Are exchange tokens a good investment in 2026? Compare how BNB, UNI, and HYPE turn exchange fees into token value, and learn to spot governance-only traps.

Author: Kritika Gupta

Exchange Tokens sit at the center of one of crypto’s most important value-capture debates. Centralized exchanges and decentralized exchanges can generate massive trading fees, but their tokens do not always benefit from that activity. Some tokens capture value through burns, buybacks, or fee-sharing. Others only offer governance rights with no direct revenue link. This article breaks down how CEX tokens like BNB compare with DEX tokens like UNI, HYPE, and AERO, and explains what actually gives an exchange token lasting value.

An exchange token only matters if the token connects to the business behind it.

Start with the basic model. An exchange makes money when people trade. Every time a user buys or sells crypto, the exchange charges a small trading fee. If millions or billions of dollars move through the platform each day, those small fees can turn into serious revenue.

However, token holders need to ask one simple question: does any of that money reach the token?

This is where many people get confused. A popular exchange does not automatically mean a valuable token. The exchange can earn huge fees while the token sits on the side with no real claim on that revenue. So, before judging any exchange token, investors should understand the three main ways a token can capture value.

The first lever is burns. A burn means the project permanently destroys tokens, usually by sending them to an address no one can access. This reduces the total supply. If fewer tokens exist, each remaining token represents a bigger slice of the network. Burns do not guarantee price growth, because demand still matters. However, if demand stays steady or rises, lower supply can support the token over time.

The second lever is buybacks or fee-share. A buyback means the exchange uses revenue to buy its own token from the open market. This creates real buying demand because the exchange itself becomes a regular buyer. Fee-share means the protocol pays part of its revenue directly to token holders, stakers, or lockers. This works more like a cash-flow claim because holders receive value from the exchange’s activity. In both cases, trading volume can translate into token demand or holder rewards.

The third model is governance-only. Governance means token holders can vote on proposals, such as fee changes, treasury spending, or protocol upgrades. Voting power can matter, but it does not automatically create economic value. If the token only gives holders a vote and no share of revenue, no buybacks, and no burns, then holders depend mostly on speculation. This is the trap. The exchange may grow, but the token may not capture that growth.

Therefore, the key question is not “Is this exchange successful?” The better question is “How does this token benefit from the exchange being successful?”

A great exchange can still have a token that captures nothing. That gap between exchange revenue and token value is the whole article.

