Author: Chirag Sharma

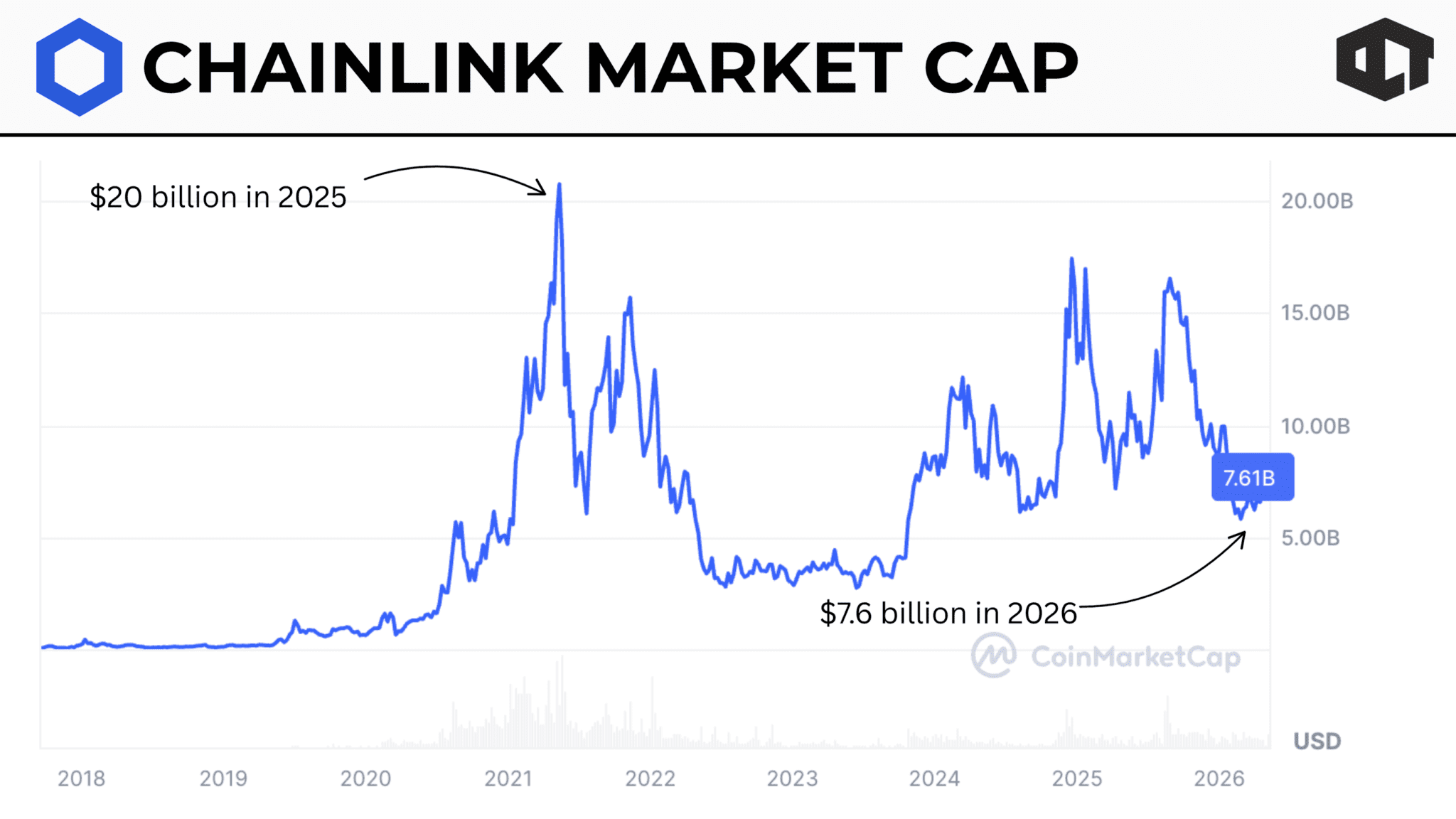

Chainlink (LINK) has become one of the most important infrastructure projects in crypto. Nearly every major DeFi protocol depends on its oracle network for accurate price feeds, real-world data, and secure communication between blockchains. Yet despite all this growth, the LINK token has struggled badly. LINK reached its all time high near $52 in May 2021. Since then, the network has expanded across DeFi, stablecoins, tokenized assets, and institutional partnerships. However, the token still trades far below those levels in 2026. This creates one of the biggest debates in crypto today.

