DeFi passive income 2026 guide for beginners: learn lending, staking, APY risks, and how to earn yield safely with your first $100.

Author: Kritika Gupta

The average US savings account pays 0.45% APY. Stablecoin lending on Aave pays 3–8%. Both are denominated in dollars. One requires a bank. The other requires a wallet. DeFi passive income 2026 has become one of the most practical ways for crypto holders to earn yield on idle assets through lending, staking, and liquidity strategies. Unlike earlier market cycles, today’s DeFi landscape offers more mature protocols, clearer regulation, and safer entry points for beginners. This guide explains the safest ways to start, the real risks involved, and how to put your first $100 to work step by step. By the end, you will understand how DeFi passive income 2026 works and which strategy best fits your risk level.

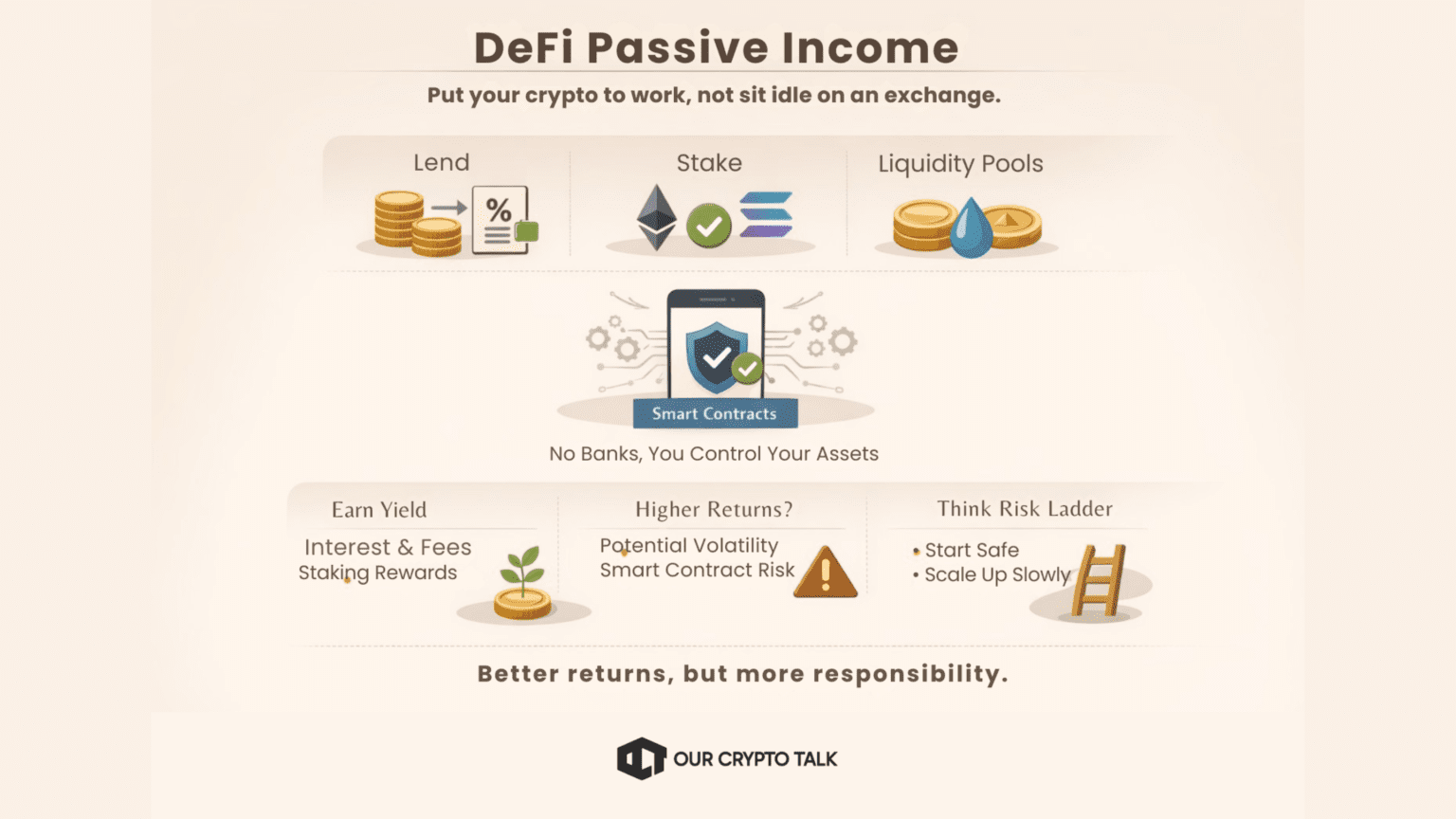

The simplest way to think about DeFi passive income 2026 is this: instead of letting your crypto sit idle on an exchange, you put it to work inside decentralised protocols that generate yield. If you already hold crypto on an exchange and want to do more with it, DeFi gives you a way to put those assets to work. Instead of leaving coins idle, you can lend them, stake them, or use them in liquidity pools to earn yield. Smart contracts handle the process instead of a bank.

That is the basic appeal. A typical savings account in the US still pays very little, while stablecoin lending in DeFi can often pay more. The tradeoff is simple: banks feel familiar, but DeFi gives you direct control. You hold the assets in your own wallet, and you interact with protocols yourself.

The yield comes from real activity inside these protocols. Borrowers pay interest. Traders pay swap fees. Blockchains reward people who stake assets and help secure the network. Some protocols also add token incentives, although those tend to come with more risk.

That said, not all DeFi yield works the same way. Some strategies feel closer to a high-yield savings account. Others expose you to volatility, smart-contract bugs, or liquidity risk. That is why it helps to think in terms of a risk ladder instead of chasing the highest number on the screen.

