Stablecoin lending alternatives 2026: compare safe yield options, DeFi lending, T-bill tokens, wrappers, CeFi risks, and LP pools.

Author: Kritika Gupta

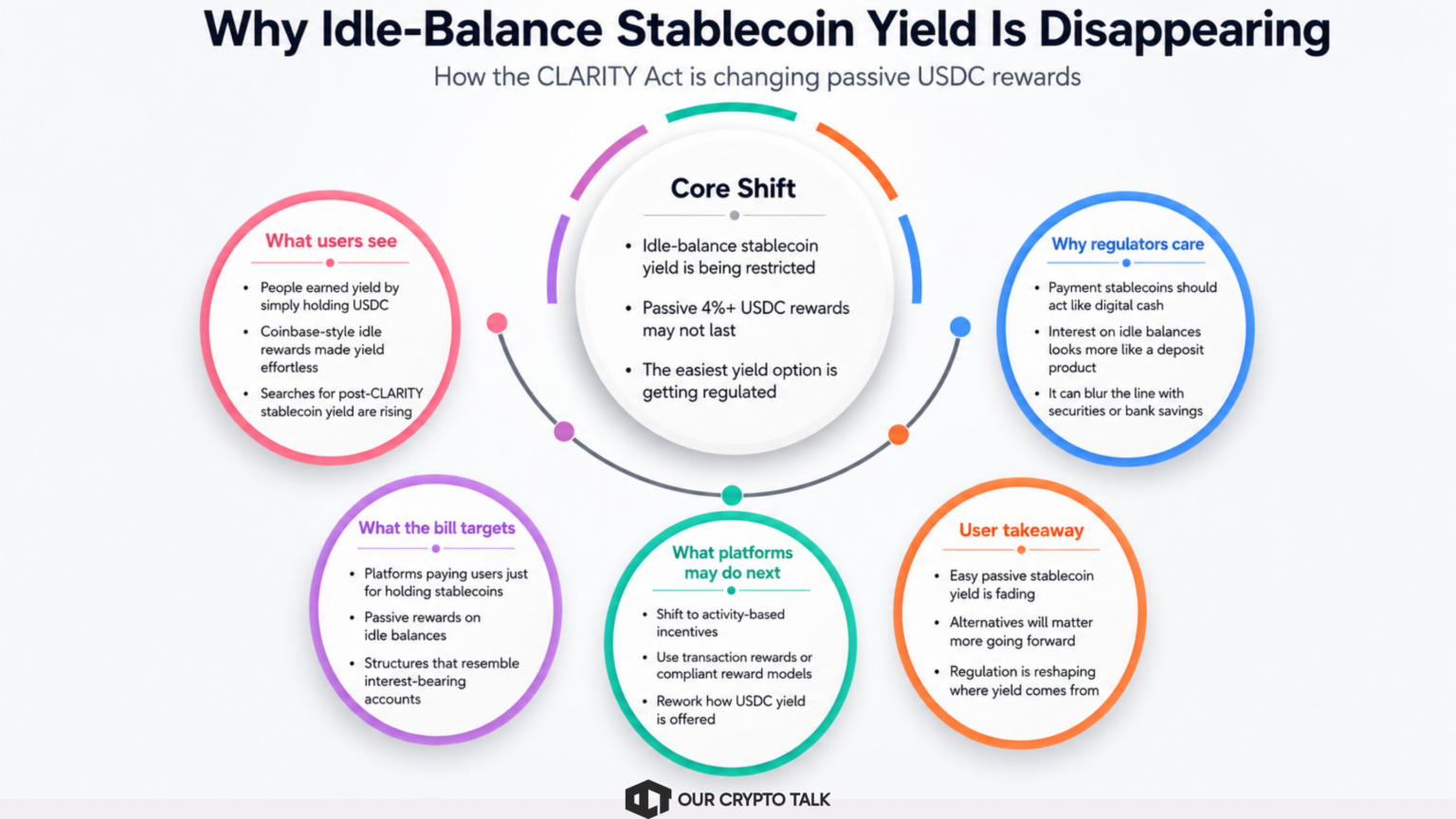

If you’ve been earning 4%+ on USDC just by holding it in a Coinbase account, that easy yield model may not survive in its current form. The CLARITY Act, the digital asset regulation bill moving through the US Senate, restricts how stablecoin issuers and platforms can offer passive yield on idle balances. As a result, crypto users now need to compare stablecoin lending alternatives 2026 more carefully instead of relying on one-click rewards from centralized platforms.