If Chainlink is winning the infrastructure race, why is LINK still underperforming?

The answer is more complicated than most investors think. The issue is not whether Chainlink has utility. It clearly does. The challenge is how that utility translates into token value. Several structural problems continue to weigh on LINK’s price action. These include dilution pressure, weak value accrual, growing competition, and broader market narratives that currently favor speculation over infrastructure.

Still, many long-term investors believe the current disconnect could become a major opportunity if these issues improve over time.

One of the strangest things about Chainlink is that its fundamentals keep improving while its token struggles.

The network secures hundreds of billions in DeFi value. Major lending platforms rely on Chainlink price feeds daily. Cross-chain communication through CCIP is also becoming increasingly important as blockchains become more interconnected.

On top of that, Chainlink has positioned itself aggressively in the real-world asset sector.

Banks, institutions, and tokenization platforms continue exploring Chainlink integrations because reliable off-chain data remains critical for tokenized finance. Stablecoins and RWAs both require secure oracle systems to function properly.

This means Chainlink is not just surviving. It is expanding across nearly every important crypto sector.

However, crypto markets do not always reward utility immediately.

Investors often assume that growing adoption automatically leads to higher token prices. In reality, token performance depends heavily on how value flows back to holders. That is where LINK still faces challenges.

One of the biggest reasons LINK struggles is its token supply dynamics. Back during the 2021 bull market, Chainlink had a much lower circulating supply. Many investors viewed LINK as relatively scarce because only part of the total supply was actively circulating.

That scarcity narrative helped fuel explosive price action. Today, the situation looks very different.