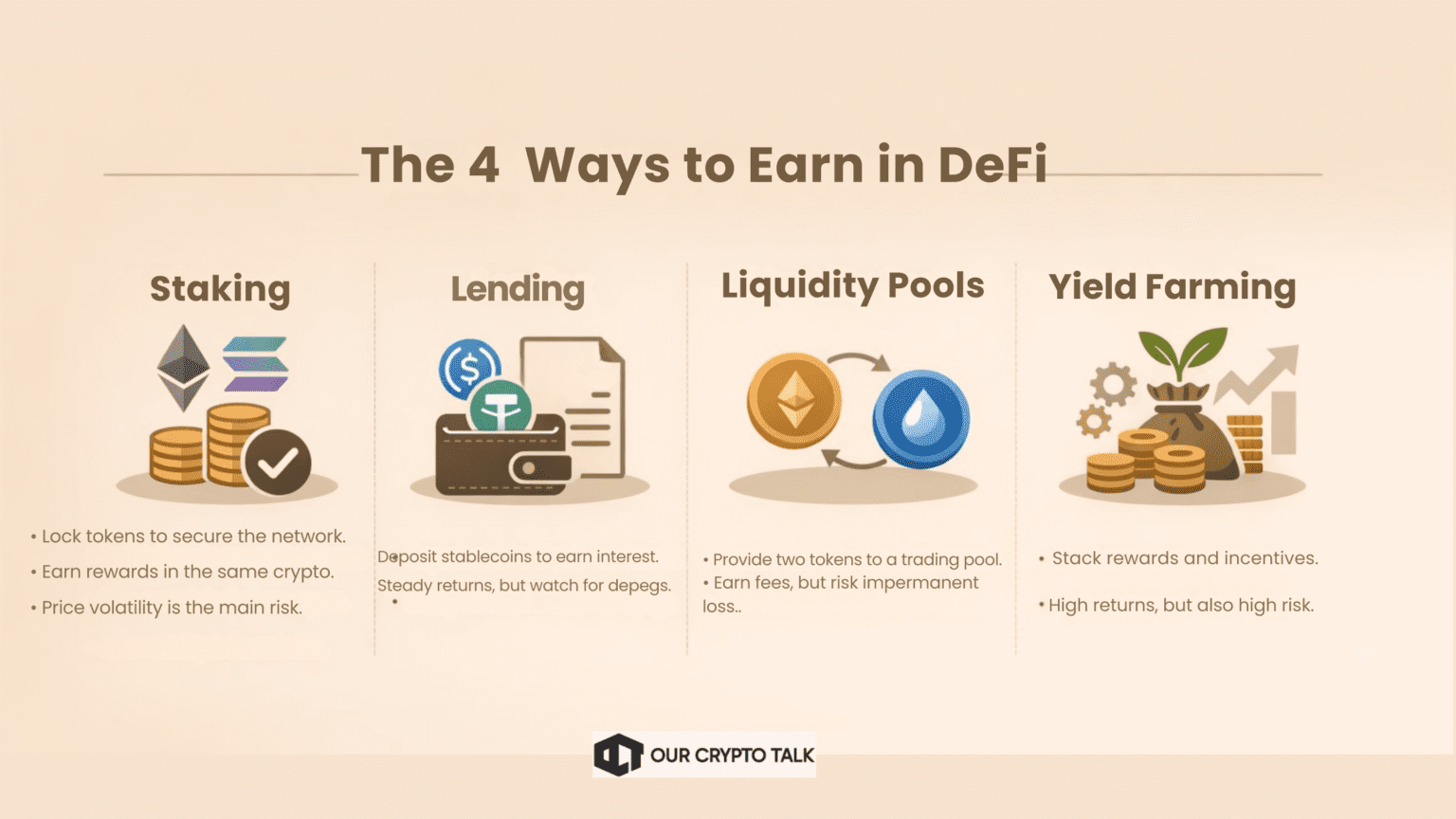

Staking means locking or delegating a blockchain’s native token to help secure the network. In return, the network pays rewards in that same asset. This works well if you already want long-term exposure to ETH or SOL. The risk is that your token price can fall while you earn yield, so a nice APY does not protect you from market drawdowns.

