Hyperliquid vs Aster: market share, OI, tokenomics, and the ETF race. Why the dethroning narrative was wrong.

Author: Tanishq Bodh

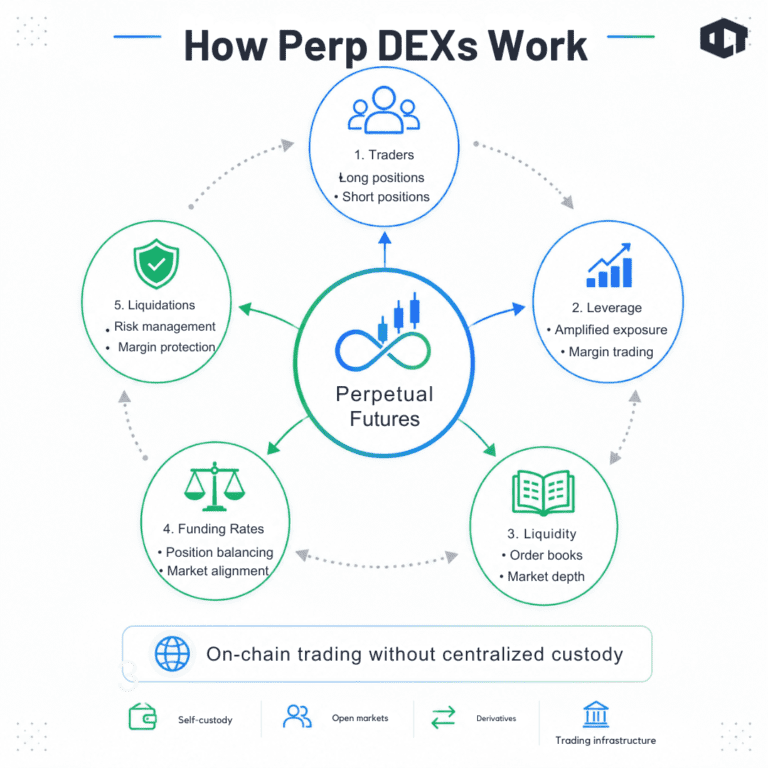

Perpetual DEXs are no longer a niche corner of crypto. They are becoming one of the biggest battlegrounds in the entire industry. For years, centralized exchanges like Binance dominated perpetual futures trading because they offered deep liquidity, fast execution, and leverage that decentralized platforms simply could not match. Most on-chain derivatives platforms felt slow, fragmented, and expensive compared to centralized competitors. That dynamic is now shifting as platforms like Hyperliquid and Aster push on-chain trading infrastructure into a new phase of growth.

By improving execution quality, liquidity depth, and trading efficiency, these perpetual DEXs are starting to compete with centralized venues on speed and user experience rather than just decentralization alone.

That changed when Hyperliquid exploded onto the market. Suddenly, traders had an on-chain exchange that actually felt competitive with centralized platforms. Tight spreads, smooth execution, deep liquidity, and a fast custom-built Layer 1 pushed Hyperliquid into the center of crypto’s derivatives market. But Hyperliquid is no longer alone.

Aster has emerged as one of the fastest-growing challengers in the perp DEX race, taking a completely different approach. Instead of building a vertically integrated trading chain, Aster is betting on multi-chain accessibility, extreme leverage, and trader-focused flexibility. The result is a genuine market split between two very different visions for the future of decentralized trading.

One platform is trying to become the institutional-grade infrastructure layer for on-chain trading, while the other is optimizing for speed, accessibility, and retail trader growth. This is no longer just a competition over volume. It is a battle over what the future of decentralized trading actually looks like.

It is a battle over what the future of decentralized trading actually looks like.

At a high level, Hyperliquid and Aster are trying to solve the same problem in completely different ways.

Hyperliquid focuses on execution quality, liquidity depth, and infrastructure efficiency. The platform runs on its own custom-built Layer 1 optimized specifically for trading performance. That approach allows Hyperliquid to offer an experience that feels much closer to a centralized exchange, especially for professional traders handling larger positions.