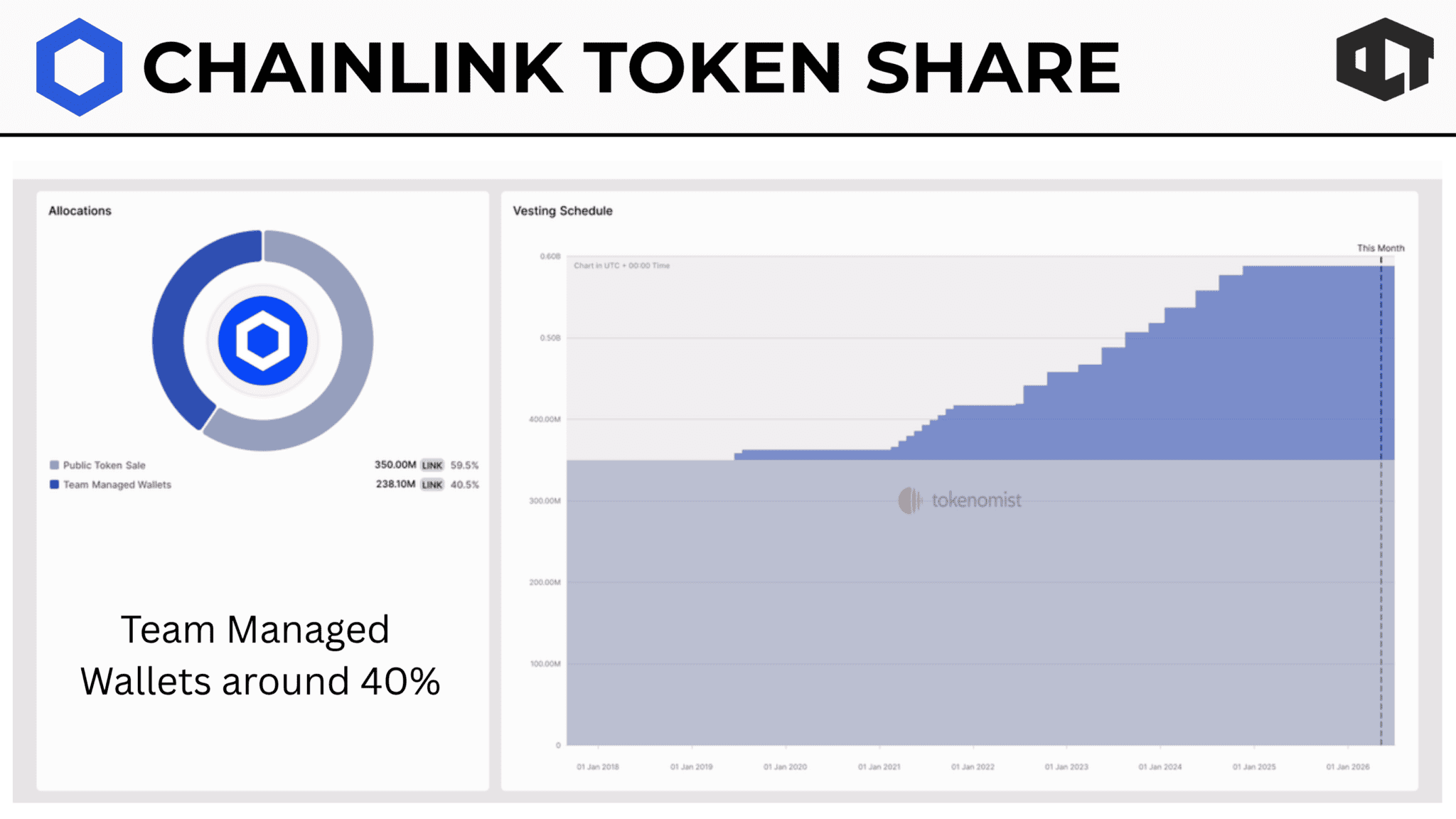

Roughly 727 million LINK tokens are already circulating out of the maximum 1 billion supply. The remaining supply continues unlocking gradually over time through ecosystem allocations, partnerships, and team distributions. This creates ongoing dilution pressure. Even though Chainlink has a capped supply, investors still worry about the steady flow of new tokens entering the market each year. Around 70 million LINK can enter circulation annually under current schedules.

That matters because price growth now requires demand to outpace these emissions consistently. Whale concentration also plays a role. Large holders reportedly control a major percentage of the supply. During accumulation phases, this can tighten liquidity and support price action. However, it also increases volatility whenever large wallets move tokens or sell into rallies.

Chainlink has attempted to address some of these concerns through newer mechanisms. The Chainlink Reserve, introduced in 2025, aims to buy back and lock LINK using protocol-related revenue. Staking also encourages some long-term holding behavior by offering modest yields.

Still, these mechanisms remain relatively small compared to overall emissions. For many investors, LINK no longer feels like a “low supply” asset the way it did in 2021. That narrative shift alone has impacted speculative momentum significantly.

Chainlink may have one of the strongest utility cases in crypto. The network powers DeFi applications, supports stablecoins, enables interoperability, and secures massive financial activity daily. Few infrastructure protocols have reached this level of adoption.

The problem is that LINK holders do not always benefit directly from that growth.

This is one of the most misunderstood parts of Chainlink’s economics. Node operators use LINK as collateral and receive payments in LINK for providing services. However, many operators sell those rewards quickly to cover operational costs. That creates continuous market sell pressure instead of long-term token accumulation.

Some enterprise integrations also abstract away direct LINK usage.

In several cases, institutions can pay through fiat or other systems while the backend handles token conversion automatically. While this still technically uses LINK, the demand becomes less visible to markets compared to models that aggressively burn tokens or distribute revenue directly to holders. This weakens the psychological connection between network success and token appreciation.

