Hyperliquid 2026 breakdown: $5B TVL, $630M revenue, 60% perp DEX market share, HYPE tokenomics, HIP-3 permissionless markets, risks and data.

Author: Kritika Gupta

Hyperliquid 2026 is growing while most crypto trading venues fight for flat volume. In 2025, the protocol processed $2.6 trillion in derivatives volume, nearly double Coinbase’s $1.4 trillion.

Hyperliquid operates as a decentralized perpetual futures platform built on its own high-performance Layer 1 blockchain. While much of the market retrenches, Hyperliquid scales. In 2025 alone, the protocol processed approximately $2.6 trillion in notional trading volume. By comparison, Coinbase handled around $1.4 trillion during the same period.

Hyperliquid continues to outperform during broader market weakness. It does so through a combination of technological advantages, product expansion, and a tightly aligned economic model. Its custom Layer 1 delivers centralized-exchange-level speed with full on-chain settlement. Meanwhile, protocol upgrades such as HIP-3 and the upcoming HIP-4 have expanded Hyperliquid’s scope beyond crypto into real-world assets and event-based markets.

For more coverage on decentralized derivatives, perp DEX growth, and on-chain trading infrastructure, read OurCryptoTalk’s latest analysis on Hyperliquid, dYdX, GMX, Aster, and the broader shift from centralized exchanges to self-custodied markets.

Hyperliquid 2026 is a custom Layer 1 blockchain and decentralized exchange built for perpetual futures, spot trading, and on-chain financial markets. Its architecture combines HyperCore, HyperEVM, a fully on-chain order book, self-custody, and USDC collateral to deliver fast execution without relying on centralized custody. This design lets traders access exchange-like performance while keeping settlement transparent and verifiable on-chain.

Hyperliquid’s 2026 expansion is visible in the numbers. DefiLlama data shows the protocol holding $5.09 billion in TVL, generating $630.83 million in annualized revenue, and processing $178.51 billion in 30-day perpetual volume. Its 24-hour perpetual volume stands at $7.89 billion, while open interest sits near $8.91 billion, showing sustained derivatives activity rather than a short-lived spike.

Hyperliquid 2026 metrics at a glance

Hyperliquid matters in 2026 because it shows how derivatives trading is moving from centralized exchanges to high-performance on-chain venues. The shift is not just about decentralization. It is about execution quality, liquidity depth, transparency, and custody.

Hyperliquid works by combining a purpose-built trading chain, an on-chain execution engine, and an EVM-compatible app layer. Its design focuses on fast derivatives trading while preserving self-custody and transparent settlement.

HyperCore is the trading engine at the center of Hyperliquid. It supports perpetual futures, spot trading, margin management, funding payments, and liquidations. Its on-chain order book lets traders place limit and market orders in a structure that feels closer to centralized exchanges than traditional DeFi AMMs.

The key difference is settlement. On a centralized exchange, traders depend on the venue’s internal database and custody system. On Hyperliquid, execution and settlement happen on-chain, meaning trades, funding rates, and liquidations remain transparent and verifiable while users keep control of their assets.

HyperEVM expands Hyperliquid from a derivatives exchange into a broader on-chain financial platform. Because it supports EVM-compatible applications, builders can create lending markets, vaults, structured products, bridges, analytics tools, and yield strategies around Hyperliquid’s trading activity.

This matters because Hyperliquid’s long-term value does not depend only on perp volume. If builders create useful applications around its liquidity, collateral, and user base, the network can evolve into a wider DeFi ecosystem rather than remain a single trading venue.

HyperBFT is Hyperliquid’s consensus system. It supports low-latency execution, fast settlement, and high-throughput trading, which are critical for perpetual futures markets where delays can create slippage, liquidation risk, and poor execution.

The trade-off is decentralization. Hyperliquid’s relatively small validator set improves speed and coordination, but it also makes the network less decentralized than larger Layer 1s with broader validator participation. In 2026, the core question is whether traders value execution transparency, self-custody, and speed more than maximum validator distribution.

