A full breakdown of Sam Bankman-Fried investments. The Anthropic, Cursor, SpaceX and Solana bets that would be worth $114 billion today.

Author: Tanishq Bodh

The story of Sam Bankman-Fried investments begins inside a low-rise federal prison in Mendota, California. A thirty-three-year-old man in a grey jumpsuit sits down for his email slot. He has fifteen minutes. He opens his messages. An article flashes past. Anthropic has just closed a new round at $82.3 billion. He reads it twice. Then he keeps scrolling, because that is what you do when you have fifteen minutes and twenty-two more years to sit with the knowledge that you once owned eight percent of the most important AI company on earth.

The full accounting of Sam Bankman-Fried investments between 2020 and late 2022 reads like something out of a different timeline. Not the timeline where he is serving twenty-five years. The one where he is on the cover of Fortune.

Before we get to the story, the numbers.

Between 2020 and late 2022, SBF and the various entities he controlled, FTX Ventures, Alameda Research, and his personal book, deployed roughly $5 billion into early-stage companies. Not tokens. Not trades. Equity. Real board seats, real cap tables.

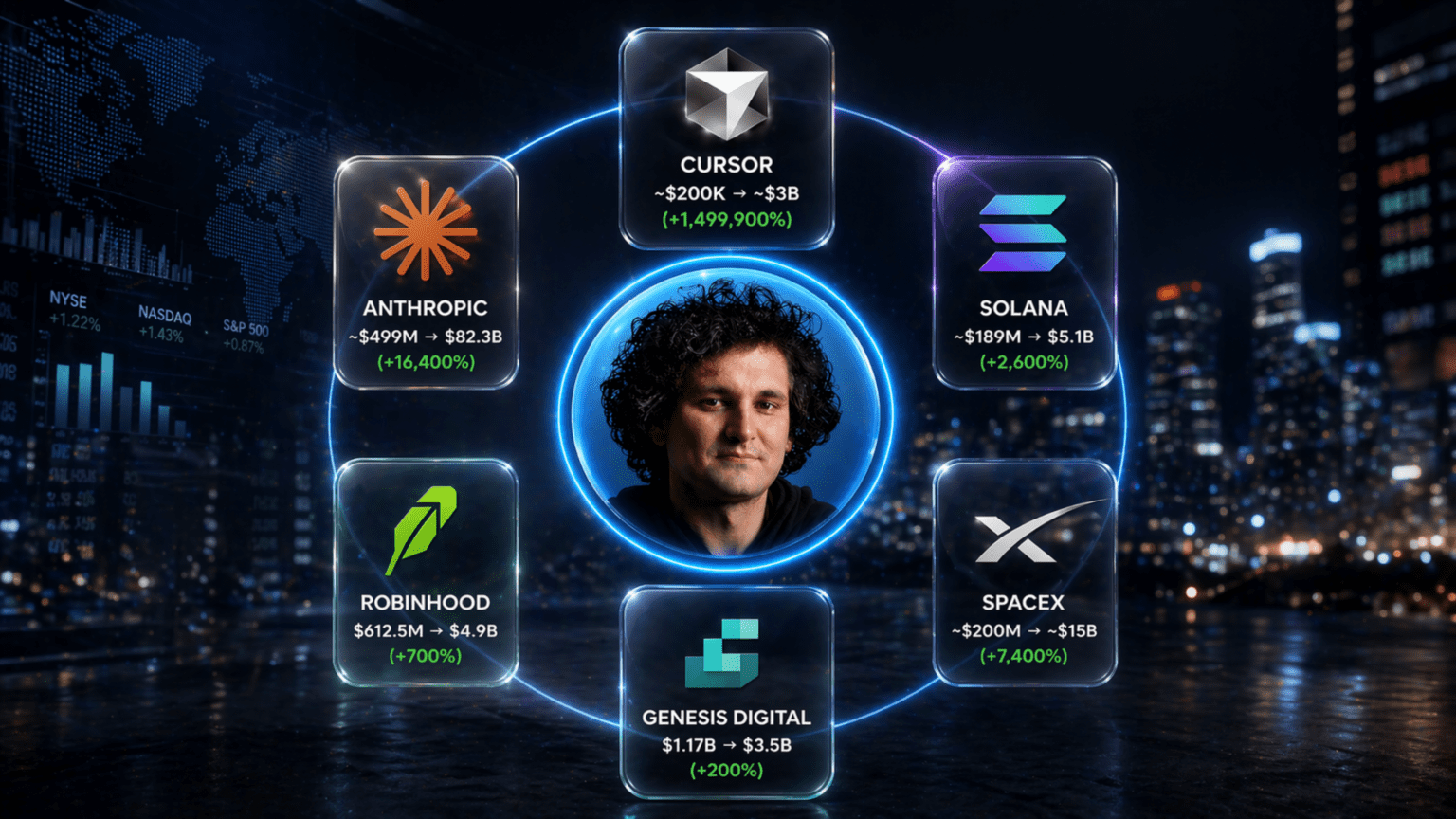

Here is a partial reconstruction of Sam Bankman-Fried investments, with mark-to-today values where the companies remain private, and latest reported valuations where they are public or marked:

Anthropic: roughly $499 million in, now worth around $6.5 billion at the $82B round valuation

SpaceX: roughly $200 million in, now worth around $15 billion at current secondary pricing

Solana: roughly $189 million in, with peaks of over $5 billion during the 2024 rally

Robinhood: $648 million in, now worth over $4.9 billion after HOOD’s run

Cursor: roughly $200 thousand in at the seed, now worth somewhere near $3 billion

Genesis Digital Assets: $1.17 billion in, now worth around $3.5 billion

And a long tail of smaller bets in stablecoins, L1 infrastructure, and AI tooling.

Add it up. Stress-test it. Haircut it for illiquidity and estate-sale discounts. You still land in a range that no functioning venture fund on earth can match for the 2020-2022 vintage.

By the most generous reading, if the Sam Bankman-Fried investments had simply been run as a legitimate venture firm and never touched a dollar of customer funds, the portfolio would be worth somewhere close to $114 billion today.

For context, Peter Thiel’s entire net worth is roughly $21 billion. Thiel took twenty-four years to build that. Sam did his in thirty-six months.

That is not a moral claim. It is just an accounting one. And it is what makes the story so difficult to tell honestly.

To understand why the portfolio is so good, you have to understand what Sam was actually doing, because the popular story gets it wrong.