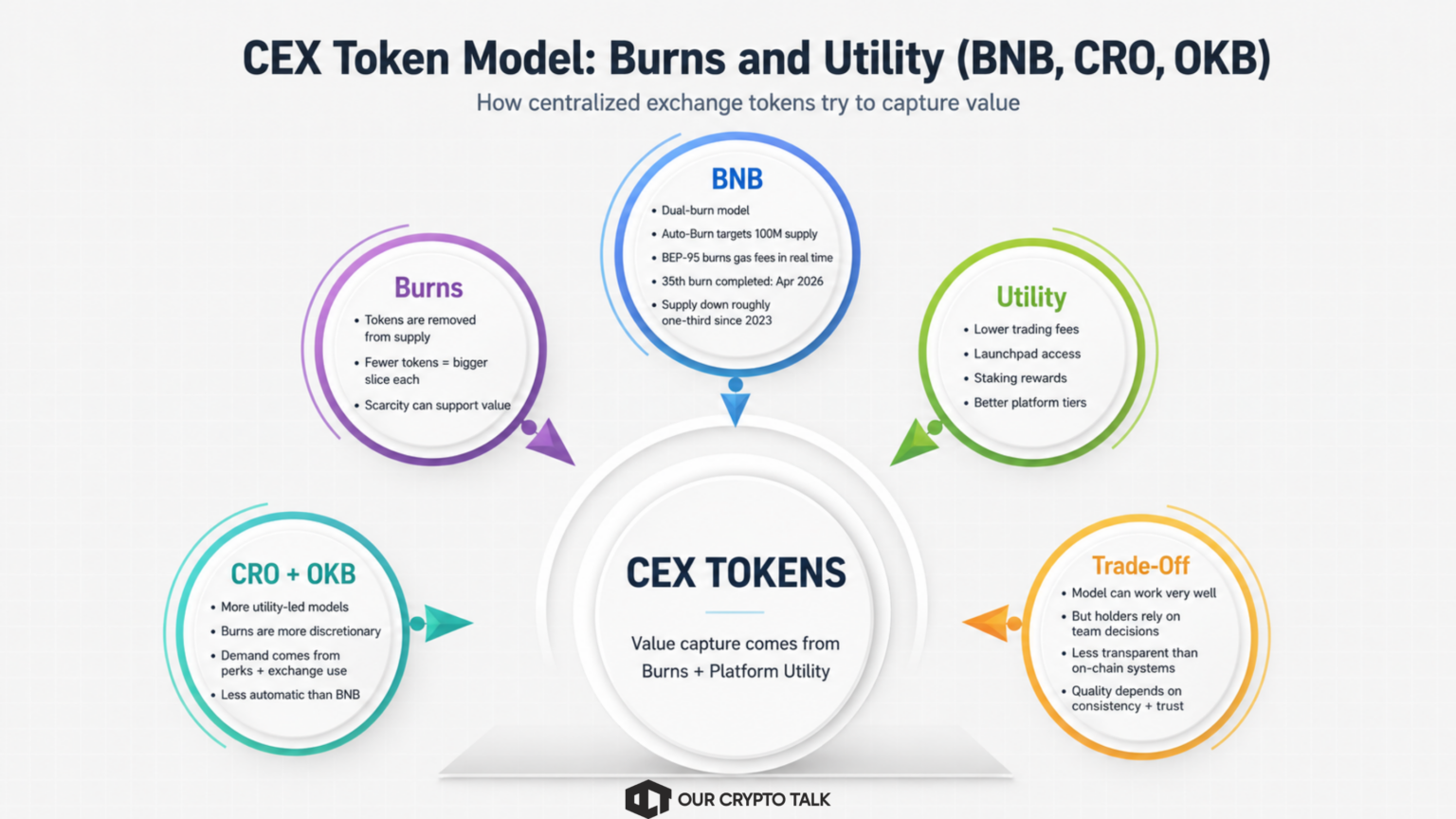

Centralized-exchange tokens, or CEX tokens, usually capture value in two main ways: burns and platform utility.

A burn means the exchange permanently removes tokens from circulation. If the supply falls over time, each remaining token represents a larger share of the total supply. Platform utility means users hold the token because it gives them practical benefits, such as lower trading fees, launchpad access, staking rewards, or better product tiers.

BNB gives the cleanest example of this model. Binance uses a dual-burn system. First, it runs a quarterly Auto-Burn that removes BNB from supply based on a formula linked to BNB price and the number of blocks produced on BNB Smart Chain. This mechanism aims to reduce total BNB supply toward a long-term cap of 100 million tokens.

Second, BNB uses BEP-95. This mechanism burns a portion of gas fees in real time on every block. Gas fees are the transaction fees users pay when they interact with BNB Smart Chain. Therefore, BEP-95 links part of BNB’s supply reduction to actual network activity.

Together, these two burn systems create a clear scarcity story. Binance completed its 35th quarterly BNB burn in April 2026. Since 2023, BNB’s circulating supply has fallen by roughly one-third. That matters because BNB combines large exchange demand, chain usage, fee discounts, and recurring burns into one token model.

However, not every CEX token works as cleanly as BNB. CRO from Crypto.com and OKB from OKX lean more heavily on utility and exchange-led decisions. Users may hold these tokens for trading-fee discounts, access to launchpad sales, staking benefits, or platform perks. These use cases can create real demand, especially when the exchange has a large user base.