Aster is taking a more flexible and aggressive growth approach. Instead of building a vertically integrated ecosystem around one trading chain, Aster prioritizes accessibility across multiple ecosystems while leaning heavily into retail-friendly features and extremely high leverage.

The difference becomes obvious when looking at the type of traders each platform attracts.

Hyperliquid increasingly appeals to professional users, market makers, and traders who care deeply about execution quality. Aster attracts faster-moving retail traders looking for flexibility, accessibility, and speculative opportunities. Their long-term visions are also very different.

Hyperliquid is positioning itself as foundational infrastructure for on-chain trading. Aster is positioning itself as a fast-growing trading environment optimized for user expansion and multi-chain participation. That distinction shapes everything from liquidity behavior to tokenomics.

Crypto traders increasingly want the benefits of centralized exchanges without the risks that come with custodial platforms. The collapse of FTX permanently changed how many users think about exchange risk. Traders still want deep liquidity and advanced products, but they also want self-custody, transparency, and on-chain settlement. That created the perfect environment for perpetual DEXs to grow rapidly.

Perpetual futures are already one of the largest markets in crypto, with global crypto derivatives volume regularly surpassing spot trading activity. A growing percentage of that volume is now happening on-chain as trading infrastructure improves. The rise of app-specific chains accelerated this trend because newer projects stopped trying to force trading onto general-purpose blockchains that struggle with latency and congestion.

Hyperliquid became the clearest example of this infrastructure-first model, while Aster emerged with a more flexible multi-chain strategy. Hyperliquid is trying to build the most efficient trading engine possible, while Aster is trying to build the most accessible and flexible trading environment possible. That distinction matters because the next phase of crypto derivatives probably will not be winner-takes-all.

Different traders want different things from their platforms. Some care primarily about liquidity depth and execution quality, while others care more about leverage, accessibility, incentives, or chain flexibility. The perp DEX wars are ultimately about which platform can build the most durable liquidity network over time.

