Telcoin ($TEL) Review: Is TEL Worth Buying in 2026?

An honest review of Telcoin covering telecom-powered remittances, tokenomics, MNO partnerships, risks, and whether $TEL is a strong 2026 bet.

Author: Akshat Thakur

Why Crypto Remittance and Mobile Money Platforms Are Hard to Get Right

Crypto remittance projects sound simple. Move money faster, charge lower fees, and remove banking intermediaries. In practice, very few have succeeded.

The biggest challenge is distribution. Building a blockchain is easier than convincing millions of users to change how they send money. Most remittance platforms secure partnerships, run pilot programs, and generate headlines. Very few reach meaningful transaction volume.

The economics are also tougher than they appear. Remittance fees are already competitive in many corridors, while compliance, liquidity management, and local payment infrastructure remain expensive. Many projects end up relying on token incentives to drive activity, creating long-term sell pressure instead of sustainable growth.

Regulation creates another hurdle. Cross-border payments require KYC, AML, licensing, and relationships with local financial providers. A technically sound platform can still fail if it cannot navigate regulatory requirements across multiple jurisdictions.

This is why comparisons to Ripple or Wise often miss the point. The challenge is not moving value on-chain. The challenge is building a system people actually use.

Telcoin takes a different approach. Instead of targeting banks or crypto-native users, it focuses on telecom operators and mobile money networks. The thesis is straightforward: billions of people have phones but limited access to affordable financial services.

It is a focused strategy. That helps differentiate Telcoin from broader payment networks. But specialization alone is not enough. The model only works if telecom partnerships translate into real user activity and transaction volume.

What Is Telcoin?

If you’re searching “what is Telcoin” or looking for a Telcoin review, the simplest answer is that Telcoin is a blockchain-powered remittance platform built around telecom networks.

Founded in 2017 by Paul Neuner, the project aims to connect mobile users with low-cost financial services through existing telecom infrastructure. Rather than building a completely new financial system, Telcoin attempts to use networks that already reach billions of people.

The idea comes from a simple observation. Mobile phone adoption has expanded much faster than banking access in many parts of the world. Telcoin believes telecom operators can become distribution partners for payments, remittances, and digital financial services.

The network itself is built as an EVM-compatible Layer 1 secured by telecom operators through a Proof-of-Stake model. The TEL token powers transactions, governance, and incentives across the ecosystem.

What makes Telcoin interesting is not the blockchain itself. Plenty of projects offer payments and remittances. The differentiator is the telecom-first approach. If telecom operators become active participants in the network, Telcoin gains access to a distribution channel most crypto projects simply do not have.

The opportunity is clear. So is the risk. Telecom partnerships look impressive on paper, but the industry is known for moving slowly.

How Telcoin Works

Telcoin’s user experience is designed to feel closer to a fintech app than a traditional crypto application.

A user sends money through the Telcoin app or a partner integration. The transfer moves through TELx, Telcoin’s liquidity infrastructure, where assets can be converted and routed efficiently. Settlement occurs on-chain, and recipients receive funds through supported mobile wallets, e-money accounts, or local cash-out options.

The process matters because it removes many of the friction points that normally slow crypto adoption. Most users do not want to manage private keys, bridge assets between chains, or understand blockchain mechanics. They simply want money to arrive quickly and cheaply.

Behind the scenes, the system combines blockchain settlement with telecom distribution. The network handles transactions, while mobile money partners provide local access points for end users.

This is where Telcoin’s model becomes more interesting than a typical remittance token. The project is not trying to convince users to become crypto natives. It is trying to hide the complexity entirely.

The challenge is execution. Fast settlement means little if liquidity is shallow or payout networks remain limited. The user experience is only as strong as the infrastructure supporting it.

Technology & Architecture

At the protocol level, Telcoin takes a different path from most payment-focused crypto projects.