The key issue is simple: regulators want payment stablecoins to function like digital cash, not like bank deposits or securities. When platforms pay users just for holding stablecoins, that line becomes blurry. Products such as Coinbase USDC Rewards may need to restructure, while DeFi lending protocols, T-bill backed tokens, yield-bearing wrappers, and liquidity pools offer different paths to stablecoin yield.

If you’ve been earning 4%+ on your USDC just by holding it in a Coinbase account, that’s about to change. The CLARITY Act, the digital asset regulation bill moving through the US Senate, restricts how stablecoin issuers and platforms can offer yield on idle balances. That is why searches for stablecoin yield after Clarity Act are rising now: users want to know where the yield goes when the easiest option gets regulated.

The issue comes down to how regulators define stablecoins. Lawmakers want payment stablecoins to function like digital cash, not like securities or bank deposits. When an issuer or platform pays users just for holding USDC, that product starts to look like a deposit account with interest. The CLARITY Act targets that exact structure because it blurs the line between stablecoins, bank savings products, and investment contracts.

This matters because platforms like Coinbase USDC Rewards may need to change how they offer yield. Instead of paying passive rewards on idle balances, they may need to shift toward activity-based incentives, transaction rewards, or other compliant structures. For users, the takeaway is simple: the easiest stablecoin yield option is getting regulated, so alternatives now matter.

Stablecoin yield only makes sense after users answer one question: where does the money come from? That question separates the old DeFi yield era from the new one. In 2020–2022, many protocols created “yield” by printing their own tokens and handing them to users as rewards. Compound popularized this model when users earned COMP for lending, and dozens of protocols copied the playbook. The APY looked attractive, but the yield often depended on inflationary token emissions instead of real income.

That model worked only while token prices kept rising. Once the market turned, the math broke. Protocols kept printing rewards, token prices collapsed, and “20% APY” often became a net loss after users accounted for falling reward-token value, borrowing costs, and liquidation risk. Terra’s UST collapse in May 2022 gave the market the clearest warning. Anchor offered roughly 20% yield on UST, but real economic activity did not support that return. When confidence disappeared, the yield disappeared with it.

By contrast, the new DeFi yield era from 2024–2026 looks more grounded. Sustainable yield now comes from real economic activity, including US Treasury bills, institutional borrowing demand, and trading fees. Ondo’s USDY passes through income from Treasury-backed assets. Sky’s sUSDS earns from a mix of protocol collateral, RWAs, and lending activity. Aave pays suppliers from borrower interest. These products usually offer lower APYs, often in the 3–8% range, but the source of yield looks more durable because real assets or real users generate it.

That distinction should change how every crypto reader evaluates stablecoin yield. If someone offers 20% APY on stablecoins in 2026, ask one question: where does the money come from? If the answer depends mainly on “our governance token,” run. Real yield may look less exciting than old farming APYs, but it gives users a better chance of surviving bear markets, regulation, and liquidity shocks.