Still, the burn side often depends more on the company’s decisions than on a fully automatic, on-chain rule. For example, an exchange may decide when to burn tokens, how many to burn, or whether to connect burns to profits, reserves, or special events. OKB’s major 2025 supply reduction showed how powerful a one-time exchange-led burn can be, but it also showed how much control the centralized team holds.

That is the trade-off with CEX tokens. When the exchange grows, commits to burns, and gives users strong reasons to hold the token, the model can work very well. BNB proves that. However, holders must accept more trust risk. They rely on the exchange’s reports, team decisions, and long-term discipline.

So, CEX tokens can capture value, but the quality of that value capture depends on transparency, consistency, and how directly the burn connects to real usage.

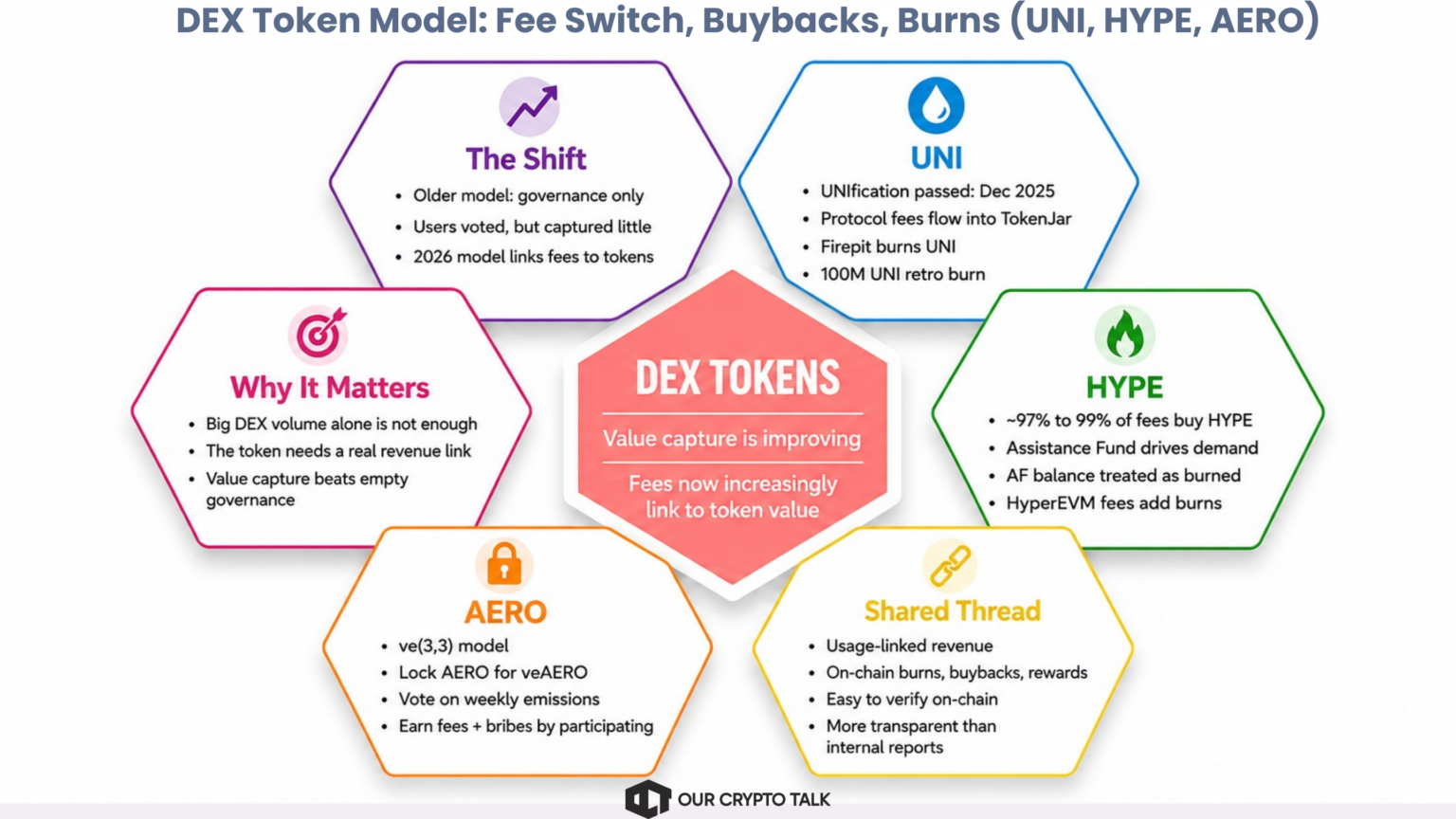

Decentralized-exchange tokens, or DEX tokens, have historically struggled with value capture. Many DEXs handled huge trading volume, but their tokens only offered governance rights. In simple terms, holders could vote, but they did not receive a clear share of the fees.

That model has started to change. In 2026, the strongest DEX token designs increasingly connect trading activity to the token through fee switches, buybacks, burns, or direct rewards.

UNI shows the clearest shift from governance-only to value accrual. For years, Uniswap generated major trading volume while UNI mainly acted as a governance token. Holders could vote on proposals, but the token had no direct link to protocol revenue.

That changed after the UNIfication proposal passed in late December 2025. Under this model, protocol fees flow into a system called TokenJar. Those fees can only leave TokenJar by burning UNI through the Firepit mechanism. A burn means the protocol permanently removes UNI from circulation. Therefore, as Uniswap earns fees, the system can reduce UNI supply.

UNIfication also introduced a one-time 100 million UNI retroactive burn. This burn aimed to account for years of missed value capture while Uniswap grew without passing meaningful economics to UNI. The important point is not only the burn itself. The bigger change is that UNI moved from a pure governance token toward a token with usage-linked value accrual.

HYPE takes a more aggressive route. Hyperliquid uses its Assistance Fund to direct almost all trading fees, roughly 97% to 99%, toward buying HYPE from the open market. This creates direct demand because the protocol regularly buys its own token using real exchange revenue.

