An in-depth analysis of Re, which has grown to $465M TVL, covering insurance-backed yield, tokenomics, competition, and catalysts.

Author: Akshat Thakur

Re is an onchain reinsurance protocol that connects stablecoin capital to regulated insurance markets. Instead of generating yield from trading activity or token emissions, Re generates yield from real insurance premiums collected through licensed reinsurance treaties.

Users deposit assets such as USDC, USDe, or sUSDe into the Insurance Capital Layer and receive either reUSD or reUSDe. reUSD acts as the senior tranche, targeting lower-risk yield with greater liquidity. reUSDe acts as the junior tranche, absorbs more risk, and targets higher returns. Capital flows through Surplus Notes and Section 114 Trust structures that qualify as admitted collateral for licensed U.S. reinsurers.

The structure matters because it creates a clear loss hierarchy. Reinsurer equity absorbs losses first, followed by reUSDe and then reUSD. This design gives senior capital additional protection while still exposing the protocol to real underwriting profits rather than synthetic crypto yields.

Transparency remains central to the model. Chainlink-powered attestations publish reserves, premiums, claims, and portfolio performance onchain. As of June 2026, Re reports approximately $465.69 million in TVL, including $80.37 million in onchain capital, $177.45 million in offchain capital, and $207.87 million in premium receivables.

The timing is important. Global reinsurance capital continues to grow, yet the industry still operates through closed institutional networks that exclude most investors. At the same time, stablecoins have matured into institutional-scale financial infrastructure and tokenized real-world assets have moved beyond proof-of-concept.

Re sits at the intersection of those trends. It gives onchain capital access to an asset class that historically remained available only to insurers, pension funds, and large institutions. That makes Re less of a DeFi yield product and more of a bridge between crypto liquidity and one of the world’s largest financial markets.

Re operates between two very different groups of competitors.

On the crypto side, Nexus Mutual remains the most established insurance protocol. It provides coverage against smart contract exploits, custodial failures, and other crypto-native risks. Several smaller insurance projects also exist, but most focus on DeFi protection, parametric insurance, or synthetic risk markets rather than real-world underwriting.

On the traditional side, firms such as Lloyd’s, Swiss Re, and Munich Re dominate the global reinsurance industry. These companies manage enormous amounts of capital and decades of actuarial expertise. However, they operate through closed institutional networks and offer little transparency or accessibility to crypto-native investors.

Re’s core differentiator is its ability to bridge those two worlds. The protocol does not insure DeFi protocols or create synthetic exposure. Instead, it gives stablecoin holders access to real insurance premiums through regulated reinsurance structures.

The model combines licensed carriers, Surplus Notes, Section 114 Trusts, and tokenized tranches with onchain transparency. Users can access reUSD and reUSDe while benefiting from daily reserve attestations and integration with DeFi platforms such as Curve, Pendle, and Morpho.

The biggest advantage may be the regulatory moat. Traditional reinsurers cannot easily open their balance sheets to crypto capital without navigating complex solvency and compliance requirements. Meanwhile, most crypto insurance projects lack access to admitted collateral structures and real carrier relationships.

That leaves Re in a relatively unique position. It combines regulatory infrastructure, real-world underwriting exposure, and DeFi composability within a single framework. As of mid-2026, few projects have achieved similar scale, transparency, and institutional integration simultaneously.

