Crypto as Commodity: What It Means?

Crypto commodity explained. Learn how this classification impacts regulation, institutions, and the future of crypto markets.

Mar 21, 2026, 7:12 PM UTC

Author: Chirag Sharma

When regulators draw a clear line, markets do not just react. They reorganize around it. That is what is happening with the rise of the crypto commodity framework. For years, one question dominated the space. Do these assets behave like securities, or do they act as independent commodities?

That uncertainty slowed everything down. Exchanges hesitated before listing assets. Institutions stayed cautious. Builders worked under constant legal pressure. No one could fully commit because the rules could shift at any time. Now that some assets fall under the crypto commodity category, that uncertainty starts to fade. And when uncertainty fades, capital and participation follow.

This shift is not just regulatory. It changes how crypto fits into the broader financial system.

To understand why this matters, we need to start from the basics. What separates a commodity from a security? And why has this distinction shaped crypto for years?

The Two Buckets: Securities vs Crypto Commodity

Every financial asset in the United States fits into a category. That classification decides how regulators treat it and who can access it.

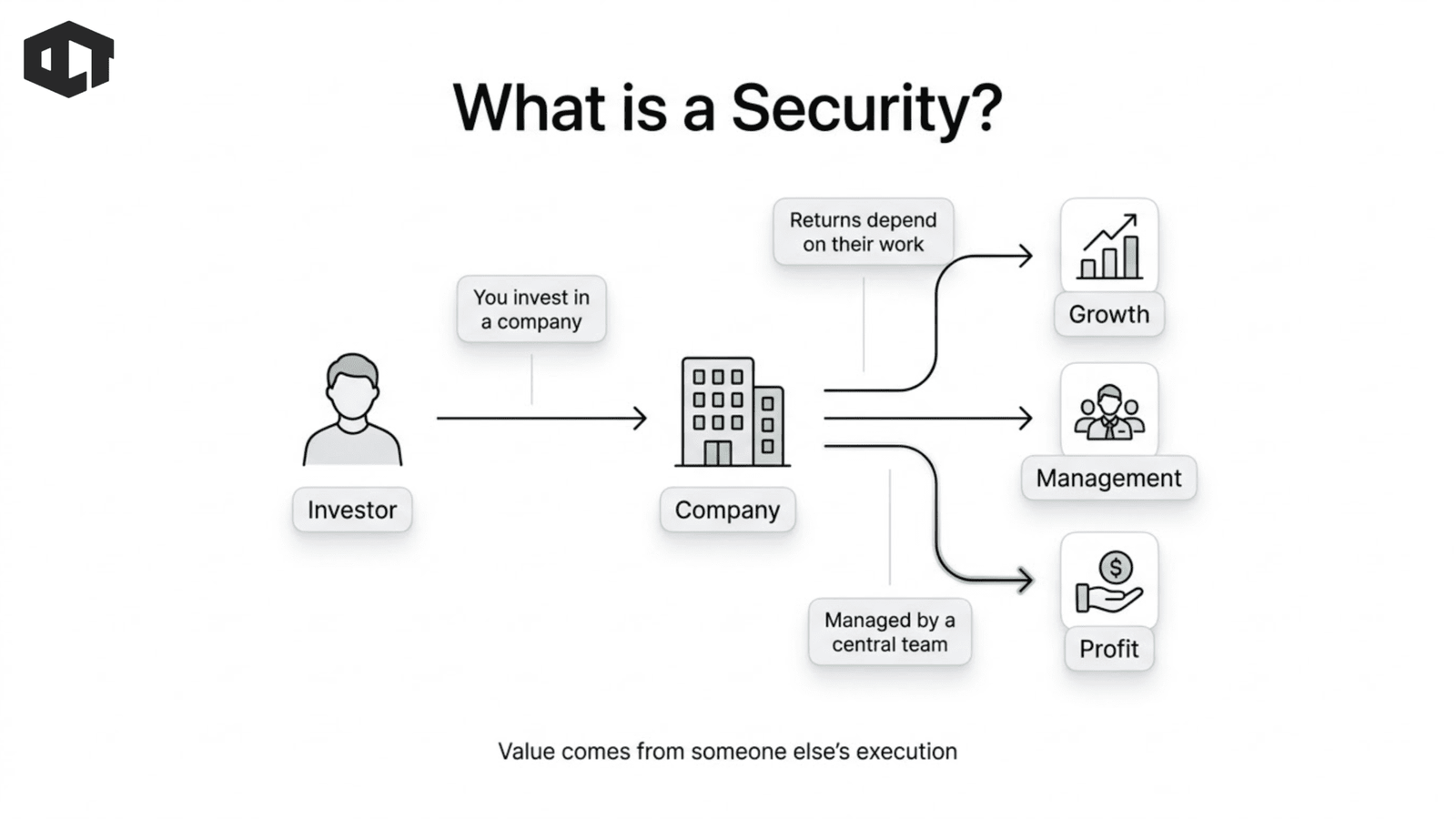

A security represents an investment tied to someone else’s effort. When you buy a stock, you trust a company’s management to grow value.

Your returns depend on their execution. Because of this dependency, regulators enforce strict rules on securities. Companies must disclose financial data and register their offerings. These rules protect investors from hidden risks.

A crypto commodity works on a different foundation. Commodities exist independently of any single entity. Their value comes from supply, demand, and real usage. Gold does not rely on a management team to stay valuable. Oil does not depend on a founder to maintain demand.

The market determines their value through activity and scarcity.

When a digital asset behaves like this, it starts to resemble a crypto commodity. Its value does not depend on promises from a central team. Instead, it depends on how users interact with the network. This distinction shapes everything in the market.

If regulators treat an asset as a security, access becomes restricted. Compliance costs increase and participation slows down. If they treat it as a crypto commodity, the framework becomes more flexible.That flexibility allows the asset to grow within open markets.

Value Driver

Ownership Meaning

Dependency

Participation

Why Crypto’s Classification Stayed Unclear for So Long

Crypto did not evolve in a straight line. It moved through phases, and that created confusion. In the early stage, many projects raised money through token sales. They attracted investors by promising development and future growth. This looked similar to traditional investment contracts.