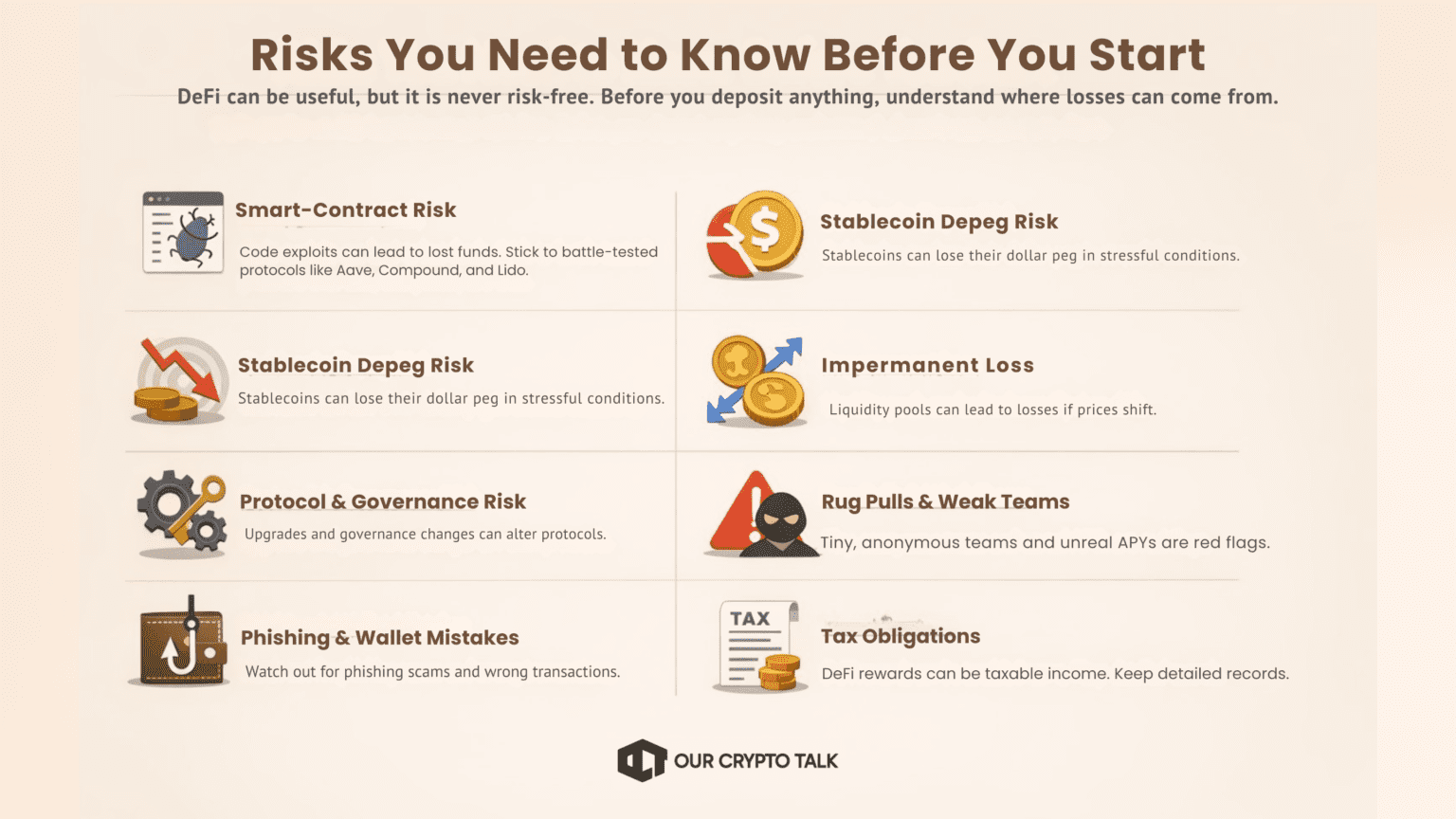

Lending is the easiest place for most beginners to start. You deposit assets into a lending protocol, and borrowers pay interest to access those funds. Stablecoin lending is especially popular because your balance stays in a dollar-pegged asset like USDC or USDT. The main risks are smart-contract risk and stablecoin depegs, but you avoid the direct price swings that come with staking volatile assets.

Liquidity pools let you deposit two assets into a decentralized exchange so traders can swap against that pool. You earn part of the trading fees, and sometimes extra incentives too. The catch is impermanent loss. If one asset moves sharply against the other, your position can underperform simply holding the tokens in your wallet.

Yield farming sits at the far end of the spectrum. This is the highest-risk way to earn DeFi passive income 2026. It usually stacks multiple forms of yield together, such as LP fees, token rewards, and auto-compounding vaults. The upside can look attractive, but so can the downside. These strategies often involve newer protocols, more moving parts, and higher risk of losses.

Relative positioning across leading DeFi yield protocols in 2026

This is the part that matters most.

A lot of beginners make the same mistake. They open a yield dashboard, sort by highest APY, and assume bigger numbers mean better opportunities. Usually, it is the opposite. Higher APY often means higher risk, lower liquidity, or rewards that can disappear fast.

The smarter approach is to start with the safest rung, learn how the flow works, and move up only if it still makes sense for your goals. That way, you build confidence without taking unnecessary risk on day one.APY figures are approximate and fluctuate. Check the protocol’s app for current rates.

Relative positioning across DeFi yield strategies in 2026

This is where I would tell almost any beginner to start.

