Trace evolution of DePIN from storage to AI and machines. See why DePIN is not dead in 2026 and how it’s building lasting infrastructure.

Author: Arushi Garg

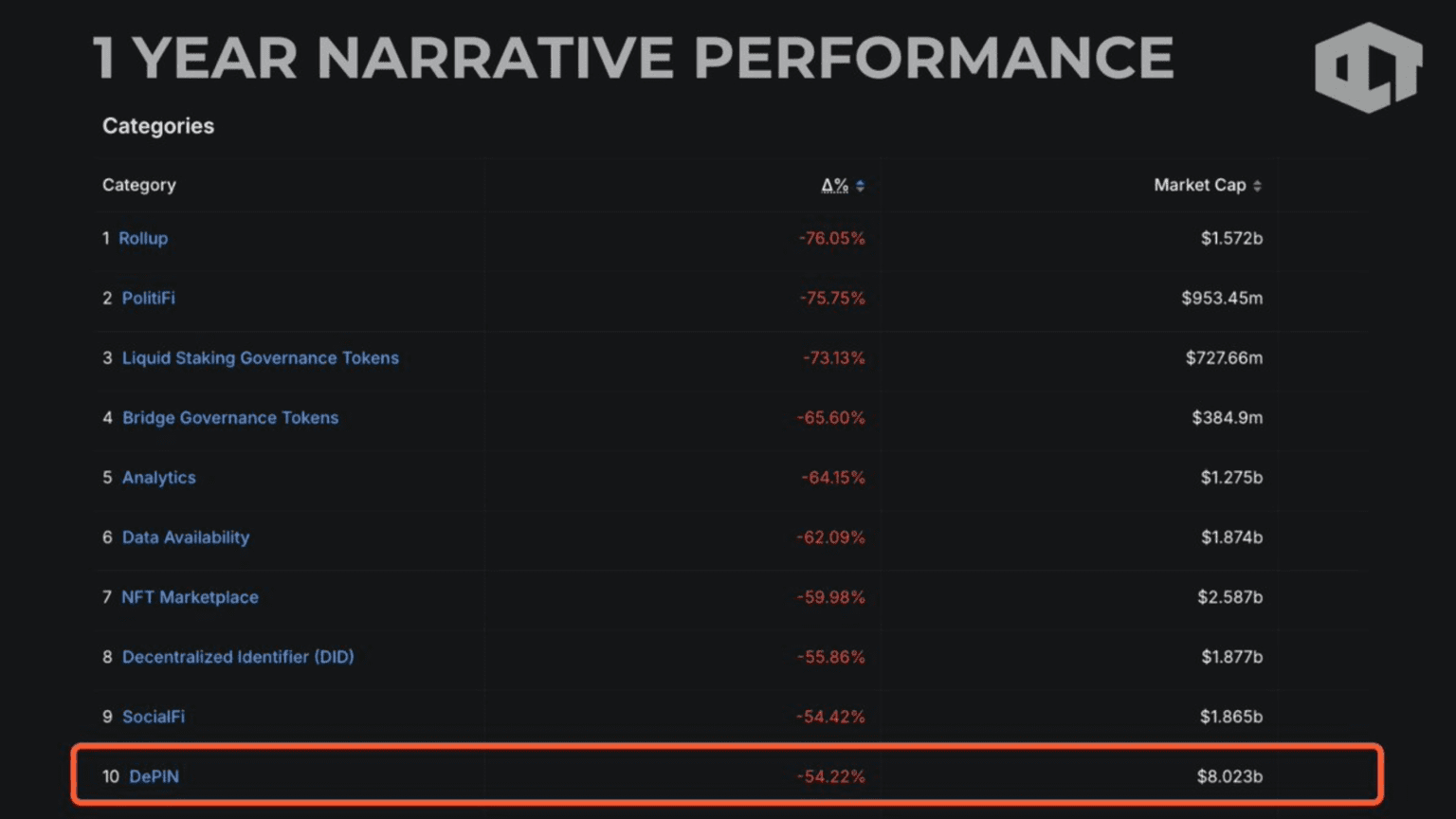

You’ve seen the posts and the charts. DePIN tokens are down over 70% from their November 2021 peak, according to CoinGecko data, across leading networks including Filecoin, Helium, and Render Network. Capital has rotated from AI memes to RWA and now to whatever is trending this week. Judging DePIN purely by price action is the first mistake, because infrastructure should not be measured by token value alone. The evolution of DePIN shows a deeper story.

This article is not here to defend every DePIN token. Some deserved to lose value. Some were poorly designed and underdelivered. Instead, we take a more useful approach. the article traces how DePIN has evolved and trace how DePIN has evolved, wave by wave. We will separate speculation from infrastructure and focus on the fundamentals.

Finally, we will answer the crucial question. Is DePIN dead in 2026? Or is it simply shape-shifting for the next phase of growth?

No. While DePIN token prices have declined, infrastructure deployment and enterprise adoption continue to grow. Networks remain operational, and real-world coordination is expanding across storage, compute, sensors, and machine fleets. The term was formally popularized by Messari in 2022, but the coordination architecture behind it existed long before it had a label.