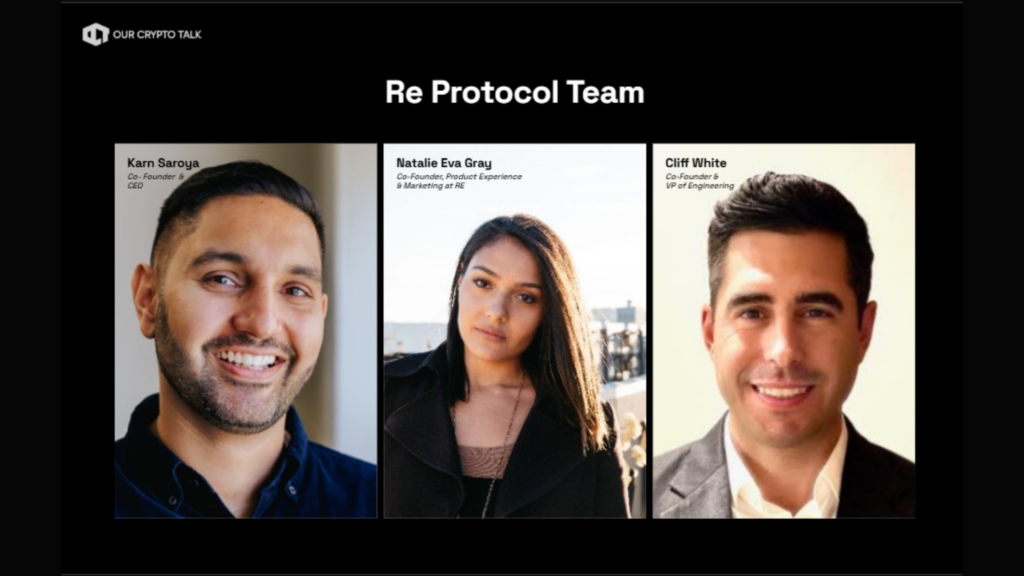

The team behind Re comes from the insurance industry rather than traditional crypto circles. That background matters because reinsurance requires expertise in regulation, risk management, and capital markets as much as software development.

Founder and CEO Karn Saroya previously co-founded Cover.com, a venture-backed insurance platform that operated as a licensed brokerage in the United States. Before Cover, he founded Stylekick, which Shopify acquired in 2015. He also worked in financial services consulting and holds graduate finance credentials from MIT.

Saroya’s experience gives Re something many blockchain projects lack: direct exposure to insurance regulation and underwriting operations. Building a reinsurance platform requires much more than token engineering. Teams must understand carrier relationships, trust structures, solvency requirements, and claims management.

The broader leadership team includes Natalie Gray, who co-founded Cover and now leads Product Experience & Marketing at Re. Several key engineers, including Cliff White, Ben Aneesh, and Anand Dhillon, also Co-founded Cover before joining Re.

The company remains relatively small, with fewer than a dozen full-time employees as of 2026. Despite that size, the team has secured relationships with more than 30 insurance carriers and several major global reinsurance brokers.

Perhaps the most important signal is continuity. The team spent years building insurance products before pivoting toward onchain reinsurance. Rather than entering insurance from crypto, they entered crypto from insurance.

That explain why Re has progressed from concept to hundreds of millions of dollars in deployed capital while maintaining a regulatory-first approach. In a sector where many projects remain theoretical, Re’s team brings direct experience from the industry it aims to modernize.

This is not a whitepaper project. Re is fully live on mainnet and already deploys stablecoin capital into regulated reinsurance treaties.

Users can visit app.re.xyz today, complete KYC verification, deposit supported stablecoins, and mint either reUSD or reUSDe. The protocol currently operates across Ethereum, Avalanche, Arbitrum, Base, BNB Chain, Ink, and Katana. The product is functional, capitalized, and actively generating yield from insurance premiums rather than token incentives.

Transparency is one of Re’s strongest features. The platform publishes daily reserve, premium, claims, and NAV data through Chainlink-powered attestations. Users can also monitor redemption capacity, portfolio allocation, and solvency metrics through the protocol’s public dashboards.

The protocol currently supports approximately $195.92 million in deposits across its live products, including $176.24 million in reUSD deposits and $19.68 million in reUSDe deposits. The protocol supports dozens of live insurance programs and reinsures hundreds of thousands of policyholders across the United States.