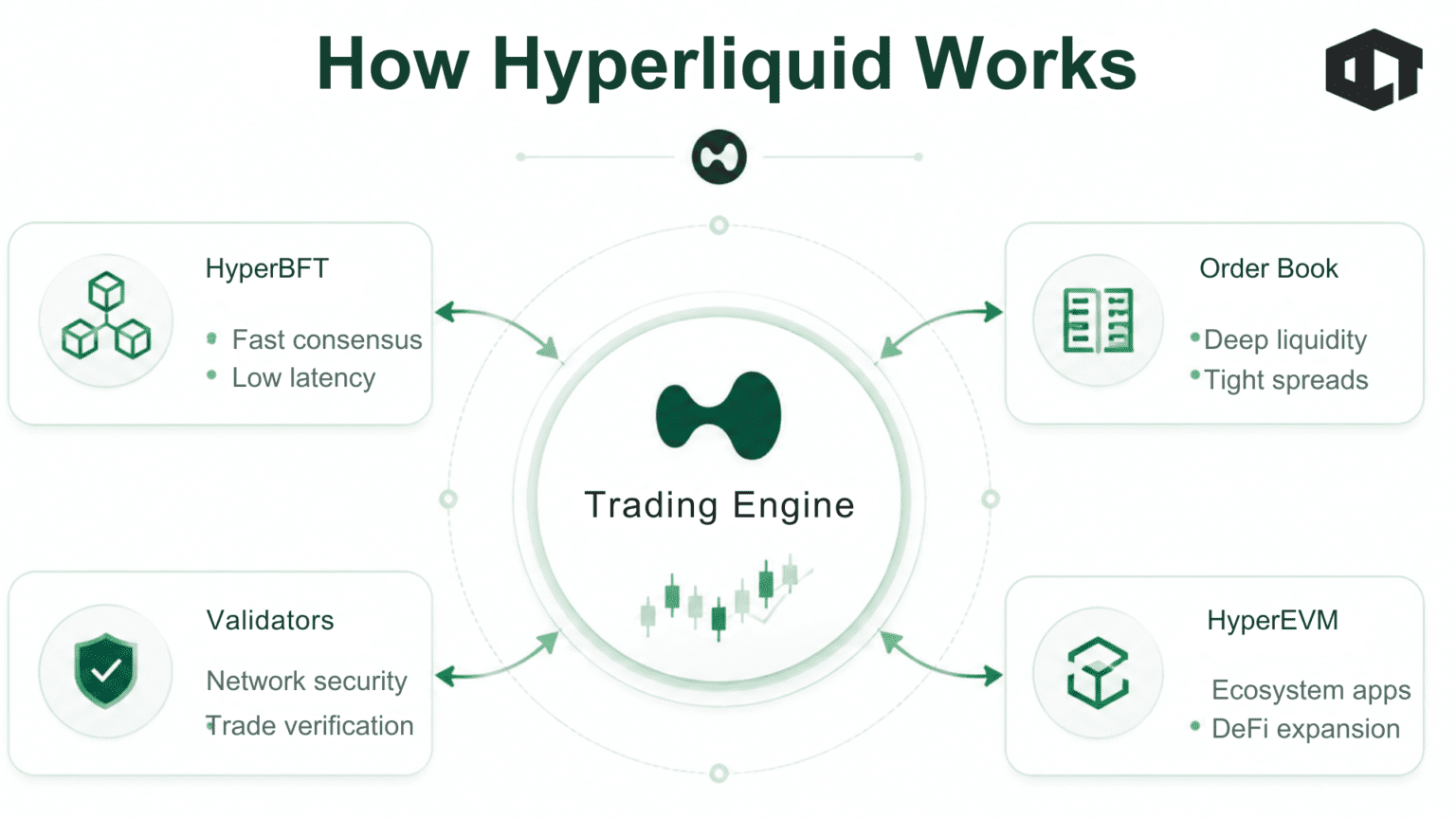

Hyperliquid’s core advantage is simple: it feels closer to a centralized exchange than almost any other decentralized trading platform. That is not accidental. The entire system was built specifically for high-performance trading instead of adapting a general-purpose blockchain for derivatives activity. Instead of launching as an app on Ethereum or another Layer 1, Hyperliquid built its own trading-focused chain.

This architecture allows Hyperliquid to support an on-chain order book instead of relying entirely on AMM-style liquidity systems. That difference is enormous because traditional AMM-based perp platforms often struggle with slippage, fragmented liquidity, and inefficient pricing during volatility. Hyperliquid’s order book structure creates a trading experience that feels much more familiar to professional users.

Execution is faster, liquidity is deeper, and larger orders move with less slippage. The platform also solved one of the biggest problems that held back earlier DeFi trading systems: user experience. Most older on-chain trading apps felt clunky and unreliable during heavy volatility. Hyperliquid feels smooth and responsive, and that alone became a major competitive advantage.

Hyperliquid uses its own consensus mechanism called HyperBFT. The goal is straightforward: maximize throughput and minimize latency for trading activity. This trading-first architecture helped Hyperliquid become one of the few decentralized exchanges capable of handling serious derivatives volume at scale.

Professional traders care about milliseconds. They care about spread quality. They care about liquidation efficiency. Hyperliquid built its reputation around solving those problems better than most competitors.

The order book is one of Hyperliquid’s biggest differentiators. Most decentralized exchanges still rely heavily on AMMs because they are easier to implement on-chain.

But AMMs introduce several limitations:

An on-chain order book allows Hyperliquid to create tighter spreads and better execution quality. That makes the platform particularly attractive to:

This is one reason Hyperliquid has consistently maintained strong open interest numbers compared to many other perp DEXs.

Hyperliquid is no longer just a trading platform. It is increasingly trying to become an ecosystem. HyperEVM expands the network beyond derivatives trading into broader DeFi applications, liquidity systems, and ecosystem tooling. This matters because liquidity networks become more powerful as ecosystems deepen.

If developers build:

around Hyperliquid liquidity, the platform’s moat becomes much stronger. The goal is clear. Hyperliquid wants to evolve from a successful exchange into foundational financial infrastructure.

