Bittensor subnets generated $43M in Q1 2026. Learn how dTAO, alpha tokens, and the 6-factor framework help you evaluate the top AI subnets before investing.

Author: Kritika Gupta

Bittensor subnets are a self-contained competitive marketplace on Bittensor where miners perform a specific AI task and validators score their work.

Think of subnets like apps on a smartphone, or departments inside a company. In this setup, Bittensor is the base network, while each subnet runs its own job on top of it. One subnet may focus on AI inference. Another may train large language models. Another may provide GPU compute, scrape data, or build prediction systems. Although they all use the same broader Bittensor economy, each subnet has its own rules, participants, and output.

Inside each subnet, miners do the work. Validators then check that work and assign scores based on the subnet’s incentive mechanism. That mechanism matters because it defines what the subnet considers valuable. For example, an inference subnet may reward speed, cost, and output quality. A compute subnet may reward verified GPU availability. A data subnet may reward freshness, accuracy, or coverage.

To join the network, subnet teams register for limited network slots through Bittensor’s registration process, which has historically involved TAO costs through burn or auction-style mechanisms. As of May 2026, Bittensor operates around 128 active subnet slots, with the ecosystem preparing for broader expansion. Because those slots are limited, subnets compete not only for users and miners, but also for capital, validator attention, and emissions.

This is what makes Bittensor subnets different from a normal AI token. TAO is the base asset, but subnets are where most of the specialized AI work happens. Instead of being one single AI product, Bittensor becomes a network of AI markets, where each subnet tries to prove that its specific machine-intelligence output is useful enough to earn capital, operators, and demand.

New to Bittensor? Start here: Bittensor (TAO) Explained: The Complete Guide

Ecosystem trackers estimated subnet revenue at approximately $43M in Q1 2026, though no single audited source confirms the exact figure. However, that figure still needs careful framing. No single official Bittensor dashboard currently provides a fully audited, subnet-by-subnet revenue statement. Therefore, the best way to read the number is as a market-reported benchmark for external AI demand, not as a protocol-level financial filing.

This distinction matters because subnets are not supposed to be simple emission farms. A serious subnet should sell a useful AI service. Revenue can come from inference fees, data marketplace payments, API access, compute rentals, model services, and enterprise contracts. For example, inference subnets can charge users or applications for model output. Data subnets can earn from access to specialized datasets or labeling markets. Compute subnets can earn from GPU capacity. Meanwhile, enterprise-facing subnets can package these services into direct customer contracts.

This is the line skeptics should watch. TAO emissions are inflationary. They come from the network and reward miners, validators, subnet owners, and stakers. In other words, emissions can bootstrap supply, but they do not prove customer demand by themselves. External revenue is different because it shows that someone outside the reward loop is paying for the service.

As a result, this distinction changes the Bittensor debate. If a subnet only survives because TAO rewards flow into it, the market should treat it as high risk. By contrast, if a subnet earns real revenue, then uses part of that revenue to support its alpha token, pay contributors, or deepen liquidity, it creates a more credible economic loop.

At the protocol level, Bittensor’s own documentation describes the network as a system of independent subnets where miners produce digital commodities and validators evaluate their work. Those commodities include AI inference, training, compute, storage, and other machine-intelligence outputs.

Ultimately, the Q1 2026 revenue figure does not prove every subnet is healthy. Instead, it proves something more specific: parts of the subnet economy are already selling usable AI infrastructure. That is why real revenue remains the strongest answer to the “is this just emissions?” question.