“Where Does the Yield Come From?” Source Reference

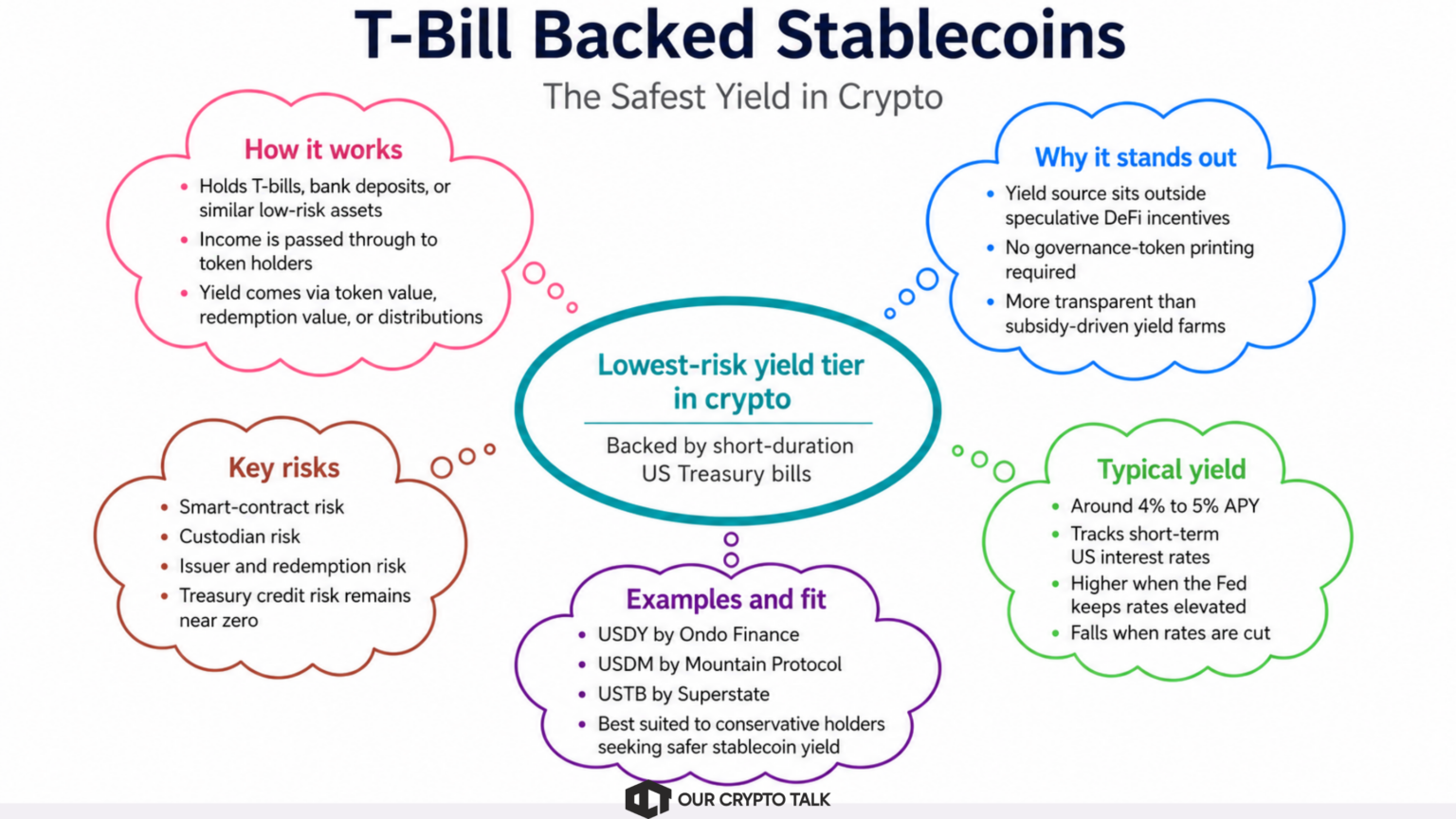

The lowest-risk stablecoin yield tier in crypto comes from T-bill backed stablecoins and tokenized Treasury products. These assets hold short-duration US Treasury bills, bank deposits, or equivalent low-risk instruments, then pass most of the income through to token holders. In practice, you hold the token while the underlying T-bills earn yield. The issuer keeps a management fee, and you receive the rest through a rising token value, redemption value, or yield distribution.

This model works because the yield source sits outside speculative DeFi incentives. US Treasury bills currently generate roughly 4–5%, so products in this category can offer stablecoin yield without printing a governance token or relying on unsustainable subsidies. Examples include USDY from Ondo Finance, USDM from Mountain Protocol, and USTB from Superstate. USDY has become one of the most visible RWA stablecoin products, while USTB targets a more institutional tokenized Treasury market.