HYPE’s tokenomics tie network activity to token demand through staking, governance, buybacks, and the Assistance Fund. The model matters because Hyperliquid does not rely only on speculative demand. Instead, trading fees, market creation, validator participation, liquidity incentives, and emissions all shape how value flows through the ecosystem.

HYPE tokenomics: where value accrues

HYPE has a fixed total supply of 1 billion tokens, with roughly one-quarter of that supply currently circulating. The remaining supply matters because future emissions, ecosystem allocations, and unlock schedules can influence market structure over time. Unlike many token launches, Hyperliquid did not rely on a traditional ICO or private presale model, which reduces classic VC cliff risk but does not remove dilution risk entirely.

Hyperliquid’s value accrual loop starts with trading activity. When users trade perpetual futures or spot markets, the protocol generates fees. A large share of those fees can support HYPE buybacks, while the Assistance Fund acts as a strategic reserve for liquidity, incentives, and ecosystem stability.

The loop is simple:

More trading volume -> more protocol fees -> more buyback capacity -> lower net supply pressure -> stronger value accrual potential for HYPE

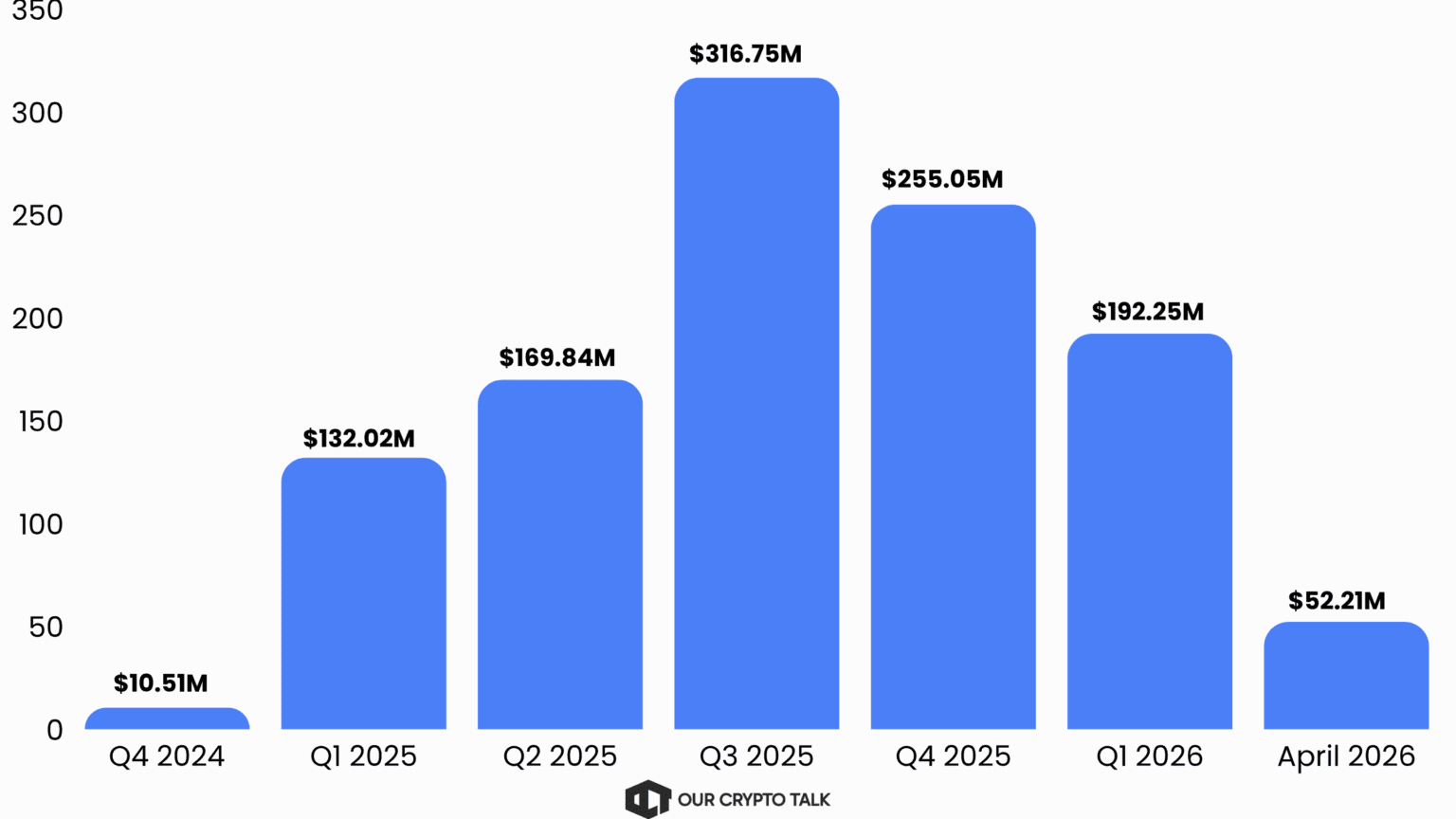

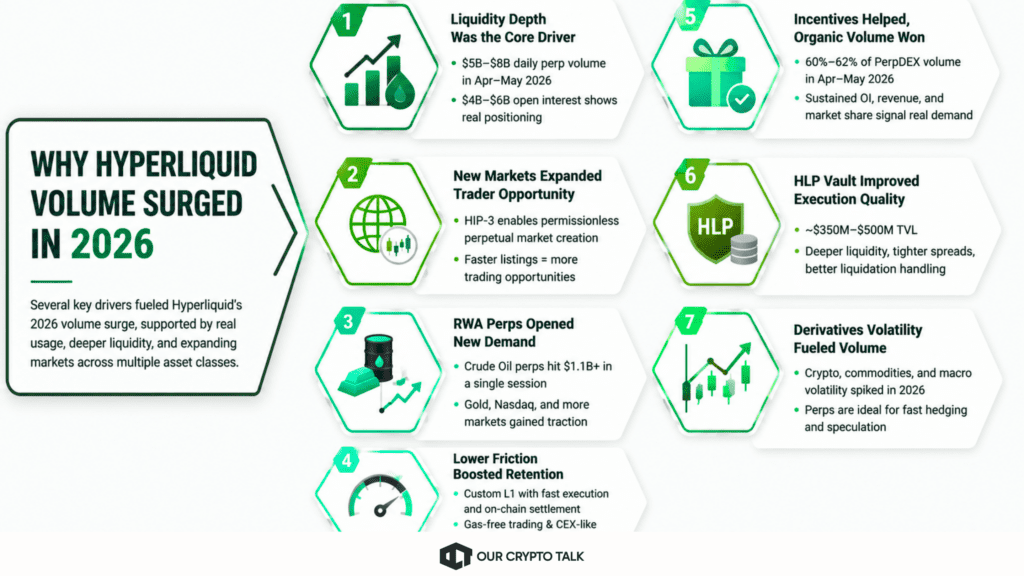

Hyperliquid 2026 volume surge came from several reinforcing drivers: deeper liquidity, faster execution, new market creation, RWA perpetuals, lower trading friction, and sustained derivatives volatility. The growth was not only incentive-led. While token mechanics and ecosystem incentives supported activity, the stronger evidence came from persistent open interest, multibillion-dollar daily perp volume, high revenue, and repeated usage across crypto, commodities, equities, and event-driven markets.

Liquidity depth was the first major driver. By April to May 2026, Hyperliquid’s daily perpetual volume regularly ranged between $5 billion and $8 billion, while open interest stayed around $4 billion to $6 billion. That combination matters because open interest shows active positioning, not just one-off trading volume.