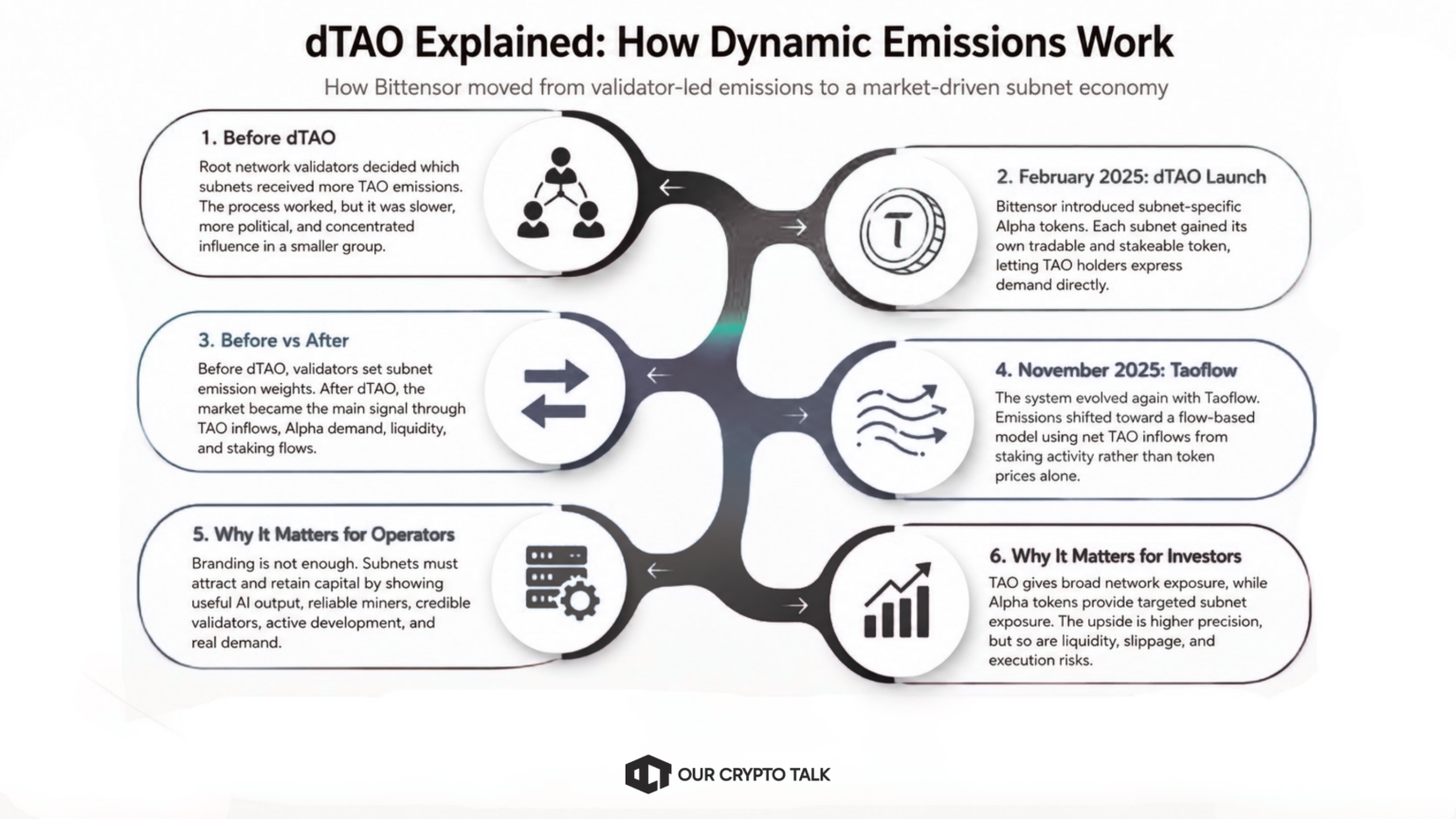

Before dTAO, Bittensor used a more validator-led system for subnet emissions. Root network validators helped decide which subnets deserved more TAO. In practice, that model gave experienced validators a powerful role in capital allocation. However, it also created clear limits. Emission decisions could become slower, more political, and more dependent on a smaller group of actors.

That changed in February 2025. dTAO introduced subnet-specific alpha tokens and moved Bittensor toward market-driven emission allocation. From that point, each subnet had its own tradable and stakeable token, commonly called an alpha token. As a result, TAO holders could express demand for a subnet by moving capital into that subnet’s alpha market. Taostats describes alpha as the generic name for subnet tokens and states that all subnets received staking tokens from the dTAO launch in February 2025.

The before-and-after frame is simple. Before dTAO, root validators played the central role in deciding subnet emission weights. After dTAO, the market became the main signal. Subnets had to attract TAO, alpha demand, liquidity, and sustained staking flows. In turn, that made subnet emissions more dynamic and more competitive.

Since then, the system has continued to evolve. Bittensor’s own emissions documentation says the network moved toward a flow-based model called Taoflow from November 2025, with emissions based on net TAO inflows from staking activity rather than token prices alone. Taostats also describes TAO flow as a normalized input used to determine how much TAO each subnet receives.

