We ranked 2026’s top DeFi tokens by real revenue to holders, not TVL or hype. Each gets a verdict: Real, Mid, or Theater. Data: DefiLlama.

Author: Akshat Thakur

The narrative in DeFi has quietly flipped. For years, protocols relied on emissions to attract liquidity. High APYs looked attractive, but most of that “yield” came from token inflation, not real usage. That model is breaking down. This guide to the top 10 real yield DeFi tokens of 2026 separates actual cash flow from emission-driven hype.

Today, the data shows a clear shift. Protocols are redistributing a larger share of actual revenue to token holders. Industry-wide, that number has moved from roughly 5% before 2025 to around 15% in 2026. This is not a small change. It is a structural shift in how value flows in DeFi.

Two major catalysts pushed this forward. Uniswap activated its long-awaited fee switch, introducing buybacks and burns across multiple chains. Aave followed with governance changes that route branded product revenue directly to the DAO and token holders. The message is clear. Revenue now matters more than emissions.

This article is different by design. It ignores TVL rankings, market cap narratives, and inflation-driven APYs. Instead, it ranks the top 10 real yield DeFi tokens 2026 based purely on actual protocol revenue distributed to holders.

All data is sourced from DefiLlama ( as of April 2026 ) and verified within the last 48 hours. Each project is graded using a strict Real, Mid, or Theater framework. The goal is simple: identify real yield crypto, not narrative-driven hype.

Real yield is simple. It is revenue generated by actual protocol usage and distributed to token holders. Emission yield is the opposite. It relies on minting new tokens to pay rewards, which dilutes holders over time. One is cash flow. The other is inflation.

For this ranking, the focus is only on real yield. Every data point comes from DefiLlama and is verified against on-chain activity.

The methodology is strict. First, we use annualised protocol fees based on 30-day data from DefiLlama. This shows how much real revenue a protocol generates from users. Second, we measure the percentage of that revenue distributed to token holders. This includes buybacks, fee switches, staking rewards, and veToken models.

If revenue stays in the treasury, it does not count. Third, we verify whether the distribution is actually happening on-chain. If it depends on governance discussions or future proposals, it is excluded.

The grading system is designed to remove ambiguity. Real yield means verified on-chain revenue distribution to holders. Mid refers to protocols where revenue exists but the path to holders is indirect or conditional. Yield theater includes projects that claim real yield but still rely mostly on emissions.

The broader trend matters here. Revenue redistribution to holders has increased from around 5% to nearly 15% across DeFi. This shift defines which protocols qualify as true best tokenomics crypto and which ones are still playing the old game.

We rank these tokens strictly by revenue that actually reaches holders. The table uses data from DefiLlama and reflects annualised holders revenue based on the latest 30-day figures. Every percentage and mechanism is verified on-chain. No TVL. No market cap. Only real cash flow.

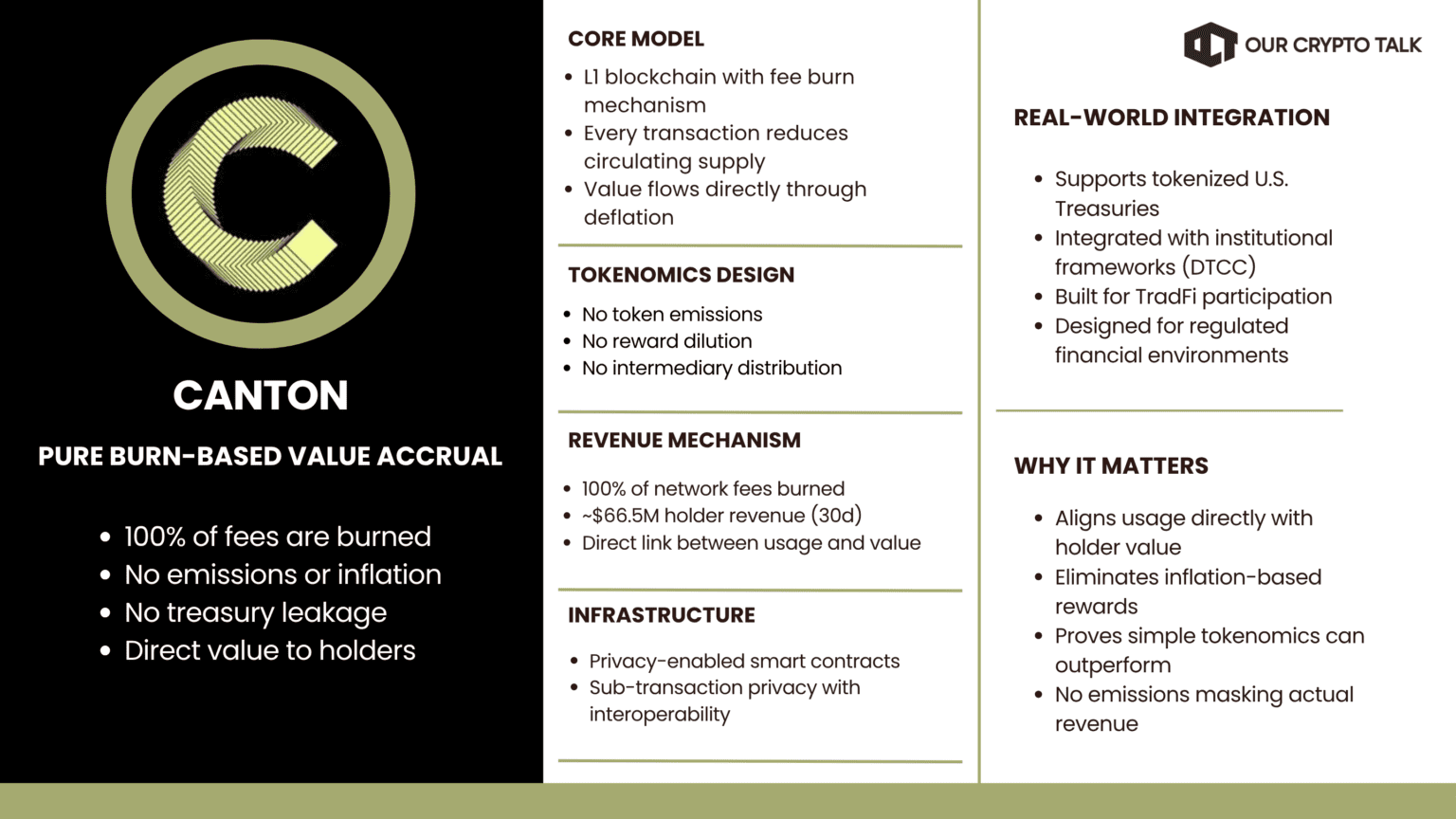

Canton operates as an L1 chain where every transaction fee is burned. This creates direct value for holders through supply reduction. There is no emission layer and no treasury leakage.