That pushed regulators toward treating these tokens as securities. At the same time, some networks followed a different path.

Bitcoin launched without a central issuer. It operated as a decentralized system from the start. Ethereum began differently but reduced central control over time. As these networks matured, they started behaving like independent systems.

This created a split within the same market. Some tokens clearly resembled securities. Others behaved like commodities. Many sat somewhere in between, which made classification difficult. Regulators tried to apply existing frameworks, but those frameworks came from traditional finance. They did not account for decentralized systems that evolve over time.

As a result, uncertainty dominated the market. Projects faced long legal battles. Exchanges made cautious listing decisions. Institutions avoided exposure due to unclear risks. The biggest problem was not strict regulation. It was inconsistent interpretation.

When participants cannot predict the rules, they hesitate to act. That hesitation slowed growth across the ecosystem.

What It Means to Be a Crypto Commodity

The shift toward recognizing assets as a crypto commodity changes how the system views them. At its core, this classification means the asset no longer depends on a central team. Its value comes from network activity and user participation.

This changes the legal perspective. Instead of treating the asset as part of an investment contract, regulators view it as a decentralized resource. The focus moves from the issuer to the network itself.

This clarity unlocks participation across the market. Exchanges can list these assets with more confidence. Custodians can hold them under clearer guidelines. Financial institutions can build products with lower legal risk.

On-chain activity also becomes easier to interpret. When users stake tokens or transfer assets, they interact with a system. They are not entering an investment contract. This aligns regulation with actual usage. That alignment removes friction from the system. And once friction disappears, growth tends to accelerate naturally.

Decentralization

Network Maturity

Utility

Distributed Control

Market Behavior

No Ongoing Promises

The Characteristics of a Crypto Commodity

Not every digital asset qualifies as a crypto commodity. The ones that do share clear and consistent traits, and these traits develop over time rather than appearing instantly.

The first factor is decentralization. A network moves toward commodity status when no single entity controls its direction. Decision-making spreads across developers, validators, and users. No team can directly influence value through its actions, which removes the dependency that defines a security.

The second factor is network maturity. Most assets begin with strong central influence, but mature networks evolve beyond that stage. They show sustained activity, multiple contributors, and consistent usage across market cycles. This evolution reduces reliance on any founding team and strengthens their independence.

