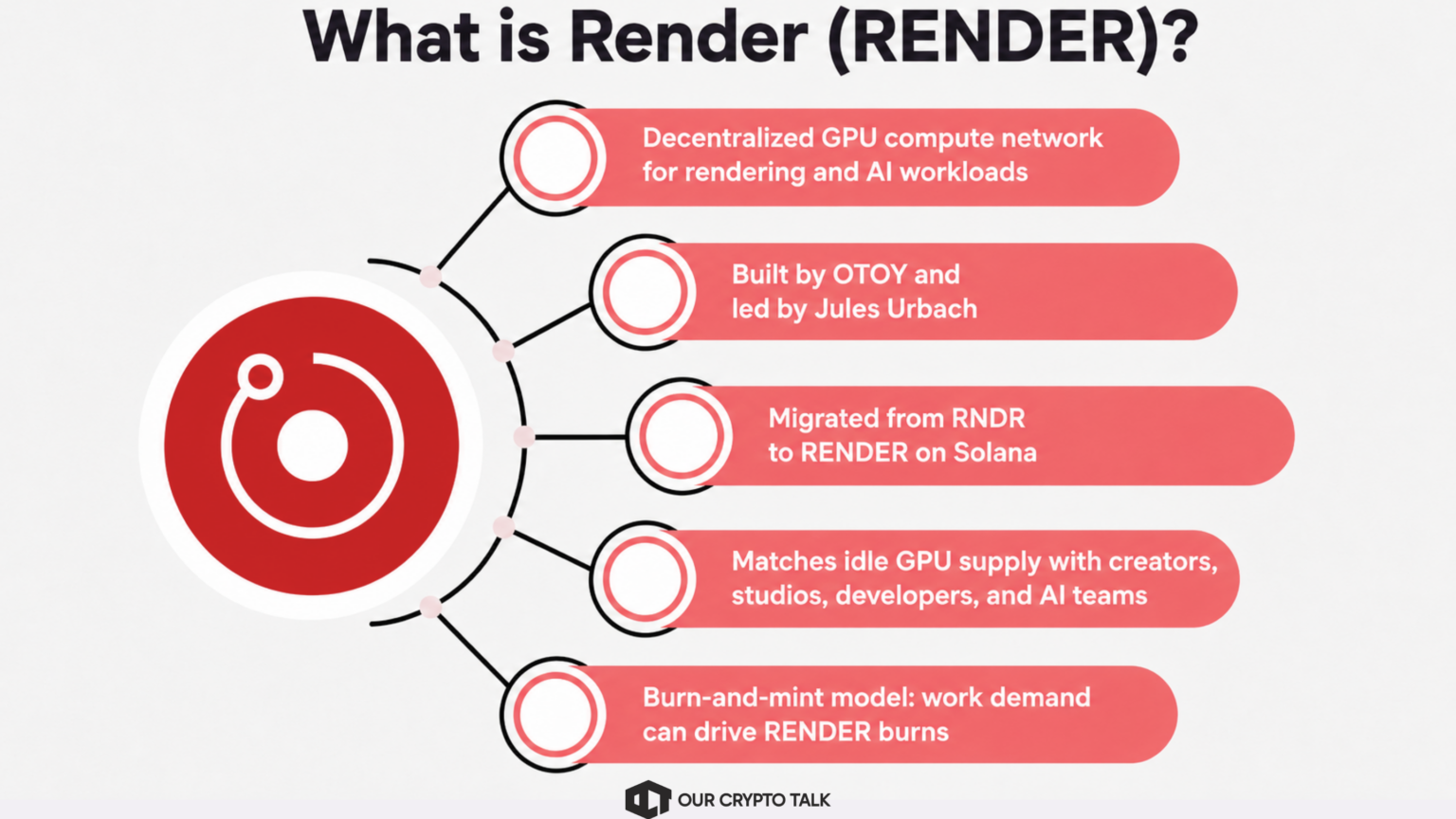

Render Network is one of the more established decentralized GPU compute projects in crypto. OTOY built it, and Jules Urbach leads the project. That background matters because OTOY has spent more than fifteen years building professional GPU rendering software through OctaneRender, a production-grade renderer used across design, VFX, film, and high-end creative workflows.