The ecosystem also treats the Assistance Fund balance as effectively burned, and validators formally recognized that balance as burned. In addition, HyperEVM fees are burned at the execution layer, which adds another supply-reduction mechanism. Together, these features make HYPE one of the most aggressive revenue-to-token models in crypto. When trading volume rises, fees rise. When fees rise, the buyback engine becomes stronger.

AERO uses a different model. Aerodrome runs on a ve(3,3) system, which means holders lock AERO to receive veAERO, or vote-escrowed AERO. Once users hold veAERO, they can vote on where weekly token emissions should go. In return, they earn trading fees and bribes from projects that want more liquidity directed toward their pools.

This structure does not reward passive holders in the same way as a simple buyback or burn. Instead, AERO rewards participation. Users who lock, vote, and manage their position can capture trading fees and incentives. So, value flows to active participants rather than everyone who simply holds the token.

These three examples show how DEX token design is maturing. UNI uses a fee switch and burn model. HYPE uses buybacks and burns. AERO uses locking, voting, fees, and bribes. The mechanics differ, but the shared thread is clear: DEX tokens increasingly tie value to real, on-chain, usage-linked revenue.

That matters because anyone can verify these systems on-chain. Investors do not need to rely only on internal company reports or opaque exchange disclosures. They can track fees, burns, buybacks, and distributions directly. This transparency gives DEX tokens a major advantage when the mechanism works.

The easiest way to compare exchange tokens is to ask one question: when the exchange earns fees, what happens to the token?

Readout: HYPE and UNI create the most direct link between exchange usage and token value because trading fees feed buybacks, burns, or supply reduction. AERO also captures value, but it rewards active lockers rather than passive holders. On-chain mechanisms are easier to trust than reported ones because investors can verify the flows directly instead of relying on internal exchange numbers. For more information on HYPE, read Hyperliquid vs dYdX 2026: Fees, Liquidity & Performance.

Value capture sounds powerful, but it does not remove risk. Burns, buybacks, and fee switches can help a token, but they do not guarantee upside. Investors still need to check whether the mechanism is strong enough to matter after emissions, unlocks, and market cycles.