The architecture combines onchain transparency with offchain regulatory compliance. Licensed carriers, trust structures, and admitted collateral remain within traditional insurance frameworks, while balances and performance data appear onchain for verification.

Public GitHub activity remains limited. That may frustrate crypto-native users who prefer open development. However, regulated insurance infrastructure operates differently from most DeFi protocols. Re focuses on audited production systems, legal structures, and third-party attestations rather than shipping features through public repositories.

The simplest test is whether users can interact with the product today. They can. Capital is live, yield is live, and the protocol has operated at meaningful scale for years. Re passes the “are they shipping?” test without relying on a testnet, waitlist, or future roadmap.

Re has assembled a funding base that reflects both its crypto ambitions and its insurance roots.

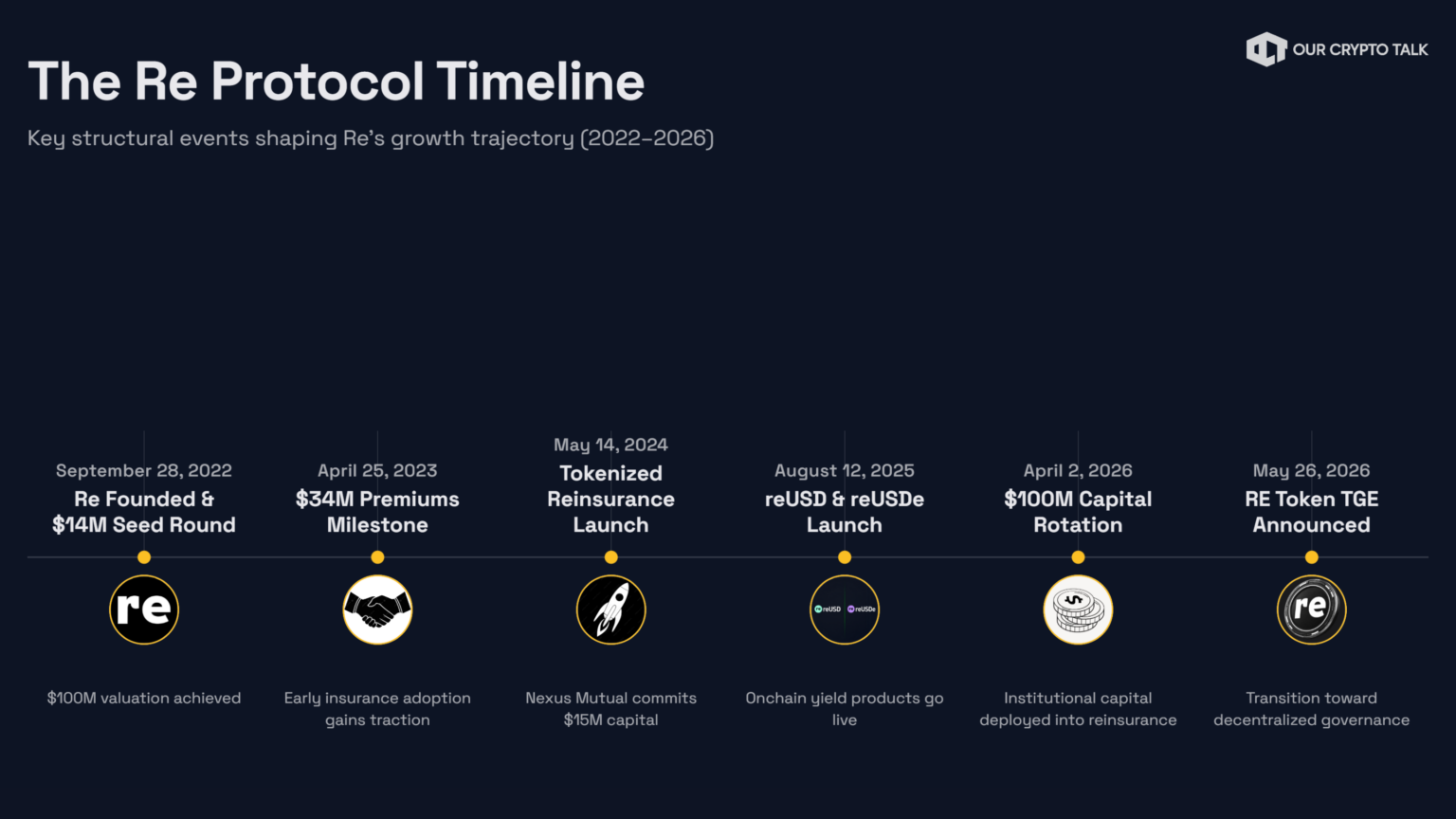

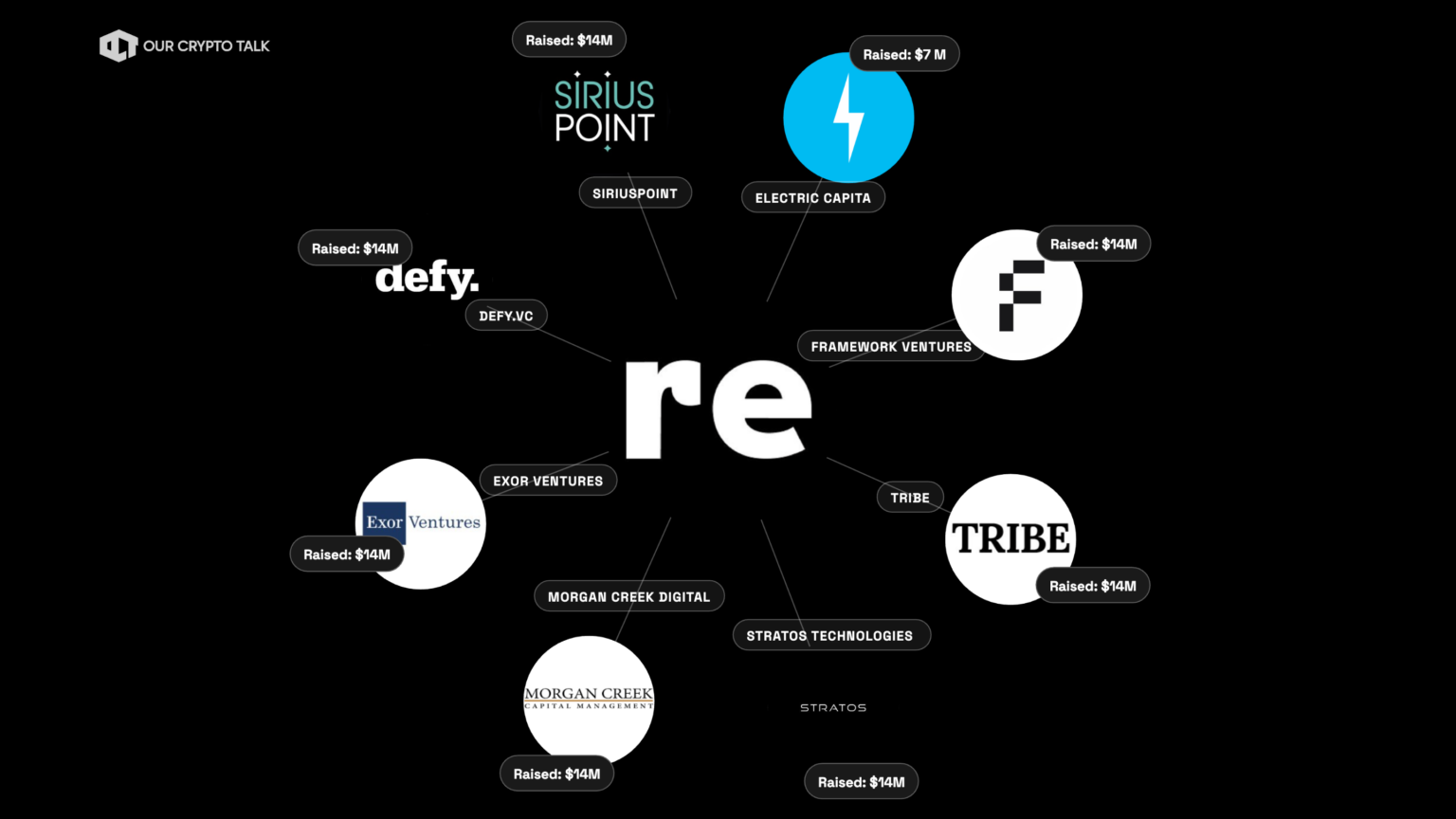

The company raised a $14 million seed round in 2022 led by a mix of crypto-native investors, venture capital firms, and insurance-focused institutions. Key participants included Tribe Capital, Framework Ventures, Morgan Creek Digital, Defy VC, Stratos, Exor, and SiriusPoint.

The composition of that investor group is notable. Framework and Morgan Creek bring deep experience in digital assets and token networks. SiriusPoint contributes expertise from the global reinsurance industry. Exor adds long-term institutional capital through one of Europe’s most established investment groups.