Render originally launched as RNDR before migrating to Solana as RENDER. The move gave the network faster settlement and better economics for the small, frequent transactions that job-based compute networks require. Today, Render connects idle GPU supply with users who need rendering capacity. Increasingly, it also targets AI compute through initiatives such as Dispersed AI and expanded GPU sources.

The core idea is simple. Many creators, studios, developers, and AI teams need GPU power. At the same time, many GPU owners have unused capacity. Render tries to match those two sides through a decentralized marketplace.

Its tokenomics use a burn-and-mint model. Jobs are priced in dollar terms, users pay in RENDER, and the protocol burns tokens as work gets purchased. Then, node operators receive newly minted RENDER for completing compute jobs. Therefore, real demand can directly create token burn pressure. This matters because burns rose sharply in 2025, giving investors a clearer way to track whether network usage is translating into token demand.

Render also has real enterprise and professional credibility. Its ecosystem and OTOY’s software footprint have touched major names and workflows associated with Apple, F1, and Santander. That does not make RENDER risk-free, but it gives the project more substance than a generic AI infrastructure narrative.

Still, the honest counterweight is competition. Render operates in a crowded compute market. It competes with other DePIN GPU networks, specialized AI compute projects, and hyperscale cloud providers with deep capital, mature infrastructure, and strong service guarantees. As a result, Render must keep proving that decentralized GPU supply is not only available, but also preferred for meaningful workloads.