The Telcoin Network is an EVM-compatible blockchain secured by telecom operators rather than traditional validator groups. Only approved GSMA member operators can participate in validation, creating a security model tied directly to established telecommunications infrastructure.

Supporters will see this as a major strength. Telecom companies already manage critical infrastructure, operate under regulatory oversight, and maintain large customer bases. Bringing them into network validation creates a direct link between blockchain infrastructure and real-world distribution.

Critics will point to centralization concerns. Restricting validator participation inevitably reduces openness compared to permissionless networks. The tradeoff is greater regulatory alignment and operational accountability.

The network is supported by TELx, a liquidity layer designed to facilitate swaps, remittances, and on-chain financial activity. Together, the blockchain and liquidity infrastructure form the foundation of Telcoin’s broader ecosystem.

The roadmap remains focused on bringing telecom operators fully on-chain as validators and expanding the network’s remittance capabilities. That is the right priority. Without active operators and real transaction flow, the technology itself offers little advantage.

Compared with projects like XRP or Stellar, Telcoin’s differentiator is clear. It is not trying to win banks. It is trying to win telecoms.

My view is that this approach makes more sense than launching another generic payments network. The telecom angle gives Telcoin a unique position in the market. The question is whether telecom adoption arrives fast enough to justify the thesis. That remains the biggest variable for TEL in 2026.