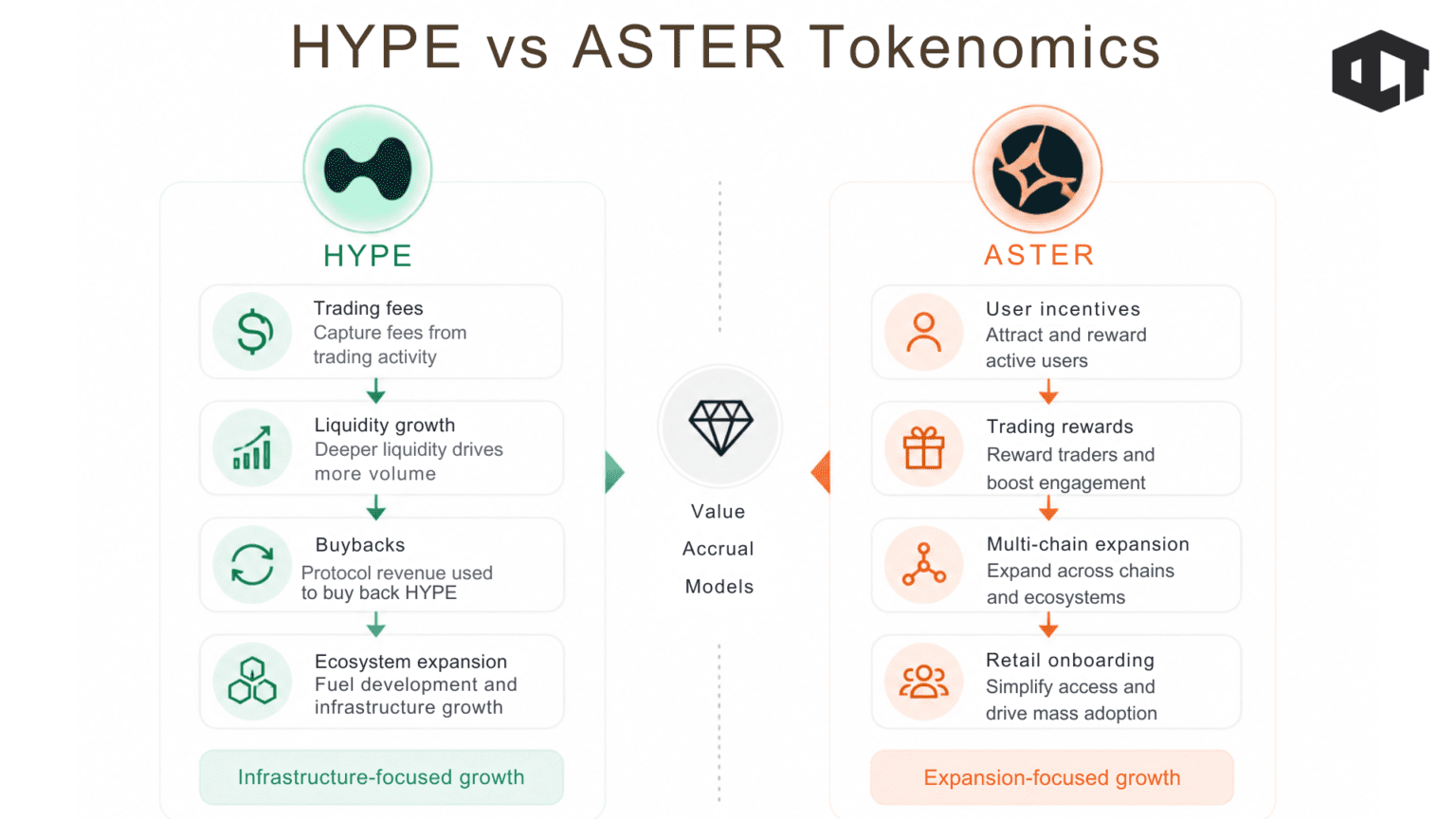

The HYPE token is central to Hyperliquid’s long-term thesis. Traders are not just betting on exchange growth. They are betting that Hyperliquid can become one of the dominant infrastructure layers for on-chain derivatives. The token’s appeal comes from several factors:

One of the biggest bullish arguments for HYPE is that Hyperliquid generates real usage. The platform’s liquidity depth and trading activity are not entirely dependent on short-term token farming incentives. That distinction matters. Crypto history is filled with platforms that generated massive volume during incentive periods but collapsed once rewards disappeared. Hyperliquid’s supporters argue its liquidity is far stickier.