The third factor is utility. A strong crypto commodity serves a clear role within its ecosystem. It may power transactions, support staking, or enable governance decisions. The stronger and more necessary this role becomes, the more the asset behaves like a resource rather than a contract.

Another important factor is the absence of ongoing promises. Projects that constantly signal future returns or depend on a team’s roadmap resemble securities. A crypto commodity does not rely on such narratives. Its value emerges from usage, activity, and market demand.

These characteristics do not appear overnight. They develop gradually as networks grow, which is why classification often follows years of evolution rather than early-stage launches.

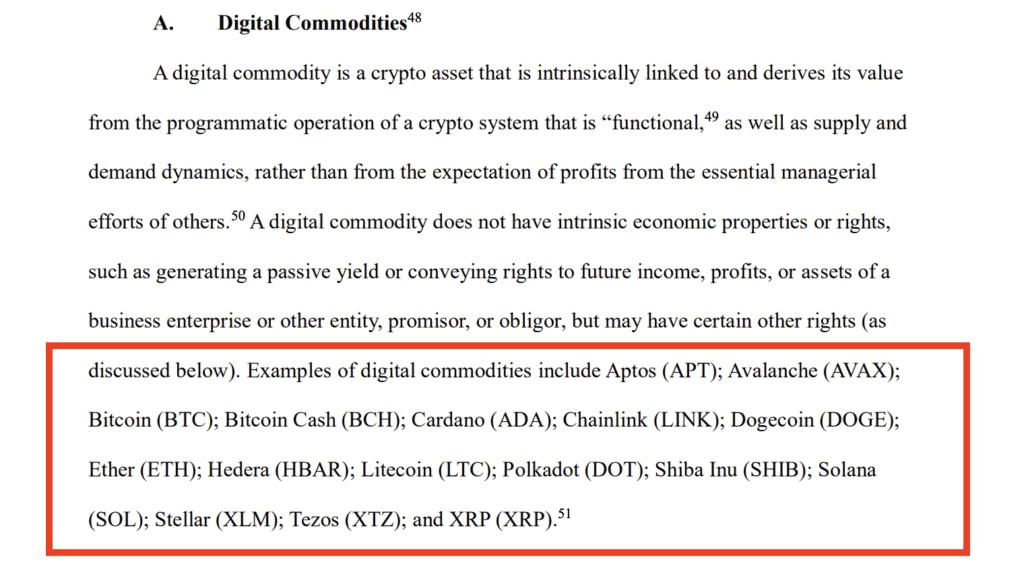

Which Assets Fit This Model and Why It Matters

The assets that qualify as a crypto commodity follow a clear pattern, and understanding this pattern helps explain how regulators view decentralization.

Most of these networks have existed for years and survived multiple market cycles. They have built strong communities and proven that their value does not depend on a single team. This history creates confidence in their independence.

They also show consistent activity across the network. Users transact, stake, and build on top of these systems daily. This activity creates organic demand, which supports their classification as standalone assets.

Control also shifts over time. Founders and early teams lose direct influence as the ecosystem expands. Decision-making spreads across participants, which reduces central authority and strengthens decentralization.

Market perception also plays a role. If participants treat an asset as an independent system rather than an investment contract, it moves closer to the crypto commodity category. Behavior and structure often align over time.

This creates a natural roadmap for new projects. They do not start as a crypto commodity. They must prove decentralization, build usage, and reduce reliance on central teams. Only networks that survive and evolve reach this stage.

How This Unlocks Institutional Participation

The most important impact of the crypto commodity classification comes from institutional capital. Large investors operate under strict compliance frameworks, and they require clear rules before allocating capital.

Before this shift, most digital assets existed in a gray area. Institutions could not confidently classify them, which created legal and compliance risks. If regulators later treated those assets as securities, it could create serious consequences for investors.

Because of this uncertainty, most institutions stayed away from the market.

Now the situation changes. A crypto commodity fits into a framework that institutions already understand. Commodities have been part of portfolios for decades, and the rules around them are well established.

This familiarity reduces friction across the system. Compliance teams can approve exposure more easily, and custodians can offer services under defined guidelines. Financial firms can build products without navigating unclear regulations.

The impact builds gradually. More capital enters the market, liquidity improves, and price discovery becomes more efficient. Larger participants can operate without disrupting markets, which creates a more stable environment over time.