For subnet operators, this matters because branding is not enough. A subnet needs to attract capital and keep it there. Strong teams must show useful AI output, reliable miners, credible validators, active development, and real demand. If capital flows out, emission share can fall.

For investors, dTAO makes subnet analysis much more important. TAO gives broad exposure to the network, but alpha tokens create targeted exposure to individual subnets. That can increase upside, but it also adds liquidity risk, slippage risk, and execution risk. A good subnet can gain emissions and market share. By contrast, a weak subnet can lose both quickly.

In 2026, dTAO is the core reason Bittensor looks less like a single AI token and more like a live capital market for decentralized AI. Ultimately, it lets the market decide which AI tasks deserve more resources.

Alpha tokens are the subnet-specific tokens that power Bittensor’s dTAO economy. Each subnet has its own alpha token, and that token trades against TAO inside an internal automated market maker pool. When a user stakes TAO into a subnet, the TAO enters that subnet’s reserve, and the user receives alpha tokens representing exposure to that subnet. Bittensor’s staking documentation states that each subnet maintains its own AMM pool with TAO and alpha reserves.

This is where the money conversation starts. TAO gives broad exposure to Bittensor. By contrast, alpha tokens give targeted exposure to a specific subnet. If you believe an inference subnet, compute subnet, or data subnet will win more demand, its alpha token becomes the direct market expression of that view.

From a network-design perspective, alpha tokens are minted through the subnet’s operation and emissions process. Taostats also notes that alpha is used for staking on a subnet and for registering miners and validators, with alpha spent on registration recycled back into the system.

In practice, alpha tokens accrue value through two main channels. The first is emission share. More alpha staked to a subnet can support higher emissions, while net TAO flow helps determine how much TAO a subnet receives under the current Taoflow model. The second channel is real revenue. If a subnet earns external revenue from inference, APIs, data services, or enterprise contracts, that revenue can support the subnet’s economy through buybacks, staking, liquidity, or contributor payments.

For investors, access usually starts with Taostats interfaces, the Bittensor CLI, and supported ecosystem trading routes. Some larger subnet tokens may also appear on exchanges or third-party markets. However, on-chain liquidity remains the core venue for most alpha exposure.

Importantly, the relationship between alpha price and emission share is not mechanical in a simple one-to-one way. A rising alpha price can signal demand for a subnet. Strong TAO inflows can support emissions. Higher emissions can then attract miners, validators, and more stake. However, that loop can work in both directions. If demand weakens, emissions, liquidity, and participation can fall together.

That is why liquidity is the risk most investors underestimate. Taostats warns that alpha purchases and sales carry slippage. Thin subnet pools can move sharply on moderate trade size. As a result, a good subnet thesis can still become a bad trade if the entry price, exit liquidity, or slippage is poor.

