Author: Tanishq Bodh

The March 2026 CoinDCX saga was not a hack. It was not insider fraud either. Instead, it was brand impersonation at its absolute worst. As a result, two of India’s most prominent crypto founders spent 72 hours in police custody over a crime they did not commit. Here is exactly what happened, why the CoinDCX founders faced arrest, and what the ₹100 crore Digital Suraksha Network means for Indian crypto users.

Before diving into the March 2026 saga, it is worth understanding why this incident sent shockwaves through Indian crypto. CoinDCX is not a fringe exchange. On the contrary, it is one of the largest cryptocurrency platforms in India.

IIT alumni Sumit Gupta and Neeraj Khandelwal founded CoinDCX in 2018. The exchange quickly grew into a household name among Indian retail crypto investors. Moreover, the platform earned unicorn status and secured backing from global players including Coinbase. By 2026, CoinDCX served millions of users across India. Many of them came from Tier-2 and Tier-3 cities and viewed crypto as both an investment vehicle and an inflation hedge.

Notably, the company had already faced a legitimate security crisis in July 2025. Hackers stole approximately $44.2 million from an internal operational liquidity account through a sophisticated breach. However, no user funds took a hit. CoinDCX covered the entire loss from its own treasury and launched a recovery bounty. That was a genuine hack. The March 2026 CoinDCX arrest saga, however, was something entirely different. This time, criminals stole the brand, not the money.

The story begins in mid-2025. Ashish Brijkishor Singh, a 42-year-old insurance advisor from Mumbra, Thane, received messages through WhatsApp and Telegram. Individuals claiming to represent CoinDCX contacted him directly. They offered two irresistible propositions: monthly returns of 10 to 12% on crypto investments, and a chance to become a CoinDCX franchisee for Maharashtra.

Over the next seven months, from August 2025 to February 2026, Singh and two associates transferred a total of ₹71.6 lakh. They made some payments in cash and others through bank transfers to third-party accounts. Meanwhile, the scammers provided fake promotional material and forged documents bearing the CoinDCX logo. They also directed victims to a counterfeit website called coindcx.pro.

Importantly, not a single rupee ever touched CoinDCX’s real platform or wallets. The entire operation was a textbook case of brand impersonation. As a matter of fact, this is one of the fastest-growing threats in India’s digital economy.

Unfortunately, this method is painfully common. Fraudsters clone trusted brands and create near-identical websites. These sites often differ by just a single character or use extensions like .pro, .io, or country-code domains. In addition, scammers exploit the fear of missing out around crypto returns. CoinDCX had been sounding the alarm for years. Between April 2024 and January 2026, the exchange reported more than 1,212 fake websites mimicking coindcx.com to authorities including CERT-In. Yet the problem keeps growing because takedowns move slowly and new clones pop up overnight.

So why do these scams work so well in India? The answer is straightforward. High returns sound plausible during a bull market. Trusted brand names lower people’s guard. Furthermore, police often struggle with the borderless, digital nature of the evidence. As a result, Singh believed he was dealing with the real company. That belief held right up until the promised returns never materialized and his contacts vanished.

