MEGA is down 61% from its TGE high while MegaETH TVL surged 58.5%. We analyze the tokenomics, USDm growth, Kumbaya controversy, and what the June 23 unlock means.

Author: Sahil Thakur

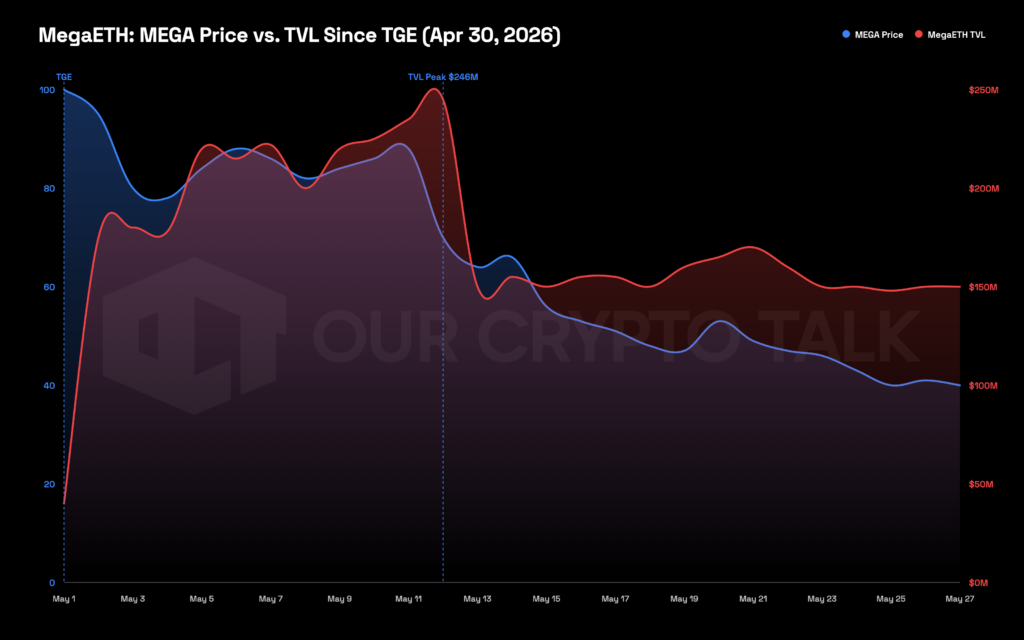

MEGA, the native token of MegaETH, sits down 61% from its all-time high of $0.1756. That high printed on April 30, 2026. The chain’s total value locked is up 58.5% over the same period. Both numbers describe the same chain. The gap between them is the MegaETH story as of May 27, 2026.

MegaETH launched mainnet on February 9, 2026 and ran its Token Generation Event on April 30. The pitch was a real-time Ethereum Layer 2 with roughly 100,000 transactions per second and 10-millisecond mini-blocks. Four weeks in, the technology works. The tokenomics, community governance, and ecosystem depth do not.

MegaETH is an EVM-compatible Layer 2 built for one thing: raw execution throughput. The team targets roughly 100,000 transactions per second with 10-millisecond mini-blocks. Ethereum mainnet, by comparison, runs on 12-second slots.

Architecturally, the chain runs a single high-performance sequencer with a custom EVM written down to the OS and memory-allocation level. State stays in memory wherever possible. EigenDA handles data availability, so the sequencer can focus purely on execution.

The thesis behind that design is direct. Every serious EVM rollup before MegaETH (Arbitrum, Base, Optimism) optimized the fraud-proof and settlement layer. The sequencer itself stayed mostly untouched. The MegaETH founders argued that throughput, not security, is the binding constraint on Ethereum. In their view, rebuilding the sequencer from first principles unlocks a different class of apps. Think on-chain games, HFT-style DeFi, and social graphs that no existing L2 can host.

Three founders built it. Yilong Li, a Stanford PhD who studied high-performance systems, serves as CEO and wrote the core EVM redesign. Lei Yang completed his MIT PhD in 2024 and runs as CTO. His research background sits in distributed systems and database-level performance. Shuyao Kong, known in the community as Mengmeng, came from Consensys and runs COO, community, and partnerships.

The MegaETH Layer 2 raised roughly $107M pre-launch across four rounds. Dragonfly Capital led the $20M seed in June 2024, with Vitalik Buterin participating in a personal capacity. That seed gave the project early legitimacy and pulled in heavy media coverage. A $10M Echo community round followed in December 2024 at about $0.02 per MEGA, selling out in 56 seconds. A Fluffle NFT mint in February 2025 added an estimated $13.5M to $27M. A $50M public sale in October 2025 priced at $0.0999 and was 3x oversubscribed.