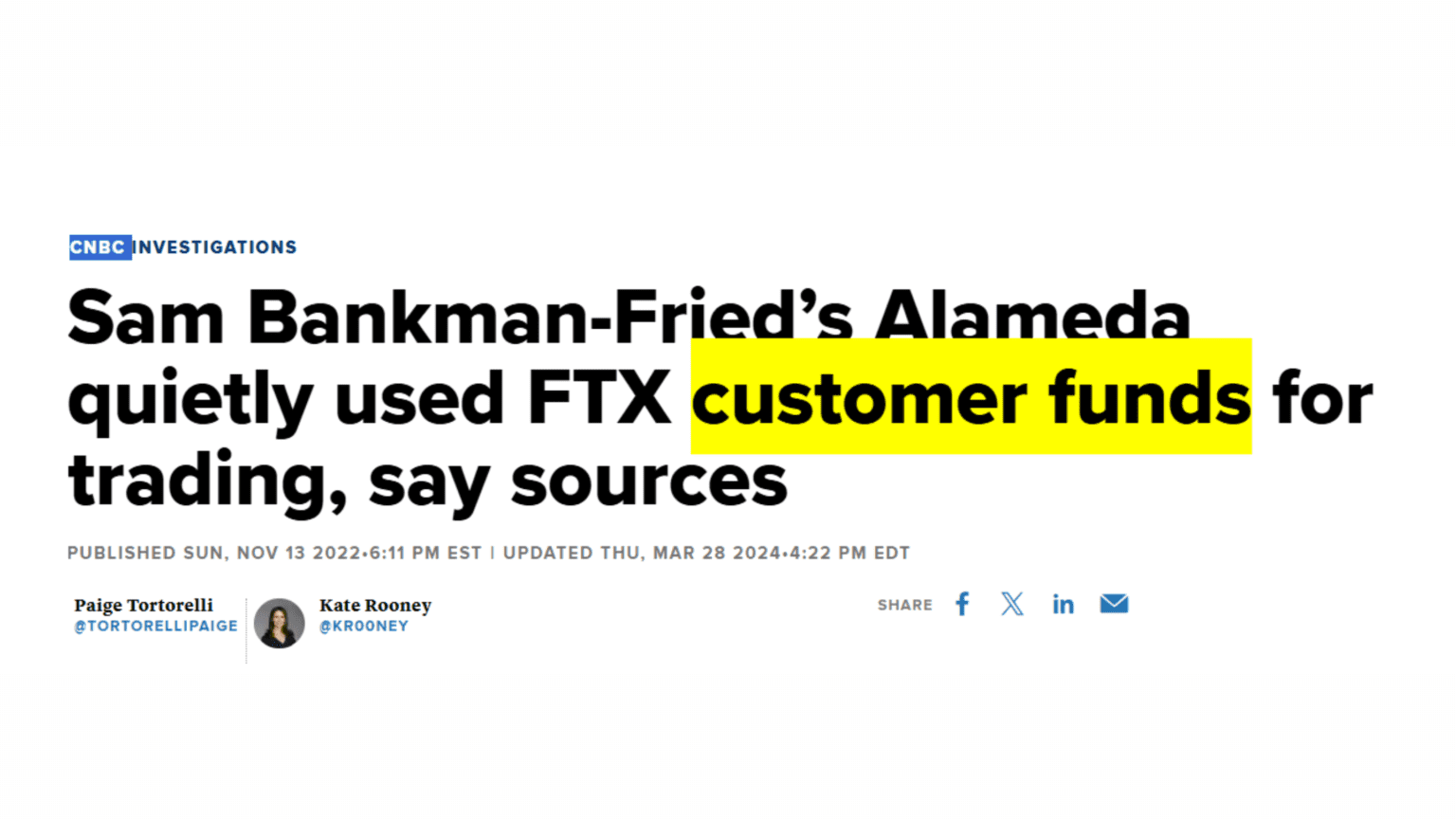

The popular story is that FTX was a crypto exchange and Alameda was a trading firm and both of them were funded by customer deposits that Sam quietly siphoned into bad bets. That story is true. It is also incomplete.

The truer story is that Sam was running a venture fund. The exchange was the cashflow engine. The trading firm was the leverage engine. The venture book was the thesis.

The thesis, stripped of all the jargon and the Effective Altruism cosplay, was this: the next decade will be owned by two technologies, artificial intelligence and crypto rails, and whoever gets early exposure to both wins everything.

In 2021, when he wrote the check to Anthropic, almost no one in crypto was thinking about AI. ChatGPT did not exist. GPT-3 was a research demo. Anthropic was a six-month-old company founded by some defectors from OpenAI who were hard to understand in meetings.

Sam wrote in $500 million.

Half a billion dollars into a company with no product, no revenue, and no clear path to having either.

When you look at the rest of Sam Bankman-Fried investments, the same pattern repeats. Cursor at the seed round, before anyone knew that AI-native IDEs would be the default. SpaceX before the Starlink cashflow inflection. Solana during the ICO when it was the fourteenth Ethereum alternative. Robinhood at the darkest post-GameStop moment.

He was early on everything that mattered. Not one thing. Everything.

This is the part that even his critics concede in private. The kid could see.

Great investors exist. Sequoia has them. Benchmark has them. Thiel’s Founders Fund has them. The difference is time.