The mechanism is simple and fully on-chain. That is why it ranks first. It represents pure real yield crypto. The verdict is Real because 100% of revenue flows to holders through burn mechanics. This is one of the cleanest examples of crypto with best tokenomics today.

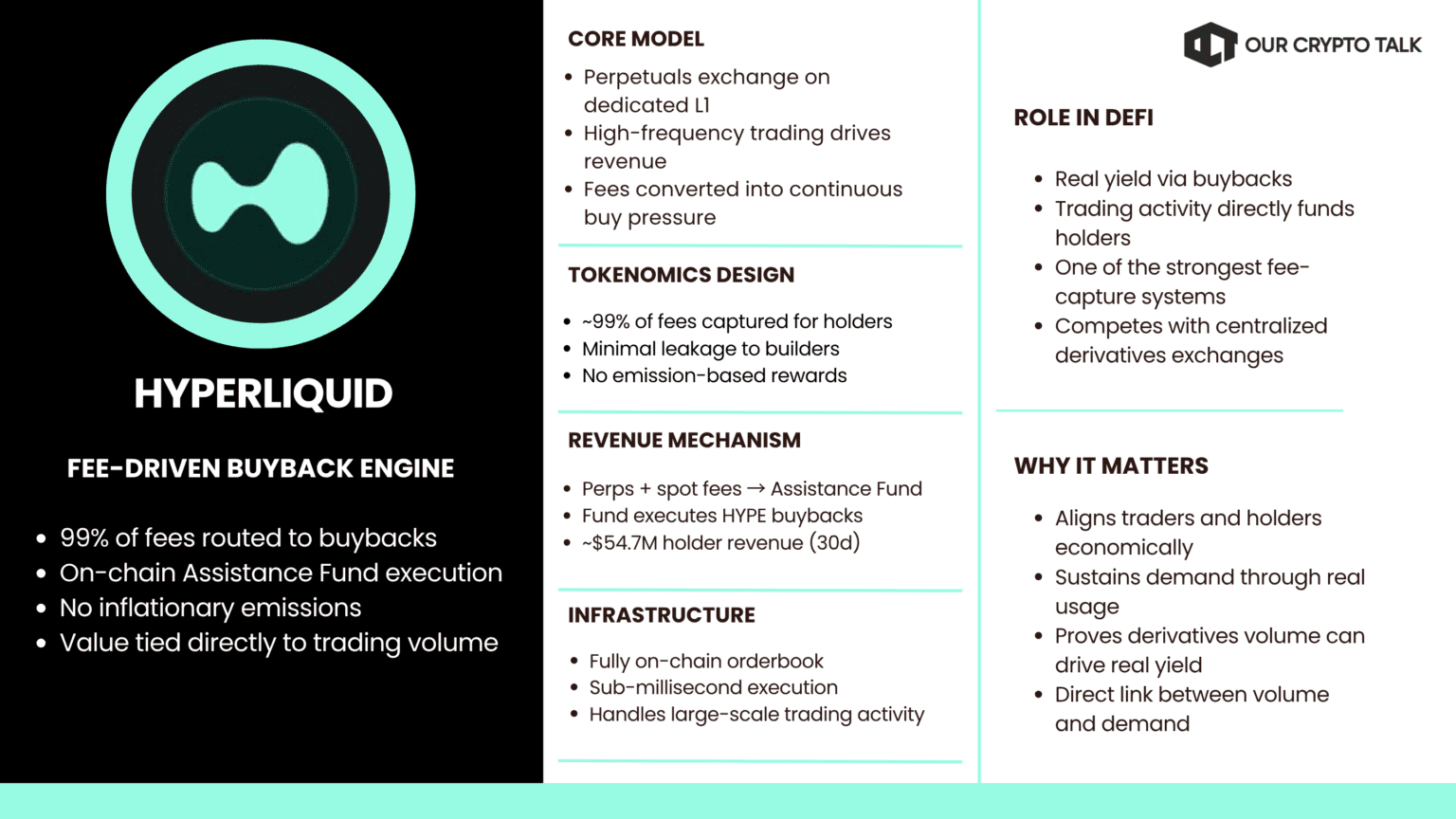

Hyperliquid runs a high-volume derivatives exchange. Almost all trading fees are routed into a buyback system through its Assistance Fund. The protocol consistently converts revenue into market demand for HYPE.

This is not theoretical. It is executed on-chain. The 99% distribution rate puts it firmly in the Real category. It ranks second because revenue capture is extremely efficient and directly tied to trading activity.