The typical APY sits around 4–5%, but users should understand what drives that number. T-bill backed stablecoins track short-term interest rates. When the Fed keeps rates high, these products can pass through stronger yield. When the Fed cuts, the yield drops. That makes this category more transparent than old DeFi farms, but it also means users should not treat today’s APY as permanent.

The risk profile remains the lowest in crypto, but it does not fall to zero. US Treasury credit risk sits near zero, but users still take smart-contract risk from the token wrapper, custodian risk from whoever holds the underlying assets, and issuer risk from the company managing redemptions. Even so, this option fits conservative holders who want to earn interest on USDC safely without taking heavy crypto-native risk.

Yield-bearing stablecoin wrappers form the DeFi-native savings layer. Instead of holding a plain stablecoin like USDC, DAI, or USDS, users hold a wrapped version that automatically accrues yield. For example, a user deposits DAI and receives sDAI. Over time, sDAI’s value increases as the underlying stablecoins generate income. The user does not need to stake, claim rewards, or rebalance a position.

These wrappers generate yield through lending income, RWA income, or a mix of both. The protocol can lend deposited stablecoins to borrowers, allocate a portion of reserves to T-bills, or route capital through other approved income-producing strategies. That makes the yield source easier to understand than inflationary token farms. sUSDS from Sky, formerly MakerDAO’s savings-rate product, sits at the center of this category. sDAI and sFRAX follow similar logic, although each product uses different collateral, governance, and risk controls.

Typical APYs sit around 3–6%, depending on utilization, protocol decisions, collateral performance, and broader rate conditions. When borrower demand rises or RWA income improves, wrappers can pay more. When utilization falls or governance lowers the rate, the yield drops. This makes the return variable, but it also keeps the model more sustainable because the protocol does not need to manufacture APY from token emissions.

The risk profile sits in the low-to-medium range. Users take smart-contract risk from the wrapper protocol and governance risk from the system that controls rates and allocations. If the underlying lending markets or T-bill allocations perform poorly, the yield can fall. However, users do not need to manage LP positions, monitor reward tokens, or chase farms across chains. That makes these wrappers ideal for DeFi-native users who want passive stablecoin yield without active management.

The key insight is simple: yield-bearing stablecoins are becoming the savings accounts of DeFi. Hold sUSDS instead of idle USDC, and the token does the work in the background.

Stablecoin Yield Options at a Glance: Risk-Ranked Comparison (June 2026)

