DOT sits just cents above its all-time low after treasury blowouts, parachain failures, and builder exits. Here's what happened to Polkadot and what comes next.

Author: Sahil Thakur

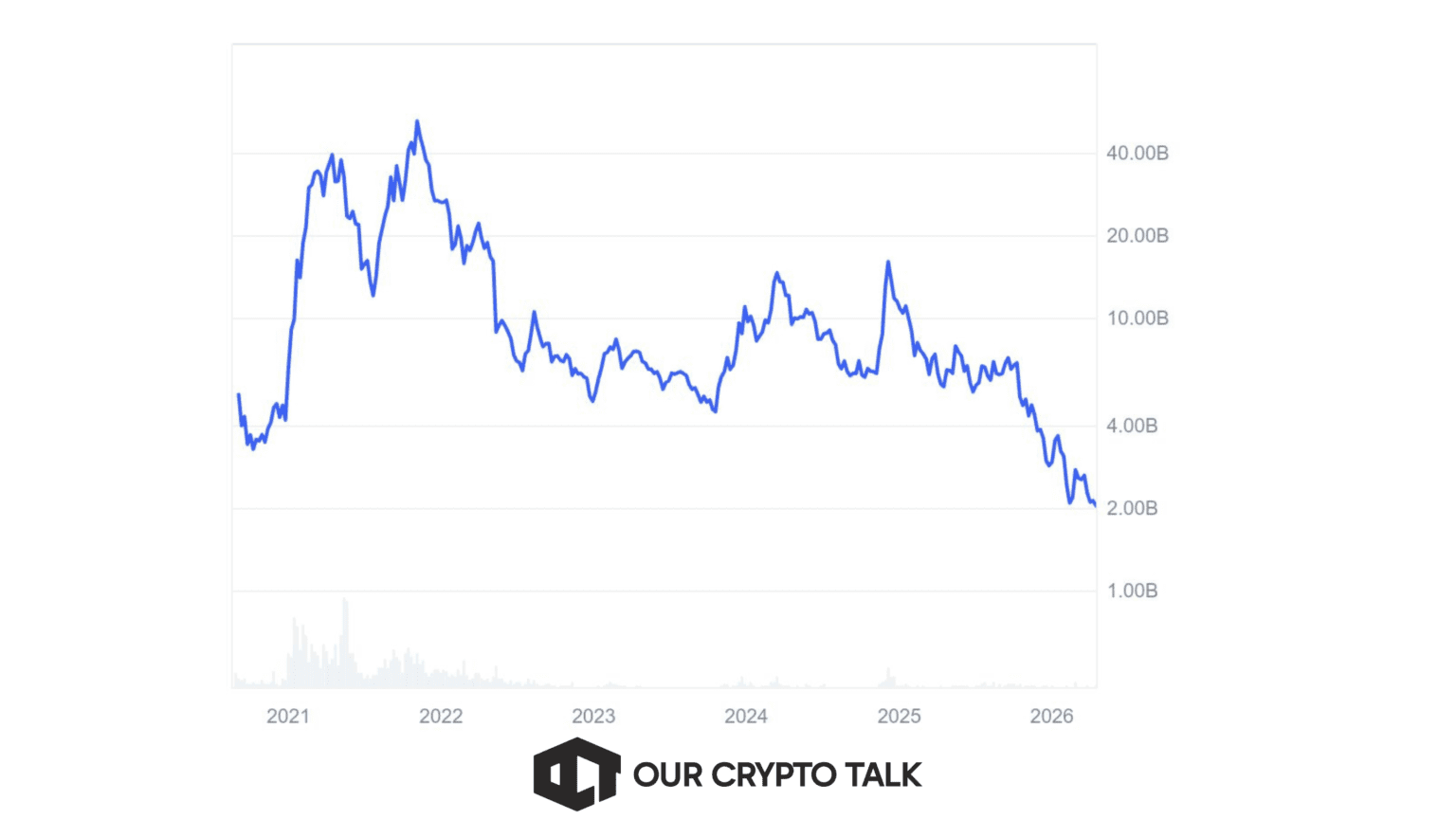

DOT trades at about $1.18 as of April 2026. Its all-time high was $54.98. Its all-time low is $1.15. That three-cent gap between where the token sits today and the worst price it has ever recorded tells you most of what you need to know about what happened to Polkadot. The April 2026 Hyperbridge exploit grabbed headlines, but the collapse didn’t start with a hack. It started years earlier, with a treasury that spent like a growth company, a parachain model that never delivered on its promise, and an ecosystem that watched its best-known builders walk away.