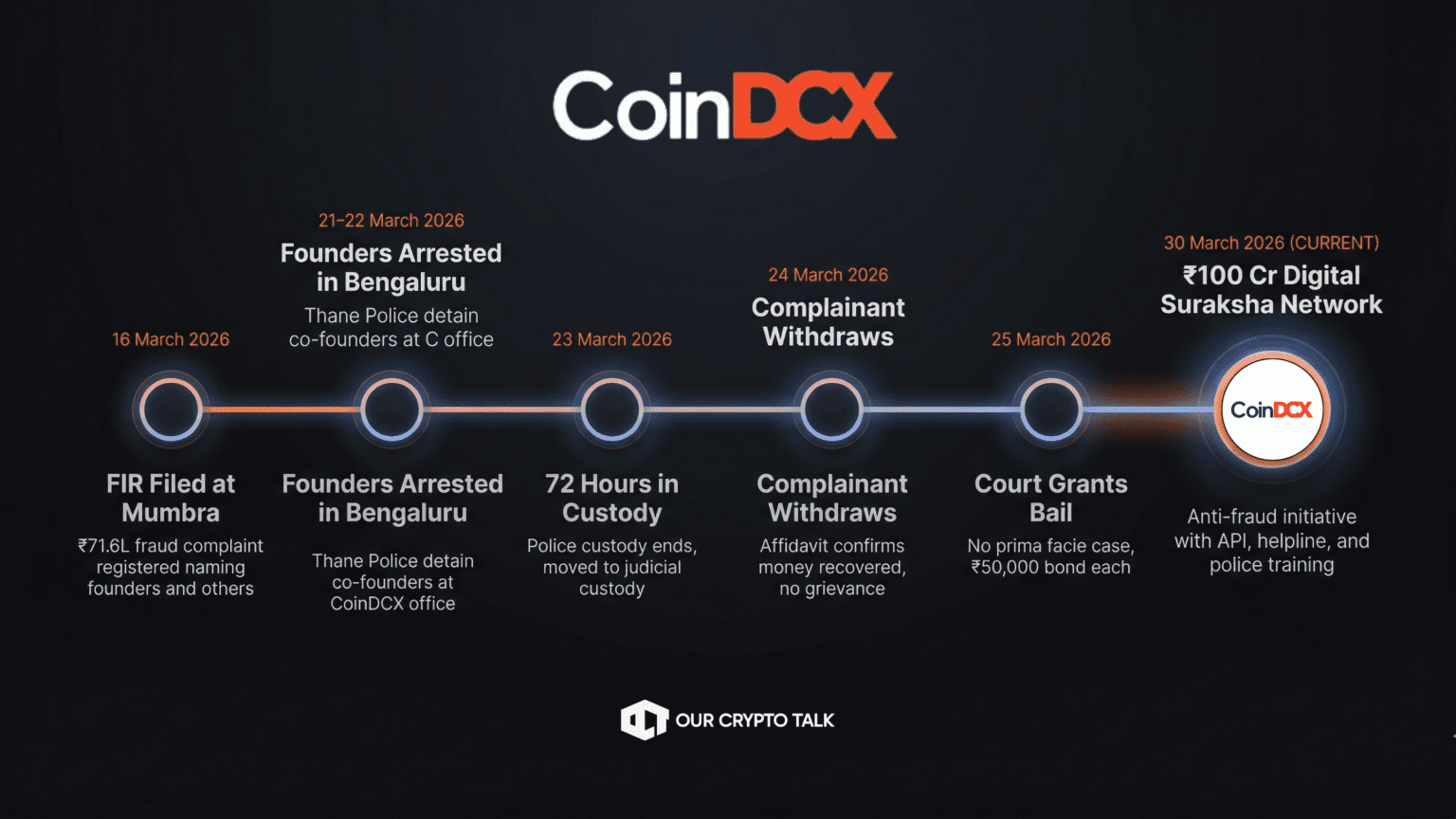

On 16 March 2026, Mumbra police station registered an FIR. The complaint named Sumit Gupta, Neeraj Khandelwal, and four others under sections of the Bharatiya Nyaya Sanhita. The charges included cheating, criminal breach of trust, and fraud. Five days later, a police team from Thane flew to Bengaluru. They detained the CoinDCX founders at their office and brought them back to Maharashtra.

Initially, officers questioned the founders at Bellandur Police Station in Bengaluru. After that, they remanded them to police custody until 23 March, followed by judicial custody. For 72 hours, two of India’s most recognized crypto entrepreneurs sat in custody more than 1,000 kilometres from home. All of this happened over a fraud they had nothing to do with.

In response, CoinDCX moved quickly. The company issued strong public statements on X calling the FIR “false.” It described the situation as a “conspiracy by impersonators posing as founders of CoinDCX.” Additionally, it emphasized that no transactions had occurred on its actual platform. CoinDCX also pointed to a 2024 Delhi High Court order it had already obtained. That order restrained unknown persons from misusing its brand name and logo.