Hyperliquid also benefited from liquidity concentration. Instead of spreading execution across multiple chains, AMM pools, and external settlement environments, the protocol runs on its own application-specific Layer 1. This concentrates order-book activity, supports tighter spreads, and improves execution quality during volatile periods. As more traders moved to the venue, deeper liquidity attracted even more flow.

Hyperliquid’s growth was not limited to BTC, ETH, and major crypto pairs. HIP-3 introduced permissionless perpetual market creation, allowing new markets to be deployed with configurable oracles, leverage limits, and fee structures. That reduced reliance on a centralized listing process and let Hyperliquid respond faster to trader demand.

This matters because derivatives volume follows opportunity. When traders want exposure to a trending asset, commodity, equity index, or macro event, the platform that lists the market fastest can capture liquidity first. HIP-3 made Hyperliquid more flexible than traditional perp venues that depend on slower listing pipelines.

Real-world asset perps added a second demand layer beyond crypto-native speculation. After HIP-3, markets tied to gold, silver, crude oil, equities, and other real-world assets started gaining traction. The draft notes that Crude Oil perpetuals exceeded $1.1 billion in trading volume in a single session, while Gold and Nasdaq perps also became active markets.

That expansion gave Hyperliquid access to traders who wanted leveraged exposure to macro assets without relying on brokers, custodial exchanges, or traditional derivatives accounts. As commodities and equities saw stronger volatility in 2026, RWA perps helped Hyperliquid capture flows that would normally sit outside crypto-only DEXs.

Hyperliquid reduced several frictions that usually hurt decentralized derivatives adoption. Its custom Layer 1 supports fast execution, on-chain settlement, and gas-free trading for users. Its order-book model also feels closer to centralized exchange trading than AMM-based DeFi interfaces.

That lower-friction experience helped attract more professional and high-volume traders. They could retain self-custody, verify execution on-chain, and still access a trading environment with deep liquidity and low-latency execution. This narrowed the gap between CEX performance and DEX transparency, which became especially important after repeated concerns around centralized custody risk.

Incentives supported Hyperliquid’s early momentum, but the 2026 data points to more durable usage. Incentive-driven volume often disappears when rewards fall. Hyperliquid, however, continued to show elevated daily volume, open interest, revenue, and market share.

By April to May 2026, the platform often captured around 60% to 62% of total decentralized perpetuals volume. That level of share suggests traders were using Hyperliquid for execution quality, liquidity depth, and available markets, not only for temporary rewards. Sustained open interest also indicates real positioning from sophisticated traders rather than pure wash-style volume.

The Hyperliquidity Provider vault, or HLP, became a major part of Hyperliquid’s market structure. HLP pools community capital into a shared market-making and liquidation backstop. The current draft places HLP at roughly $350 million to $500 million in TVL, giving the protocol a deeper liquidity layer during both normal and stressed markets.

This design supports tighter spreads, lower slippage, and more resilient liquidation handling. Traders benefit from better execution, liquidity providers earn returns tied to real trading activity, and the protocol becomes less dependent on short-term mercenary liquidity. As volumes scale, HLP helps turn liquidity depth into a repeatable advantage.

The broader 2026 market favored perpetual futures. Crypto price swings, commodity volatility, macro uncertainty, and event-driven trading all increased demand for instruments that allow fast long or short positioning without expiry. Perps naturally benefit from that environment because traders can hedge, speculate, and adjust exposure quickly.

Hyperliquid was well positioned for this backdrop. It had the liquidity depth, execution speed, self-custody model, and expanding market list needed to capture volatility-driven flows. As derivatives demand increased, the platform converted that activity into higher volume, stronger revenue, and greater relevance within the on-chain trading market.

HIP-3 and HIP-4 matter because they turn Hyperliquid from a single derivatives exchange into a market-creation layer. It lets qualified builders deploy their own perpetual futures markets on HyperCore, including markets for crypto assets, commodities, equities, and other RWAs. Hyperliquid’s official HIP-3 docs state that mainnet deployers must stake 500,000 HYPE, with the requirement expected to decline over time as infrastructure matures. HIP-4 extends the same idea into outcome-based trading, where users can trade event results through fully collateralized, expiry-based contracts similar to prediction markets.