This is the full accounting of what happened to Polkadot. What went wrong, what the numbers actually say once you strip out the sloppy retellings, what the network got right despite the mess, and whether any of it adds up to a recovery case.

The technical facts of the April 2026 exploit matter, because the most common version of the story gets them wrong. The attacker didn’t mint native DOT on the relay chain. The vulnerability sat in Hyperbridge’s Ethereum gateway, specifically in its proof verification logic. A forged proof gave the attacker admin control over the bridged DOT token contract on Ethereum. From there, they minted 1 billion bridged DOT and dumped it on a decentralized exchange.

Actual losses came in around $237,000. Both Hyperbridge and Polkadot released official statements confirming that native DOT, parachains, and the core network were unaffected. Other bridges continued operating normally.

So why did it matter?

Because interoperability is supposed to be one of Polkadot’s defining strengths. In its own 2024 year-end report, the ecosystem celebrated the launch of three trustless bridges, including Hyperbridge, as a headline milestone. The exploit hit a pillar that Polkadot had actively promoted as evidence of progress. For a market already skeptical about the ecosystem’s direction, the technical distinction between native DOT and bridged DOT was important but not enough to change sentiment. The damage was reputational, and it landed on a network that couldn’t afford more of it.

If you want to understand what happened to Polkadot, start with the treasury. The most damaging evidence against the network didn’t come from critics or short sellers. It came from Polkadot’s own spending reports.