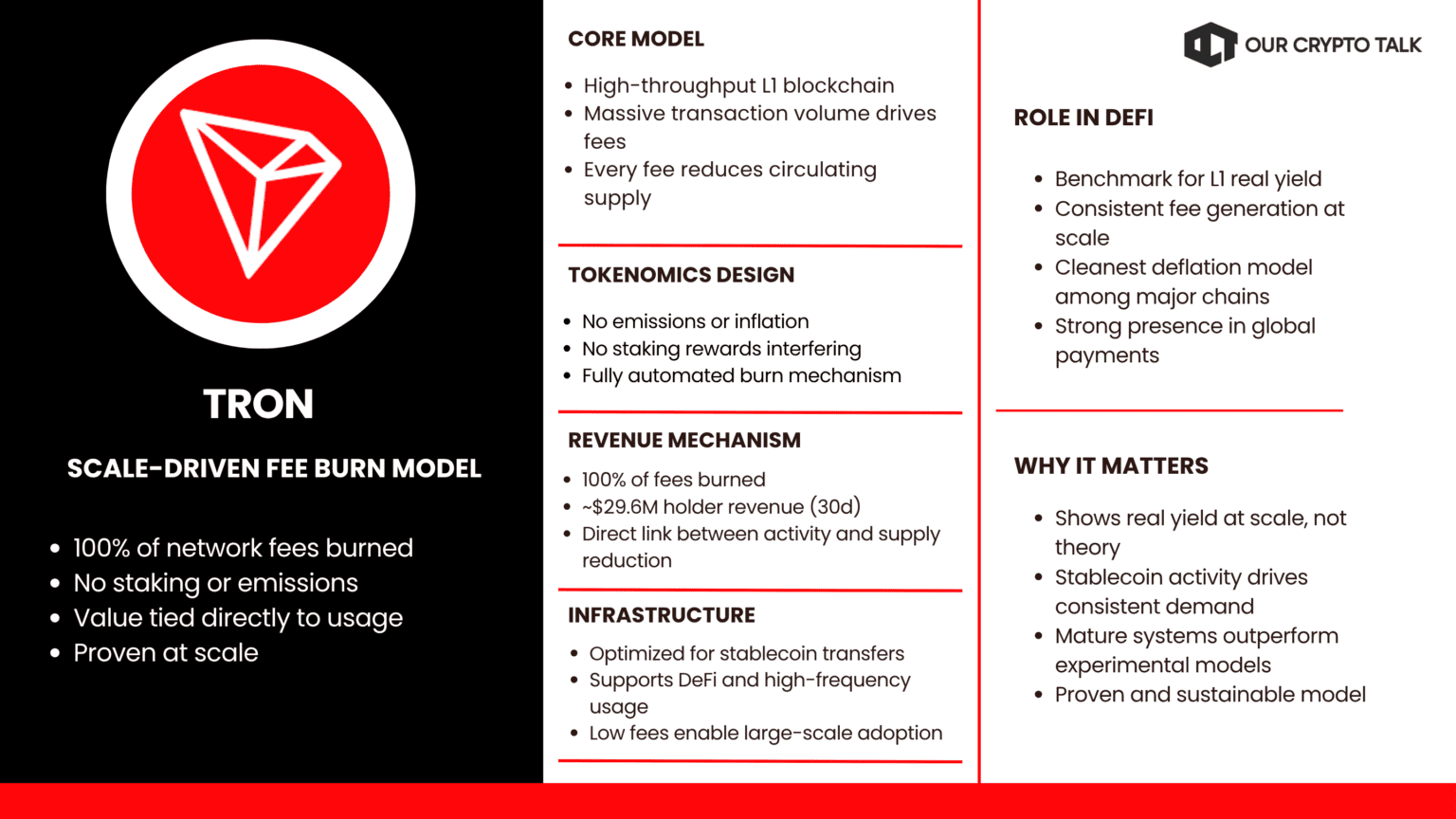

Tron uses a full burn model for network fees. Every transaction reduces supply. This benefits holders without requiring staking or lockups. The model is mature and proven at scale.

The Real verdict is straightforward because distribution is complete and automated. Tron ranks high due to strong fee generation combined with full value capture. It remains a benchmark for real yield crypto at the L1 level.