Sequoia took sixty years to accumulate a portfolio that ever touched this range, and they had hundreds of partners doing the work. Peter Thiel’s iconic $500,000 check into Facebook is now worth something like two thousand times the original, but it took twenty years to mature. Jason Calacanis’s Uber angel check is one of the great investments of the 2010s, but he has been doing deals since 2009.

Sam did it in three years, largely alone, largely unsupervised, and while running two other companies at the same time.

This is the compression problem, and it matters because it introduces the question that most of the coverage of Sam Bankman-Fried investments has ducked.

Was the run skill, luck, or leverage?

The skill case is easy. He made the picks, wrote the checks and took the meetings. In every case where we have records of his diligence process, he was asking better questions than the people across the table.

The luck case is also easy. 2020-2022 was a once-in-a-generation entry window. AI was about to become the dominant investment theme of the decade. Crypto was minting new billionaires quarterly. You could have blindfolded yourself and thrown darts at a list of AI and crypto companies that vintage and done well.

But the leverage case is the uncomfortable one, and it is the one that explains the compression.

Thiel, Sequoia, Son. They all deployed money that belonged to them or to limited partners who had signed ten-year lockups, had to be careful and they had to be patient.

Sam was deploying customer deposits from a crypto exchange. The money was supposed to be sitting in a segregated account, ready to be withdrawn at a moment’s notice. Instead, it was being rotated into illiquid private equity positions that would take five to ten years to mature.

When you do not have to care about liquidity, you can be as early as you want. You can write checks nobody else would write, at sizes nobody else would write, can concentrate, you can spray. You can do both at once.

The compression was real. It was also fraud.

Both things are true. They have to be held at the same time to tell the story honestly.

Sam’s investment style, pieced together from founders who took meetings with him, was not what you would expect.

It was not Peter Thiel’s contrarian philosophical chess and it was not Masayoshi Son’s gut-feel megabets. It was not Jason Calacanis’s warm-intro networking.

It was something closer to the way a quant prices an option chain. He was running probability-weighted scenarios on founders in real time and writing checks as fast as his thesis would let him. If a company had a ten percent chance of becoming a hundred-billion-dollar outcome, it was worth a cheque of meaningful size, regardless of what it did today.

Cursor at $200K is the case study. At the seed, they were pitching an AI-native code editor when Copilot was barely working. Sam did not negotiate. He wrote a small cheque fast and moved on. Three years later that cheque is worth about $3 billion. The return multiple is roughly 1,500,000%.

You do not hit those multiples by being careful. You hit them by being willing to look stupid at the moment of the bet.

And you can afford to look stupid when the capital you are deploying is not really yours.

That is the second layer of the method. The famous term in venture is “concentration risk.” You are supposed to size positions so that any single failure does not kill the fund. Sam did the opposite. He concentrated because concentration did not feel risky to him. The money was replenishing every day from FTX trading fees and, when the fees were not enough, from the customer omnibus account.

A venture capitalist with unlimited refill cannot be compared to one without. The math is different. The risk tolerance is different. The speed is different.

Of course he outran them. He had a cheat code none of them had.

Here is the hardest part of the piece to write, because it forces the reader to sit with an ugly counterfactual.

What if FTX had survived 2022?

Not a thought experiment in the abstract. A concrete, specific one.