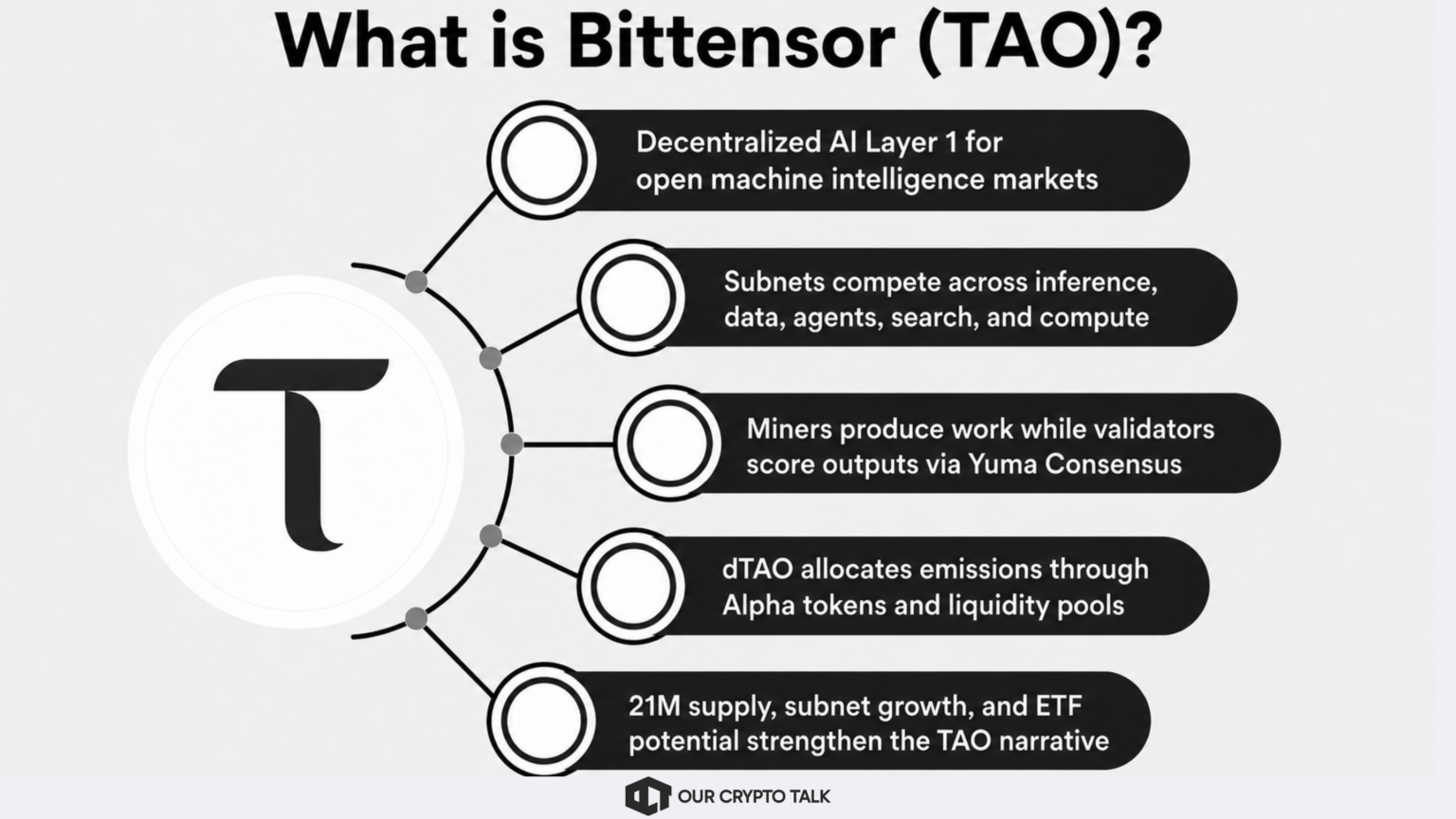

Bittensor is a decentralized Layer 1 blockchain built for AI. Instead of running one model or one application, it creates open markets where specialized subnets compete to produce useful machine intelligence.

Each subnet focuses on a specific category of AI work. Some subnets can target inference, data, model outputs, agents, search, compute, or other machine-learning services. Miners contribute the work, validators assess the output, and the network rewards the participants that deliver the most valuable results.

Yuma Consensus sits at the center of that scoring process. It helps validators judge which outputs deserve rewards. Meanwhile, dTAO changes how the network allocates emissions. Instead of relying only on validator weight setting, dTAO lets market participants signal demand across subnets through subnet-specific Alpha tokens and liquidity pools. As a result, stronger subnets can attract a larger share of TAO emissions.

That structure makes Bittensor very different from Render. Render sells decentralized GPU capacity. Bittensor tries to coordinate the market for intelligence itself.

In 2026, this has made TAO one of the leading AI crypto assets by narrative strength and market attention. Subnet growth has accelerated, and traders closely watch registration costs because rising costs often signal stronger demand to launch or compete inside the network. At the same time, Bittensor’s 21 million hard cap gives TAO a scarcity story that many AI tokens lack.

Institutional interest also gives the asset another catalyst. A possible spot ETF pathway, including trust conversion efforts and related filings, could bring new traditional capital into TAO if regulators approve those products.

Still, Bittensor remains complex. Investors need to watch subnet quality, external revenue, validator behavior, and whether dTAO allocates emissions efficiently over time.

The table below shows the clearest way to compare Bittensor vs Render. Render wins on visible usage today. Bittensor wins on the size of the vision.

How RENDER and TAO compare across thesis, tokenomics, usage, catalysts, and risks

In short, Render gives investors the cleaner infrastructure case. Bittensor gives investors the bigger coordination-layer case.

Bull case: Render has one of the strongest real-usage stories in AI crypto. The network already processes GPU work for creators, studios, and increasingly AI-related workloads. That gives investors something tangible to monitor: jobs completed, frames rendered, node activity, and token burns.