A DePIN network introduces a structurally radical concept. It replaces centralized capital expenditure with distributed economic incentives. Instead of raising hundreds of millions in venture funding to deploy servers, wireless towers, sensors, GPUs, or devices, it invites individuals to contribute resources directly and compensates them in tokens. The token is not merely for speculative upside. It is the coordination mechanism. It serves as the economic bridge between early resource providers and future demand. This is where most people get confused.

DePIN is not a sector in the traditional sense. It is not limited to “storage coins,” “wireless tokens,” or “AI GPU plays.” It is a coordination model that can be applied to any physical bottleneck where centralized infrastructure is expensive, slow to scale, or geographically constrained.

For the model to work sustainably, three conditions must align. First, the contributed resource must be verifiable. Second, there must be genuine demand for that resource. Third, token incentives must bridge the cold-start phase without permanently replacing revenue.

When these conditions are met, the result is functional infrastructure. When they are not, it results in emission cycles. The early years of DePIN were experiments to identify which bottlenecks could satisfy these conditions. Some succeeded. Some failed. However, the failures are often mistaken for structural invalidation.

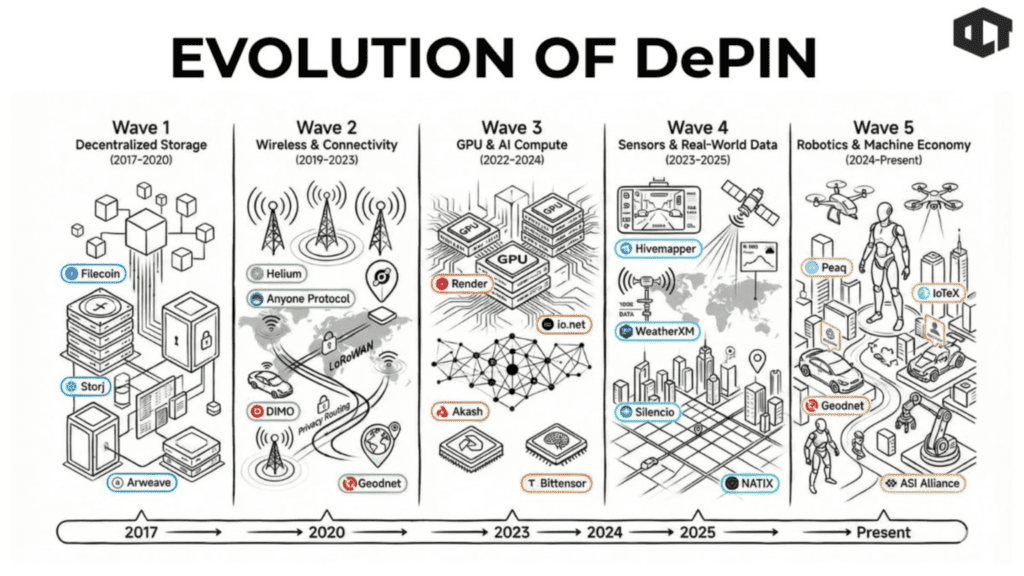

To understand DePIN fully, it is essential to revisit its waves of evolution.

Before the term DePIN existed, the earliest large-scale experiments were in decentralized storage. In the late 2010s, cloud infrastructure was dominated by Amazon, Google, and Microsoft. Centralized hyperscale data centers offered advantages in reliability and pricing power, but they also carried concentration risk, censorship vulnerability, and high upfront capital requirements.