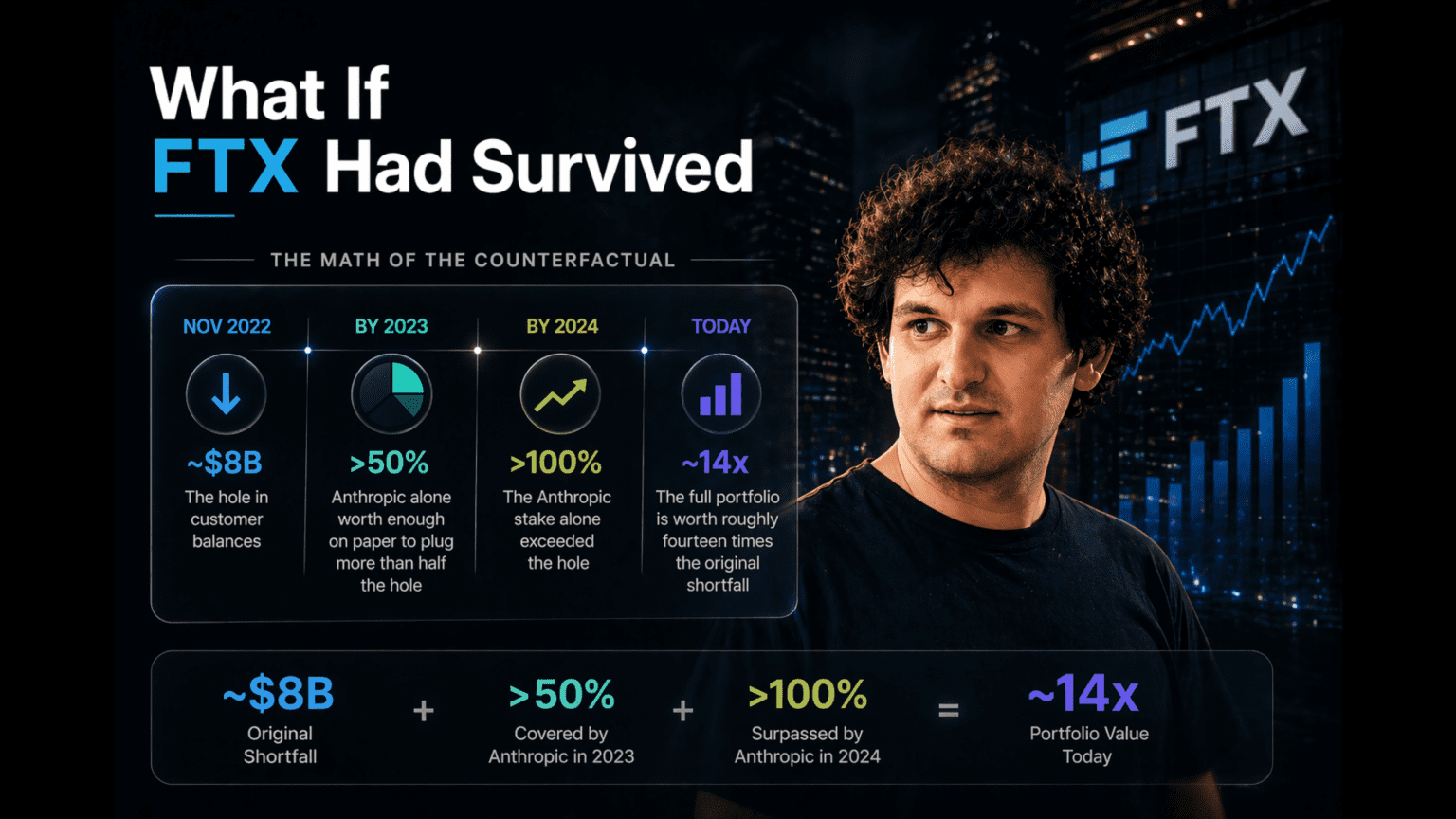

In November 2022, FTX had roughly an $8 billion hole in its customer balance sheet. Everyone has since agreed this was the fatal wound. The bank run came, the hole was exposed, the empire collapsed in ninety-six hours.

But the venture portfolio was sitting there the whole time.

At fair value. The Sam Bankman-Fried investments kept their book value even as the exchange burned.

At fair value, the Sam Bankman-Fried investments were enough to fix the hole. Anthropic alone, by 2023, was worth enough on paper to plug more than half the hole. By 2024, the Anthropic stake alone exceeded the hole. By the time of this writing, the full portfolio is worth roughly fourteen times the original shortfall.

Read that again. The venture book, if it had been allowed to mature, was large enough to make every single FTX customer whole with eleven-figure leftovers.