The burn-and-mint model strengthens that thesis. Users buy work through RENDER, and the protocol burns tokens when work gets purchased. Then, it mints rewards for node operators that provide compute. As demand grows, burns can offset emissions and create a cleaner value-accrual story than many AI tokens offer.

Render also has credible roots outside crypto. OTOY and Jules Urbach bring a long operating history in professional GPU rendering through OctaneRender. That matters because the project did not start as a speculative AI narrative. It started from a real software and rendering base, then expanded into decentralized GPU supply and AI compute.

In addition, Render targets a massive market. Demand for GPU compute continues to rise across rendering, inference, training, simulation, design, and media production. If decentralized supply can compete on cost, availability, or specialized workflows, Render can grow into a serious infrastructure asset.

Bear case: Render still competes in a brutal market. Other DePIN compute networks want the same AI infrastructure narrative. At the same time, hyperscale cloud providers such as AWS, Google Cloud, and Azure already offer deep liquidity, mature enterprise relationships, uptime guarantees, and massive GPU fleets.

Therefore, Render must do more than show usage. It must convert that usage into durable token demand. Frame counts and job activity matter, but investors still need to see whether burns consistently balance emissions and whether high-value AI workloads grow beyond the rendering base.

Render also carries a specific supply overhang from previously seized Alameda-linked tokens. If authorities or related entities move or sell those tokens, traders may price in short-term pressure even if the amount looks small relative to total market cap.

So the bull case rests on real usage and a vast GPU market. The bear case rests on competition, token-demand durability, and supply overhang risk.

For a broader crypto review framework, read our Bittensor crypto review.

In the Bittensor vs Render debate, Bittensor’s strongest case comes from the size of its vision.

Bull case: Bittensor leads the decentralized AI narrative in crypto. It does not pitch itself as another GPU marketplace or AI app. Instead, it aims to build an open market for machine intelligence, where subnets compete to produce useful outputs and earn emissions for the value they create.

That vision gives TAO a much larger conceptual addressable market than most AI tokens. If decentralized networks can coordinate models, data, inference, agents, search, and other AI services at scale, Bittensor could capture value from the intelligence layer itself.

The market also has real signals to track. Subnet growth shows builder activity. Rising registration costs often show demand to launch and compete inside the network. Meanwhile, dTAO gives the market a more direct role in deciding which subnets deserve emissions, rather than leaving allocation only to validator judgment.

TAO also has a tight monetary profile. Its 21 million max supply gives it a cleaner scarcity narrative than many AI crypto assets. In addition, a spot ETF approval would create a major institutional access point and could bring traditional capital into a category that remains difficult for many funds to buy directly.

Bear case: Bittensor still faces a serious external-revenue question. Critics argue that much of the current economy remains circular, with value driven by emissions, staking, subnet token speculation, and internal incentives rather than large-scale demand from non-crypto users.

The tokenomics also became more complex after dTAO. Investors now need to understand subnet Alpha tokens, liquidity pools, emission flows, validator behavior, and market signaling. That complexity can improve allocation, but it also makes the system harder to value and easier to misunderstand.

Subnet quality also varies. Some subnets may deliver real services, while others may attract capital before they prove durable demand. As a result, subnet count alone does not equal fundamentals. Investors need to track which subnets generate external usage, not just which ones attract emissions.

Validator and stake concentration remain another concern. If too much influence sits with a small group of participants, the network’s market-driven story weakens.

So the bull case rests on Bittensor becoming the coordination layer for decentralized AI. The bear case rests on circularity, complexity, uneven subnet quality, and a valuation that still prices in a vision not yet matched by external revenue.

As of mid-June 2026, Bittensor still trades as the larger asset. CoinMarketCap places TAO around the $2.3 billion market-cap range, while RENDER sits closer to the $850 million range. That puts TAO at roughly 2.5x to 3x Render’s size, depending on the source and the exact time checked.