The MegaETH mainnet went live on February 9, 2026 with $40.3M already bridged in. That number grew steadily over the next 80 days, reaching $105.5M by the eve of TGE. Pre-token TVL of that size, with no MEGA in circulation yet, is a stronger demand signal than most L2 launches manage.

Three pieces of pre-launch infrastructure mattered. The team designed USDm, MegaETH’s yield-bearing stablecoin, to generate T-bill and PoS yield that would later fund MEGA token buybacks. The Fluffle collection distributed 10,000 soulbound NFTs to roughly 80,000 eligible community members. Holders received 5% of total supply on a six-month vest. The Terminal points program, launched April 28, was a last-mile engagement push that drew under 6,000 participants.

In November 2025, the team opened a pre-deposit bridge to let early capital flow onto the chain. Around $500M of deposit intent came in within hours. Then the bridge shut down and refunded every dollar. The cause: a misconfigured multisig controlling the bridge contract. Users got everything back. Still, a multisig error on a $500M deposit window is an uncomfortable look for a team selling itself as infrastructure-grade engineering. The incident foreshadowed the trust pattern that came after TGE.

MEGA opened on April 30 at roughly $0.1637 per DefiLlama. It hit an all-time high of $0.1756 at 13:52 UTC that same day. Some web sources cite a brief $0.38 spike on thin DEX liquidity before centralized order books opened. The confirmed exchange ATH still sits at $0.1756. Day 1 DEX volume was $137.5M, roughly 40x the pre-TGE daily average, with no sequencer downtime reported.

Thirteen exchanges listed MEGA at the same time, including Binance, Coinbase, OKX, and Bybit. The team has stated they paid zero listing fees. That would be unusual but consistent with the breadth of coverage. Echo participants who entered at $0.02 were up 778% at ATH. Public sale buyers at $0.0999 saw a peak gain of 75.8%. Fluffle holders, at an effective basis of about $0.03, were up 485%.

The price arc after ATH was a slow unwind, not a single dump. May 2 was the worst single day at -13.16%. The first green close came on May 5. By May 27, MEGA trades at $0.0688, down 61% from ATH.

The on-chain numbers tell a more interesting story than the token chart. Total Value Locked, USDm supply, and fee revenue have all moved in the same direction for the same reasons.

TVL has moved through four distinct regimes. Mainnet launch on February 9 started the count at $40.3M. The 80-day pre-TGE phase climbed organically to $105.5M. The 12 days from April 30 to May 12 then surged to a peak of $245.6M, a 133% increase. MEGA incentives and Aave V3’s launch incentives kicked in together. The 15 days after walked back down to $158M as MEGA fell and dollar-denominated yields contracted.

The composition skews hard. Aave V3 holds $119.6M, or 75.3% of all tracked protocol TVL on the chain. That figure is up 521.5% in 30 days per DefiLlama. Kumbaya DEX sits at roughly $25.3M, down 57.6% over 30 days. GMX on MegaETH is down 89.1%. The remaining protocols add up to around $13.5M between them.

That concentration is both a strength and a structural risk. Blue-chip lending depth gives institutional users a reason to be on the chain. It also means MegaETH’s ecosystem is, for now, narrower than the $158M TVL number suggests.

The USDm stablecoin is the most underreported MegaETH story. At TGE, supply stood at $63M. By May 8, eight days later, USDm had grown to $480M. That’s a 662% increase. The stablecoin briefly crossed $500M between May 6 and May 13 before retreating to around $300M.

USDm is over-collateralized and yield-bearing. The collateral backing it is a mix of T-bills (the same paper that backs USDC) and proof-of-stake yield from staked ETH. That yield accrues to the protocol, not to individual holders, which gives MegaETH a revenue stream that’s independent of token-price action.

Two things matter about the growth. First, it’s a clear signal that users actively prefer a yield-bearing native stablecoin to bridged USDC when one exists. Second, USDm yield funded the first MEGA token buyback on May 7. The Foundation used yield accumulated in April, before MEGA even had a full week of trading. A buyback that runs on T-bill yield instead of token-price appreciation is the strongest tokenomic mechanism in the ecosystem.

TGE created a permanent step-change in fee revenue. Pre-TGE, MegaETH apps generated roughly $15,710 per day. Post-TGE, the average sits at $69,598 per day, a 4.4x multiple. The 30-day total is $2.58M. Annualized, that’s a $31M run-rate.