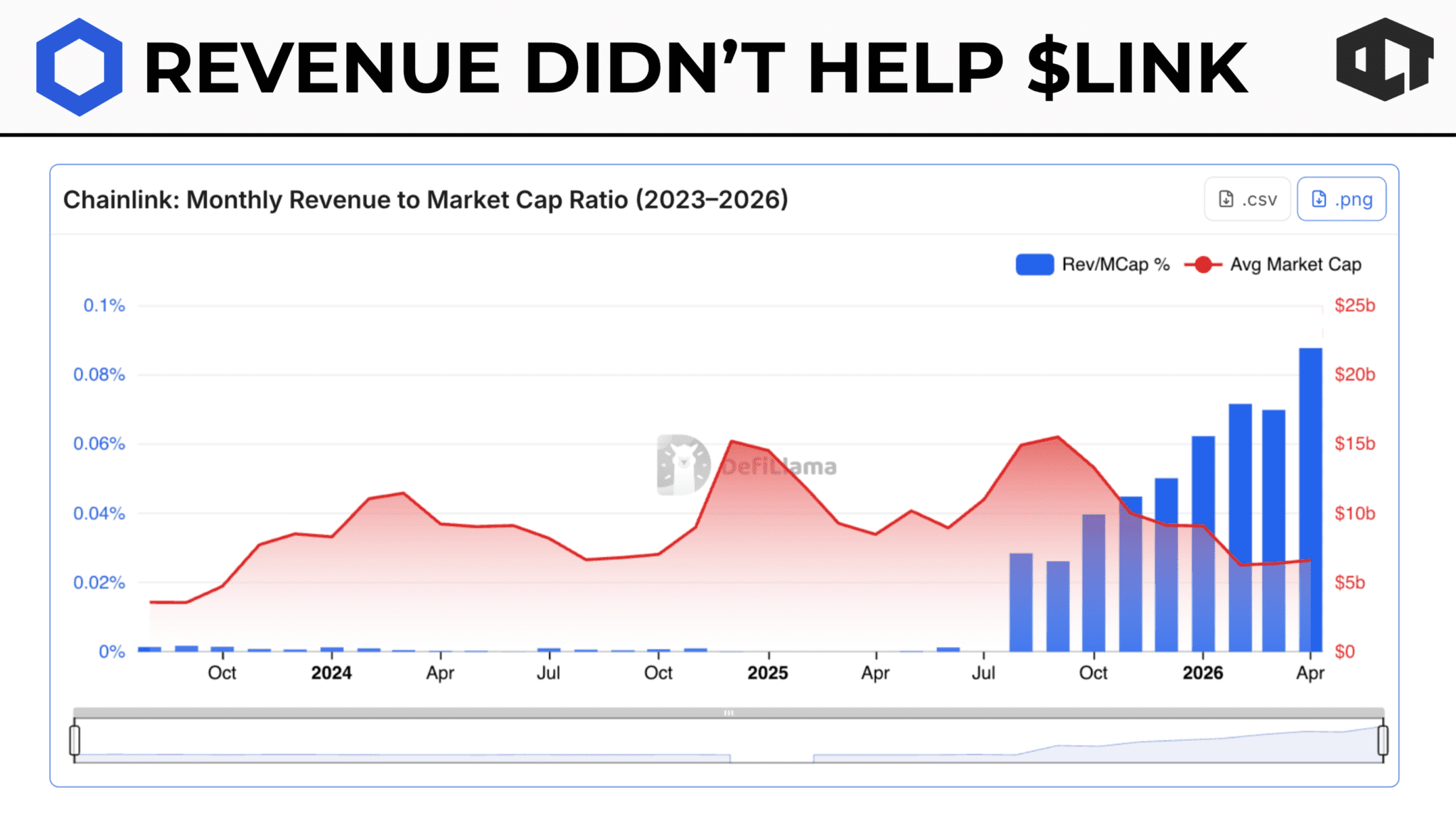

Chainlink’s Economics 2.0 initiative aims to improve this situation.

The idea is to create stronger alignment between protocol growth and holder value through staking rewards, fee systems, and reserve-based buybacks. If adoption continues scaling aggressively, these systems could eventually create a stronger token flywheel. However, current revenue figures still remain relatively modest compared to Chainlink’s overall importance.

That is why many investors feel frustrated. The network appears dominant, yet the token does not behave like a high-growth asset. Until value capture improves meaningfully, LINK may continue struggling to reflect Chainlink’s real ecosystem position.