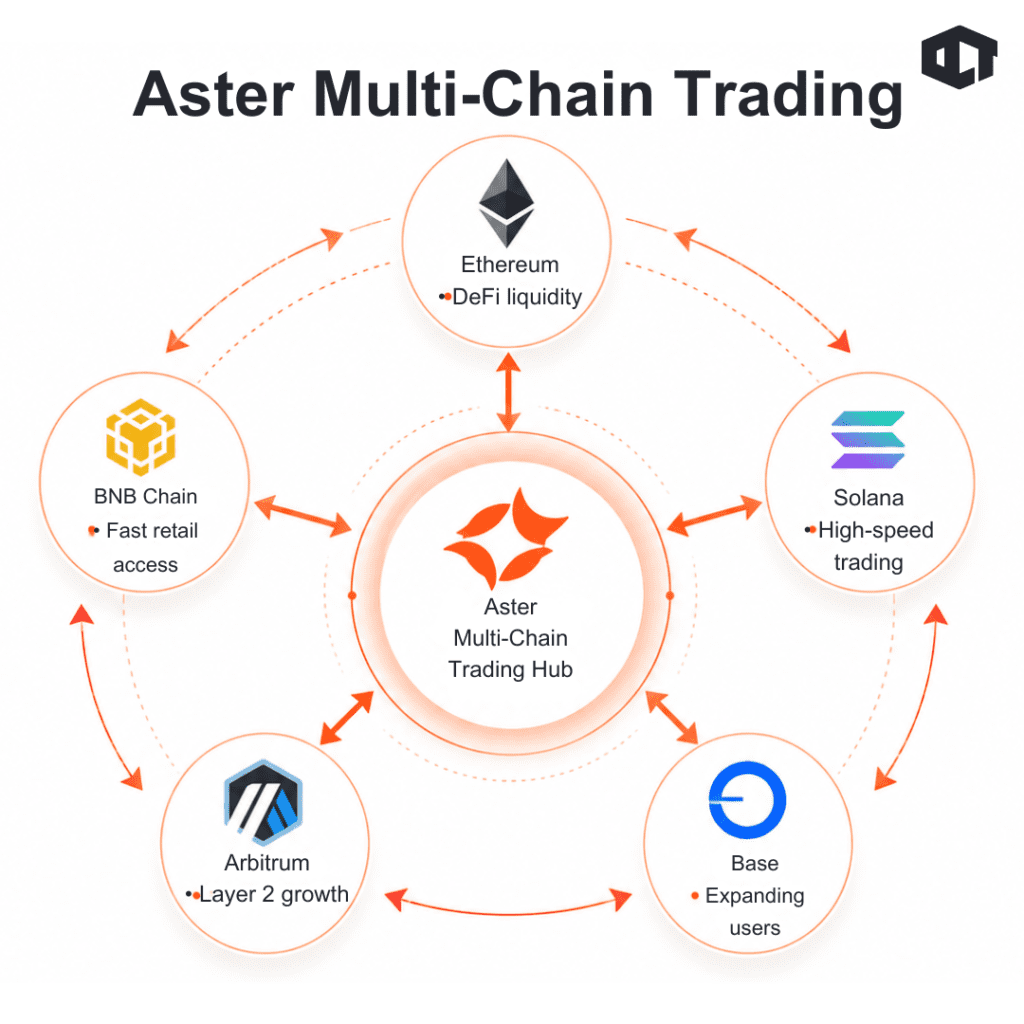

Aster is attacking the market from a completely different angle. Instead of building a specialized Layer 1 around execution quality, Aster focuses on accessibility, trader growth, and flexibility. The platform leans heavily into multi-chain connectivity and aggressive leverage offerings, which immediately makes it attractive to a different type of user.