Meanwhile, public reaction was mixed. Some crypto users expressed outrage over what they saw as poor due diligence by police. Others, however, defended the founders and cited the well-documented pattern of brand-jacking in India’s fintech space.

The case fell apart almost as quickly as it had escalated. On 24 March, the complainant appeared before Judicial Magistrate Nilesh Rathod. Ashish Singh filed an affidavit confirming that he had recovered the full ₹71.6 lakh from one of the actual accused, a man named Akash Rana. He also stated that he had “no grievance” against the CoinDCX founders. Moreover, he admitted he had never met Gupta or Khandelwal in person and never interacted with the real CoinDCX platform. The fake website had duped him entirely.

On top of that, the court noted that the CoinDCX founders were not present at the location where the fraudulent transactions took place. The investigating officer did not oppose bail either. Consequently, Magistrate Rathod granted bail on personal recognizance bonds of ₹50,000 each. He ruled explicitly that “no prima facie case” existed against them. The founders also secured transit anticipatory bail from a Bengaluru court the same day.

Within hours, the CoinDCX legal team began framing the episode differently. Rather than treating it as a personal defeat, they positioned it as a systemic failure. In their view, the incident exposed deeper cracks in how India handles fraud cases involving digital platforms.

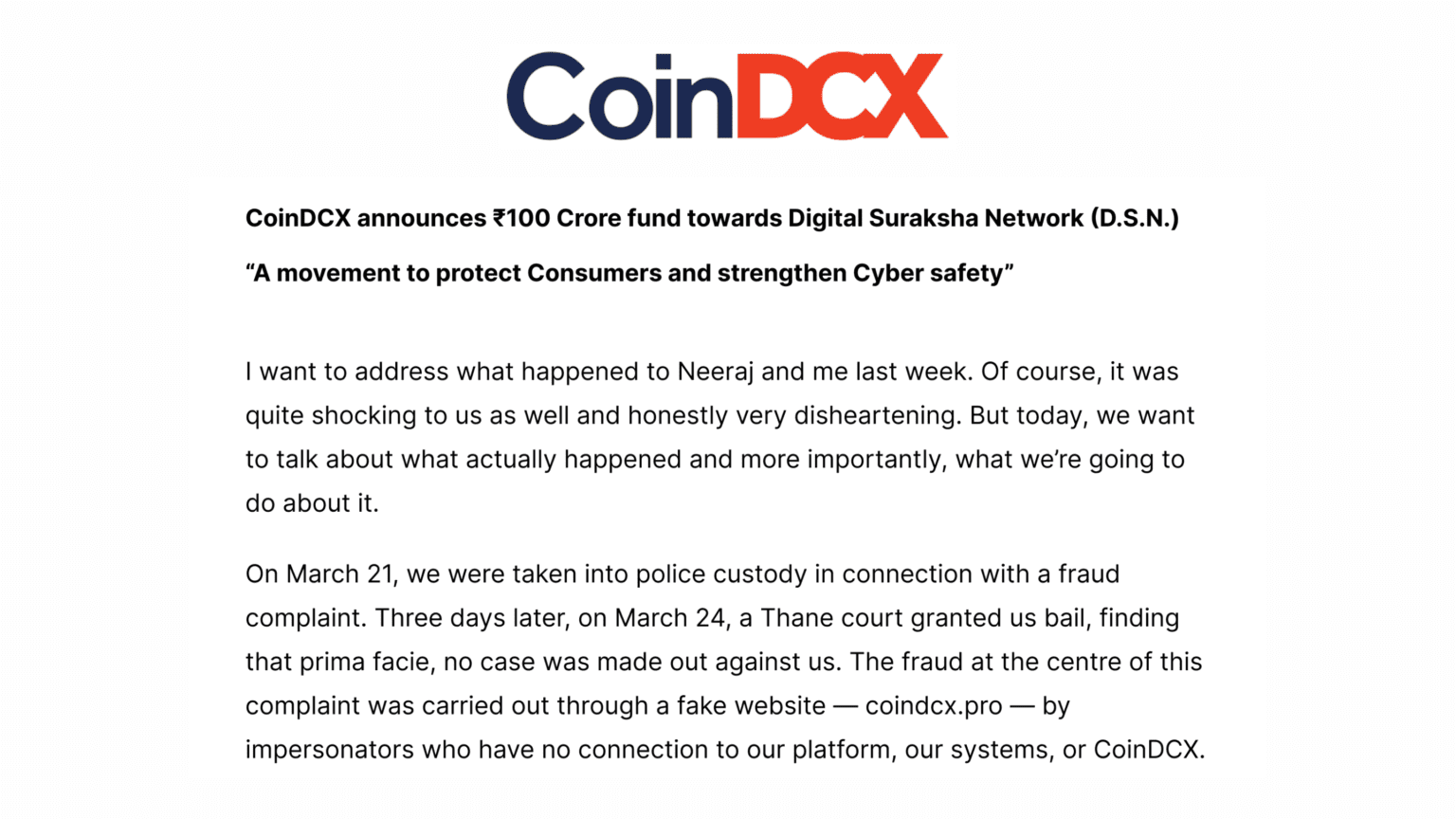

Most companies would have gone quiet after an ordeal like this. CoinDCX, however, did the opposite. Just six days after their release, on 30 March, one of Coin DCX founders CEO Sumit Gupta broke his silence in a virtual press briefing. He announced the Digital Suraksha Network (D.S.N.). CoinDCX committed ₹100 crore (roughly $11-12 million) to fund the initiative over the next three to five years.

Gupta described the arrest as “deeply unsettling.” He also called it “a wake-up call” that exposed structural gaps in India’s digital security ecosystem. Above all, he was direct about the scope of the problem: “I never imagined that building one of India’s leading crypto platforms would lead to me being arrested over a scam I had no part in.”