Performance also needs context. TAO still trades far below its all-time high near $757.60, while RENDER remains far below its all-time high near $13.53. That means both assets carry recovery narratives, not clean breakout narratives. In 2026, TAO has benefited from subnet growth, dTAO attention, and ETF speculation, but it has also stayed volatile. Meanwhile, RENDER has traded as a DePIN and AI compute proxy, with price action still needing stronger proof that network usage can translate into sustained token demand.

Liquidity looks stronger for TAO in absolute terms. Recent daily volume has sat above RENDER’s, which makes sense given TAO’s larger market cap and stronger AI narrative leadership. Still, both tokens remain liquid enough for major exchange coverage and active crypto-market discussion.

The broader backdrop matters. Capital has rotated toward decentralized AI, DePIN, and compute infrastructure through 2026. That has supported both stories. Even so, momentum should not become the verdict. A hot narrative can act as a catalyst, but it does not replace usage, revenue, token demand, or sustainable network economics.

For broader TAO context, read our Bittensor price prediction.

In the Bittensor vs Render debate, render is the better bet if you want tangible infrastructure exposure with clearer proof points today. It has a simpler thesis: users need GPU compute, Render connects them with decentralized GPU supply, and network activity can translate into token burns. Investors can track frames rendered, AI workload growth, node participation, burn activity, and enterprise adoption. That makes RENDER easier to underwrite than most AI crypto assets.

However, that clarity comes with a trade-off. Render competes directly with other DePIN compute networks and with cloud giants such as AWS, Google Cloud, and Azure. Therefore, the bull case depends on more than usage. Render must prove that decentralized GPU supply can win meaningful demand and convert that demand into durable token value.

Bittensor is the better bet if you want the higher-conviction, higher-volatility wager on the decentralized AI economy itself. TAO gives investors exposure to the intelligence coordination layer, not just the infrastructure layer. If subnets become real markets for models, data, inference, agents, and other AI services, Bittensor could capture value from a much larger conceptual market.

Still, investors need to accept the risks. Bittensor remains complex. dTAO, subnet incentives, validator behavior, emissions, and Alpha tokens all require close monitoring. In addition, much of the current valuation still depends on future external revenue catching up to the scale of the vision. That makes TAO a more ambitious bet, but also a more fragile one if the narrative cools.

So the answer depends on the investor. Choose Render if you want a cleaner AI infrastructure thesis with visible usage and you can tolerate brutal compute competition. Choose Bittensor if you want higher-upside exposure to decentralized intelligence markets and you can stomach complexity, volatility, and narrative risk.

For some readers, holding both may be the rational answer. Render and Bittensor sit at different layers of the same AI stack. One targets compute supply. The other targets intelligence coordination. They can coexist, and they can compound the same broader AI crypto thesis.

None of this is financial advice. It is a framework for deciding which risk profile fits your portfolio.

The balance between Bittensor vs Render will shift based on proof points, not price targets.

For Bittensor, watch the ETF decision first. A successful spot ETF pathway would give TAO a cleaner institutional access route and could strengthen its position among AI crypto assets. However, the bigger test sits inside the network. Leading subnets need to attract real users, real demand, and external revenue beyond the internal emission economy. Investors should also track whether dTAO keeps allocating emissions toward high-quality subnets without encouraging low-activity speculation or excessive concentration.

For Render, watch enterprise AI-compute traction. The project already has a clearer usage story, but it needs more evidence that AI workloads can grow beyond traditional rendering and become a durable source of demand. Token burns also matter. If burns rise consistently against emissions, the value-accrual case becomes easier to defend. In addition, traders should monitor the seized-token overhang and whether any movement creates short-term pressure. Finally, Render must prove it can compete with both DePIN compute rivals and hyperscale cloud providers.

That is the real bottom line. Bittensor and Render are two different bets on the same AI megatrend. Render gives investors exposure to decentralized compute infrastructure. Bittensor gives investors exposure to decentralized intelligence coordination. The better asset depends on which layer of the AI economy a reader wants to own, and which risks they can underwrite.