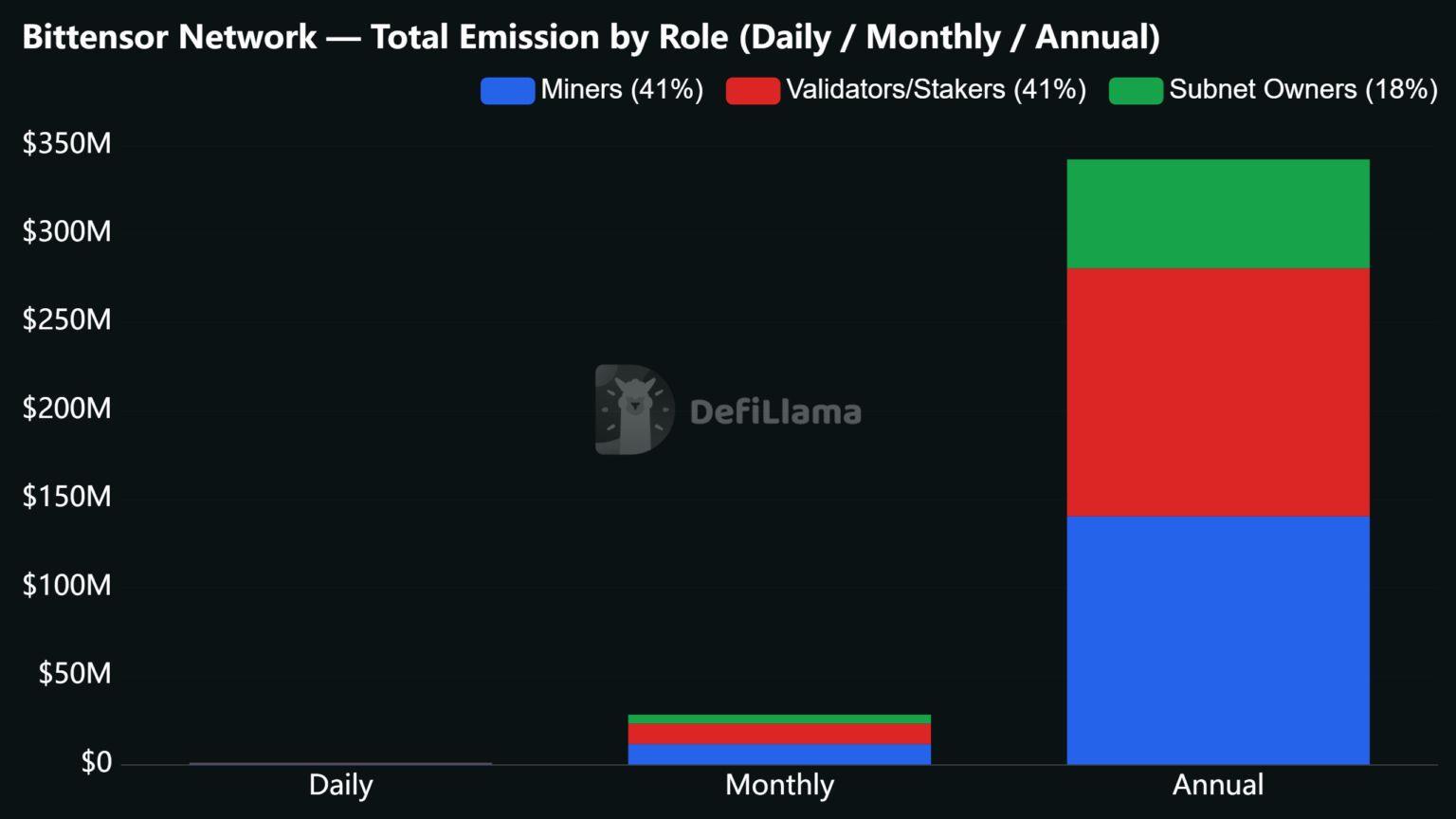

A Bittensor subnet has three core roles: miners, validators and subnet owners. Each role controls a different part of the market, and each one earns from the subnet’s emission flow.

The validators judge that work. They run the subnet’s validator code, test miner outputs and submit scores back to the network. A validator does not simply vote on vibes. Instead, it uses the subnet’s incentive mechanism to decide which miners delivered the best output. Bittensor’s docs state that validator scores determine how miner emissions are allocated through Yuma Consensus.

Finally, subnet owners design the market. They define the task, write the incentive mechanism, set key parameters and maintain the miner and validator codebase. Taostats describes subnet owners as the teams responsible for the base miner and validator code, as well as the incentive mechanism that assigns value to miner work.

Economically, the split is straightforward. For each subnet, emissions are generally divided into three buckets: 41% to miners, 41% to validators and their stakers, and 18% to the subnet owner. Bittensor’s emissions documentation lists the same split, with 18% allocated to the subnet owner, 41% to miners and 41% to validators and stakers. Taostats also shows the same owner, miner and validator allocation on subnet pages.

That 18% subnet owner take matters. It gives builders an ongoing revenue stream for maintaining the subnet, improving the mechanism and supporting operations. When the team keeps shipping, this can align incentives. However, it can also become a red flag if the owner collects emissions while the codebase, miners or real usage stagnate.

For investors, this structure creates a simple test. A healthy subnet should have useful miners, honest validators and an owner team that keeps improving the market. If one of those three breaks, the subnet’s economics can weaken fast.