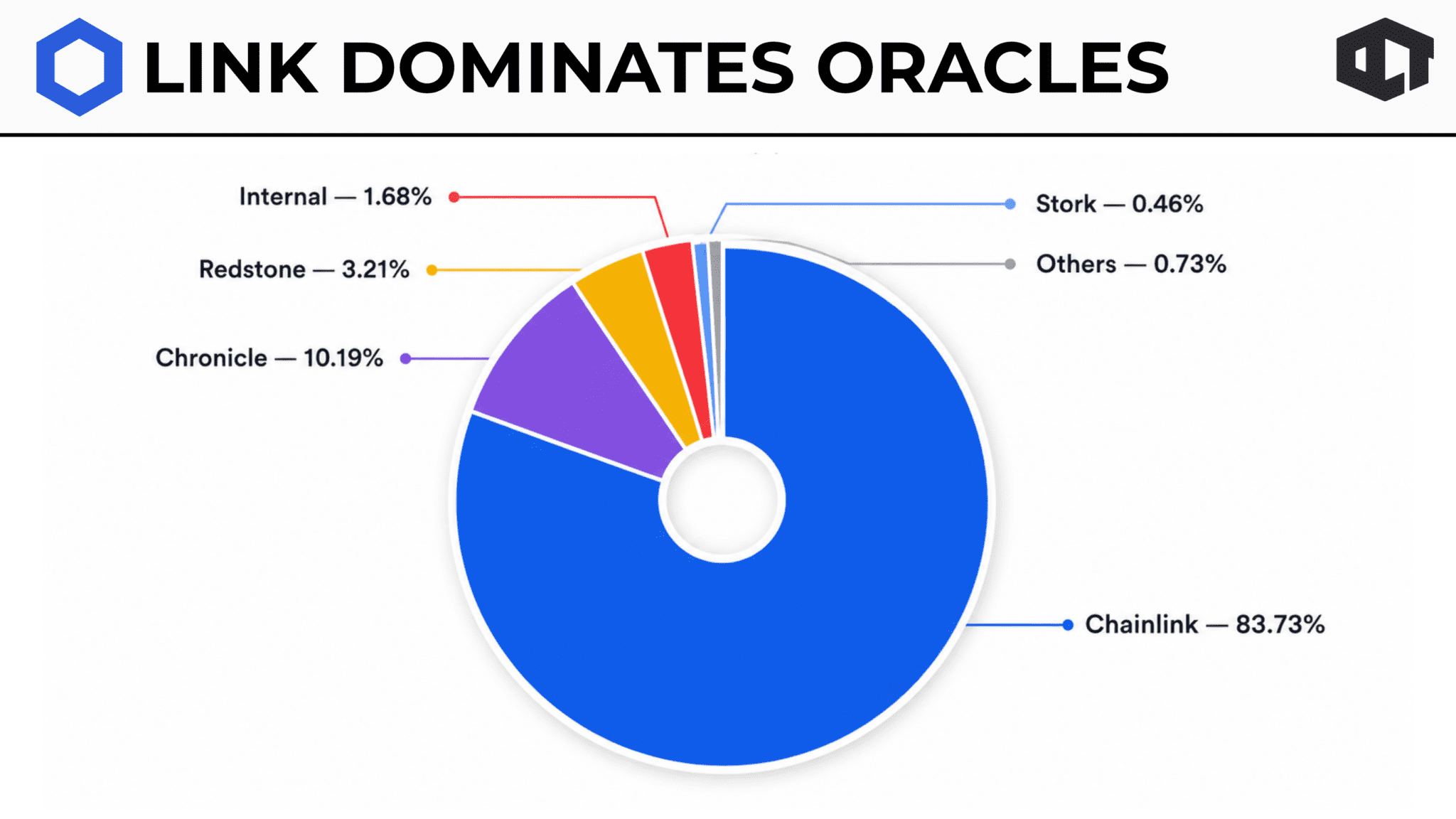

Chainlink still dominates the oracle market, but competition is no longer insignificant. Several newer projects now offer specialized solutions targeting specific ecosystems and use cases.

Pyth Network has become particularly strong in high-frequency trading environments, especially across Solana-related applications. RedStone has gained traction by offering flexible and cost-efficient oracle models. API3 focuses on first-party oracle systems, while Band Protocol continues expanding cross-chain capabilities. Each competitor tries attacking a different weakness. Some focus on lower costs. Others prioritize faster updates or ecosystem-specific optimizations.