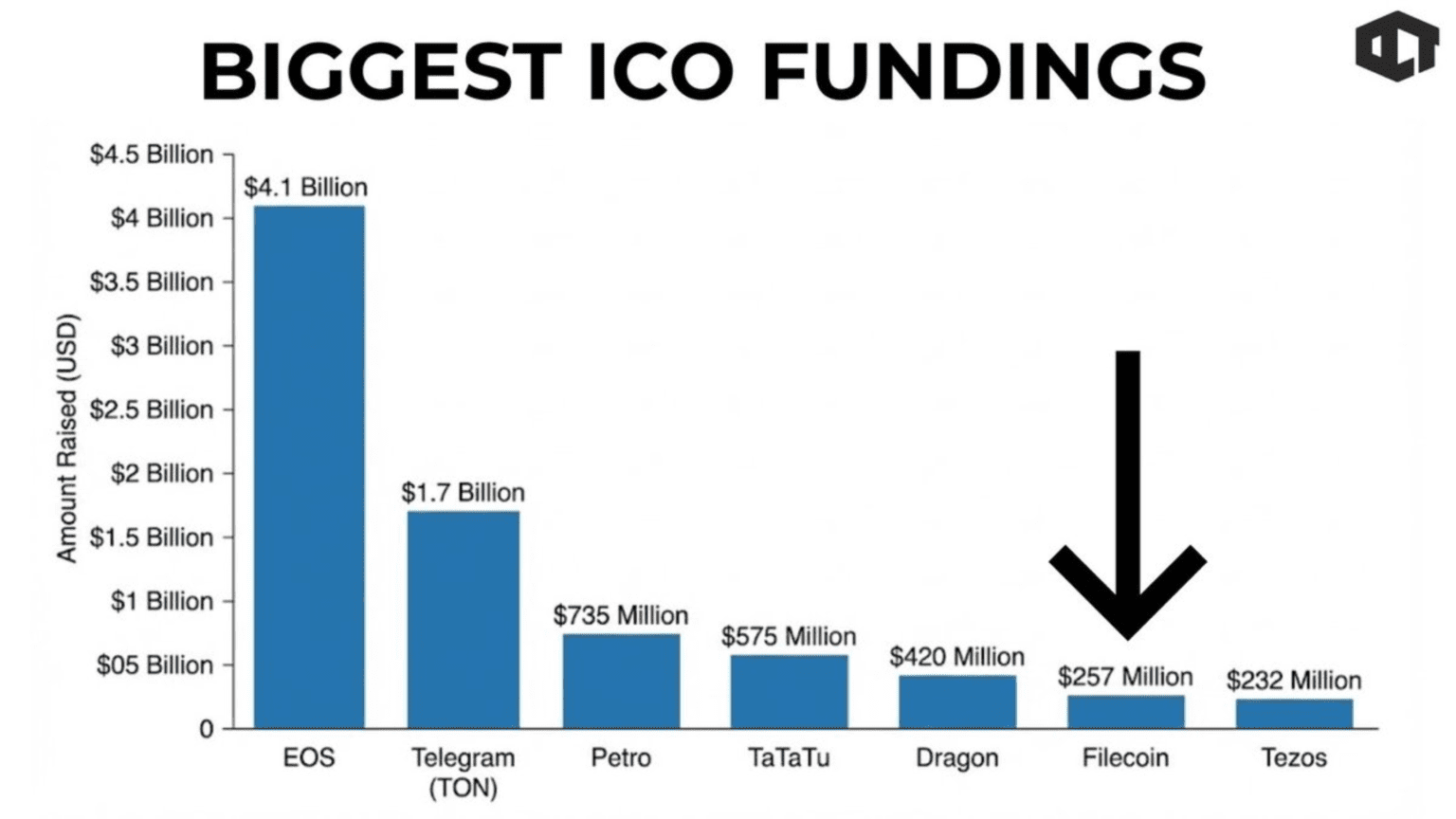

geodAt the same time, individuals around the world had vast amounts of unused storage capacity. The idea behind Wave One was simple: create a marketplace where spare hard drive space could be monetized. Filecoin became the flagship project of this movement. Its 2017 token sale raised $257 million, making it one of the largest initial coin offerings in history.

More importantly, Wave One introduced novel cryptographic proofs such as Proof of Replication and Proof of Spacetime. These mechanisms allowed the network to verify that storage providers were genuinely storing client data. Storj positioned itself as a decentralized alternative to Amazon S3, offering a viable competitor in the cloud storage market.

At the same time, Arweave introduced permanent storage through a one-time fee model. This approach later became critical for ensuring NFT metadata permanence and long-term digital asset reliability.

Around the same time, Render Network created by OTOY founder Jules Urbach, began connecting idle GPU owners with artists who required rendering capacity. Although technically compute, its architecture followed the same distributed incentive logic as storage networks. Token prices experienced dramatic cycles, and speculative capital certainly flowed in and rotated out. Yet, something more important happened beneath the volatility. Petabytes of storage capacity were deployed, thousands of nodes went live, real data was stored, and real workloads were processed. The coordination model demonstrated that distributed hardware could be verified and incentivized at scale.

The first wave did not solve every challenge. Cold-start demand remained difficult, enterprise adoption lagged behind retail enthusiasm, and emissions were high relative to revenue. Infrastructure was built, and that distinction matters because infrastructure tends to outlast its speculative overlay.