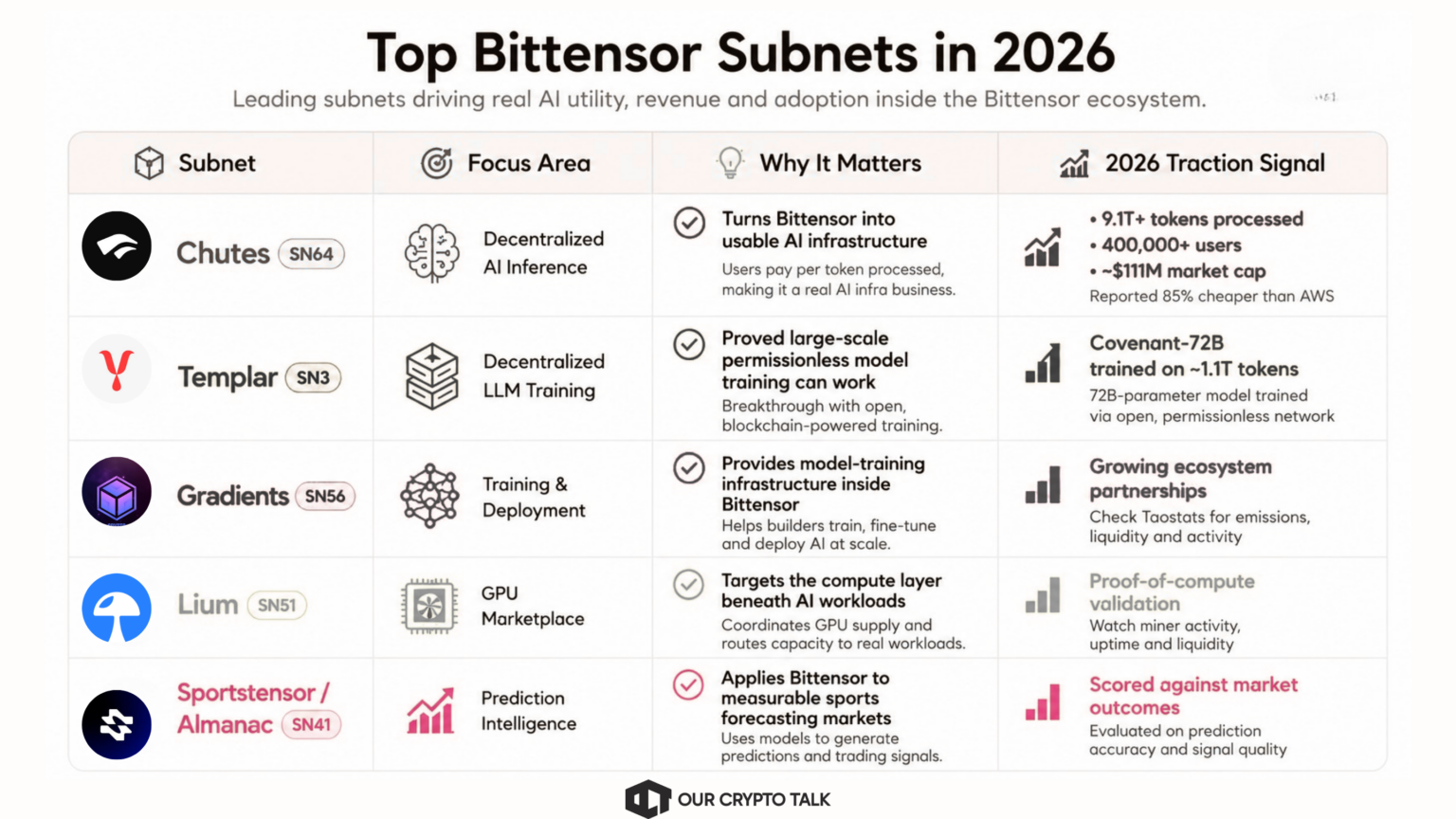

Chutes (SN64)

Chutes is the cleanest product-market fit story in the Bittensor subnets economy. It gives developers decentralized AI inference without asking them to manage servers, GPUs or backend infrastructure. Users pay per token processed, which makes Chutes closer to an AI infrastructure business than a pure emissions play.

Its reported traction is why it leads most 2026 subnet lists. OurCryptoTalk’s May 2026 subnet ranking listed Chutes at 9.1 trillion-plus tokens processed, more than 400,000 users and roughly $111 million in market cap. It also described Chutes as 85% cheaper than AWS, based on public ecosystem disclosures.

The pitch is simple. If decentralized AI needs a usage layer, Chutes is one of the first subnets proving that users will actually pay for it.