You deposit a stablecoin like USDC into a lending protocol such as Aave, Compound, or Morpho. Borrowers take over-collateralized loans against crypto, and the protocol passes part of the interest back to you. As of March 2026, stablecoin lending often pays around 3–8% APY, depending on the chain, the asset, and how much borrowing demand exists.

What makes this a strong first step is that your balance stays in a dollar-pegged asset. You are not depending on ETH or SOL going up to make the strategy work. You are just earning yield on an asset that is meant to stay close to one dollar.

Still, things can go wrong. Smart contracts can have bugs. Stablecoins can depeg. Rates can also fall when demand drops. Those risks are real, but on established protocols and major stablecoins, this remains the cleanest entry point for most people.

Staking makes sense once you are comfortable using a wallet and you already want to hold the asset anyway.

When you stake ETH or SOL, you help secure the network and earn rewards in the same token. Liquid staking platforms like Lido and Rocket Pool make the process easier because you do not need to run your own validator, and you often receive a liquid token in return.

The catch is obvious. If ETH drops 25%, your staked ETH drops 25% too. The yield helps, but it does not offset a big market move. There is also platform risk if you use a liquid staking protocol rather than native staking.

So this rung works best for people who already believe in the long-term value of the asset. If your priority is capital stability, stablecoin lending is still the safer first move.

Liquidity pools can pay more, but they are where many people start misunderstanding risk.

You deposit two assets into a pool on a decentralized exchange like Uniswap, Curve, or Aerodrome. Traders use that pool to swap between assets, and you earn a share of the fees. On paper, this can look great. In practice, the return depends heavily on what the assets do after you deposit.

The big issue is impermanent loss. If one token runs much harder than the other, the pool rebalances automatically, and you can end up with less of the outperforming asset. That means your position may earn fees and still underperform simply holding the tokens in your wallet.