HIP-3 and HIP-4 market creation examples

The combination of HIP-3 and HIP-4 changes the platform’s identity. Hyperliquid no longer operates as just a crypto derivatives venue. Instead, it functions as a permissionless financial platform where any asset or event can become a tradable market.

Hyperliquid’s closest competitors do not all compete on the same axis. dYdX is the closest decentralized order-book rival, GMX remains a liquidity-pool-based perp DEX, Aster competes through high leverage and aggressive fee positioning, while Coinbase represents the regulated centralized exchange benchmark. Hyperliquid’s edge comes from combining self-custody, a custom Layer 1, an on-chain order book, deep perp liquidity, and expanding market breadth through HIP-3 and HIP-4.

Hyperliquid vs dYdX, GMX, Aster and Coinbase

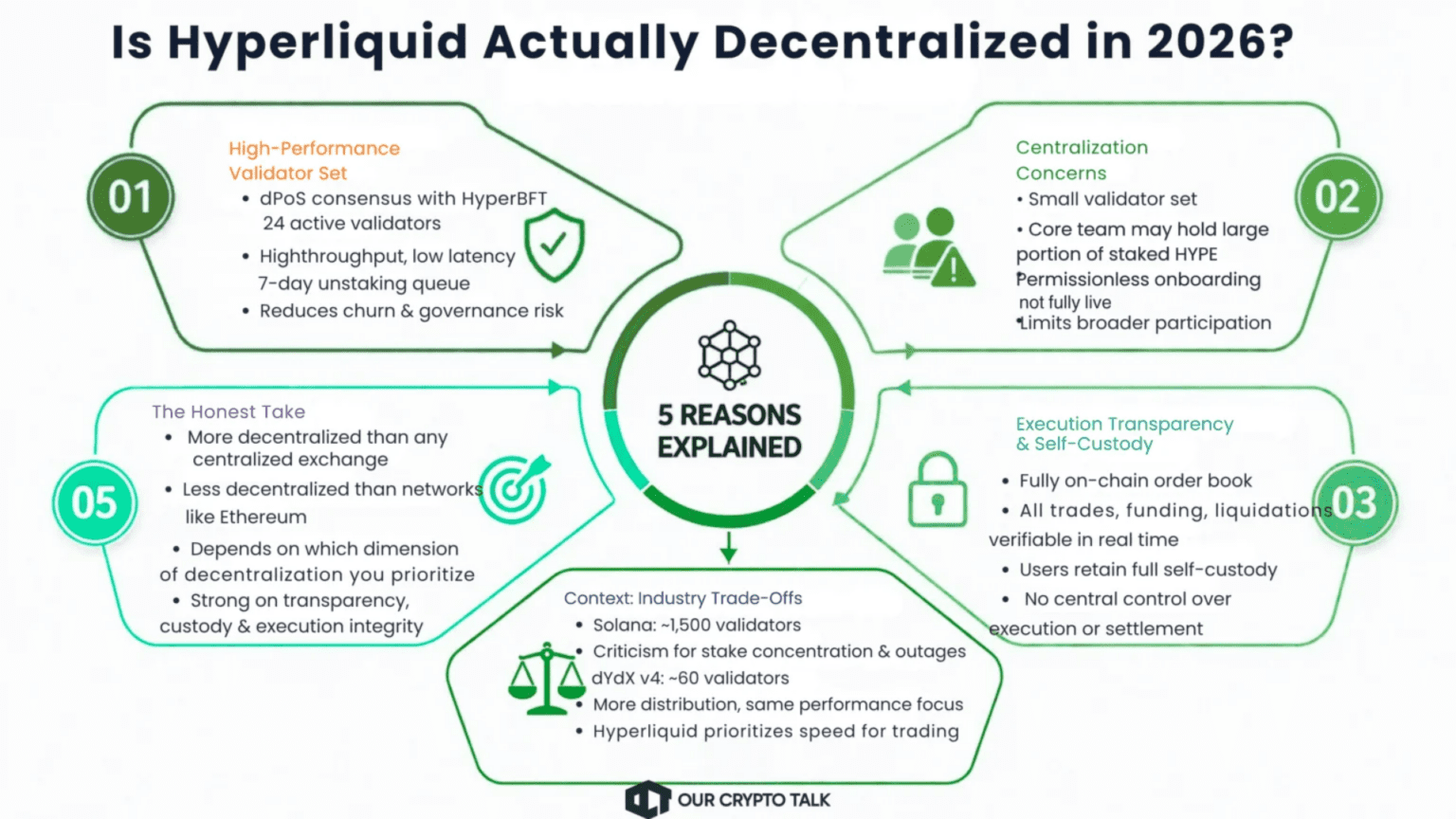

Hyperliquid 2026 is decentralized in some ways and more centralized in others. The honest answer depends on which criteria matter most: validator distribution, permissionless participation, custody, execution transparency, governance control, or sequencing risk. In 2026, Hyperliquid looks far more decentralized than a centralized exchange, but less decentralized than mature Layer 1 networks such as Ethereum and Solana.

Hyperliquid decentralization criteria in 2026

The strongest case for Hyperliquid’s decentralization comes from self-custody and execution transparency. Traders do not need to trust a centralized exchange balance sheet, and they can verify order-book activity, funding rates, liquidations, and settlement directly on-chain. That makes Hyperliquid structurally different from custodial venues such as Coinbase or Binance.

The weakest case comes from validator distribution and permissionless participation. Hyperliquid’s smaller validator set helps the network deliver low-latency trading, but it also means the chain has not reached the decentralization profile of Ethereum.