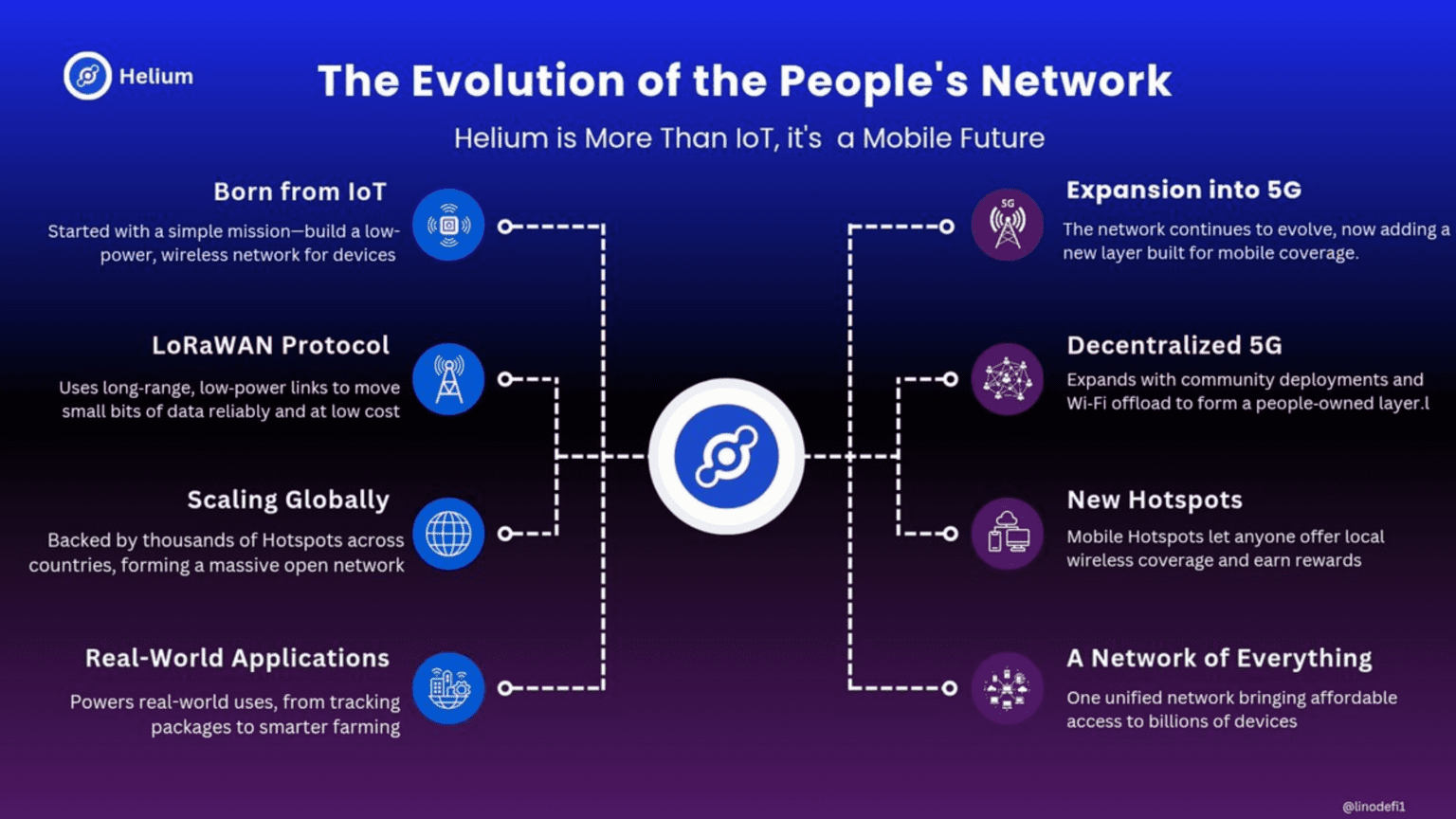

While storage networks targeted centralized cloud monopolies, the second wave focused on telecom and sensor bottlenecks. Helium introduced a deceptively elegant concept: individuals could deploy LoRaWAN hotspots, provide network coverage, and earn tokens. Instead of telecom companies slowly expanding coverage based on projected ROI, token incentives accelerated global deployment.

At its peak, Helium coordinated nearly one million hotspots worldwide. Economic tensions soon emerged. The supply of hotspots grew faster than IoT data demand, while token emissions subsidized participation and real-world usage fees lagged behind hardware growth. Speculation outpaced revenue, and prices corrected. Critics declared the experiment a failure.

Yet the network did not vanish. Helium migrated to Solana to improve performance and reduce friction, expanded into mobile services, and formed telecom partnerships. The key lesson was not that DePIN failed, but that supply-side bootstrapping must eventually converge with real demand.

Other projects refined the sensor model in parallel. DIMO incentivized vehicle telemetry collection, Hivemapper crowdsourced street-level imagery, and GEODNET built a global precision GPS correction network enabling centimeter-level positioning for drones and robotics. These were not speculative abstractions. They were distributed physical networks capturing real-world data. The second wave successfully expanded the DePIN model from digital resources into physical sensor economies.

Then an external force reshaped the landscape.

The public launch of ChatGPT by OpenAI triggered a surge in global demand for AI compute. NVIDIA GPUs became strategic assets, cloud providers struggled with capacity shortages, and compute prices soared.

For the first time, DePIN networks were not merely pushing supply through token emissions. They were being pulled by overwhelming external demand. Render Network pivoted toward AI inference workloads, Akash Network gained renewed relevance, and Bittensor experimented with decentralized AI training incentives.

This wave was fundamentally different from previous ones. Demand existed before token speculation accelerated. Enterprises required compute capacity immediately, providing strong validation for the DePIN coordination model. Even after AI token hype cooled, workloads continued, providers stayed online, and revenue persisted. According to Render Network deployment data, Q1 2024 was a peak onboarding period for AI-focused compute providers.

The AI wave showed that DePIN performs best when external industries face acute bottlenecks. However, it also highlighted a key limitation. Compute without high-quality data is constrained. Synthetic data eventually saturates, making real-world, verifiable data increasingly valuable. This insight pushed DePIN into its next phase.