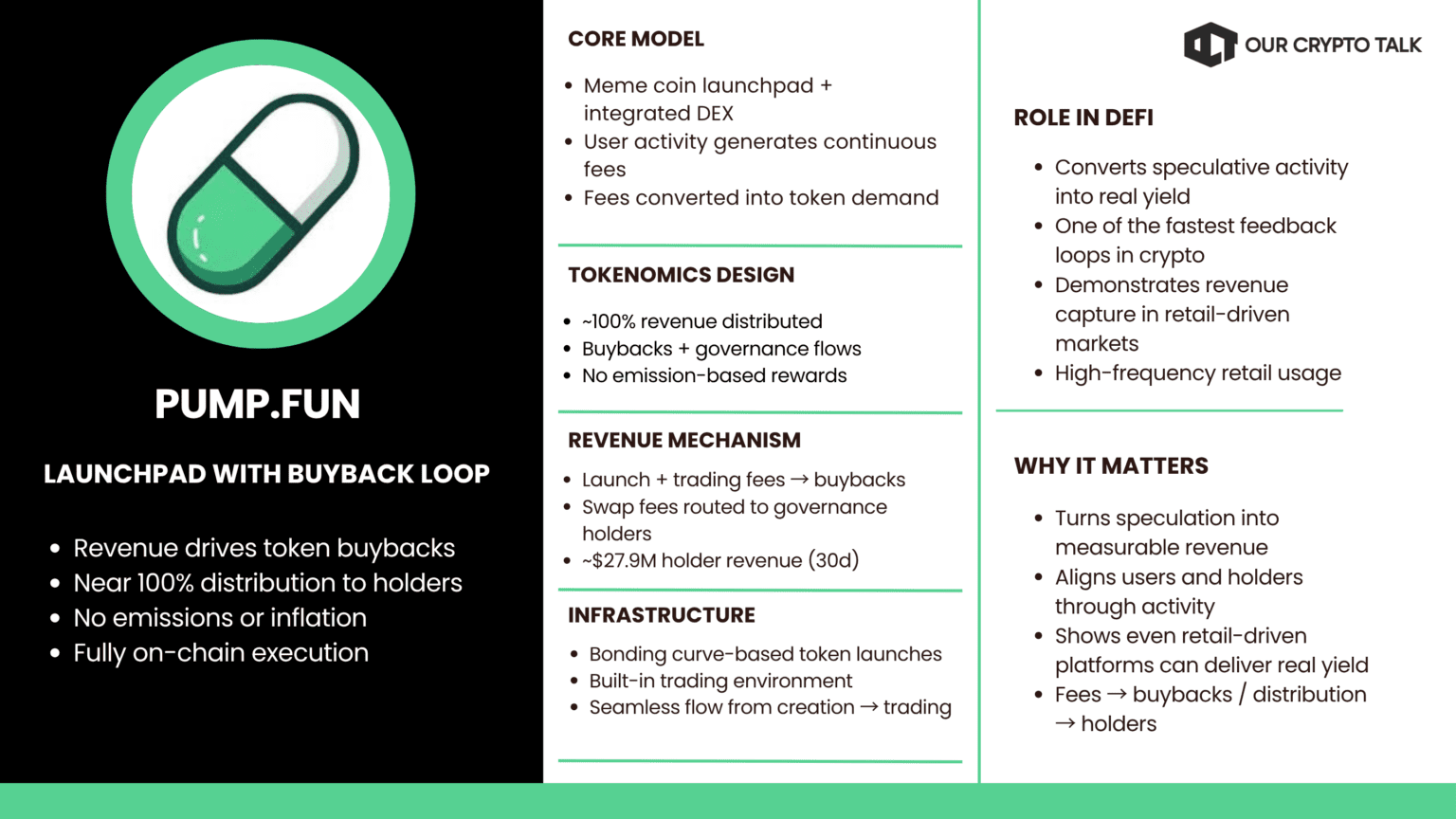

Pump functions as a launchpad with integrated trading. Revenue is routed into token buybacks and governance distribution. The mechanism is close to full distribution and happens on-chain. There is no reliance on emissions.

This direct loop between usage and token demand is why it ranks fourth. The verdict is Real because value flows are transparent and immediate. It stands out among newer protocols claiming crypto with best tokenomics.

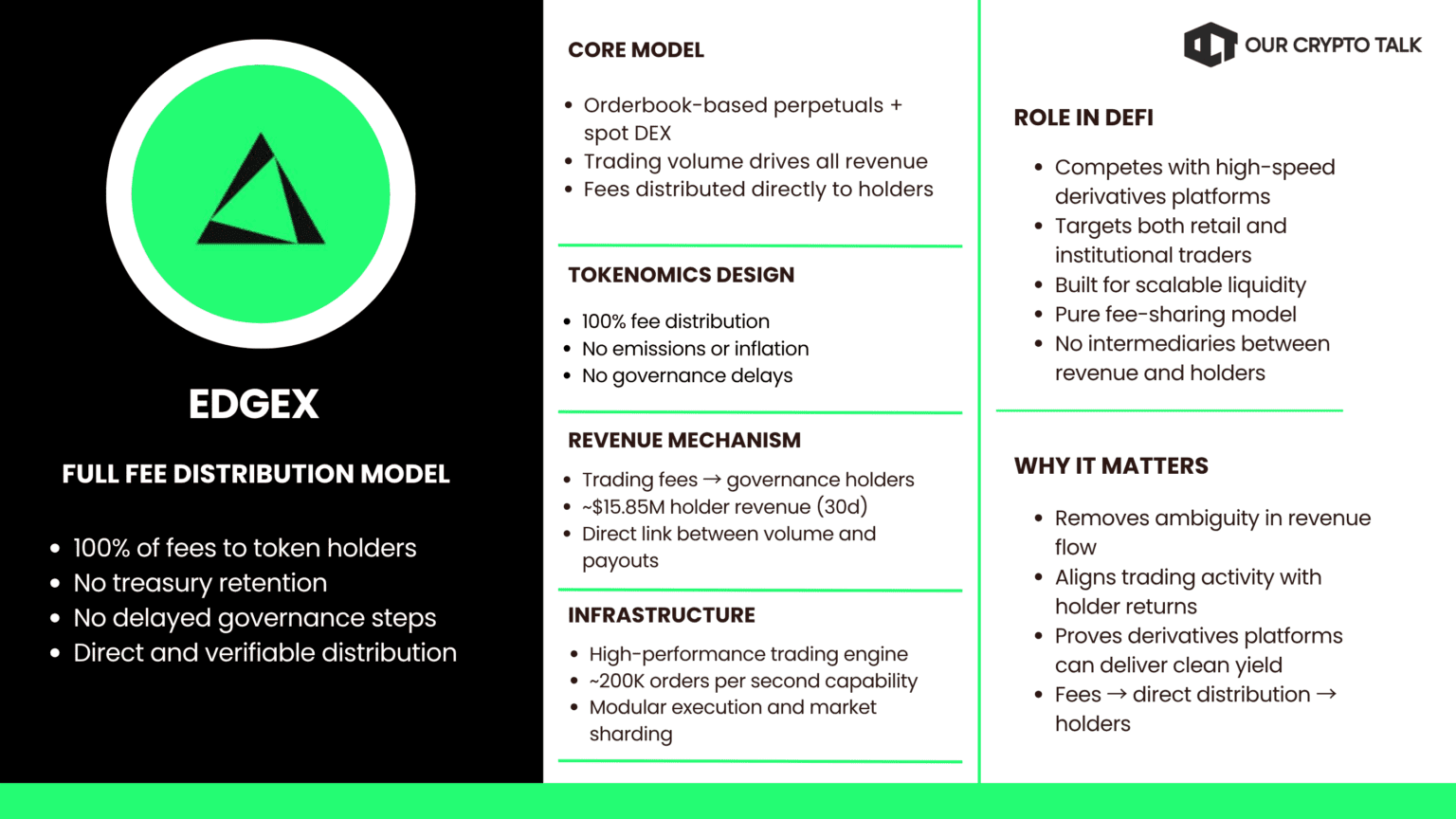

edgeX is a derivatives platform that routes all trading fees to token holders. The model removes ambiguity. There is no treasury retention and no delayed governance step. Revenue distribution is direct and verifiable.

This earns a Real classification. It ranks fifth because of strong revenue capture and clean tokenomics. It shows that derivatives protocols can deliver real yield crypto without complexity.