At a $688M FDV, MEGA token trades on a price-to-fees ratio of about 22x. That’s aggressive against established L2s but reasonable for an early-stage chain with a growing app surface. Fees are still heavily Aave-concentrated, which is the same caveat that lives on the TVL number.

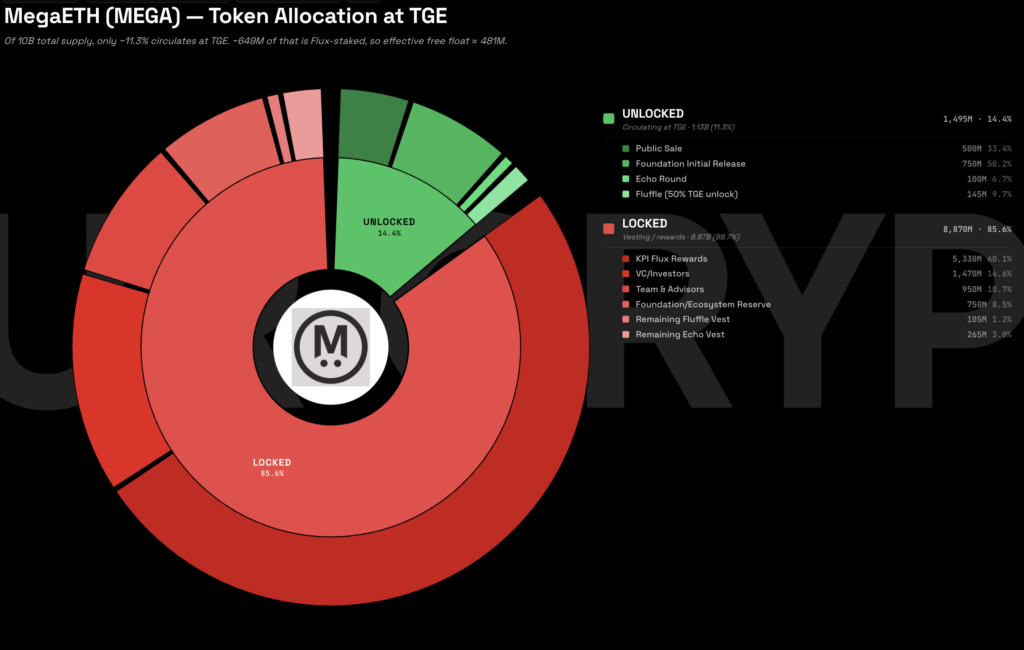

The token chart needs the supply structure to make sense. At TGE only about 1.13 billion of MEGA’s 10 billion total supply hit circulation. That’s 11.3% of the cap. The remaining 88.7% sits locked across team, investor, Foundation, and KPI Flux allocations.

The 1.13B circulating supply splits roughly into 500M from the public sale, 750M from the Foundation’s initial release, 100M from Echo, and around 145M from Fluffle. With a float that thin, even modest selling pressure creates outsized price impact. The 61% drawdown from ATH reflects that imbalance as much as any shift in fundamentals.

Flux staking pulls another 649M MEGA off the immediate market. That’s about 57% of the float. It softens effective sell pressure significantly. It doesn’t fix the structural overhang.

The KPI Flux mechanism is where the design gets clever, and where retail confusion lives. Three milestones gate roughly 53.3% of total supply, or 5.33B MEGA. KPI #1, a USDm threshold, triggered on April 23, before TGE. KPI #2 needs USDm to hold $500M on a 30-day time-weighted average. That hasn’t happened. USDm retreated from its peak back to roughly $300M. KPI #3 needs three independent apps each clearing $50K per day in fees for 30 straight days. The current Aave-concentrated profile doesn’t satisfy that.

The unlock calendar is the more immediate concern. On June 23, 2026, the Mainnet Campaign tranche releases 250M MEGA in one day. That’s roughly 22% of the current float and about $17.2M at the current price. Then comes a quieter stretch. The Echo cliff drops another 132.6M MEGA on April 30, 2027. Team and investor vesting begin a daily drip after that, running through about 2030.

The deepest community fracture didn’t come from price. It came from the Kumbaya DEX controversy, and the way the MegaETH Foundation handled it.

Kumbaya was the chain’s native DEX and the first significant app on MegaETH. The Foundation effectively endorsed it through featured placement. At launch it handled the majority of on-chain volume. Community members discovered post-launch that the contract routed a 50% LP fee split to a Foundation-controlled wallet. Half of all trading fees went to the Foundation rather than to liquidity providers. The structure was visible in the contract code. It appeared nowhere in the docs or the UI. Legal advisor Gabriel Shapiro defended the omission as “code is disclosure.”