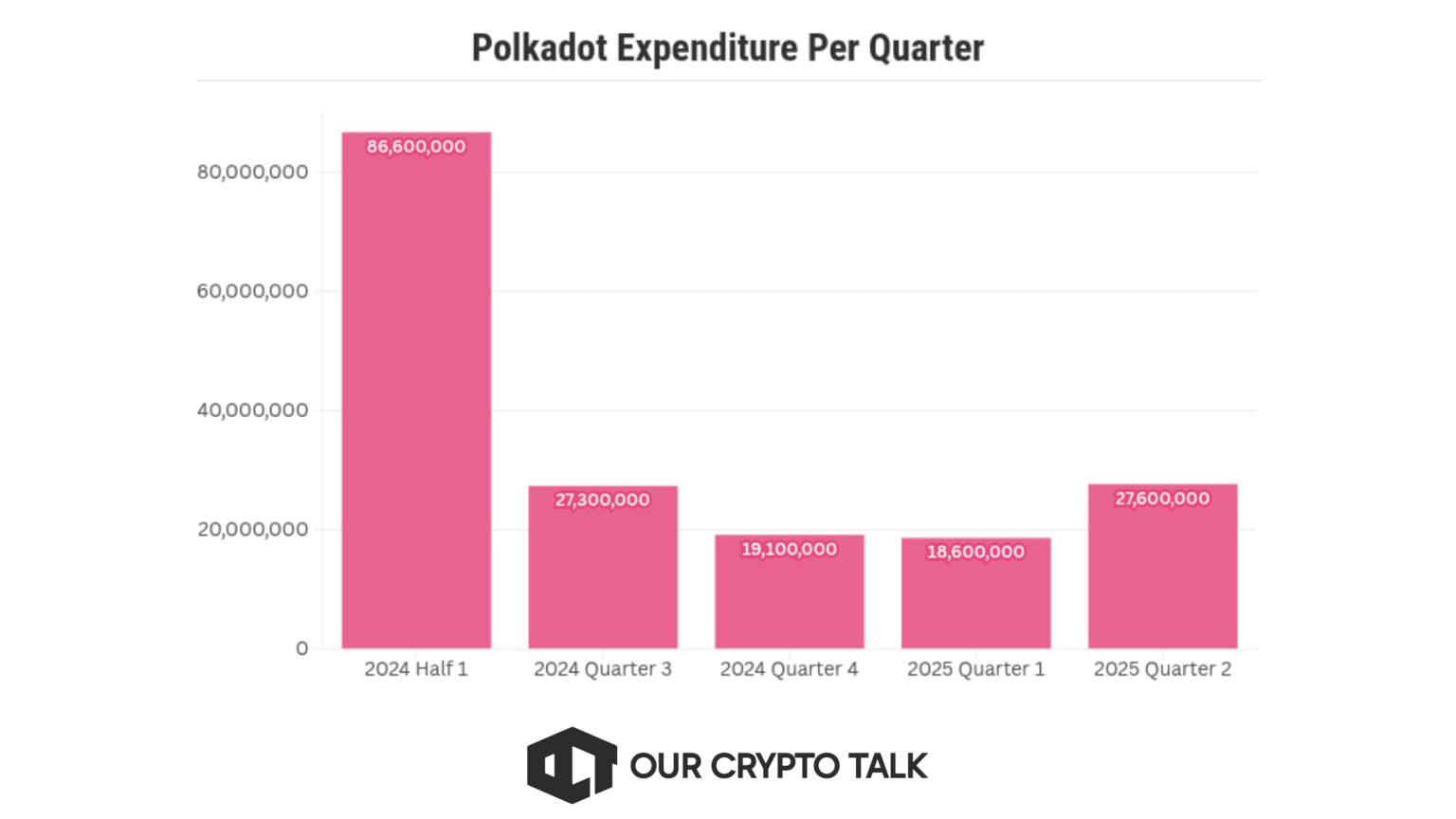

The 2024-H1 report disclosed $87 million in spending during the first half of the year. Direct fee revenue was described as “marginal,” with regular fees running at roughly 20,000 DOT per quarter. The full-year 2024 report then put total annual Polkadot treasury spending at $133 million. Outreach alone consumed $48 million of that.

The line items told the story. In H1 2024, sponsorships accounted for $10 million, influencer spending hit $4.9 million, and digital ads cost $4 million. By Q3 2024, the treasury report logged another $3.9 million top-up tied to the Inter Miami CF sponsorship and $3.3 million more for influencers. This wasn’t one weird proposal slipping through governance. It was a repeated preference for awareness spending before proving that awareness could convert into users, developers, or fee revenue.

Some commonly repeated numbers deserve correction. The Inter Miami sponsorship doesn’t appear in primary reports as a single $8.8 million figure. The H1 and Q3 reports together point to roughly $10.7 million in 2024 accounting impact. The Conor Daly sponsorship was $1.9 million according to the H1 report, not the $2.1 million that circulates online. And the CoinMarketCap deal: the primary proposal verifiable in treasury records was a $980,000 six-month integration, with separate reporting referencing about $478,000 for event credits and a dynamic logo. The exact $418,000 figure often repeated online doesn’t match any primary treasury document I could verify.

Getting these numbers right matters because the real story is bad enough without embellishment. A network spending $133 million per year while generating marginal fee revenue doesn’t need exaggerated marketing budgets to look like a problem.

The most important update is that the community eventually responded. By Q4 2025, the treasury report showed spending had fallen to $7.4 million for the quarter. The report described the income statement as positive for the first time since OpenGov launched. That doesn’t erase the 2024 blowout, but it does show the governance process can course-correct when the pressure gets bad enough.