Templar (SN3)

Templar is Bittensor’s flagship decentralized training story. Its core claim is not cheaper inference or idle GPU resale. It is permissionless large-language-model pre-training across distributed contributors.

The proof point is Covenant-72B. The March 2026 research paper describes Covenant-72B as a 72-billion-parameter model trained on roughly 1.1 trillion tokens through open, permissionless participation supported by a live blockchain protocol. The paper says the run used a communication-efficient optimizer and dynamic contributors rather than a closed data-center setup.

That made Templar one of the most visible Bittensor subnets in 2026. It also brought risk into focus after Covenant AI’s reported exit from Bittensor in April 2026. The takeaway is balanced. Templar proved decentralized training can produce serious research results, but it also showed how dependent a subnet can become on a single operator.

Gradients (SN56)

Gradients sits in the training and deployment lane. It is useful because Bittensor needs more than one breakout inference subnet. It needs infrastructure for teams that want to train, fine-tune and deploy AI models without relying fully on centralized platforms.

The appeal is ecosystem leverage. Gradients is often discussed alongside the Chutes and Rayon Labs orbit, which gives it a stronger engineering narrative than many early-stage subnets. It targets a real bottleneck: making advanced model training and deployment more accessible to developers, researchers and application teams.

Current public metrics are less standardized than Chutes, so investors should verify live miner count, validator activity, emission share and alpha liquidity on Taostats before making any call. The pitch remains strong, but the underwriting standard should be strict. Gradients needs to show sustained usage, not only strong ecosystem association.

Lium (SN51)

Lium is a decentralized GPU marketplace. That makes it one of the more straightforward Bittensor subnets to understand. AI needs compute. Lium tries to coordinate GPU supply and route that capacity toward real workloads.

OurCryptoTalk’s May 2026 subnet ranking placed Lium among the top five Bittensor subnets, listed it as SN51 and described it as a GPU marketplace with proof-of-compute validation. The same ranking highlighted its positioning as a large sovereign GPU cluster inside Bittensor.

That matters because compute is the base layer beneath training, inference and agent workloads. If Bittensor’s application subnets grow, compute demand should grow with them. Lium’s challenge is execution. It must prove that its marketplace can attract reliable hardware, verify work and compete with centralized cloud capacity on price and availability.

Sportstensor, Almanac (SN41)

Sportstensor, now commonly tied to Almanac, is one of the clearest examples of Bittensor moving beyond generic AI infrastructure. It focuses on sports forecasting and prediction-market intelligence. Instead of rewarding vague model output, it can score miners against market outcomes, trading accuracy and signal quality.

SubnetAlpha describes Almanac, Subnet 41, as a decentralized AI-driven platform for sports prediction markets that aggregates independent forecasts into a meta-model and routes signals into external markets such as Polymarket. The project’s GitHub states that miners generate information signals by trading on Almanac, with each trade scored by accuracy, ROI, timing and informational value.

That gives SN41 a compelling pitch. It turns prediction into a measurable market contest. The risk is also clear. Sports and prediction markets are competitive, regulated and volatile. Sportstensor needs durable signal quality, not just strong narrative fit.

Top Bittensor subnets to watch in 2026

A good subnet review starts with one question: does this subnet produce useful work, or does it only recycle emissions? Use this six-factor framework before touching any alpha token or staking decision.

Red flags checklist:

The best subnet investments usually look boring before they look obvious. They have users, working code, measurable output, honest validators and enough liquidity to support real participation.

There are three main ways to get exposure to Bittensor subnets: buy alpha tokens, stake TAO through delegation, or run your own validator. Each path has a different risk profile.

Start with research, not the swap button. Open Taostats, choose the subnet, then check alpha price, pool depth, recent flows, emission share and slippage. Taostats explains that every alpha purchase has slippage, and the displayed alpha price is only an estimate of what you may receive after the trade executes.

Most users buy alpha through Taostats subnet pages or Bittensor staking tools. More advanced users can use the Bittensor CLI. Some subnet tokens may also appear through third-party venues, but internal subnet pools remain the core market.

Use smaller entries on thinner pools. A 1 TAO trade and a 50 TAO trade can have very different execution. Bittensor’s own slippage documentation shows how larger staking actions can change the alpha received because the trade moves the subnet pool price.