This shift does not happen instantly, but the direction becomes clear once classification is defined.

The Structural Shift in Market Infrastructure

When clarity enters a market, infrastructure evolves quickly. The crypto commodity framework enables the development of financial products that were previously difficult to launch. Exchange-traded funds, index products, and diversified portfolios become easier to structure and approve. This expands access for investors who prefer traditional financial systems and do not want to manage assets directly.

Custody solutions also improve. Institutions require secure and regulated storage, and clearer classification allows banks and financial firms to offer these services with confidence. This raises the overall security standard across the ecosystem.

Lending and borrowing markets also expand. Assets within a crypto commodity framework can serve as collateral more easily, which unlocks capital efficiency and new financial strategies. This allows participants to use their holdings more productively.

Another important shift is the reduction of regulatory arbitrage. In the past, companies moved to favorable jurisdictions to avoid uncertainty. With clearer rules, more activity can move into regulated environments, which strengthens the overall system.

The market becomes more structured and connected. Instead of fragmented systems operating in gray areas, a more unified financial layer begins to form around these assets.

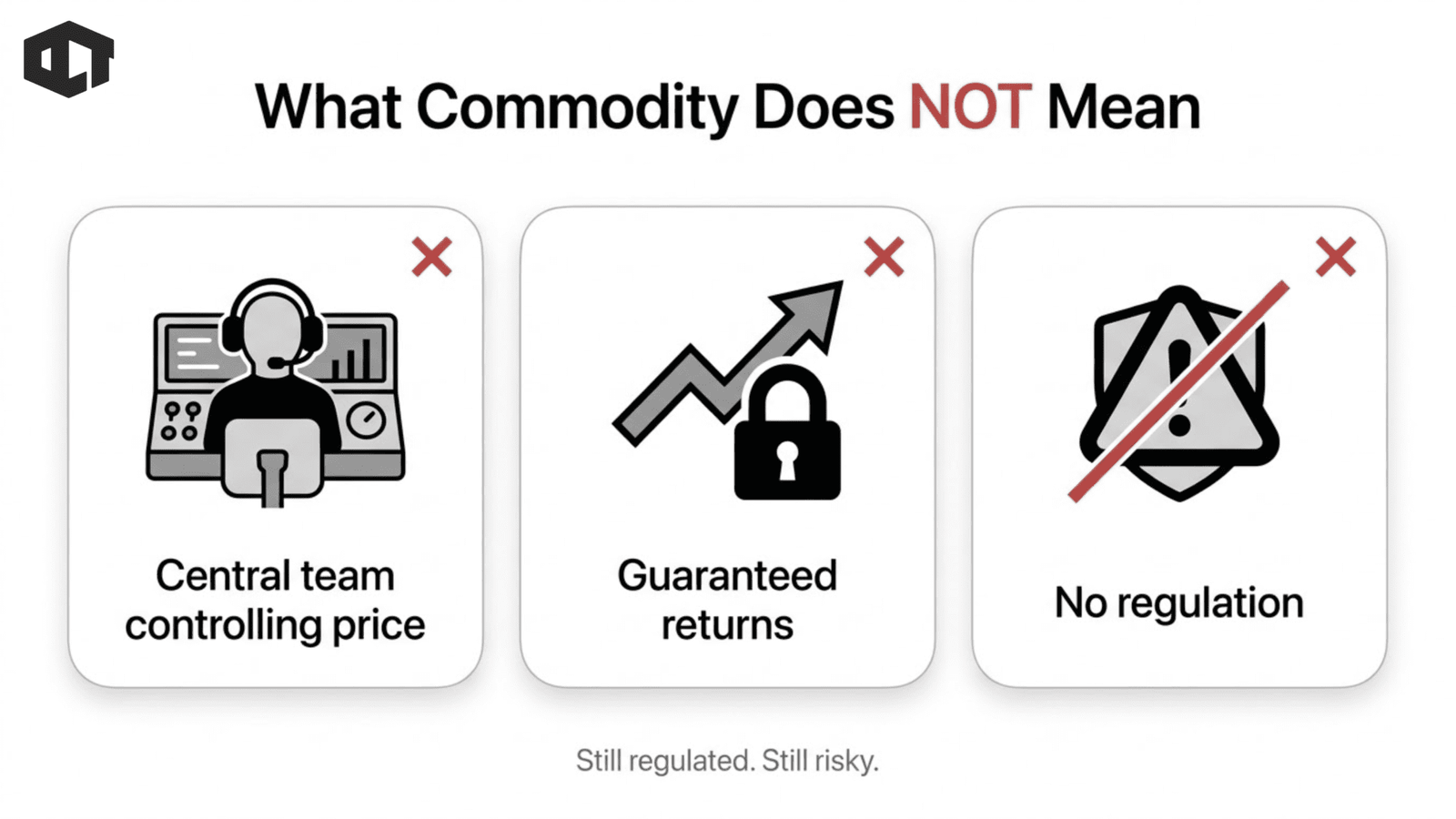

What Crypto Commodity Status Does Not Mean

It is easy to assume that this shift solves every problem in crypto. That is not the case, and misunderstanding this can lead to poor decisions. A crypto commodity is not an unregulated asset. Regulators still monitor markets for fraud, manipulation, and illegal activity. Trading platforms must follow compliance rules, especially when they offer derivatives or structured products.

It also does not mean that every cryptocurrency qualifies. Only networks that meet decentralization and maturity standards fall into this category. New projects, especially those controlled by a central team, can still be treated as securities. Another important point is risk.

A crypto commodity can still be highly volatile. Prices can rise quickly, but they can also drop just as fast. Classification does not protect against market cycles, competition, or weak fundamentals. It also does not make all assets equal.

Bitcoin, Ethereum, and other networks may share the same classification, but their technology, adoption, and long-term potential differ significantly. Regulatory clarity does not remove the need for analysis. This distinction matters because it separates legal structure from investment quality. One defines how an asset is treated. The other defines whether it is worth holding.