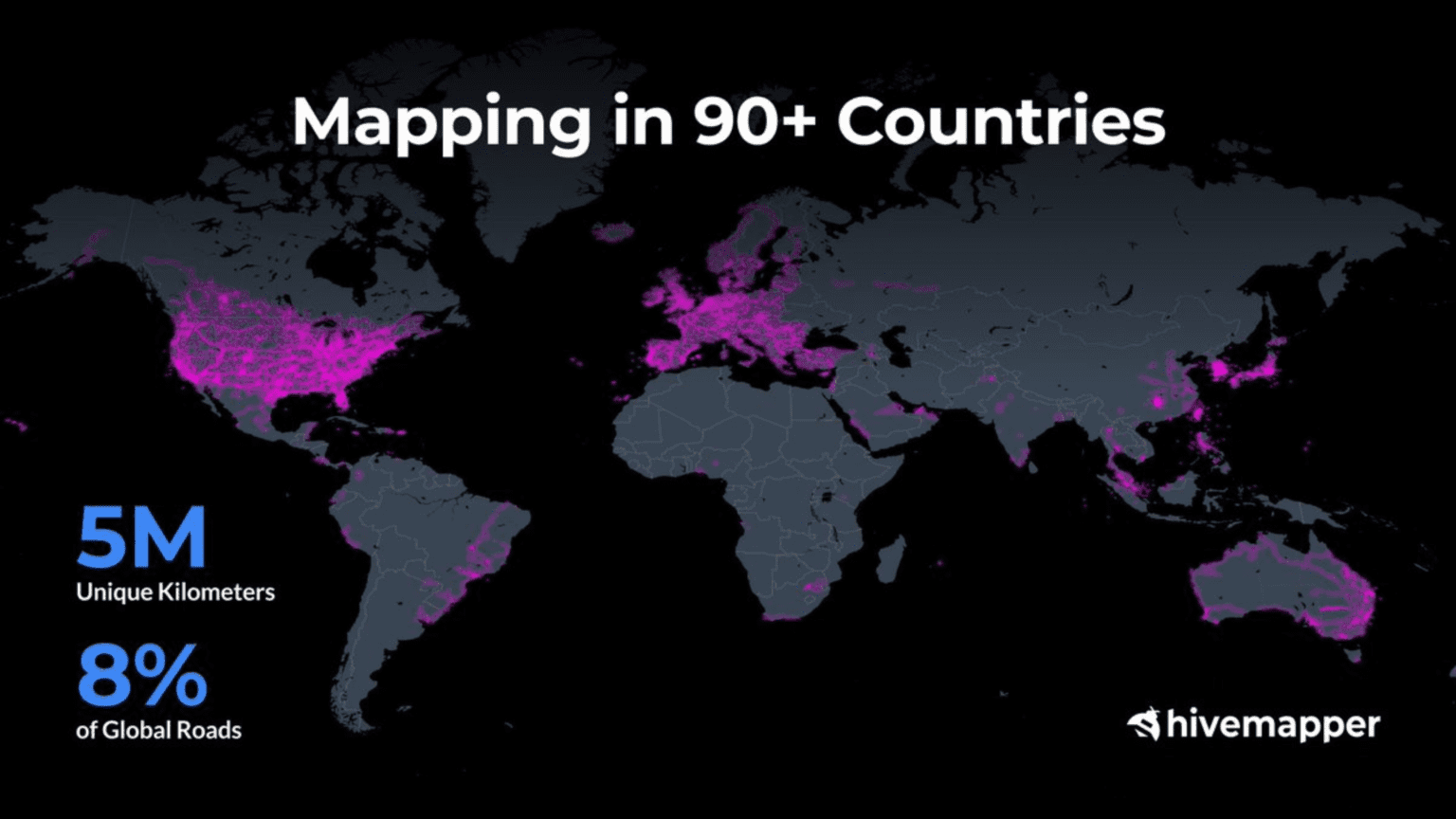

While much of crypto debated whether AI tokens were overvalued, DePIN was quietly evolving beyond virtual resources such as storage and GPUs into real-world data capture. This shift made the sector much harder to dismiss. Once information that cannot be replicated digitally is collected, the resulting network becomes defensible. Hivemapper serves as a clear example of this transition.

Instead of building expensive mapping fleets like Google, Hivemapper incentivized drivers to mount dashcams and contribute street-level imagery. This approach creates a living, continuously updated global map. No centralized company can economically deploy millions of vehicles for such coverage, but a token-incentivized network can.

WeatherXM operates on a similar principle. Individuals own physical weather stations distributed globally, feeding hyperlocal climate data into a decentralized network. That information is valuable to insurance companies, agricultural firms, and government agencies.

Wingbits applies the model to aviation. It pays contributors to operate ADS-B receivers that track aircraft in real time, feeding data into a decentralized aviation tracking network. Again, centralized competitors face massive capital requirements, whereas tokenized networks leverage coordination to scale.