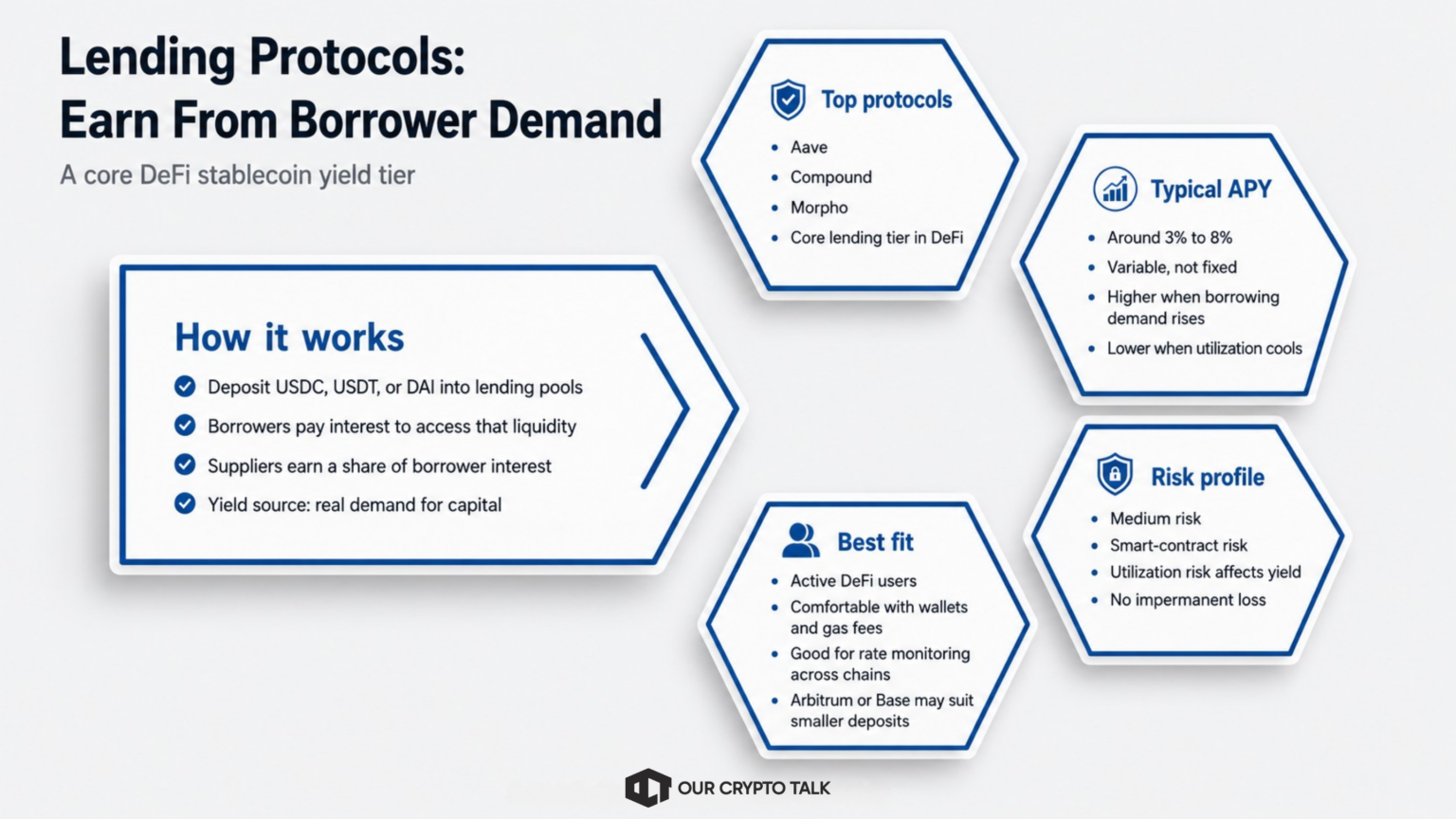

Lending protocols offer the most established DeFi route for stablecoin yield. Instead of holding USDC, USDT, or DAI idle in a wallet, users deposit those assets into a lending pool. Borrowers then pay interest to use that liquidity, and suppliers earn a share of that interest. This makes the yield source easy to understand: real borrowers pay for capital, and lenders receive the return.

Aave leads this category as the largest multi-chain lending protocol. Compound remains one of DeFi’s original money markets, with activity across Ethereum and Base. Morpho adds another layer by optimizing rates and matching lenders with borrowers more efficiently. Together, these protocols form the core lending tier for users searching for the best stablecoin yield 2026 without entering higher-risk LP strategies.

Typical APYs sit around 3–8%, but rates move constantly. When traders, institutions, or DeFi users borrow more stablecoins, utilization rises and lenders earn more. When borrowing demand cools, yields fall. That variable-rate structure makes lending more active than T-bill backed tokens or yield-bearing wrappers, but it also gives users access to market-driven returns.

The risk profile sits in the medium range. Users take smart-contract risk, although Aave has operated as one of DeFi’s most battle-tested lending protocols since 2020, with no major exploits on its core markets. Users also take utilization risk because lower borrower demand directly lowers yield. However, lending protocols do not expose users to impermanent loss, which makes them simpler than liquidity pools.

This option suits active DeFi users who feel comfortable with wallets, gas fees, chain selection, and rate monitoring. Aave on Arbitrum or Base can make more sense than Ethereum mainnet for smaller deposits because gas costs are significantly lower.