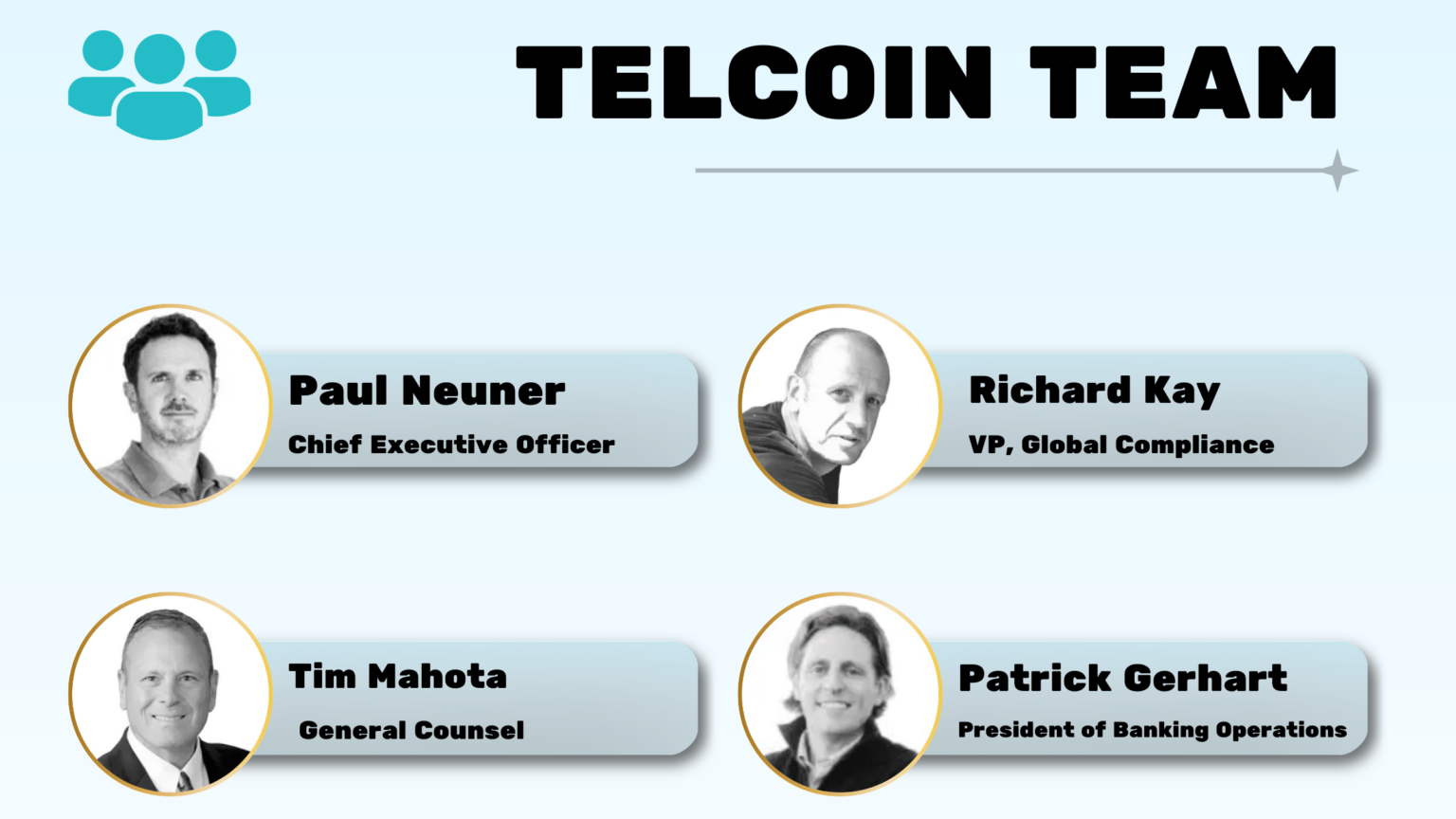

Team & Backers

One area where Telcoin stands out from many crypto payment projects is the team’s background. Most remittance tokens are built by crypto-native founders trying to enter financial services. Telcoin took the opposite route.

Paul Neuner comes from the telecom industry and previously built Mobius Wireless Solutions, a fraud management and revenue assurance platform used by mobile network operators. That experience matters because Telcoin’s entire thesis depends on telecom adoption. The company is not trying to disrupt operators. It is trying to work alongside them.

The broader leadership team follows the same pattern. Many executives come from telecom, compliance, security, and regulated financial services backgrounds. That may not generate hype, but it is relevant for a project operating in one of the most heavily regulated sectors in crypto.

Funding also reflects this approach. Telcoin has raised tens of millions of dollars through private rounds and strategic financing, including capital tied to the development of the Telcoin Digital Asset Bank. Unlike many payment tokens that rely primarily on retail speculation, Telcoin has spent years building relationships with regulated institutions and telecom stakeholders.

Its association with the GSMA is arguably more important than any funding round. The Telcoin Association exists specifically to represent telecom operators participating in governance and network development. Validator participation is restricted to eligible GSMA member operators, creating a structure that directly aligns the network with telecom infrastructure.

This approach has clear advantages. Telecom operators already have distribution, compliance experience, and access to millions of users. If Telcoin succeeds, those relationships become a significant moat.

The downside is that progress depends on large organizations moving quickly. Telecom companies are not known for rapid innovation. Telcoin’s biggest strength and biggest risk come from the same place: its dependence on operator adoption.

Telcoin Tokenomics (TEL)

Token Overview

TEL has a maximum supply of 100 billion tokens, with more than 96% already in circulation. That immediately separates it from many newer projects that still face years of large unlock schedules.

The token serves multiple purposes across the ecosystem. It functions as the native gas asset for the Telcoin Network, supports governance through the Telcoin Association, and powers incentives across liquidity, remittance, and validator programs.

The supply profile creates an interesting dynamic. On one hand, most of the major historical unlocks are already behind the project. On the other hand, TEL remains far below its 2021 peak, showing that circulating supply alone does not guarantee price performance.

Ultimately, TEL’s future value depends less on scarcity and more on whether the network generates meaningful usage.

Token Allocation

The initial allocation heavily favored ecosystem growth. Large portions of supply were dedicated to incentives, liquidity programs, partnerships, and user acquisition rather than purely investor ownership.

That decision makes sense for a remittance network. Adoption requires liquidity, active users, and distribution partners. Without incentives, reaching scale becomes difficult.