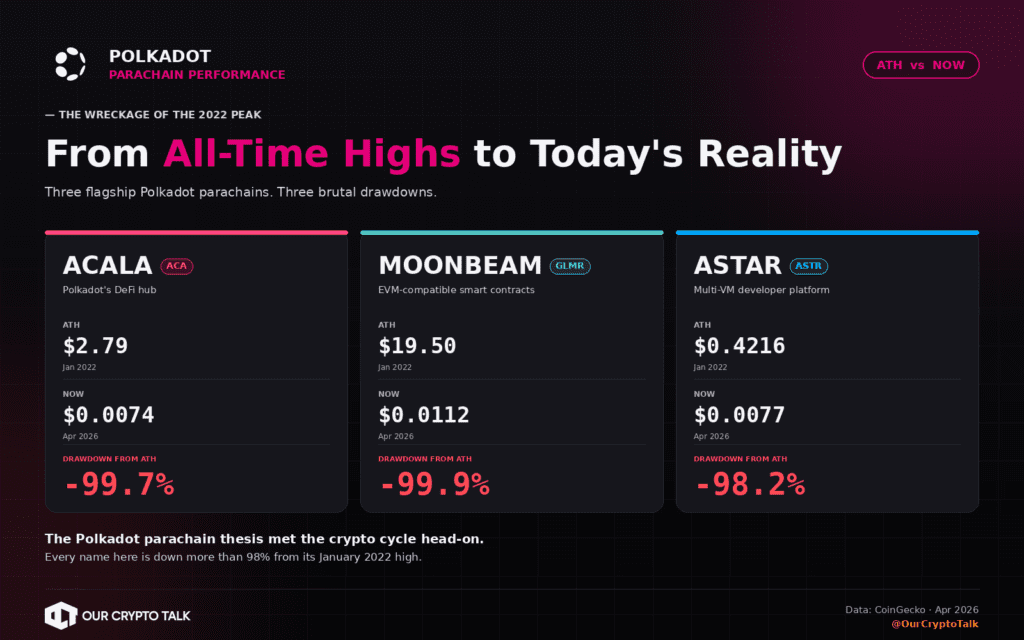

Polkadot’s original pitch was built on parachain slot auctions. Teams would bid to lease slots on the relay chain, creating a scarcity mechanism that tied DOT demand directly to ecosystem growth. The theory made sense on paper. In practice, the tokens of the projects that won those slots tell a different story.

Acala, once positioned as Polkadot’s DeFi hub, trades at roughly $0.0006846 against an all-time high of $2.79. That’s a decline of about 99.98%. Moonbeam, the ecosystem’s primary EVM-compatible chain, sits around $0.01134 versus a $19.50 high, down approximately 99.9%. OKX delisted GLMR spot pairs in September 2025. Astar trades near $0.0077 against a $0.4216 high, a drop of about 98.2%. If the promise was that parachains would become thriving specialized economies, these numbers are the market’s verdict on that promise.

The exits were just as telling. Phala Network’s own 2025 year-in-review announced the sunsetting of its Polkadot parachain in November 2025, with staking, governance, and core activity migrating to Ethereum L2 infrastructure. This wasn’t a multichain expansion. It was one of the ecosystem’s more recognized projects saying its future wasn’t on Polkadot anymore.

Parallel Finance was worse. The project posted a “Shutdown & Full Liquidation Notice” on its Medium page in August 2025. Separately, a formal Polkadot referendum sought investigation into alleged secret minting and burning of cDOT-related positions. Those allegations aren’t the same thing as a court judgment, and that distinction matters. But even with that caution, a shutdown plus formal fraud complaints through on-chain governance is exactly the kind of episode that kills confidence in an already struggling ecosystem.

Then there was the culture problem. Manta Network co-founder Victor Ji publicly described the Polkadot ecosystem as “highly toxic” during the same period when spending controversies were dominating the conversation. One founder’s frustration doesn’t represent the entire builder community. But a prominent ecosystem participant openly telling others to look elsewhere carries weight. Markets can absorb low prices. They’re much less forgiving when insiders lose conviction in public.

Part of what happened to Polkadot is that the original “killer feature” isn’t even the product being sold anymore. The 2024 year-end report confirmed that Agile Coretime and Async Backing had phased out the Parachain Slot Auction model entirely. Technically, that’s an upgrade. Narratively, it means the 2021 scarcity thesis around auctioned parachain slots wasn’t fulfilled. It was replaced. That’s why the fairest verdict isn’t that Polkadot is dead in a literal sense, but that its first major product story has already died.