Delegation means staking TAO to a validator instead of running validator infrastructure yourself. Bittensor docs state that TAO holders can stake any amount to a validator, and that the validator’s total stake helps determine consensus power and emission share. After the validator takes its fee, the remaining emissions go back to delegators in proportion to stake.

Pick validators by take rate, uptime, subnet focus, historical performance and reputation. Do not chase the highest displayed APY without checking consistency. Public staking APYs can vary, and centralized staking products showed around 5% TAO APY in May 2026, but subnet-specific delegation can move above or below that based on emissions, flows and validator performance.

Also check exit mechanics. Taostats says there is no hold period for staking, but alpha staking carries price risk because alpha/TAO values fluctuate.

This is the hardest path. A validator needs a hotkey, live infrastructure, subnet-specific code, monitoring and enough stake weight to matter. Bittensor docs state that validator emissions depend on hotkey stake weight, and validators can stake their own TAO or attract delegated stake from others. Taostats also notes that some subnets require minimum stake to be effective, otherwise validator weights may have near-zero impact.

The ROI can be higher than passive delegation, but only if the validator wins stake, scores miners well and stays operational. Treat this like running infrastructure, not passive yield.

Bittensor subnets can produce real AI value, but they can also fail fast. Investors should treat subnet exposure as high-risk venture-style crypto, not passive AI yield.

The first risk is emission decay. Bittensor subnets have a limited pool of TAO emissions, and subnets compete for that pool. When more subnets enter the network, weak subnets face more pressure. Bittensor’s 128-subnet cap and resumed deregistration process mean new subnets can replace the lowest-performing non-immune subnets, forcing teams to prove value or lose their slot.

The second risk is alpha token dilution. Alpha tokens are part of each subnet’s emission and staking economy. If new alpha supply keeps entering the market while demand stays flat, holders can get diluted. This becomes worse when a subnet has weak revenue, falling emissions, or no clear buy pressure.

The third risk is subnet failure. Failure can mean formal deregistration, team abandonment, emission collapse, or incentive-mechanism gaming. Taostats says that when a subnet is deregistered, its alpha is liquidated and exchanged back into TAO from the pool. That protects users from being left with a dead token, but it does not remove price risk before deregistration happens.

The clearest 2026 example is Covenant AI and Templar. Covenant helped prove decentralized training through Covenant-72B, but its April 2026 exit triggered a sharp governance debate and a major TAO selloff. Reports said TAO fell roughly 20% to 28% after the exit and related token sales. That was not a failed model-training experiment. It was subnet owner risk made visible.

A second example is the broader deregistration zone. Low-emission subnets that cannot attract stake, miners, validators, or usage are at risk of being replaced when new teams register. This is not a bug. It is the network’s survival mechanism. Weak subnets make room for stronger ones.

A third example is incentive-mechanism failure. Academic analysis of Bittensor subnets found concentration in stake and rewards, with rewards often driven more by stake than quality. That points to a real risk: a subnet can look active while failing to measure useful work correctly.

Liquidity is another hard risk. Alpha pools can be thin. A 2026 paper on decentralized AI subnets found that slippage can erase returns at larger trade sizes, with transaction costs exceeding gross returns at $100,000 in assets under management.

Smart contract, wallet, validator and protocol risks remain. The honest conclusion is simple: real revenue helps answer the Ponzi critique, but it does not save every subnet. Weak teams, weak mechanisms and weak liquidity still fail.

Taostats is the main dashboard most Bittensor subnets users rely on for subnet discovery, staking, portfolio tracking and validator analytics. Start with the Subnets page. This is your market map. Sort the table by emission, market cap, volume, validator activity or subnet number. Use it to answer one question first: which subnets are attracting capital and attention right now?

Next, click an individual subnet. This page gives you the subnet’s core health metrics. Look near the top of the page for market cap, volume, FDV, circulating supply, alpha in pool and TAO in pool. Taostats defines these as the key subnet market fields, including the amount of alpha and TAO sitting inside the subnet liquidity pool.

Then check the emission and participant data. Emission shows how much reward the subnet is receiving. Miner and validator data show whether real operators are active. A subnet with rising emissions but weak participation deserves caution. A subnet with stable validators, competitive miners and improving liquidity is more credible.