Over two days, Kumbaya generated roughly $375K in fees. The Foundation silently extracted about $187K of that. The dollar amounts were small. The reputational damage wasn’t. The Foundation’s response, which was silence, made it worse. Community LPs migrated to Prism DEX, which uses a more transparent and LP-friendly split. Kumbaya’s TVL fell 57.6% over 30 days while the chain as a whole grew.

Two other incidents reinforced the same pattern. The Foundation announced the first MEGA token buyback on May 7 without disclosing size or execution price. That made it a PR event more than a verifiable financial mechanism. Then on May 21, the Terminal points program closed 33 days ahead of schedule with no prior warning. Users had been actively grinding for rewards. The announcement tweet drew 437 replies, the highest engagement on any tracked MegaETH post in the post-TGE period.

The most useful comparison set for MegaETH is its direct peer Monad and the cautionary case of Blast. Both data sets sit on DefiLlama.

Monad and MegaETH are siblings. Both are high-throughput EVM chains that ran long testnets, raised heavy capital, and launched within months of each other. As of May 27, Monad sits at $398.8M in TVL. MegaETH sits at $158.4M. So MegaETH is at roughly 40% of Monad’s scale. The flip side: MegaETH’s 30-day TVL growth is +58.5% against Monad’s +21.8%. MegaETH also generates about $16,311 in annualized fees per million dollars of TVL. Monad generates $5,228 on the same basis. On capital efficiency, MegaETH is roughly 3.1x ahead.

The token story diverges hard. MON is up 14.67% over a comparable 90-day window. MEGA is down 58.22%. Fundamentals alone don’t explain that gap. Monad launched with a lower initial float concentration and a less contentious community governance period. Both translate directly to lower sell pressure on a thinly traded float.

Blast is the other anchor. Peak TVL of about $2.7B in July 2024 collapsed to $30.75M as of writing. That’s a 98.9% drawdown. BLAST returned -65% in 2024. The pattern was incentive-driven TVL that fled when incentives ended. MegaETH’s structural difference from Blast is real: $2.58M in 30-day fees, a functioning buyback funded by USDm yield, and a tokenomic design that punishes incentive farming. Across the 2024-2026 L2 token cohort, MEGA’s -58% drawdown sits in the BLAST and STRK range. The peer numbers: STRK -72%, BLAST -65%, SCR -12%, ZK -7%. MON is the upside outlier.

The next 60 days are the test. Three near-term catalysts and a couple of structural risks will tell us whether MegaETH grows toward Monad’s $400M TVL or mean-reverts toward Blast’s $31M.

The June 23, 2026 Mainnet Campaign unlock is the most pressing near-term variable. 250M MEGA in one day is roughly 22% of current float. How the market absorbs that supply, and whether recipients are long-term aligned or passive airdrop collectors, sets the tone for the rest of the year.

MOSS SDK is the second variable. MegaETH demoed it at a Seoul event in late May. The announcement tweet drew 1,566 likes, the highest engagement on any dev-focused MegaETH content tracked in the period. MOSS gives developers tools to build order books, live games, and streaming financial apps that exploit the 10ms block time. Those apps are architecturally impossible on any other EVM chain. They also attack the Aave-concentration problem directly.

The KPI path is the third variable. KPI #2 needs USDm to re-cross $500M and hold it on a 30-day TWA. KPI #3 needs three independent apps each clearing $50K per day in fees for 30 straight days. Either trigger unlocks a tranche of Flux emissions and accelerates the buyback flywheel. Neither is close as of May 27.

A few longer-term risks sit in the background. The sequencer still runs on a single Foundation-controlled node, with a 4-of-8 multisig and 16 validators in a limited capacity. The team hasn’t published a decentralization roadmap. Foundation communications in late May have also hinted at a third revenue stream beyond USDm yield and fees. No details have surfaced. Credible candidates are MEV capture, RWA integration, or a shared sequencer product sold to other chains.

None of this is financial advice. The chain has real fees, real USDm yield, and real technical differentiation. Together they form a floor that Blast never had. The tokenomics complexity, the trust deficits, and the 88.7% supply overhang form a ceiling. That ceiling won’t lift until the KPI structure clarifies. Watch the June 23 unlock, the USDm $500M trajectory, and the MOSS SDK reception. Those three signals will tell the story.