This is not a defense of what Sam did. The fraud was real. The betrayal of customer trust was real. The arrogance that led him to rotate segregated funds into illiquid bets was real and is, morally, unforgivable.

But the counterfactual is stark and it deserves to be stated plainly.

If FTX had held together for eighteen more months, Sam Bankman-Fried is not in a prison cell. He is on the cover of Fortune. The $8 billion hole becomes a footnote in the story of how a kid from MIT built the most aggressive venture fund in history and used a crypto exchange as his deployment rail.

The press calls him visionary. The regulators call him a pioneer. Michael Lewis’s book lands as intended. Anthropic’s eventual IPO mints him at a hundred billion and change.

He is not a criminal in that timeline. He is the best investor of his generation.

The only thing separating the two outcomes was time.

Here is the thing that finance Twitter has mostly missed, because finance Twitter does not really do moral analysis.

Sam was not a fraud who got lucky with good picks.

He was a generational investor who committed fraud because he did not believe the rules applied to his kind of conviction.

That is a different and more disturbing story. It is the story of what happens when you combine a real gift with an ideological framework, the aggressive utilitarianism of Effective Altruism, that lets you rationalize any behavior on the grounds that the expected value of your future contribution is so large.

He did not steal because he was greedy but he stole because, in his own head, the math said he should. He believed that every dollar he directed toward the Sam Bankman-Fried investments was worth more, in expected human welfare, than that dollar sitting in a customer account.

In a sense, the returns now prove he was right about the portfolio.

They also prove he was wrong about the right to make the decision in the first place.

This is the part that people find hard to accept, because it resists simple framing. He did not fail because he was stupid. He failed because he was extraordinarily skilled and believed his skill gave him moral permission.

Both readings have to sit next to each other. He is a historic investor. He is also a criminal. The trades were real. The betrayal was real. The portfolio is real. The prison sentence is real.

No one at the table gets to choose which of those sentences to forget.

So what do we actually take from the story of Sam Bankman-Fried investments?

A few things, none of them comfortable.

2020-2022 was a once-in-a-decade entry point for AI and crypto. Sam saw it and acted. The people who did not see it, or saw it and hesitated, will spend the rest of their careers explaining why they passed.

If there is one lesson the ledger teaches, it is that conviction at the right moment matters more than being right over the long run.

You cannot match Sam’s speed legitimately. Anyone who tries is either deploying someone else’s money without permission or faking the speed with marketing.

Real venture capital takes time. The compression Sam achieved was a direct function of the capital structure he was stealing from. You cannot copy the result without copying the crime.

The next SBF will not look like him. He will not run a crypto exchange, nor will not wear cargo shorts. He will build something cleaner, probably an AI-adjacent fund with a crypto treasury, and he will have all of Sam’s conviction and none of his moral blind spots.

Or, more likely, the same blind spots pointed at a different kind of hole.

Most of the people still snickering at Sam in 2026 will be worse investors than him in 2036.

The picks do not lie. The ledger does not lie. Even a decade into his sentence, the Sam Bankman-Fried investments keep compounding in the dark, and by the time he walks out of Mendota in his late fifties, he will be worth more on paper than every venture capitalist who laughed at him when he went down.

He will also still be a criminal. That part does not age either.

Back to the prison in Mendota.

It is evening. The man in the grey jumpsuit closes his browser. His fifteen minutes are up. Somewhere in California, Anthropic engineers are pushing a new model, somewhere in Texas, a SpaceX rocket is being fueled. Somewhere in Manhattan, a Cursor engineer is reviewing the commit that will ship to the next version of the best-selling developer tool in the world.

Sam owns, on paper, a piece of every one of those stories.

He also owns, permanently, the part where he stole from a million customers to pay for his seat at the table.

Both are his, both are the portfolio and both are the ledger.

The full story of Sam Bankman-Fried investments cannot be told without holding both at the same time. History will have to figure out how.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.