At the same time, large ecosystem allocations create ongoing supply pressure. Tokens used to drive growth eventually enter circulation, and markets must absorb them.

This is a common tradeoff across payment networks. Growth requires incentives. Incentives create dilution.

Vesting & Unlock Pressure

The good news for TEL holders is that most early investor and team allocations have already vested. The market has spent years absorbing that supply.

The more relevant issue today is treasury emissions.

The Telcoin Association continues allocating tokens toward validator rewards, network operations, and ecosystem expansion. For a network still in its growth phase, that approach is understandable. Validator participation and liquidity do not appear automatically.

The concern is whether growth eventually outpaces dilution.

If remittance volume increases, network activity expands, and transaction demand rises, emissions become easier to justify. If adoption remains slow, treasury distributions simply create additional sell pressure.

This remains one of the most important variables for TEL in 2026.

Token Utility

TEL is deeply integrated into the network rather than existing as a purely speculative asset.

Transactions on the Telcoin Network require TEL for gas. Validators receive TEL incentives for securing the chain. Governance decisions flow through TEL ownership, while liquidity providers and ecosystem participants can earn rewards through network activity.

That gives the token genuine utility, which is something many payment-focused projects struggle to achieve.

However, utility alone does not create value accrual.

The key question is whether people actually use the network. A token can have multiple functions and still underperform if transaction volume remains limited. Real remittance activity matters far more than theoretical utility.

My view is that TEL’s tokenomics are stronger than many remittance-focused competitors because most supply is already circulating and the token has clear network functions. The weakness is that value accrual still depends heavily on adoption. Until transaction volume scales meaningfully, TEL remains a utility token waiting for its core thesis to play out.

Is Telcoin Safe?

If you’re asking “is Telcoin safe?”, the answer is more nuanced than a simple yes or no.

On the positive side, Telcoin has invested heavily in compliance, audits, and regulatory infrastructure. The project has undergone multiple third-party security reviews, maintains ongoing testing procedures, and operates with a level of regulatory oversight that most crypto projects never reach.

Its validator model is also unique. Instead of allowing anyone to run a node, validation is restricted to approved GSMA member mobile network operators. Supporters argue this creates a more accountable and secure network because validators are known entities with existing infrastructure, regulatory obligations, and reputational risk.

The tradeoff is obvious. Security comes at the cost of decentralization. Telcoin is not trying to compete with permissionless validator networks. It is prioritizing compliance and operator trust.

There are also historical incidents worth acknowledging. The Telcoin Wallet exploit in late 2023 exposed vulnerabilities in application-layer infrastructure, although affected users were reimbursed and security procedures were strengthened afterward. Importantly, the issue was not a failure of the underlying blockchain itself.

The biggest risk today is not security. It’s execution.

The Telcoin Network remains in its pre-mainnet phase, which means the system has not yet been tested under large-scale economic activity. Audits help. Certifications help. Neither replaces real-world stress testing.

My view is that Telcoin ranks above the average crypto project from a regulatory and operational perspective. However, investors should treat it as developing infrastructure rather than a battle-tested network. The foundation looks solid, but the most important tests are still ahead.

Telcoin vs Competitors

The biggest difference is positioning.

Ripple built for financial institutions. Stellar focused on open payment rails and anchor networks. Celo expanded into broader mobile payments and DeFi.

Telcoin is focused almost entirely on telecom distribution.

That gives it a unique angle. Mobile operators already have customer relationships, compliance processes, and local market reach. If those operators actively participate in the network, Telcoin gains an advantage that competitors cannot easily replicate.

Telcoin (TEL)

(GSMA MNO validators only)

Pre-mainnet

Mainnet targeted Q1 2026

Remittance app live

Ripple (XRP)

(Federated Consensus)

Tested >65K TPS

3–5s finality

Stellar (XLM)

Target: 5,000 TPS

2–5s finality

Celo (CELO)

(L2 migration underway)

1–5s finality target

(Espresso)

The problem is scale.