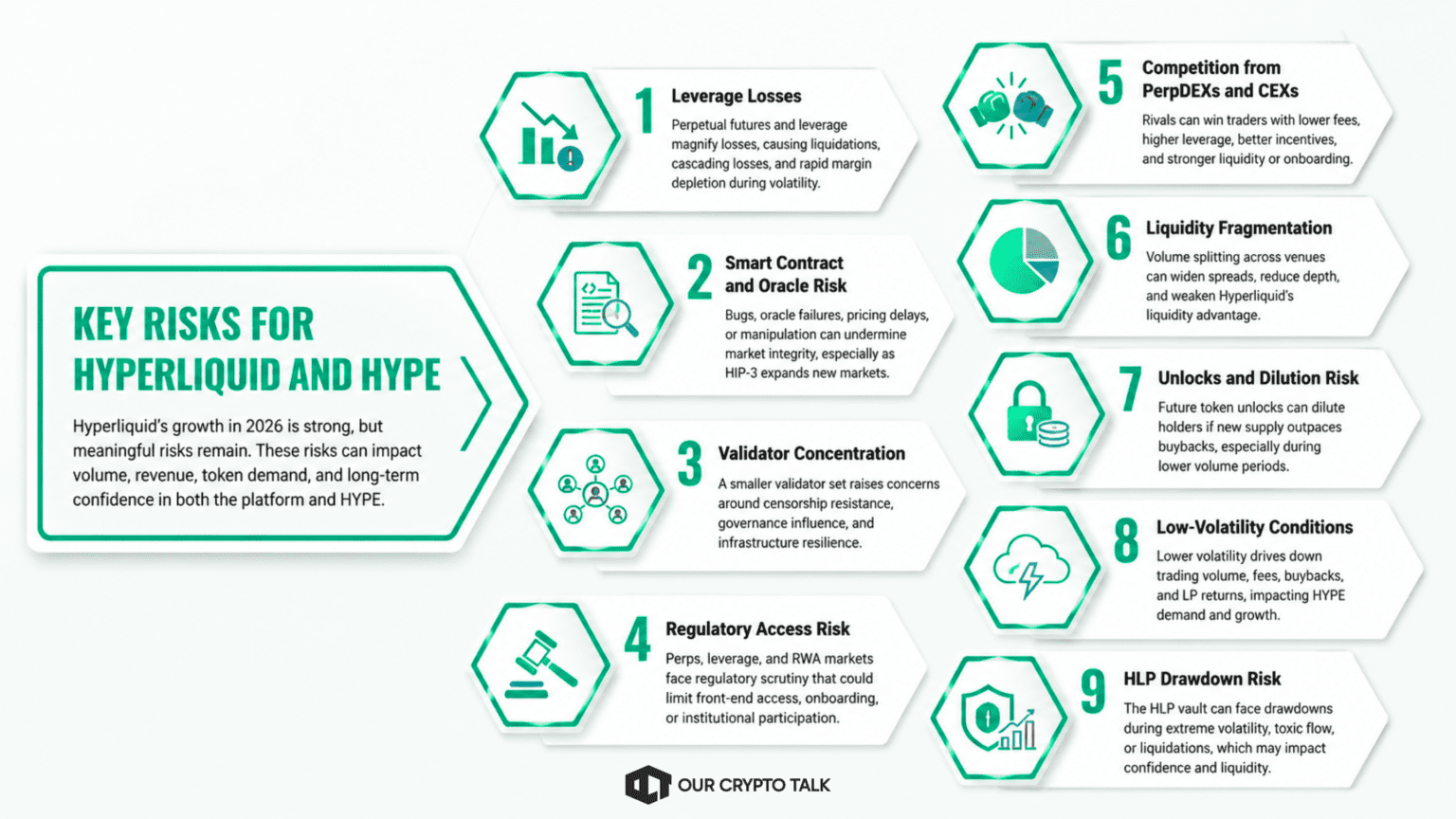

Hyperliquid 2026 growth is strong, but the platform still carries meaningful risks. These risks should appear before any HYPE price outlook because they directly affect volume, revenue, token demand, and long-term confidence. The main risks come from leverage, technical infrastructure, validator concentration, regulation, competition, liquidity fragmentation, token unlocks, low volatility, and potential HLP drawdowns.

Hyperliquid is built around perpetual futures, which means users can take leveraged long or short positions. Leverage increases capital efficiency, but it also magnifies losses. During sharp price moves, traders can face forced liquidations, cascading losses, or rapid margin depletion. This risk grows when newer users treat perp trading like spot trading.

Hyperliquid depends on reliable smart contracts, accurate oracle inputs, and secure liquidation mechanics. Any bug, oracle failure, pricing delay, or manipulation event could damage market integrity. This risk becomes more important as HIP-3 expands markets into RWAs, commodities, equities, and other assets that may require more complex data feeds.

Hyperliquid’s smaller validator set supports high-speed execution, but it also creates decentralization concerns. A concentrated validator structure can raise questions around censorship resistance, governance influence, and infrastructure resilience. Until permissionless validator participation broadens, critics can reasonably view Hyperliquid as performance-first but not maximally decentralized.

Perpetual futures, leveraged trading, and RWA-linked markets face regulatory scrutiny across major jurisdictions. Hyperliquid’s growth into commodities, equities, event markets, and prediction-style products could increase that attention. Even if the protocol remains accessible on-chain, front-end access, user onboarding, fiat rails, or institutional participation could face restrictions.

Hyperliquid competes with decentralized rivals such as dYdX, GMX, Aster, Lighter, Paradex, and edgeX, as well as centralized exchanges like Coinbase and Binance. Competitors can attack its moat through lower fees, higher leverage, stronger incentives, better onboarding, or deeper institutional relationships. If traders migrate, Hyperliquid’s fee revenue and HYPE buyback demand could weaken.