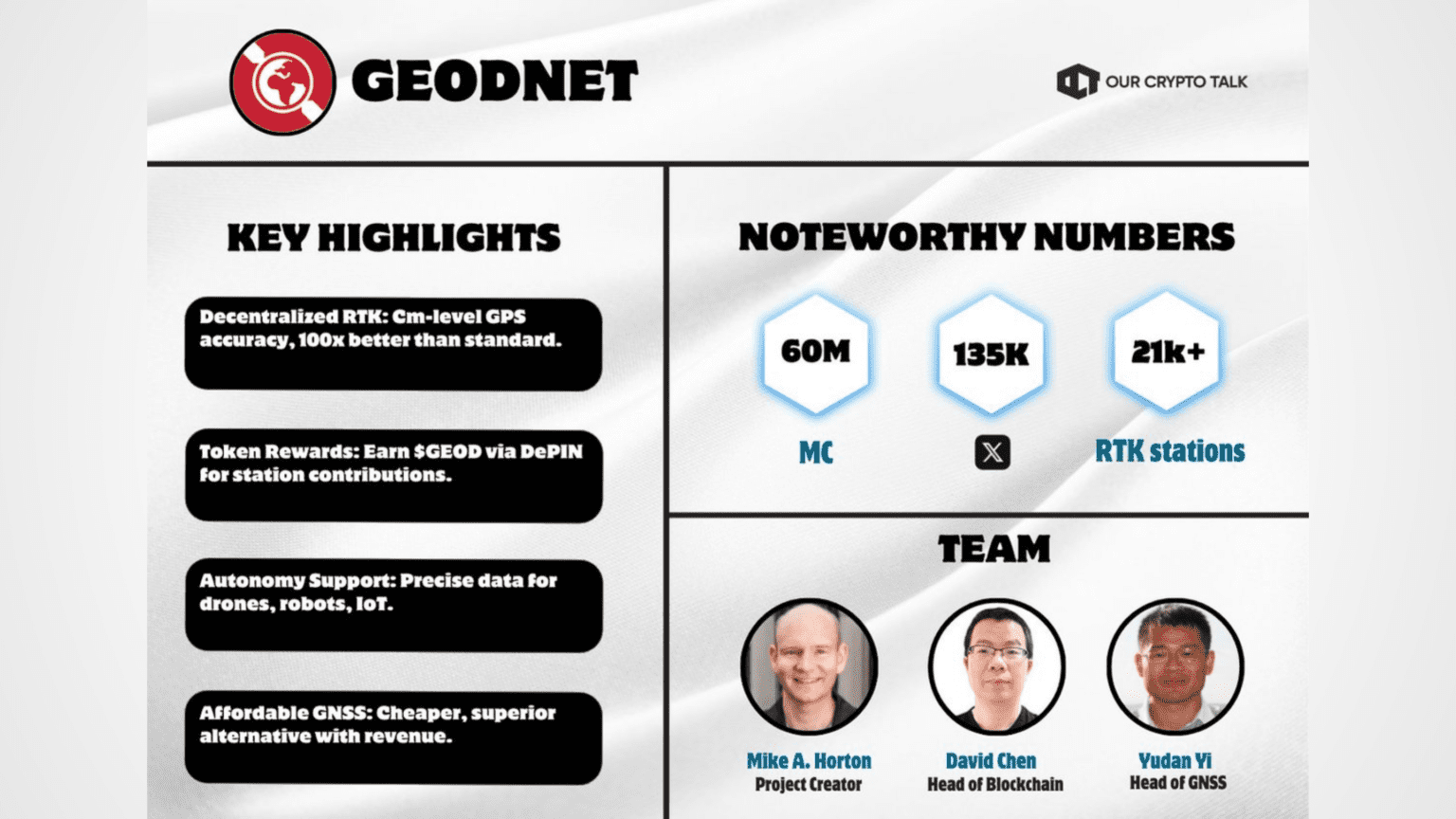

Geodnet is another critical example. Its precision GPS correction data, though not glamorous, is essential for drones, robotics, surveying, and autonomous systems, demonstrating how DePIN can deliver highly defensible, real-world infrastructure.

Geodnet built a distributed reference station network that delivers centimeter-level positioning accuracy at a fraction of the cost of traditional infrastructure. Geodnet generated consistent annual revenue through enterprise GPS correction services. This highlights a critical point: the sensor wave shifted DePIN from subsidized supply experiments to real-world data businesses.

Once the data exists, its value increases, especially in an AI-driven world. AI models require massive, high-quality, real-world data, while synthetic data eventually saturates. Environmental data, mobility data, mapping data, and precision positioning data are now premium assets, and structural demand does not disappear even as retail investors rotate to the next narrative.

The fifth wave is the most abstract and transformative. Unlike earlier waves, which focused on underutilized resources such as spare storage, idle GPUs, excess bandwidth, dashcams, GPS receivers, or weather stations, the fifth wave centers on machines that actively generate economic value through operations in real-world environments.

As robotics, drones, and AI-driven automation scale globally, DePIN infrastructure is no longer just about data or compute; it is about fleets of physical devices operating semi-independently in the real world.