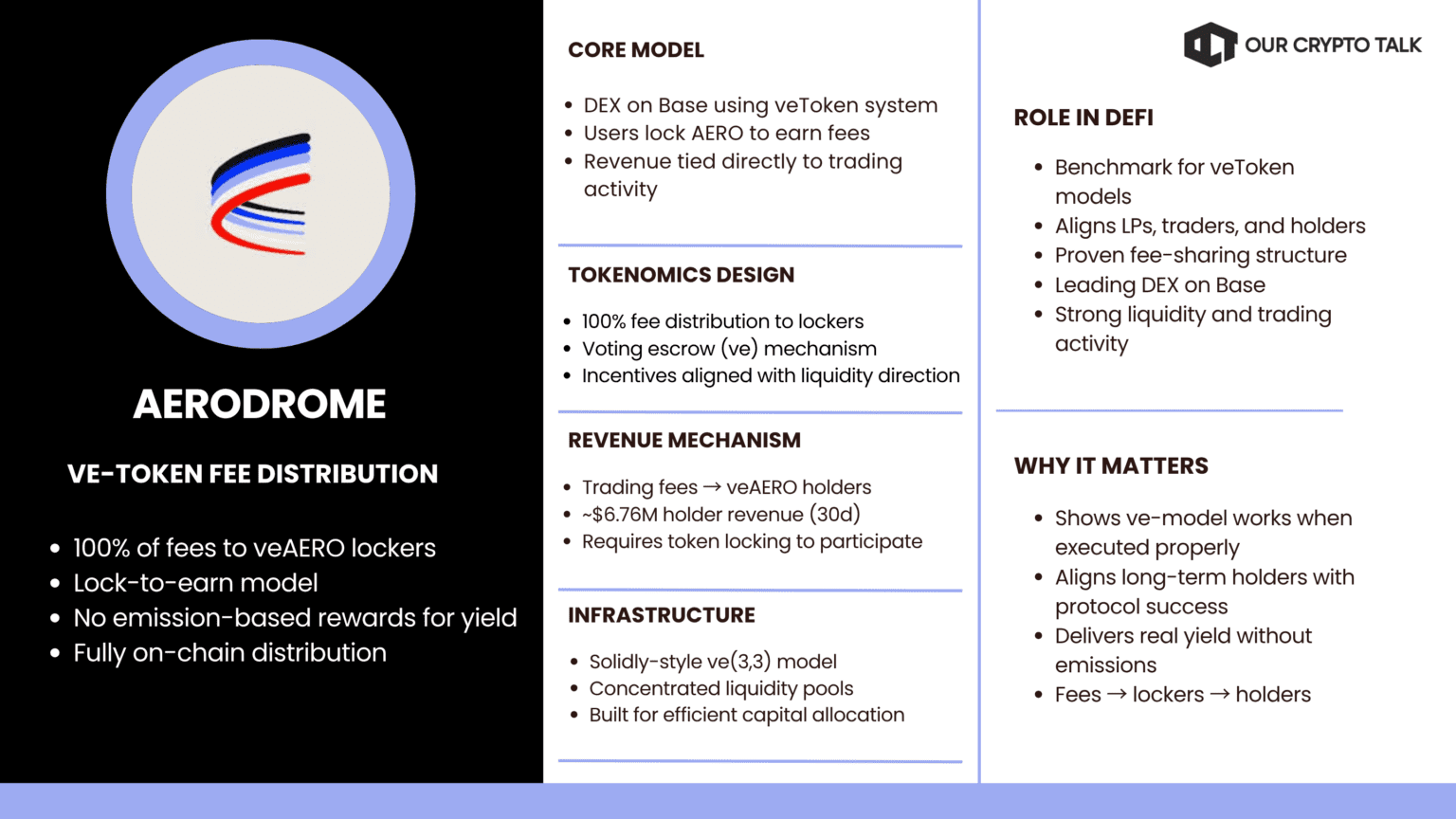

Aerodrome uses a veToken model on Base. Users lock tokens to receive a share of protocol fees. All revenue is distributed through this system. The design aligns incentives between liquidity providers and token holders.

The Real verdict comes from full on-chain distribution. It ranks sixth because the mechanism is efficient but depends on user participation in locking. Still, it remains a strong example of crypto with best tokenomics.