This combination provides more than funding. It gives Re access to strategic relationships across both insurance and crypto markets. That advantage matters because the protocol depends on regulatory compliance, carrier partnerships, and long-term capital formation.

The Resilience Foundation also plays a role in supporting governance and ecosystem development. Together, the foundation and investor base provide a structure designed to support the protocol beyond its token launch.

Re continued to attract investor interest in May 2024, securing an additional $7 million funding round led by Electric Capital. This follow-on raise further strengthened the project’s financial position and demonstrated continued confidence from investors in Re’s vision of bringing reinsurance on-chain.

For pre-token projects, funding often serves as a credibility signal. Re’s backers span insurance, venture capital, and crypto infrastructure rather than a single niche. That diversity suggests investors view the project as more than another yield protocol.

The stronger takeaway is not the amount raised but who participated. Re attracted investors who understand underwriting risk, regulatory requirements, and tokenized capital markets. That alignment significantly increases the project’s ability to scale its reinsurance model over the long term.

Most crypto projects lead with vanity metrics. Re’s strongest numbers cost participants real money.

The clearest signal is capital commitment. Approximately $195.92 million in stablecoin deposits currently sit inside the protocol.

Re reports approximately $465.69 million in total value locked, including $207.87 million in premium receivables tied to active underwriting activity. Those numbers reflect actual underwriting activity rather than speculative token demand.

Another useful metric is realized performance. Since launch, Re has distributed more than $5.7 million in cumulative yield to reUSD and reUSDe holders. Unlike projected APYs, this reflects actual value returned to participants.

The third signal is distribution. The protocol works with more than 30 insurance carriers and reinsures over 700,000 policyholders across dozens of active programs. Large global brokers including Lockton Re, Howden, Gallagher Re, and Guy Carpenter have also participated in the ecosystem.

Participation quality matters too. Re reports roughly 4,000 verified onchain participants. That number may look small compared with typical DeFi projects, but every participant completed compliance checks and contributed real capital.

Now compare that with the usual crypto metrics.

Follower counts cost nothing. Discord members cost nothing. Testnet wallets cost nothing. Most can be inflated through incentives, bots, or farming campaigns.

Re’s points program exists, but it remains secondary to the core product. Users earn points through deposits, referrals, and ecosystem participation. However, the protocol’s strongest traction signal remains capital at risk rather than points earned.

A points leaderboard proves attention. More than $191 million in deposited capital proves conviction. That distinction matters. Demand can come from marketing. Capital commitment usually comes from trust.