This does not mean Chainlink is losing leadership. It still remains the most trusted oracle provider for high-value applications and institutional-grade systems. However, the monopoly narrative has weakened.

In crypto markets, narrative strength matters heavily. Investors reward projects that appear dominant and irreplaceable. Once competition starts fragmenting attention, speculative enthusiasm often declines. Many protocols now use hybrid oracle setups instead of relying entirely on Chainlink alone. That trend matters because it limits Chainlink’s ability to capture every part of future oracle-driven growth. Even if LINK remains the industry leader, reduced exclusivity can still impact long-term valuation multiples.

Competition also changes developer behavior.

New projects entering crypto today have far more choices than developers did in 2020 or 2021. This naturally reduces Chainlink’s ability to dominate mindshare the same way it once did during earlier DeFi cycles.

Sometimes the biggest factor is simply market psychology. The current crypto cycle has rewarded very different sectors compared to 2021.

Back then, infrastructure narratives performed extremely well. Investors aggressively chased oracle projects, interoperability plays, and DeFi infrastructure because those sectors represented the future of blockchain growth. Today, capital flows differently.

Memecoins, AI tokens, and high-volatility speculative assets dominate retail attention. Bitcoin also absorbed enormous institutional flows through ETFs, pulling liquidity toward large-cap assets. Infrastructure projects like Chainlink often struggle in these environments because they move slower and rely on long-term adoption rather than explosive hype cycles.

Ironically, Chainlink’s growth has become more institutional and mature exactly when markets became more speculative.The project continues announcing integrations, CCIP expansion, and enterprise partnerships. However, these developments rarely generate the same excitement as fast-moving meme narratives or AI speculation.

There is also the broader macroeconomic backdrop. Higher interest rates and tighter liquidity conditions have reduced appetite for slower-moving altcoins across the board. Many mid-cap infrastructure projects remain trapped below previous cycle highs despite strong development activity.

LINK became a victim of this environment. Even though its fundamentals improved steadily, the market simply stopped prioritizing infrastructure narratives during large portions of this cycle.

Despite all these challenges, many investors still believe LINK has strong long-term potential. The reason is simple.

Very few crypto projects have achieved the level of real adoption that Chainlink currently enjoys.

If the stablecoin sector expands dramatically, Chainlink benefits. If tokenized real-world assets become mainstream, Chainlink likely becomes critical infrastructure. If cross-chain communication becomes essential, CCIP could become increasingly valuable.

The long-term thesis still exists. What needs to change is the connection between network growth and token demand.

If Economics 2.0 successfully improves value accrual, staking participation rises, and reserve-based buybacks scale aggressively, LINK could eventually regain stronger momentum. Market conditions also matter heavily.

A true altseason would likely benefit infrastructure projects significantly. During euphoric cycles, investors often rotate into fundamentally strong assets after speculative sectors become overheated. That environment could help LINK outperform again.

However, reaching another all time high will not be easy.

The token now faces more competition, higher circulating supply, and a far more mature market than it did in 2021. Investors expecting a straight return to previous highs may underestimate how much the landscape has changed. Still, Chainlink remains one of the few crypto projects with undeniable real-world relevance.

That alone keeps many long-term believers interested despite years of disappointing price action.

Chainlink’s biggest challenge is not technology. It is token economics and market perception. The network itself continues expanding across DeFi, RWAs, stablecoins, and interoperability. Few projects can match its infrastructure importance within crypto today.

Yet LINK still struggles because utility alone does not guarantee strong token performance. Dilution concerns, weak direct value accrual, rising competition, and shifting market narratives have all limited upside during this cycle. Until those structural issues improve, LINK may continue underperforming relative to its ecosystem importance.

At the same time, this disconnect could eventually create opportunity. If Chainlink successfully strengthens its economic flywheel while crypto markets rotate back toward infrastructure narratives, LINK could regain momentum over the coming years.

The question is no longer whether Chainlink matters. The real question is whether the LINK token can finally capture the value the network continues creating behind the scenes.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.