Importantly, the Digital Suraksha Network is not a CoinDCX-only product. Instead, it is designed as an ecosystem-wide initiative. It rests on four pillars.

At the core of the D.S.N. sits an open API. Any bank, fintech, crypto platform, or digital lender can plug into it. The API will provide real-time access to CoinDCX’s database of over 1,200 flagged fraudulent websites. In addition, it will enable cross-platform fraud signal sharing. Gupta described it as “a shared immune system for India’s digital finance ecosystem.” He also invited every exchange and fintech in India to contribute data.

CoinDCX will also launch a free, round-the-clock WhatsApp helpline. This service will be open to every Indian citizen, not just CoinDCX users. Anyone can forward suspicious links, messages, or offers for instant verification before making a transaction.

Under the banner “Caution Before Transaction,” the D.S.N. will fund educational content and media partnerships. It will also run programs in schools and colleges. The goal is to build awareness about crypto scams and brand impersonation across India.

Finally, the initiative will invest in workshops for cybercrime units. It will also improve digital evidence handling protocols and speed up coordination with CERT-In and other regulators. This pillar directly addresses one of the root causes behind the CoinDCX founders’ arrest. In many cases, police forces lack the forensic tools or training to quickly tell a legitimate company apart from its impersonators.

Gupta was blunt about the stakes: “No single company can solve this. Fraud networks are sophisticated, cross-border, and evolving daily. We are putting ₹100 crore on the table because the ecosystem cannot afford to wait.”

The CoinDCX arrest did not happen in a vacuum. Rather, it is a symptom of a much larger epidemic sweeping through India’s digital economy.

According to Ministry of Home Affairs data from February 2026, India recorded approximately 28.15 lakh cybercrime complaints in 2025. That marks a 24% spike over the previous year. Total financial losses stood at a staggering ₹22,495 crore. Specifically, investment-related frauds accounted for roughly 76% of the monetary damage. These include fake crypto schemes, trading apps, and Ponzi setups.