Aster is designed for speed of onboarding and rapid user expansion. The experience feels much more optimized for fast-moving retail traders than institutional desks. That is not necessarily a weakness because retail-driven trading activity still dominates huge parts of crypto derivatives volume. Crypto markets remain heavily driven by speculation and momentum.

Where Hyperliquid increasingly feels like a professional trading venue, Aster feels more like a high-speed speculative trading environment. That distinction shapes everything from liquidity behavior to token demand. The platform’s broader accessibility also creates a larger funnel for attracting new traders entering the on-chain derivatives market.

One of Aster’s biggest advantages is flexibility. Users increasingly move between ecosystems instead of staying loyal to a single chain. Traders today often hold assets across Ethereum, BNB Chain, Solana, Arbitrum, Base, and multiple Layer 2 networks simultaneously. Aster is designed around that reality.

Instead of forcing users into one tightly controlled ecosystem, the platform focuses on reducing friction between chains and simplifying onboarding. That gives Aster a broader funnel for attracting new traders, especially retail users who prioritize convenience over infrastructure purity. This also changes the psychology of growth.

Hyperliquid’s ecosystem feels more vertically integrated and specialized. Aster feels more open-ended and adaptable. That flexibility can accelerate adoption during bullish market conditions because users can access the platform more easily from ecosystems they already use.

Aster became widely known for offering extremely high leverage. That is controversial. But it is also highly effective for attracting attention and trading activity. Crypto markets are heavily driven by speculation.

High leverage products naturally attract:

This creates a very different trading culture from Hyperliquid. Hyperliquid increasingly feels like a professional trading venue. Aster feels more like a high-speed speculative trading environment. That distinction shapes everything from liquidity behavior to token demand.

Aster also differentiates itself through trader-focused execution features. Hidden order systems and privacy-oriented trading mechanics appeal to users who want more flexibility in how positions are executed. This becomes increasingly important as on-chain trading grows more sophisticated. Large traders often do not want their positions fully visible in real time. Execution privacy can reduce front-running risks and improve trade quality.

ASTER’s growth model is more aggressively tied to expansion incentives.

The token benefits from:

The bullish case for ASTER is straightforward.

If Aster continues onboarding users rapidly across multiple ecosystems, the network effect could grow extremely quickly. The bearish case is also straightforward. Some critics argue that parts of Aster’s growth may be driven more by incentives than durable organic liquidity. That question will become increasingly important over time.

This is where Hyperliquid still holds a major advantage. The platform consistently delivers tighter spreads and deeper liquidity for larger trades. That matters enormously for professional users. A trader executing a seven-figure position cares far more about execution quality than flashy leverage numbers.

Hyperliquid’s order book architecture gives it stronger performance under heavy trading conditions. Aster performs well for smaller and mid-sized retail positions but generally does not match Hyperliquid’s depth at scale.

Both platforms compete aggressively on fees. But the structure of the fee systems matters.

Hyperliquid’s ecosystem increasingly looks optimized around sustainable market making and long-term liquidity efficiency. Aster leans harder into trader acquisition and growth incentives. That creates different economic dynamics. One platform prioritizes sticky liquidity. The other prioritizes expansion speed.

Both platforms offer strong user experiences compared to older DeFi trading systems. But they feel very different. Hyperliquid feels cleaner and more institutional. Aster feels faster-paced and more retail-oriented.

This affects:

Aster’s multi-chain model gives it flexibility in onboarding new ecosystems and speculative assets quickly. Hyperliquid is more selective. That selectivity can improve liquidity quality but may reduce access to newer speculative markets.

This is one of the biggest long-term questions in the entire perp DEX market.

Institutions care about:

Hyperliquid currently looks much more aligned with those priorities. Aster’s current image is more retail and leverage-driven. That does not mean institutions cannot eventually participate there. But Hyperliquid’s architecture and branding are currently better positioned for that segment.

The token battle is just as important as the exchange battle. Most traders are not only comparing where to trade. They are comparing where long-term value accrues.