Delivery drones navigate urban environments, autonomous tractors operate farmland, warehouse robots move inventory, and smart energy systems balance distributed loads. These examples illustrate a structural question: who owns these machines, who coordinates them, and who captures the value they generate? Traditionally, corporations with capital-intensive deployment strategies controlled this infrastructure.

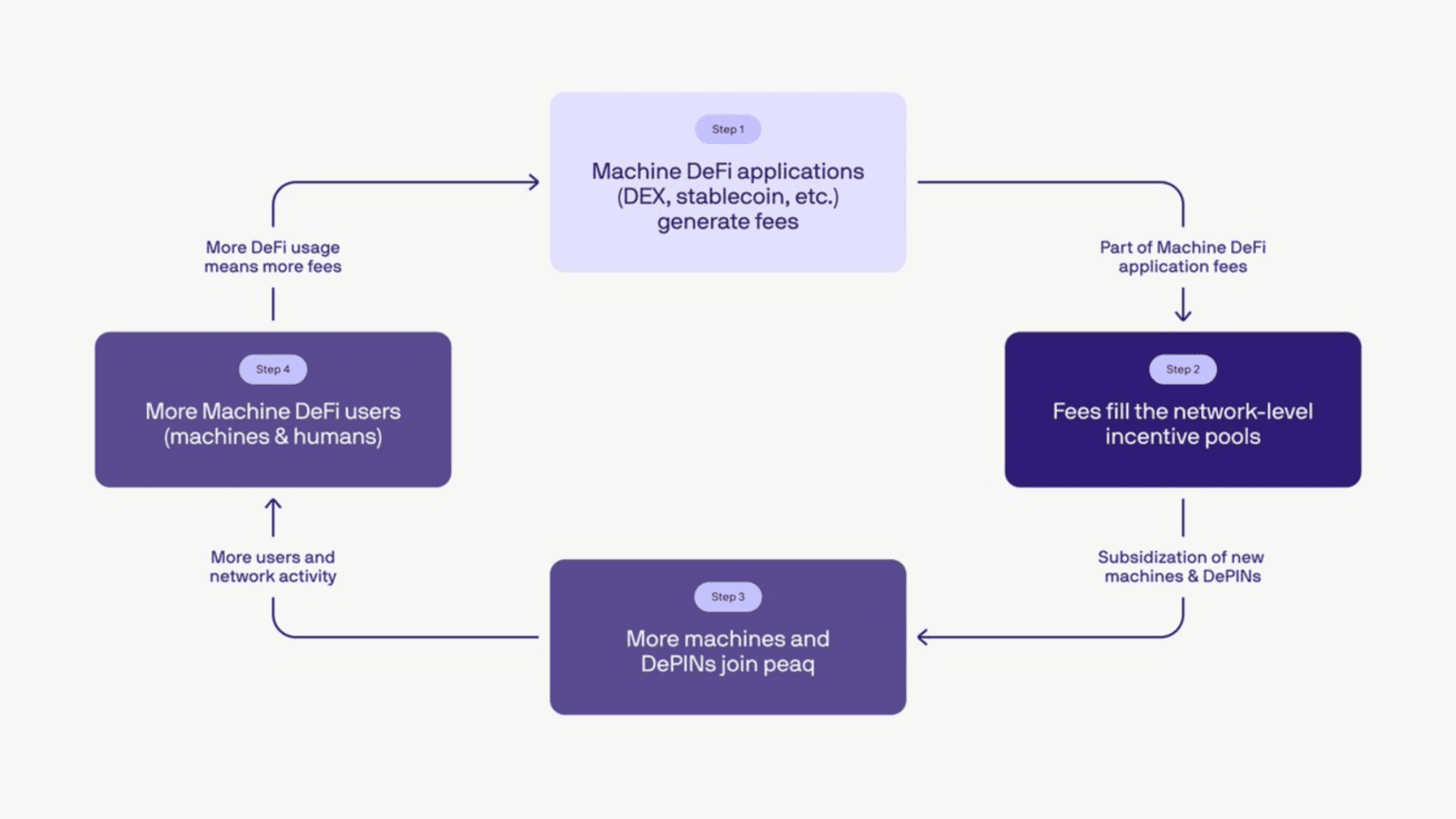

DePIN introduces an alternative. Peaq provides infrastructure for the machine economy, enabling devices to receive on-chain identities. Machines can authenticate, transact, and settle revenue autonomously, while multiple stakeholders can co-own the revenue streams generated by the hardware.

By 2025 and 2026, millions of connected devices were integrated across ecosystems experimenting with machine-level coordination. Robotics SDKs began allowing developers to plug physical devices directly into blockchain-based economic systems. Governments in regions such as the UAE explored frameworks for automated delivery fleets and smart city infrastructure.

The economic logic is compelling. Machines are becoming productive capital units. If token coordination can enable distributed ownership and incentivized maintenance, DePIN shifts from coordinating spare resources to managing active capital assets. This is a material upgrade in ambition. Unlike earlier waves, this phase does not rely primarily on emissions to attract participants. The incentive is embedded in the revenue generated by the machine itself. A delivery drone earning fees for completing routes does not require speculative token emissions to justify its existence. It relies on operational efficiency and demand for delivery.