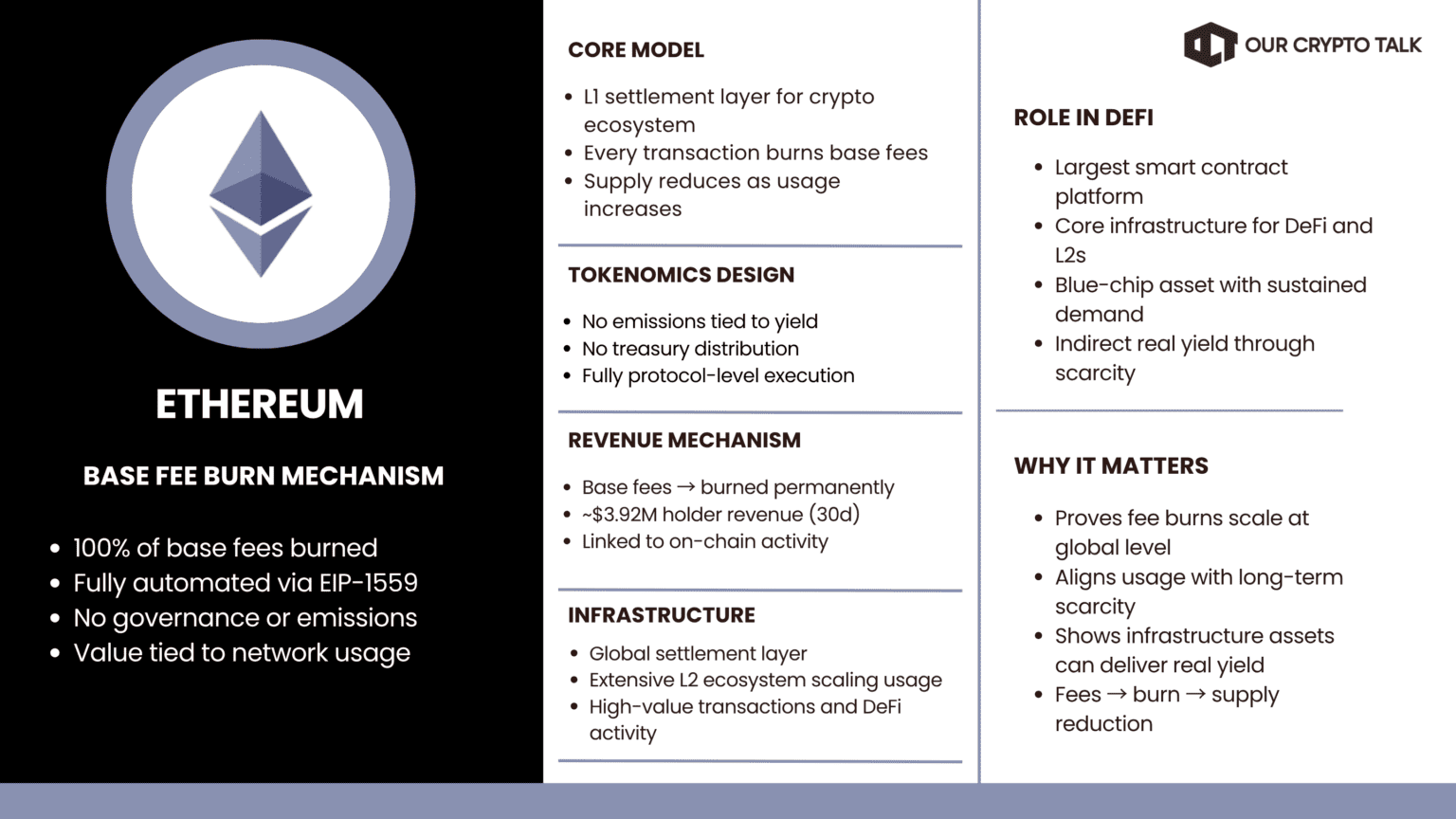

Ethereum burns base fees through its fee mechanism. Every transaction reduces supply. This creates indirect but real value for holders. The system is fully automated and does not rely on governance. The Real grade is clear.

It ranks seventh because while distribution is complete, the model is indirect compared to buybacks or staking rewards. Still, it remains a core real yield crypto asset.

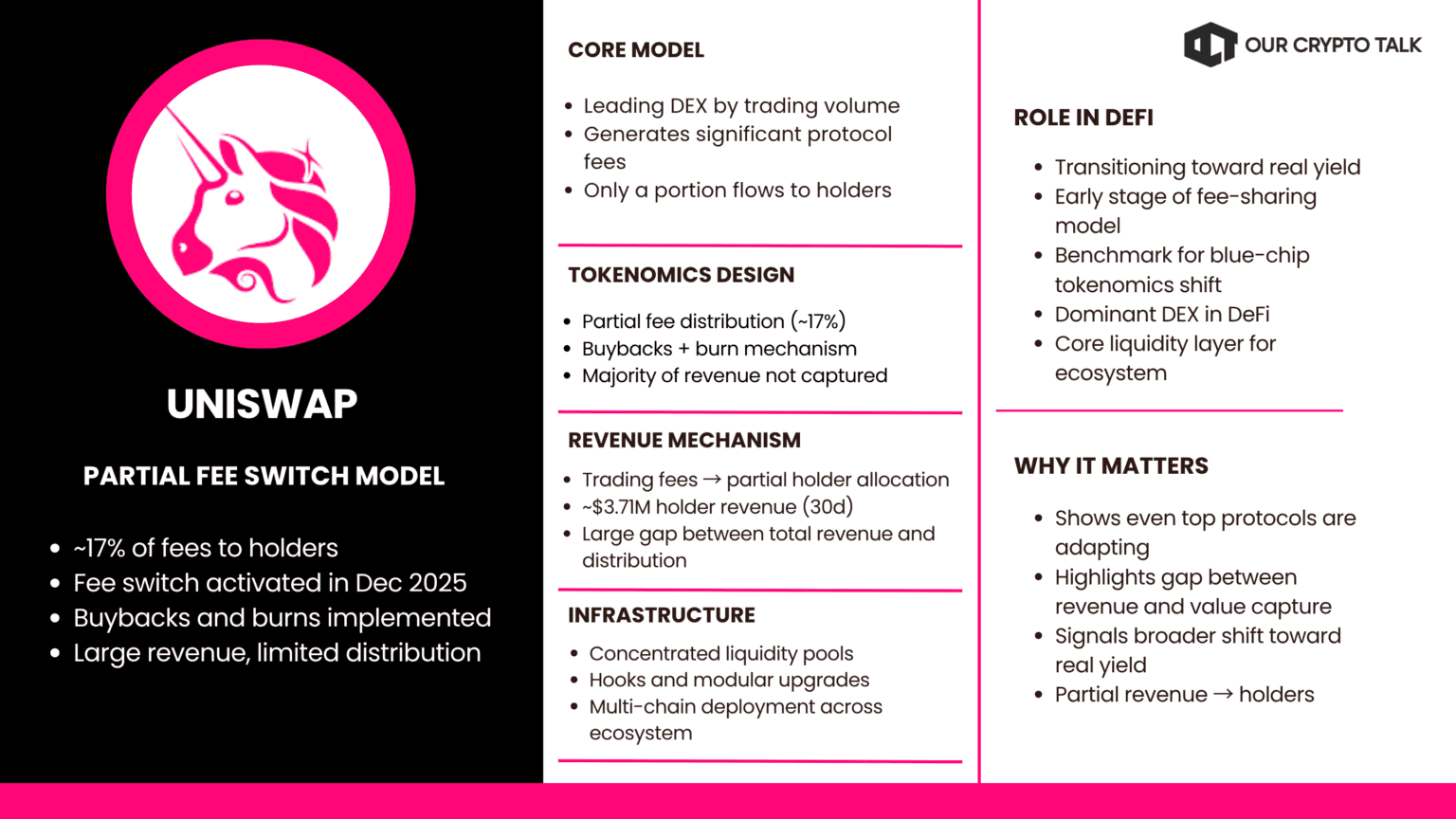

Uniswap introduced its fee switch after years of delay. A portion of trading fees now goes to UNI holders. The current distribution is around 17%. This is a meaningful shift but still limited.