The first risk is unlocks and dilution. A burn headline can look impressive, but it means little if the project creates or releases more tokens than it destroys. Many tokens still have team allocations, investor unlocks, incentive programs, or liquidity rewards entering circulation over time. If those new tokens hit the market faster than burns remove supply, net supply can still rise. Therefore, investors should not only ask, “How many tokens did the project burn?” They should ask, “Is circulating supply actually falling after emissions and unlocks?”

The second risk is LP flight, which matters most for DEXs. LPs, or liquidity providers, supply the assets that traders use on decentralized exchanges. In return, they earn a share of trading fees. If a protocol turns on a fee switch and takes too much of that revenue for token burns, LPs may earn less. As a result, they may move liquidity to rival venues with better returns. Lower liquidity can create worse trading prices, weaker volume, and fewer fees. That can starve the same burn engine the token depends on. This is the main risk to UNI’s value-accrual thesis.

The third risk is governance-only token design. Many exchange tokens still give holders voting power but no automatic link to revenue. These tokens may let holders vote on upgrades, treasury spending, or fee changes. However, if the token has no burns, no buybacks, and no fee-share, it does not capture exchange revenue directly. Beginners often miss this point because governance sounds useful. In reality, a token that only votes can remain economically weak even if the protocol itself grows.

The fourth risk is reflexivity. Buyback models work best when trading volume stays high. In bull markets, volume rises, fees grow, and buybacks become stronger. However, in bear markets, volume can fall quickly. When fees shrink, buybacks weaken at the exact moment holders want support. That does not make buyback models bad, but it means investors should not treat them as permanent price floors.

In short, value capture only matters if it survives real market conditions. Net supply, liquidity behavior, token unlocks, and trading volume all decide whether the model works in practice.

Before buying any exchange token, do not start with the chart. Start with the value-capture mechanism. The token may trade well for a period, but the long-term question stays the same: how does exchange activity benefit the token?

Use these questions as a repeatable checklist.

Does revenue actually reach the token, or only the exchange and LPs?

Exchange tokens can generate large trading fees without passing any value to its token. Centralized exchanges may keep revenue inside the company. Decentralized exchanges may send most fees to liquidity providers, or LPs, who supply assets for traders. Therefore, the first question is whether the token receives any direct benefit from fees. Look for burns, buybacks, fee-share, or another clear mechanism that connects revenue to the token.

Is the mechanism on-chain and verifiable, or reported and discretionary?

On-chain means anyone can check the activity on a blockchain. This makes burns, buybacks, fee flows, and distributions easier to verify. Reported and discretionary means the exchange or team announces the action, but holders must trust the internal numbers and future decisions. Neither model automatically succeeds or fails, but on-chain mechanisms usually give investors more transparency.

Is net supply falling after emissions and unlocks, not just gross burns?

Gross burns show how many tokens the project destroyed. Net supply shows what happened after new tokens entered circulation. This distinction matters. If a project burns 10 million tokens but releases 30 million through team unlocks, investor unlocks, rewards, or incentives, supply still rises. So, the better question is not “How much did they burn?” It is “Is circulating supply actually going down?”

Does value accrue passively, or only if you lock, stake, or participate?

Some models benefit all holders through supply reduction. Burns and broad buybacks can support passive holders because they reduce supply or create market demand. Other models require action. For example, a holder may need to lock tokens, stake them, vote on emissions, or manage a position to earn fees. Both models can work, but they serve different types of investors. Passive holders should not assume they receive the same benefits as active participants.

Does the mechanism depend on volume that could evaporate in a downturn?

Most exchange-token models depend on trading activity. When volume rises, fees rise. When fees rise, burns, buybacks, or fee-share can become stronger. However, bear markets often reduce volume. If fees fall, the value-capture engine can weaken at the exact moment holders expect support. This does not make the model useless, but it means investors should stress-test it across different market conditions.

This article is educational analysis, not financial advice. Always do your own research.