This introduces a structural maturity that earlier waves lacked. The machine economy intersects directly with broader macro trends, including global labor shortages, rising logistics costs, urban density challenges, energy optimization pressures, and government incentives for automation in infrastructure-heavy sectors. If DePIN can embed coordination logic into machine fleets, it transforms from a speculative experiment into a capital allocation framework.

Critics often dismiss this wave because it does not produce immediate token price explosions. It moves slower, requiring hardware manufacturing, regulatory engagement, insurance frameworks, and enterprise integration. But slowness does not imply weakness. It signals a shift from narrative-driven velocity to industrial integration. The fifth wave is no longer about spare GPUs or subsidized hotspots. It is about programmable machines operating in real economies, representing a structural escalation and setting up the next frontier.

When people say DePIN is dead, they usually mean the speculative phase is over and rapid multiple expansion has slowed. They are not evaluating whether decentralized storage networks continue storing data, GPU marketplaces still process workloads, or precision positioning networks are selling enterprise subscriptions. Instead, they are reacting to price compression and reduced token velocity. Price momentum is cyclical, and the tokens are performing according to market conditions.

Infrastructure deployment is not speculative. It is important to be honest about how the early DePIN cycles behaved. Many networks over-incentivized supply because they had to. Hotspot operators deployed hardware because token emissions were attractive. Storage miners added capacity because yields justified the risk. GPU providers joined because narrative momentum amplified expected upside. That behavior was not irrational; it was a necessary mechanism for solving the cold-start problem.

However, once emissions decline and speculative enthusiasm cools, networks face their true test. They must prove that demand exists independent of token rewards. Customers must be willing to pay for the underlying resource rather than for exposure to the token. Some projects fail at this stage because they never built a bridge between subsidized supply and organic demand. Others survive because their resource becomes economically useful beyond speculation.

Projects that endure often appear less exciting because revenue growth is slower than token appreciation during a bull cycle. They may look boring compared to the explosive upside of early narrative phases. But infrastructure generating steady revenue tends to outlast infrastructure that depends entirely on emissions. Calling DePIN dead at this stage is less an analytical conclusion and more a reflection of reduced speculative upside.

The part that receives the least attention in public discourse is what continues to grow during downturns. Filecoin continues to store large datasets. Render Network continues processing rendering and inference workloads. GEODNET continues expanding its global station deployments. Helium Mobile continues growing subscribers under the broader Helium ecosystem. AI-focused GPU marketplaces continue onboarding providers. Machine-focused ecosystems continue integrating devices into programmable economic systems. Meanwhile, token prices fluctuate as capital reallocates across narratives.

Market capitalization contraction does not automatically indicate infrastructure contraction; it often indicates that speculative liquidity has rotated elsewhere. This distinction becomes crucial when narrative cycles shift back toward fundamentals. Networks that generate measurable revenue, maintain active hardware deployments, and continue onboarding enterprise demand will look materially different from networks that never transitioned beyond emissions. Price charts reflect liquidity; infrastructure metrics reflect durability.

If DePIN were structurally invalid, we would observe widespread hardware shutdowns, collapsing enterprise contracts, declining device counts, and fading developer ecosystems. That pattern is not visible. Instead, what we see is consolidation, revenue optimization, reduced emissions schedules, and increasing focus on enterprise integration. Regulatory experimentation is also expanding in jurisdictions exploring automation and distributed infrastructure. The next logical expansion vector for DePIN is energy.

Distributed solar installations, home battery systems, microgrids, and peer-to-peer energy markets represent one of the largest infrastructure categories in the global economy. If DePIN coordination models can be applied to distributed energy assets, the potential scale exceeds that of storage and wireless networks combined. Edge compute presents another frontier, particularly as AI processing moves closer to devices instead of remaining centralized in hyperscale data centers.

Environmental monitoring, autonomous logistics, and industrial IoT systems all contain physical bottlenecks that can potentially be coordinated through tokenized incentives. The DePIN coordination model adapts wherever distributed contributors can challenge centralized capital concentration.

No. It is no longer a meme-driven narrative promising rapid token appreciation. The sector has transitioned into a structural infrastructure thesis that requires patience and evaluation through different metrics. Structural theses move slower than hype cycles, compounding through deployment rather than speculation.

Every wave of DePIN has left infrastructure behind. Storage networks continue operating. Wireless deployments persist. Compute marketplaces process workloads. Sensor networks capture data. Machine ecosystems coordinate devices. This cumulative progress does not happen by accident. It emerges when incentives, cryptographic verification, and real-world demand intersect.

The early years were experimental. The middle years were narrative driven. The current phase resembles consolidation. Consolidation is uncomfortable for traders because it lacks explosive upside. However, it is often where durability is built. The relevant question is not whether DePIN survives as a narrative.

The relevant question is whether the coordination model continues finding real-world bottlenecks where distributed capital can compete with centralized incumbents. If the answer is yes, the sector is not dying. It is maturing. Maturation rarely produces dramatic headlines, but it often produces lasting infrastructure.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.