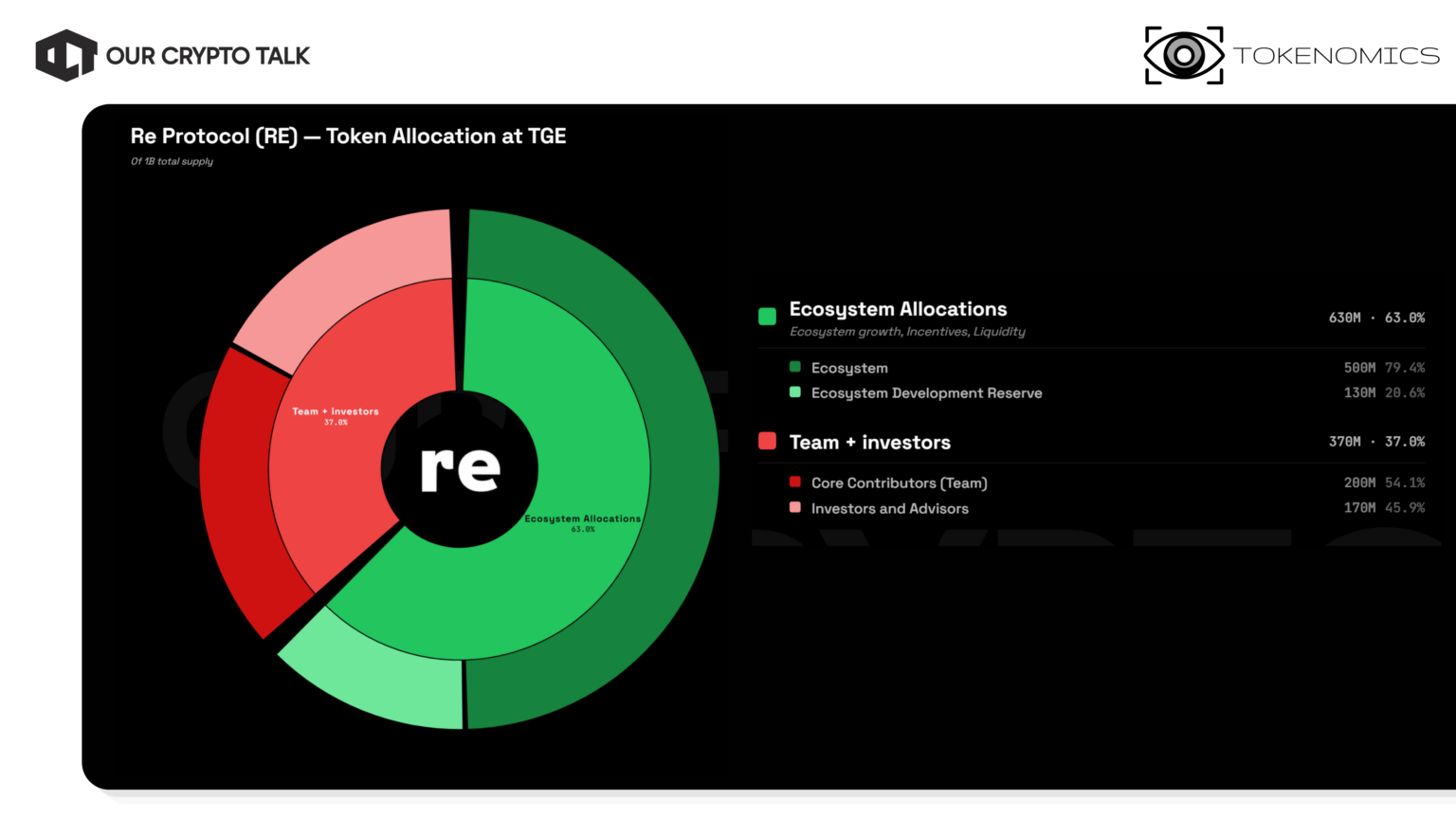

Re has now revealed the core structure of the RE token.