The protocol generates large revenue, but only a fraction reaches holders. That is why it receives a Mid verdict. It ranks eighth because distribution efficiency is still low relative to peers.

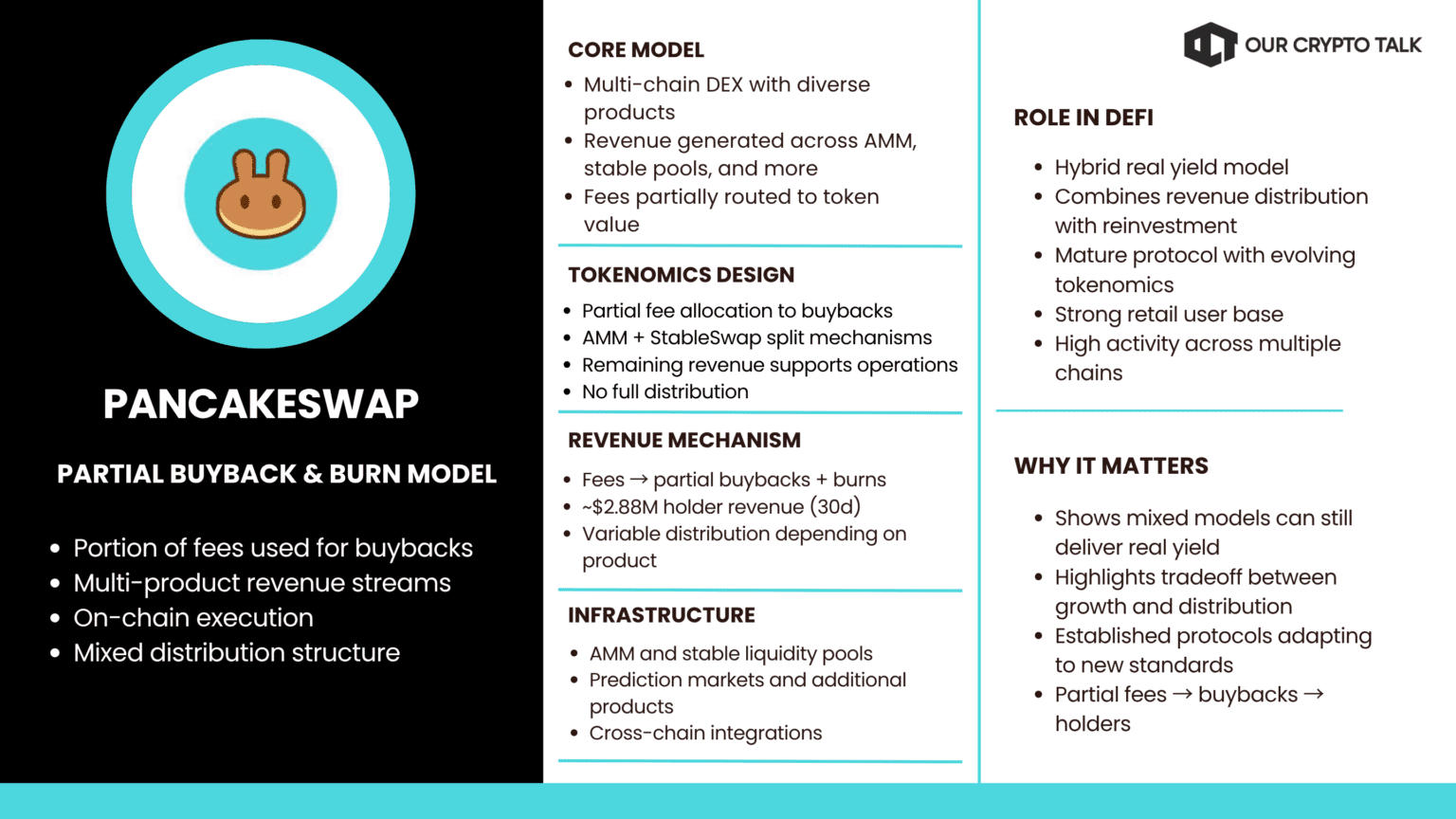

PancakeSwap uses a mixed model. A portion of fees is used for buybacks and burns, while the rest supports operations. The mechanism is verifiable but not fully distributed.

This still qualifies for Real because actual revenue reaches holders on-chain. It ranks ninth due to lower efficiency compared to full-distribution models. Even so, it remains relevant in the real yield crypto category.