Centralized platforms still offer the easiest path to stablecoin yield, especially for beginners. Coinbase USDC Rewards is the clearest example: users buy USDC, hold it on Coinbase, and earn rewards without managing wallets, bridges, gas fees, or DeFi protocols. However, this model sits directly in the area the CLARITY Act could affect. If regulators restrict passive yield on idle stablecoin balances, Coinbase may need to restructure how it offers USDC rewards.

Other CeFi platforms such as Nexo, Ledn, and YouHodler also offer stablecoin yield, often with higher headline rates than Coinbase. But those rates come with a major trade-off: custody. When users deposit stablecoins into a CeFi platform, they trust that company to manage the funds, lend responsibly, maintain liquidity, and honor withdrawals. That makes the risk different from DeFi. In DeFi, users face smart-contract and protocol risk. In CeFi, users face counterparty risk.

Crypto already learned this lesson through Celsius, Voyager, and BlockFi. Earning 5% means nothing if the platform goes bankrupt and users lose 100%. That does not mean every CeFi yield product is unsafe, but it does mean users must read the fine print. CeFi yield is simple but custodial. DeFi yield requires more work, but users keep their keys. The right choice depends on technical comfort, risk tolerance, and how much trust a user wants to place in a centralized platform.

Liquidity pools can offer higher stablecoin yield, but they sit at the highest-risk end of this guide. In stablecoin-only pools, users provide assets such as USDC and USDT to venues like Curve, Aerodrome, or similar DeFi exchanges. Traders use those pools to swap between stablecoins, and liquidity providers earn a share of the trading fees. Because both assets aim to hold a $1 value, stablecoin LPs usually minimize impermanent loss compared with volatile pairs like ETH/USDC.

However, “minimize” does not mean “remove.” Stablecoin LPs still carry smart-contract risk, depeg risk, and incentive risk. If one stablecoin in the pair loses its peg, LPs can end up holding more of the weaker asset. Many pools also advertise APYs in the 5–15% range by adding token rewards on top of base trading fees. That extra APY can disappear quickly if the reward token loses value or emissions dilute holders.

This option fits experienced DeFi users who understand impermanent loss, can monitor pool composition, and know how to judge whether incentives are sustainable. If you are reading this article for the first time, skip LPs. Start with T-bill backed stablecoins or sUSDS. Come back to liquidity pools only after you feel comfortable with wallets, gas fees, bridges, depeg risk, and basic DeFi mechanics.

The best stablecoin yield option depends on how much risk, custody, and complexity you want to accept. Beginners should not start by chasing the highest APY. Instead, they should start with the cleanest yield source and move up the risk ladder only after they understand the trade-offs.

If you just want easy, safe yield, start with T-bill backed stablecoins such as USDY or USDM. You buy the token, hold it, and earn as the underlying Treasury-backed assets generate income. This route requires minimal DeFi knowledge beyond basic wallet use, and it gives conservative users the simplest way to earn stablecoin yield without relying on inflationary token rewards.

If you feel comfortable with DeFi wallets, consider yield-bearing stablecoin wrappers such as sUSDS or sDAI. These tokens accrue yield automatically in your wallet, so you do not need to manage lending positions, claim rewards, or rebalance across protocols. They suit users who already understand self-custody and want passive DeFi-native yield.

If you want the highest yield and understand the risks, lending protocols and stablecoin LP pools become more relevant. Aave and Compound let users earn from borrower demand, while stablecoin LP pools can add trading fees and token incentives. However, these options require more active management, stronger risk awareness, and regular monitoring.

If you do not want to think about it at all, Coinbase USDC Rewards remains the simplest user experience while it stays available in its current form. Users can hold USDC on Coinbase and earn rewards without touching DeFi. However, they should monitor whether CLARITY Act changes force Coinbase to restructure the product.

Start with the safest option. Earn for a month. If you want more, move up the risk ladder. Never start at the top.

This is educational content comparing yield options. All DeFi and CeFi products carry risk. Never invest more than you can afford to lose.