This does not mean LPs are bad. It just means you need to know what can go wrong before you chase the APY. Stablecoin pools reduce that risk, while volatile pairs increase it.

This is the rung most beginners should leave alone at first.

Yield farming usually combines several moving parts. You might deposit into an LP, earn swap fees, receive token emissions, and then auto-compound those rewards through another protocol. That stack can produce high APYs, at least for a while.

The problem is that every extra layer adds risk. Reward tokens can dump. Vault strategies can break. Protocols can lose liquidity. Admin keys, governance decisions, or outright scams can hurt users fast. If the yield looks unusually high, assume the risk is unusually high too.

Experienced users can use this rung carefully with small allocations. Beginners do not need it to get started.

This can be explained by using the example of Aave. The goal here is not to make a fortune. The goal is to complete one clean deposit, see the interest start accruing, and understand how DeFi actually feels when you use it.

Log in to the exchange where you already hold crypto. Buy about $100 of USDC. If you already hold USDT, BTC, or ETH, you can convert a small amount into USDC instead.

USDC is a good first asset because it removes direct token price volatility from the experiment. Your balance should stay near one dollar per coin, so you are learning the process without adding market swings on top.

Install MetaMask or Rabby if you do not already have one. MetaMask is the default choice for most beginners. Rabby has a cleaner interface and better transaction previews, which some people prefer.

Set up the wallet carefully. Write down your seed phrase offline and store it safely. Do not save it in screenshots, notes apps, or email drafts. Then make sure you also have a small amount of ETH for gas fees.

Go back to your exchange and choose Withdraw for USDC. When the exchange asks which network you want to use, choose Base or Arbitrum if it supports direct withdrawal there.

This step matters. If you withdraw USDC on the wrong network, you can create extra work or even lose access to funds until you sort it out. Double-check the network before you confirm. For a first deposit, Base and Arbitrum are the easiest places to start because gas fees stay very low.

In your browser, go to https://app.aave.com.

Check the URL carefully. Bookmark it. Do not use random links from social media or search ads. A lot of DeFi losses come from phishing, not from the protocol itself.

On Aave, click Connect Wallet in the top corner. Choose MetaMask or Rabby, depending on what you installed.

Approve the connection in your wallet popup. Then switch the app to the Base or Arbitrum market if it is not already there. You want to be in the same network where your USDC sits.

On the dashboard, scroll to USDC. Click Supply.

Enter the amount you want to deposit, such as 100 USDC. Aave will first ask for a token approval. That approval gives the protocol permission to access that specific token from your wallet.

Your wallet will open a transaction window. Review it, then click Confirm.

Wait for that transaction to finish. On low-fee chains like Base or Arbitrum, this usually takes a short time and costs very little.

After the approval clears, Aave will prompt you to complete the supply itself. Click Supply again if needed, then confirm the second transaction in your wallet.

This second transaction is the one that actually moves your USDC into Aave’s lending market.

Once the transaction confirms, go back to the dashboard. You should now see your supplied balance, the live APY range, and the interest starting to accrue.

That is the moment most people stop seeing DeFi as abstract. You deposited from your own wallet into a live protocol, and now your money is working.

At 5% APY, $100 earns roughly $5 per year, or about $0.42 per month. The amount is small, but the learning is the point. Scale up once comfortable.

Before you close the tab, click into your USDC position and look for the Withdraw button. You do not need to withdraw now. Just make sure you know where it is.

That matters because part of feeling comfortable in DeFi is knowing how to get out, not just how to get in.

Estimated costs for a beginner’s first DeFi deposit flow

DeFi can be useful, but it is never risk-free. Before you deposit anything, understand where losses can come from.

The goal of DeFi passive income 2026 is not to chase the highest yield on day one. The biggest mistake beginners make is trying to optimize too early. You do not need the highest yield on the first day. You need one safe, successful transaction that teaches you how the system works.

That is why I like stablecoin lending as a first move. It is simple, relatively easy to understand, and honest about what it does. You deposit a dollar-pegged asset, earn a variable yield, and keep full visibility into the position.

Once you have done that, the rest of DeFi gets much less intimidating. Then you can decide whether staking fits your goals, whether liquidity pools are worth learning, or whether advanced farming is more trouble than it is worth.

This is educational content, not financial advice. DeFi involves real financial risk. Never invest more than you can afford to lose.