After that, open the validator page. This is where delegation decisions start. Look for validator take rate, stake, performance history and subnet coverage. Bittensor’s delegation docs explain that validator stake affects consensus power and emission share, while delegators receive rewards after the validator takes its fee.

Finally, review the dTAO or alpha trading view before staking or buying. Look for the estimated alpha received, price impact and slippage. Taostats warns that alpha tokens are bought with TAO through subnet liquidity pools, and every transaction can face slippage. Bittensor’s slippage docs also show how larger trades can change the amount received.

Use this order every time: subnet list, subnet page, validator page, alpha trading view. It turns Taostats from a wall of numbers into a practical decision tool.

Bittensor’s subnet roadmap is moving from scarcity to scale. The network expanded to 128 active subnet slots by early 2026, and several 2026 market reports say the next major step is a planned move toward 256 active subnets later in the year. CoinGecko described the 256-subnet expansion as projected for later in 2026, while CoinDesk reported in March 2026 that the move would bring a new wave of subnet token launches.

For existing subnet owners, this means more competition for emissions. A larger subnet set does not create unlimited TAO rewards. Instead, it increases the number of teams competing for attention, stake, alpha liquidity and validator support. As a result, weak subnets can lose emission share faster when better operators enter the market.

For new builders, 256 slots would lower the barrier to entry. More teams can launch specialized AI markets without waiting for a narrow set of openings. That should encourage experimentation across areas like scientific AI, financial modeling, data pipelines, robotics, inference routing and domain-specific agents.

For investors, the opportunity gets bigger, but so does the dilution risk. More subnet tokens means more ways to express a thesis. At the same time, it also means more fragmented liquidity, more low-quality launches and more pressure on weaker alpha tokens. A rising subnet count is not automatically bullish for every subnet. Instead, it is bullish only if the new markets attract real users and useful AI work.

For the network overall, 256 subnets would make Bittensor’s subnet economy more diverse. It gives the protocol more shots at finding durable AI markets. However, it also raises the standard for due diligence because investors and validators will need to separate serious subnet operators from speculative launches.

Ultimately, the TAO impact depends on whether expansion drives real demand or just more emissions chasing more tokens. If new subnets bring revenue, users and better AI services, the expansion can support TAO’s long-term case. By contrast, if it mainly adds speculative alpha launches, dilution becomes the story.

Conviction locks are Bittensor’s answer to a hard subnet problem: how do you prove long-term commitment on-chain? In practice, current public documentation centers the mechanism on locking alpha tokens, not simply locking TAO for a generic yield boost. Stakers lock subnet alpha for a chosen period, and over time, that locked stake builds a conviction score. As a result, conviction becomes a time-weighted measure of subnet commitment, where locked alpha can influence who controls a subnet.

The game theory is straightforward. If a holder is short-term, locking makes little sense because it reduces liquidity. However, if a holder is long-term bullish on a subnet, locking can be rational. It signals commitment, supports the current owner or a challenger, and gives the holder more influence over the subnet’s future.

This is why conviction locks matter for subnet economics. A subnet owner can no longer rely only on an old registration slot and ongoing emissions. Instead, they need visible support from committed capital. At the same time, locked alpha can reduce liquid supply, which may lower short-term sell pressure and help stabilize alpha-token markets. Still, that does not guarantee price appreciation. It simply makes speculative exit behavior more visible, especially after the Covenant controversy pushed Bittensor toward lock-based ownership reform.

Looking ahead, the tier structure and exact rollout may continue to change as the mechanism matures. Early public coverage framed the system as a phased governance upgrade, with mature subnets targeted first and newer subnets receiving more time before full rules apply. Therefore, conviction locks should be viewed less as a simple staking feature and more as a governance filter.

This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risk.

Crypto Projects Shut Down 2026: 10 Failures, $87M Lost

AI Needs Trusted Data. Can The DATA Foundation Deliver?

Crypto Bridges & DEX Aggregators in 2026: The Full Landscape

Ondo Perps vs Hyperliquid: Stock Collateral vs Speed

Crypto Projects Shut Down 2026: 10 Failures, $87M Lost

AI Needs Trusted Data. Can The DATA Foundation Deliver?

Crypto Bridges & DEX Aggregators in 2026: The Full Landscape

Ondo Perps vs Hyperliquid: Stock Collateral vs Speed