The protocol will launch with a fixed supply of 1 billion RE tokens. Allocation is split across four major buckets:

The headline number is the ecosystem allocation. Half of the entire supply is reserved for ecosystem growth, incentives, governance participation, liquidity programs, and community distribution. In a market where many venture-backed projects allocate 40-50% of supply to insiders, Re’s structure is noticeably more balanced.

The insider allocation totals 37% when combining team and investor allocations. That figure is not unusually low, but it is also not excessive for a protocol that has spent years building regulatory infrastructure, raising institutional capital, and scaling to hundreds of millions in TVL before launch.

However, the most important tokenomics information is still missing.

Re has not yet revealed vesting schedules for the team or investors. The protocol has also not disclosed cliff periods, initial circulating supply, unlock schedules, or the exact points-to-token conversion mechanism. Those details matter more than the allocation chart itself.

A token can have a healthy allocation structure and still perform poorly if large insider unlocks hit the market too early. Likewise, a generous ecosystem allocation means little if only a small percentage of supply enters circulation while the token launches at an aggressive valuation.

The initial allocation is a positive signal. Re avoided an excessively insider-heavy structure and committed the majority of supply to ecosystem growth. Still, investors should not treat the tokenomics story as complete.

The real test comes when vesting schedules, circulating supply, and unlock timelines are released. Until then, the market knows who owns the supply, but not when that supply can be sold.

Unlike many pre-token projects, Re does not rely on testnets, node sales, or speculative waitlists. The primary path to early participation involves using the live product.

Visit the platform and complete identity verification. Re operates within regulated insurance frameworks, so participation requires compliance checks before capital enters the system.

Deposit supported assets such as USDC, USDe, or sUSDe into the Insurance Capital Layer. This is the highest-signal action because it commits real capital.

Choose the product that matches your risk profile. reUSD targets lower volatility, while reUSDe targets higher insurance-related yield in exchange for greater risk exposure.

As of June 2026, reUSD targets roughly 6.1% APY while reUSDe targets approximately 12.0% APY, reflecting its higher-risk position within the capital stack.

The Re Points Program rewards users for deposits, holding activity, referrals, and ecosystem engagement. The team has repeatedly linked early participation to future governance opportunities.

Long-term participants earn yield while accumulating points ahead of the RE token launch. Monitor updates from official channels as token details become available.

A final note: points are not an investment thesis. Many crypto users chase points programs that never create meaningful value. The stronger thesis is the protocol itself. If you believe insurance premiums belong onchain, using the product today provides both exposure to the business model and a potential path to future governance participation.

This is the section that matters most. After the team, product, traction, and funding, does deploying capital into Re offer positive expected value in 2026?

The strongest part of the thesis is that users do not need to rely entirely on points. Re’s points program rewards real capital allocation rather than social farming. Users complete KYC, deposit stablecoins, mint reUSD or reUSDe, and accumulate points while earning yield from actual insurance premiums.

That immediately separates Re from most pre-token opportunities. In many points programs, participants sacrifice time for uncertain rewards. In Re’s case, capital generates yield regardless of whether the eventual token launch exceeds expectations.

The second advantage is competition quality. The points system is capital-weighted and KYC-gated. That dramatically reduces Sybil farming and makes future allocations harder to dilute. The barrier to entry is higher, but the participant quality is also higher.

There is no public presale. The only way to position early is to use the product itself. That creates stronger alignment between the protocol and participants because rewards flow toward users who actually contribute liquidity.

The risks are straightforward. Capital remains exposed to execution risk, insurance risk, and token launch risk. A poor token structure could significantly reduce the value of accumulated points. Investors also face opportunity cost because similar stablecoins could earn yield elsewhere.

My conclusion is simple. Re offers positive expected value if you already believe in tokenized real-world assets and insurance-backed yield. Users earn real returns while maintaining exposure to a future governance token. That is a stronger setup than most pre-TGE opportunities.