Risks and Limitations

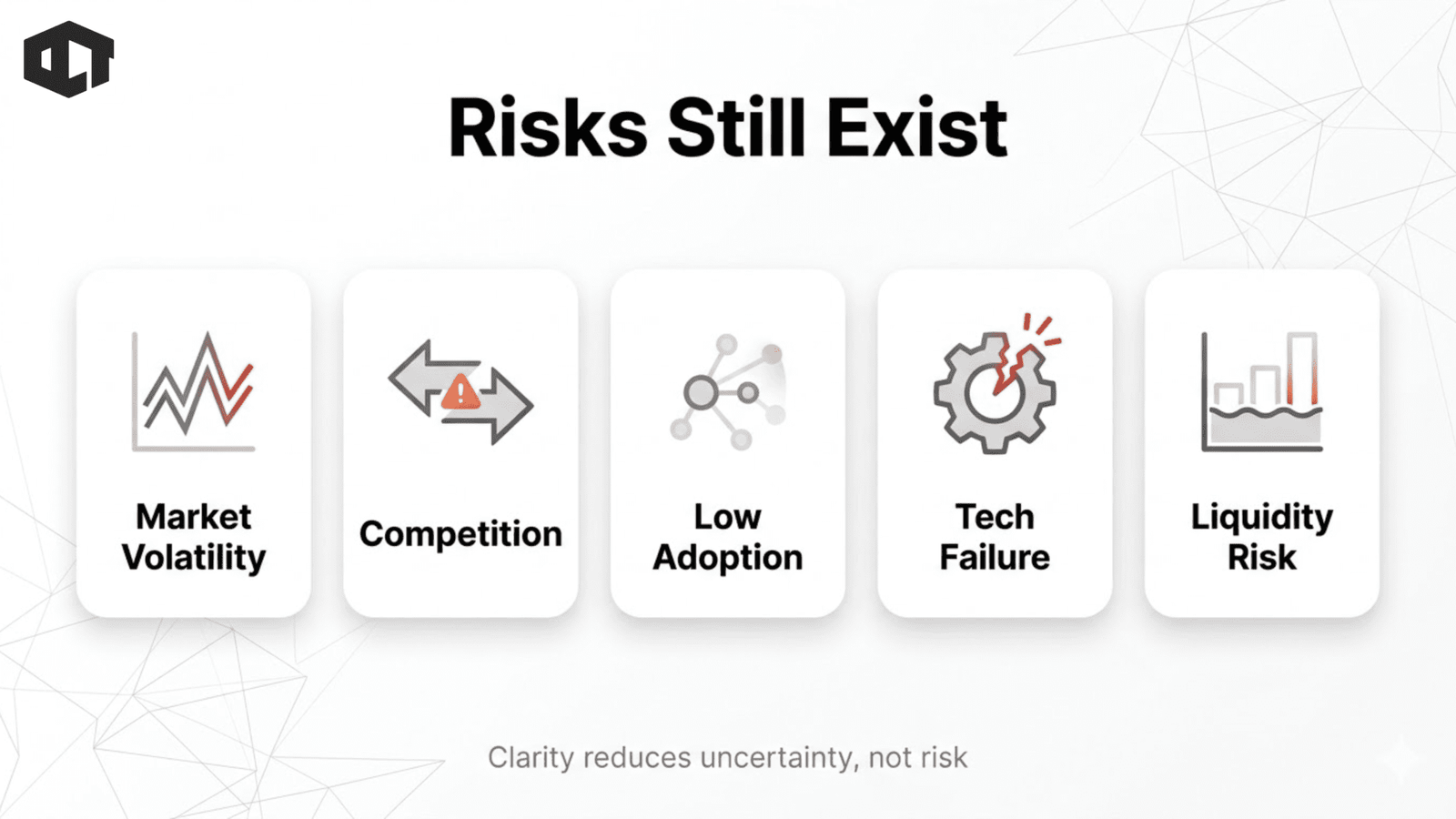

Even with better clarity, several risks remain. Market risk continues to dominate. Crypto markets move quickly and often react to sentiment as much as fundamentals. A crypto commodity can still lose value due to macro shifts, liquidity changes, or narrative rotations.

Technological risk also plays a role. Networks compete for users, developers, and capital. A stronger competitor can reduce demand for an existing asset, even if its classification remains unchanged. Adoption risk matters just as much.

If a network fails to attract users or sustain activity, its long-term value declines. Utility alone does not guarantee growth. It must translate into real usage over time. There is also the risk of misinterpretation. Some investors may see the crypto commodity label as a sign of safety. This creates false confidence. The classification removes legal uncertainty, but it does not eliminate investment risk.

Finally, regulatory evolution remains possible.

Rules can change as markets grow. While the current framework provides clarity, future updates may refine how these assets are treated. Staying informed remains important for both investors and builders.

Conclusion

The recognition of crypto assets as a crypto commodity marks a structural shift in the market. For years, uncertainty limited growth. Projects operated under unclear rules, and institutions avoided exposure due to compliance concerns. That environment made long-term planning difficult for everyone involved.

Now, a clearer framework begins to take shape. Markets can build with more confidence. Institutions can allocate capital with fewer barriers. Infrastructure can evolve in a more structured way. This creates a stronger foundation for long-term growth.