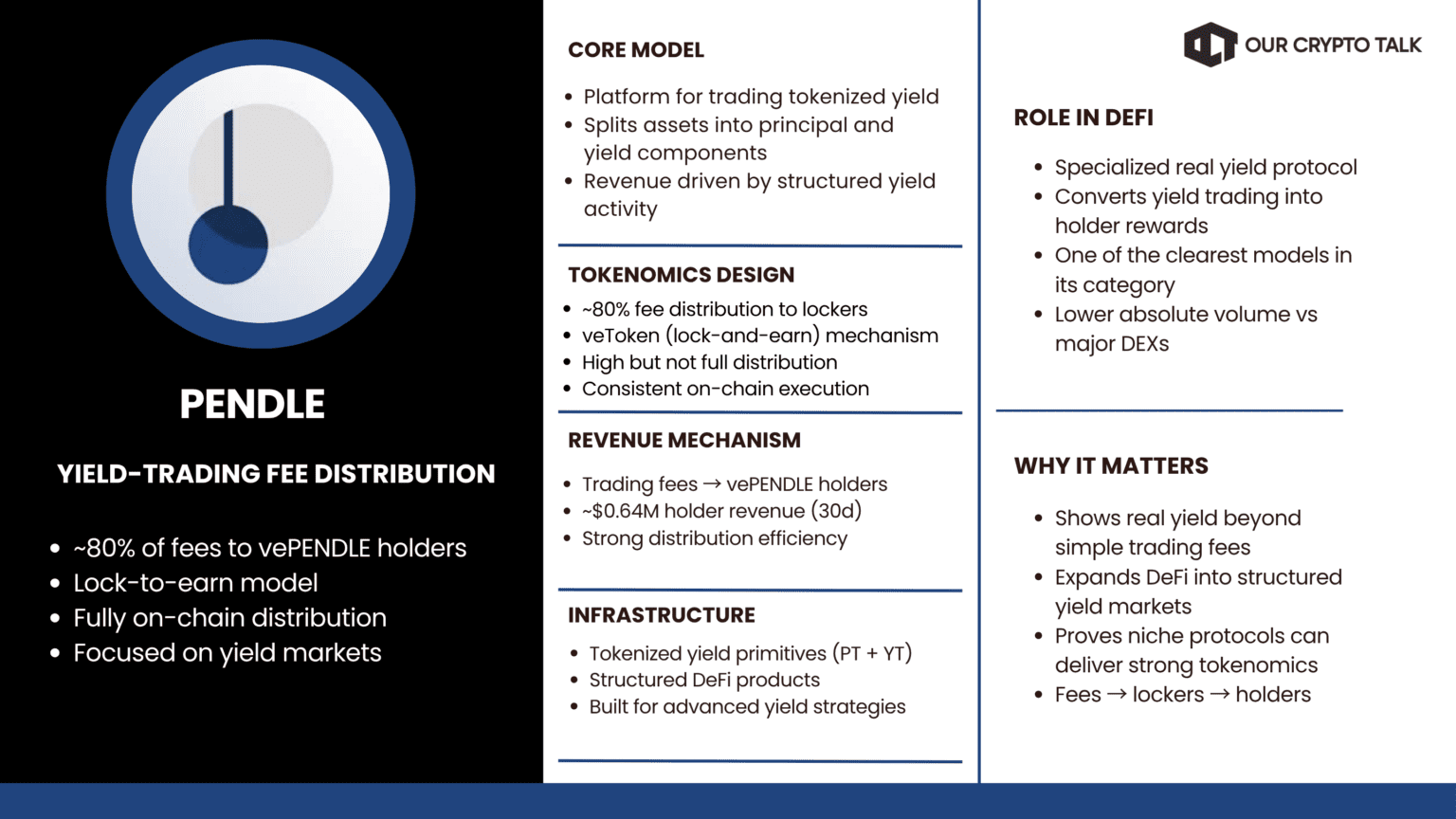

Pendle focuses on yield trading. It distributes a large share of its revenue to veToken holders. The mechanism is consistent and on-chain. Around 80% of revenue flows to holders, which secures a Real verdict.

It ranks tenth due to smaller absolute revenue compared to others. However, its distribution efficiency is strong. It remains one of the more structured examples of crypto with best tokenomics.

A few protocols come close but miss the top 10 on absolute holders revenue. The gap is not in design. It is in scale.

GMX has one of the cleanest revenue-sharing models in DeFi. Trading fees flow to GLP participants and stakers through on-chain distribution. The mechanism is real and verifiable. The reason it falls short is simple. Current holders revenue does not match the top tier on DefiLlama. Strong model. Lower volume.

dYdX also routes a portion of fees toward token holders. The structure is governance-driven but implemented on-chain. Revenue exists and distribution is active. It misses the list because the actual dollar flow to holders remains below the cutoff set by higher-volume protocols.

Jupiter has introduced buybacks funded by platform revenue. The mechanism is transparent and tied to usage. However, its holders revenue is still building relative to leaders in this cycle.

These protocols qualify as real yield crypto on structure. They just do not move enough capital to compete with the top 10 yet. That can change quickly if volume shifts.

This is where the gap between narrative and data becomes obvious. Several protocols market real yield, but the holders-revenue data shows a different reality. High APYs exist, but little to no value reaches token holders on-chain.

Lido Finance is the clearest example. It is the largest DeFi protocol by TVL and generates significant fee revenue from staking. The model takes a 10% cut, split between node operators and the DAO treasury. None of that flows to LDO holders. Data from DefiLlama shows near-zero holders revenue. LDO captures governance, not cash flow. By this framework, it is yield theater despite its scale.

Curve Finance relies heavily on emissions via the veCRV model. Fees exist, but distribution to holders is small relative to total revenue. Emissions still dominate the yield narrative.

Balancer follows a similar pattern. The veBAL system suggests revenue sharing, but verified holders revenue remains low. Most value stays within the protocol. SushiSwap continues to promote staking rewards, yet on-chain distribution is inconsistent. Emissions remain a core incentive.

If revenue does not reach holders, it is not real yield crypto. It is still yield theater.

The fee switch changed the conversation. When Uniswap activated revenue sharing in late 2025 and expanded it in early 2026, it proved that large protocols can route real cash flow to token holders. Data from DefiLlama confirms it. Holders revenue is no longer theoretical. It is measurable and growing.

If this trend continues, DeFi tokens start behaving less like speculative assets and more like cash-flow instruments. Valuation frameworks shift quickly. TVL stops being the headline metric. Revenue and holders revenue take its place. Protocols begin trading on revenue multiples, not narrative cycles.

This forces a reset in tokenomics. Buybacks, burns, and staking distributions become standard. Models that do not pass revenue to holders lose relevance. The market already shows this direction. Protocols with high distribution percentages capture more sustained attention than those relying on emissions.

The contrarian view is this transition will not be smooth. Many established protocols still retain fees in treasuries or depend on emissions to survive. Shifting to full revenue distribution reduces flexibility and exposes weak unit economics. Some will not adapt in time.

The sector benefits overall. Real yield crypto creates stronger alignment between users and holders. But the filter becomes harsher. If the fee-switch era holds, only protocols with verifiable revenue flow and efficient distribution will survive. The rest will be exposed by their own numbers.

This article is for informational purposes only and does not constitute financial advice. DYOR.

Follow OCT on X for more DeFi analysis.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.