The project benefits from liquidity concentration, but that advantage can reverse if volume splits across rival venues. New perpDEXs, app-specific markets, cross-chain liquidity layers, and incentive-driven competitors may fragment order-book depth. Fragmentation can widen spreads, reduce execution quality, and weaken the liquidity flywheel that currently supports Hyperliquid’s market share.

Only a portion of HYPE’s fixed 1 billion token supply is circulating. Future emissions and unlocks can create dilution risk if new supply enters the market faster than buybacks absorb it. This risk becomes more serious during periods of lower trading volume, because weaker fees reduce the buyback mechanism that offsets token issuance.

Hyperliquid’s revenue depends heavily on trading activity. If crypto and macro volatility decline, perpetual volume can fall. Lower volume means lower fees, weaker buybacks, reduced liquidity-provider returns, and less demand for new markets. In that scenario, HYPE may behave less like a high-growth cash-flow-linked asset and more like a cyclical exchange token.

The Hyperliquidity Provider vault strengthens market depth, but it is not risk-free. HLP participates in market-making and liquidation backstop activity, which means it can face drawdowns during extreme volatility, toxic flow, oracle stress, or liquidation cascades. A major HLP loss event could reduce confidence in Hyperliquid’s liquidity layer and weaken trader trust.

Hyperliquid’s largest risks are not isolated. They are connected. High leverage increases liquidation stress. Oracle issues can worsen liquidations. HLP drawdowns can reduce liquidity. Liquidity fragmentation can weaken revenue. Lower revenue can reduce buybacks and increase dilution pressure on HYPE. That is why the key question for 2026 is not only whether Hyperliquid can grow, but whether it can maintain execution quality, liquidity depth, and risk controls as it scales.

HYPE’s outlook in 2026 should be framed through measurable protocol variables rather than fixed price targets. The token is closely tied to Hyperliquid’s trading activity, fee generation, buybacks, unlock schedule, and market share.

HYPE price outlook metrics to watch

A constructive HYPE setup depends on volume, revenue, and buybacks staying strong while unlock pressure remains manageable. If daily volume and open interest remain elevated, annualized revenue can support continued buybacks and reinforce the token’s value-accrual loop.

The weaker setup is the opposite. If volatility falls, market share slips, or liquidity fragments across competitors, fee generation can decline. Lower revenue would reduce buyback intensity just as unlocks continue to matter. In that environment, FDV becomes more important because investors would focus more closely on future supply entering circulation.

Hyperliquid’s 2026 outperformance reflects deliberate design rather than market luck. A purpose-built chain, permissionless innovation through HIP upgrades, aligned token economics, and deep liquidity form its foundation.

While competitors iterate at the application layer, It builds infrastructure. As on-chain trading converges with traditional finance, this positioning becomes increasingly valuable.

For traders, builders, and investors, Hyperliquid represents more than another DEX. It serves as a case study in how decentralized systems can outperform centralized incumbents through transparency, speed, and economic alignment.

As HIP-4 and future upgrades roll out, Hyperliquid may define the next phase of derivatives trading. In a market saturated with hype, Hyperliquid delivers measurable execution and sustained volume.

This article is for informational purposes only and does not constitute financial advice. Crypto assets and derivatives carry risk, including possible loss of capital. Always do your own research before making investment decisions.

Hyperliquid’s 2026 outperformance reflects deliberate design rather than market luck. A purpose-built chain, permissionless innovation through HIP upgrades, aligned token economics, and deep liquidity form its foundation.

While competitors iterate at the application layer, Hyperliquid builds infrastructure. As on-chain trading converges with traditional finance, this positioning becomes increasingly valuable.

For traders, builders, and investors, Hyperliquid represents more than another DEX. It serves as a case study in how decentralized systems can outperform centralized incumbents through transparency, speed, and economic alignment.

As HIP-4 and future upgrades roll out, Hyperliquid may define the next phase of derivatives trading. In a market saturated with hype, Hyperliquid delivers measurable execution and sustained volume.