If you have no interest in reinsurance, dislike KYC requirements, or want immediate liquidity, the opportunity becomes much less attractive. For RWA-focused investors, however, Re remains one of the cleaner risk-reward setups currently available.

Strong projects rarely fail because of a lack of vision. They usually fail because of execution, competition, or market structure.

Competition is the first risk. Traditional giants such as Swiss Re and Munich Re control enormous balance sheets and relationships. If tokenized reinsurance proves successful, larger firms could launch competing products or partner with crypto infrastructure providers directly.

Insurance risk is the second challenge. Re’s yield comes from real underwriting activity. That creates genuine economic value, but it also creates exposure to claims events. Severe hurricane seasons, cyber incidents, or unexpected loss ratios could pressure returns and damage confidence.

Regulation remains another major variable. Re operates through regulated structures today, but insurance regulation evolves slowly and unpredictably. New rules affecting tokenized securities, insurance capital, or stablecoin infrastructure could create friction for growth.

Tokenomics present a separate risk. Aggressive unlock schedules, or weak utility could damage market confidence regardless of protocol performance.

Operational complexity should not be ignored either. Managing hundreds of millions in capital, daily attestations, regulatory relationships, and future governance creates significant coordination challenges. A major claims dispute, redemption issue, or oracle failure could quickly become a reputation problem.

The biggest takeaway is simple. Re’s strengths come from real-world exposure, but those same strengths introduce real-world risks. Investors are not betting on a purely digital protocol. They are betting on an insurance business that happens to operate through crypto rails.

The most important catalyst is the upcoming RE governance token launch.

The Resilience Foundation confirmed in May 2026 that the token generation event is approaching. The announcement shifted attention from the protocol’s yield products toward governance, incentives, and ownership of the network itself.

Before the token launches, the market needs answers to several questions. Investors still do not know the FDV, circulating supply, vesting schedule, or exact conversion mechanics for points participants.

Those details will likely determine the market’s initial reaction more than any other factor.

The second major catalyst is the token launch itself. The TGE will transform points from a theoretical reward into a measurable asset. It will also reveal how governance functions and how much influence early participants receive.

Beyond crypto-native catalysts, business execution remains important. January 2027 renewals will provide one of the first large-scale tests of Re’s ability to retain and expand underwriting capacity after the token launch.

For potential participants, timing matters. The points program remains active today, and future snapshots will likely reward users who engaged before the token launch. Waiting for complete certainty may also mean missing the highest-upside phase of participation.

The next few months will likely determine whether Re becomes a niche RWA protocol or one of the defining tokenized insurance platforms of this cycle.

Few pre-token projects combine a live product, meaningful revenue generation, institutional partnerships, and a clear path toward governance participation. Re checks all four boxes.

The protocol already manages hundreds of millions in capital. It generates yield from real insurance premiums rather than token emissions. It operates with established carriers, global brokers, and regulated structures. Most importantly, users can interact with the product today rather than speculate on future development.

The investment case is not perfect. Vesting and circulating supply remain the largest unanswered question. A poor launch structure could reduce the attractiveness of the opportunity regardless of how well the business performs.

That uncertainty prevents a stronger conviction rating.

However, based on the information currently available, Re offers one of the more compelling risk-reward profiles in the RWA sector. Participants earn yield while positioning for a governance token tied to a protocol that already functions at scale.

The one milestone that changes the rating: The vesting and circulating supply reveal.

Re has not revealed team vesting schedules, investor vesting schedules, cliff periods, initial circulating supply, or unlock timelines. Those figures will ultimately determine whether the launch creates long-term alignment or short-term sell pressure.

Until those details arrive, the highest-conviction approach remains simple. Use the product, earn the yield, accumulate points, and wait for the token structure to reveal itself.

Disclaimer: This is not financial advice. The information provided is for educational and informational purposes only. All investments involve risk, including the potential loss of principal. Always do your own research.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.