Perhaps the most alarming statistic is the conversion rate. Of the 28 lakh complaints filed, only 55,484 became FIRs. That translates to a rate of less than 2%. As a result, the gap between complaints and actual investigations gives scammers near impunity.

Separately, an ORF/McAfee analysis from 2025 found something equally disturbing. Around 47% of Indian adults have either experienced or know someone who fell victim to an AI voice-cloning or deepfake scam. That figure is reportedly nearly double the global average. Of those victims, 83% suffered monetary loss.

In addition, impersonation scams targeting established brands have surged alongside growing crypto adoption. This is especially true in Tier-2 and Tier-3 cities. Sophisticated actors now use AI to generate deepfake videos, clone websites, and automate WhatsApp campaigns at scale. Simply put, the tools available to scammers have evolved far faster than the infrastructure designed to stop them.

It is also worth noting that the March 2026 arrest was not CoinDCX’s only recent challenge. In fact, the episode came on the heels of several other setbacks that had already put the company under pressure.

For instance, in November 2025, the Enforcement Directorate’s Hyderabad zonal office seized ₹8.46 crore across 92 bank accounts. Some of those accounts had links to CoinDCX and a few crypto wallets. The ED launched this action as part of a money laundering probe into a nationwide cyber fraud racket. While CoinDCX was not the primary target, the association still added to the perception of regulatory heat around the exchange.

On top of that, 2025 saw multiple senior exits from CoinDCX. The company lost its Chief Technology Officer, Vice President and Head of Legal, Chief Human Resources Officer, and Senior Vice President and Head of Information Security. Together with the July 2025 hack and the March 2026 arrest, these departures paint a picture of a company navigating simultaneous storms on multiple fronts.

On the positive side, however, the Competition Commission of India approved Coinbase’s minority stake in CoinDCX parent DCX Global in December 2025. This signals continued institutional confidence in the platform’s long-term viability.

The CoinDCX saga carries direct and urgent lessons for every crypto user in India.

First, always verify the URL before making any transaction. The real CoinDCX operates at coindcx.com and nothing else. Fraudsters rely on domains like coindcx.pro or coindcx.io to trick users. A single wrong character in the URL can mean the difference between a legitimate platform and a scam.

Second, never send money based on unsolicited “franchise” or high-return offers. It does not matter how legitimate the branding looks. No reputable exchange offers 10-12% monthly returns through WhatsApp and Telegram.

Third, always use official apps downloaded from verified app stores. Do not rely on links shared via messaging platforms.

Fourth, once the D.S.N. WhatsApp helpline goes live, use it immediately. Forward any suspicious link, message, or offer for verification before transacting. The service will be free and open to everyone, not just CoinDCX users.

If it sounds too good to be true, it almost certainly is.

The investigation into the actual scammers behind coindcx.pro is still ongoing. The real culprits remain at large. These are the people who built the fake website, impersonated the founders, and collected cash from victims. One accused, Akash Rana, reportedly settled with the complainant. However, the broader network has not been dismantled yet.

For CoinDCX, the D.S.N. represents a calculated bet. The company believes proactive spending on public cyber safety infrastructure will rebuild trust faster than any PR campaign could. So far, industry observers have largely responded positively. Many have called it a “much-needed industry first” on X. Gupta has also publicly invited regulators, banks, and rival platforms to join the initiative.

For policymakers, the case offers a clear blueprint. Faster inter-state coordination, AI-assisted complaint triage, and incentives for private-sector safety infrastructure could prevent future wrongful arrests. These steps could also help reduce the annual ₹22,000-crore-plus cyber fraud bill.

The CoinDCX saga began as a story of deception and temporary injustice. Two founders spent 72 hours in custody for a crime they did not commit. Their response was not bitterness. Instead, they committed ₹100 crore to ensuring fewer Indians suffer the same fate. Whether the rest of the ecosystem picks up that shield will determine if this “wake-up call” actually changes the game.

In India’s digital gold rush, vigilance is not optional. It is survival.