The strongest argument for HYPE is that it represents exposure to infrastructure-level trading growth.

If Hyperliquid becomes a dominant settlement and liquidity layer for on-chain derivatives, HYPE could benefit from:

HYPE increasingly trades more like an infrastructure asset than a pure speculation token.

ASTER’s upside is more growth-oriented.

The token benefits from:

If Aster continues scaling aggressively, ASTER could experience very strong adoption cycles during bullish market conditions.

The market increasingly sees HYPE as a long-term infrastructure play. ASTER is viewed more as a high-growth expansion asset. Both models can succeed. But they attract different types of investors.

Neither platform is risk-free. And this is where many crypto comparisons become overly simplistic.

Critics frequently argue that Hyperliquid is not decentralized enough. Questions around validator concentration, infrastructure transparency, and sequencing remain active debates. For some users, this is not a major issue. For others, it directly challenges the platform’s decentralization narrative.

If regulators increasingly target high-leverage derivatives products, platforms with institutional ambitions could face growing scrutiny. Hyperliquid’s size and visibility may eventually make it a larger target.

Expanding beyond trading introduces execution complexity. Building an entire financial ecosystem is much harder than building a successful exchange.

One of the biggest questions surrounding Aster is whether its growth remains durable once incentives normalize. Crypto history shows that volume generated through rewards programs can disappear quickly.

Extreme leverage products attract attention, but they also attract criticism. If high-profile liquidation events occur, public perception can shift rapidly.

Multi-chain flexibility creates growth opportunities, but it can also fragment liquidity. Long-term liquidity depth matters more than temporary trading spikes.

There is no universal winner between Hyperliquid and Aster because the platforms are optimized for different trader profiles.

Hyperliquid is generally the better fit for traders who prioritize execution quality, liquidity depth, and stability. Professional users handling larger positions typically care far more about spreads, slippage, and order execution than headline leverage numbers. That is where Hyperliquid currently maintains a major advantage. The platform also increasingly appeals to institutions and sophisticated market participants because its architecture is designed around performance consistency. Its ecosystem feels structured and infrastructure-focused rather than purely speculative.

Aster appeals to a different type of trader. Retail users looking for fast-moving opportunities, aggressive leverage, and easier multi-chain access are more likely to prefer Aster’s style. The platform’s growth strategy feels much more expansion-oriented and optimized around user onboarding.

That difference creates two very different trading cultures. Hyperliquid increasingly resembles a professional trading venue built around liquidity efficiency. Aster feels more like a fast-paced speculative environment optimized for momentum traders and higher-risk users.

For beginners, Hyperliquid is generally the safer starting point because liquidity conditions tend to be stronger and the platform feels more structured overall. But leverage trading remains extremely risky regardless of platform. The most important thing for newer traders is understanding that execution quality matters just as much as leverage availability. High leverage can amplify profits quickly, but it also accelerates liquidations during volatility.

A few years ago, that question sounded unrealistic. Today, it sounds much more plausible.

Perpetual DEXs are improving rapidly across:

The gap between centralized and decentralized trading is shrinking. That does not mean centralized exchanges disappear. But it does mean the market structure is changing. The next generation of crypto traders increasingly expects:

Platforms like Hyperliquid and Aster are early examples of that shift. But competition is intensifying quickly.

Other players like:

are all trying to capture pieces of the same market. This is likely only the beginning of the perp DEX expansion cycle.

Hyperliquid and Aster are both winning. But they are winning in different ways. Hyperliquid currently looks stronger structurally. Its liquidity, execution quality, and institutional positioning give it one of the strongest moats in on-chain trading today. It increasingly feels less like a speculative app and more like foundational financial infrastructure.

Aster, meanwhile, is growing through accessibility, leverage, and aggressive retail expansion. Its multi-chain flexibility gives it a much broader onboarding funnel, especially during high-speculation market conditions. The real question is not whether one platform completely eliminates the other.

The real question is whether the future of perp trading becomes:

Right now, Hyperliquid looks better positioned for long-term dominance. But crypto markets move fast. And in the perp DEX wars, momentum can shift much faster than most traders expect.