But this is not the end of the journey. The classification defines how assets are treated, not how they perform. Value still depends on adoption, innovation, and real-world use. Strong networks will continue to grow, while weaker ones will struggle.

The opportunity becomes clearer, but the responsibility remains the same. Investors must understand what they hold. Builders must create real value. Markets must continue to mature through actual usage, not just narratives. This shift does not guarantee success, but it removes one of the biggest barriers that held the market back. What happens next depends on how the ecosystem builds on this foundation.

TL;DR — Crypto as a Commodity

- A crypto commodity derives value from network usage, not a central team.

- It differs from securities, where returns depend on managerial effort.

- This classification can reduce regulatory uncertainty across crypto markets.

- Mature and decentralized networks are more likely to qualify as commodities.

- Utility and real usage strengthen commodity-like behavior over time.

- Institutions can participate through more familiar commodity-style frameworks.

- This unlocks capital, liquidity, and stronger market infrastructure.

- Products like ETFs, custody, and structured investment vehicles become easier to build.

- Not all cryptocurrencies qualify, especially early-stage or centralized projects.

- Market risks remain, including volatility, competition, and adoption challenges.

In this article

The Two Buckets: Securities vs Crypto CommodityWhy Crypto’s Classification Stayed Unclear for So LongWhat It Means to Be a Crypto CommodityThe Characteristics of a Crypto CommodityWhich Assets Fit This Model and Why It MattersHow This Unlocks Institutional ParticipationThe Structural Shift in Market InfrastructureWhat Crypto Commodity Status Does Not MeanRisks and LimitationsConclusion