Ripple and Stellar already process real value across established networks. Telcoin is still proving that telecom adoption can translate into meaningful transaction volume.

My take is straightforward. Telcoin has the most differentiated strategy in the group. It also has the most execution risk because much of its thesis depends on future operator participation rather than existing network effects.

Strengths & Risks (Bull vs Bear Case)

The bull case starts with distribution.

Most crypto payment projects spend years searching for users. Telcoin already has relationships within the telecom industry and a governance model built around mobile network operators. If those relationships convert into active validators and payment corridors, the project gains access to a market that traditional crypto networks struggle to reach.

Regulation is another strength. The Nebraska Digital Asset Bank charter and broader compliance strategy give Telcoin a clearer regulatory path than many payment-focused competitors. That matters because remittances operate in one of the most heavily regulated sectors in finance.

The bear case is just as compelling.

Telecom adoption moves slowly. Large operators are cautious, highly regulated, and often resistant to change. Even if the technology works perfectly, commercial rollout can take years.

Token economics also remain a concern. Treasury emissions continue while the network scales. If remittance volume grows slower than expected, supply pressure can outweigh utility growth for extended periods.

Competition is another challenge. Ripple, Stellar, stablecoin providers, and traditional fintech companies are all fighting for the same payment flows. Telcoin’s niche is unique, but it is not uncontested.

My view sits somewhere in the middle. The telecom-first model is one of the more interesting ideas in crypto payments. The question is not whether the concept makes sense. The question is whether execution can match the ambition.

Should You Buy TEL? (OCT Verdict)

Builders should pay attention.

If you’re developing remittance products, mobile money applications, or telecom-integrated financial services, Telcoin offers infrastructure that few other networks provide. The combination of telecom validators, compliance-focused architecture, and mobile-first design creates a specialized environment for those use cases.

Traders should be more cautious.

The project still faces pre-mainnet uncertainty, ongoing emissions, and dependence on partnership execution. Major announcements can drive volatility in either direction.

For long-term investors, the decision comes down to one belief.

Do you think telecom operators will become meaningful participants in blockchain-based payments?

If the answer is yes, Telcoin becomes an interesting asymmetric bet. If the answer is no, the investment thesis becomes much weaker because the entire network is built around that assumption.

This is not a project to buy because of hype. It is a project to buy only if you understand and believe in the telecom adoption thesis.

Final Verdict: Is TEL a Buy in 2026?

Telcoin has built something most crypto remittance projects never achieve: a strategy that actually fits its target market.

Instead of chasing banks, institutions, or speculative narratives, it focuses on telecom operators and mobile money networks. That gives the project a clear identity and a genuine differentiator.

The challenge is that the hardest part still lies ahead.

Infrastructure is largely in place. Regulatory groundwork is strong. The next step is proving that telecom partnerships generate real transaction volume and sustainable demand for TEL.

My position is clear. Telcoin is one of the more credible remittance-focused projects in crypto, but it remains an execution story. The opportunity is significant if adoption arrives. The risk is that adoption takes far longer than the market expects.

That makes TEL a high-conviction bet on telecom-driven financial infrastructure, not a low-risk payment token.

Frequently Asked Questions

What is Telcoin?

How does Telcoin work?

When is Telcoin Network mainnet launching?

What is TEL used for?

Is Telcoin safe?

How is Telcoin different from Ripple?

Is TEL a good investment?

In this article

Why Crypto Remittance and Mobile Money Platforms Are Hard to Get RightWhat Is Telcoin?How Telcoin WorksTechnology & ArchitectureTeam & BackersTelcoin Tokenomics (TEL)Is Telcoin Safe?Telcoin vs CompetitorsStrengths & Risks (Bull vs Bear Case)Should You Buy TEL? (OCT Verdict)Final Verdict: Is TEL a Buy in 2026?