A one-sided obituary would be wrong. The engineering team kept shipping, and some of what they shipped is genuinely significant.

Agile Coretime and Async Backing went live, giving developers more flexible access to Polkadot’s block space. More than 50% of DOT supply is staked, and the active validator set expanded to 500. Between January and November 2024, unique accounts grew by 150% and signed transactions rose by more than 200%. Those aren’t ghost chain numbers.

Developer activity stayed meaningful too. Parity’s 2025 year-end dashboard, citing Electric Capital rankings, placed Polkadot 9th in full-time developers with 485. That’s behind the biggest L1s, but it’s a real developer community by any standard.

In January 2026, Polkadot Hub went live as a production smart-contract platform supporting both EVM and PolkaVM execution paths. For years, one of Polkadot’s practical weaknesses was that the easiest place for ordinary app developers to build was somewhere else. Hub at least addresses that gap structurally, even if adoption remains early.

The tokenomics shift in 2025 and 2026 was another genuine positive. The community approved a hard supply cap of 2.1 billion DOT. On March 14, 2026, annual issuance fell from 120 million DOT to 55 million, with future reductions designed to converge toward the cap. The same package began routing treasury burns and slashes into a Dynamic Allocation Pool and set up broader staking reforms. In plain English: Polkadot stopped pretending that endless inflation plus discretionary spending was a sustainable substitute for real demand.

The pattern here is a network whose engineering pace outperformed its economic capture. The code got better. The product-market fit didn’t keep up.

Any realistic Polkadot recovery starts by rejecting the fantasy that more sponsorships and influencer campaigns can fix a broken product narrative. The path back is narrower and more boring than what came before: lower treasury burn, clearer product focus, safer interoperability, and actual fee-generating applications.

The late-2025 treasury slowdown proves the first part is possible. Polkadot Hub’s launch proves the second part is at least technically available. But proving something is possible and proving it works are very different things.

The best-case scenario looks something like this. First, Hub becomes the default place for normal developers to ship contracts and apps. Not every team should need to internalize Polkadot’s full architectural complexity before they can launch. Second, the ecosystem builds around actual on-chain monetary activity rather than brand awareness. Stablecoin supply tracked on Polkadot-connected rails sits at around $75 million as of early 2026. That’s not large, but it’s a measurable base.

Third, treasury spending stays near the Q4 2025 discipline level rather than drifting back toward the $133 million annual profile. And fourth, bridge security and operational conservatism get treated as existential priorities after Hyperbridge, not optional improvements.

There’s a softer requirement too: trust repair. Polkadot doesn’t just need more code. It needs fewer reasons for builders to leave and fewer reasons for users to assume the ecosystem is chaotic or hostile. Cleaner governance, harder ROI standards for treasury proposals, and fewer episodes like the ones tied to Phala, Parallel, and Manta.

Recovery is possible. But only if the network starts compounding credibility faster than it compounds technical features.

If you’re trying to figure out whether any of this turnaround story is real, here are the metrics that matter.

Fees and revenue come first. Third-party analytics show Polkadot at roughly $3,300 in fees and $3,000 in revenue over the last 30 days as of April 2026. If those numbers don’t move decisively upward, the rest of the story is mostly branding.

Treasury discipline is the easiest leading indicator. The question is whether quarterly spending stays near $7.4 million or creeps back toward 2024 levels. This tells you whether governance has actually internalized the lesson or just paused spending temporarily under pressure.

Hub adoption is the product test. Smart contracts are live. What matters now isn’t the launch itself but whether contract deployments, active users, and stablecoin liquidity climb from today’s low base over the coming quarters.

And retention is the sentiment test. If more teams follow Phala outward, if prominent founders keep denouncing the ecosystem, or if bridge incidents keep hitting interoperability infrastructure, the market will keep treating every technical upgrade as too little, too late. If Hyperbridge remediation works cleanly and Hub gives builders a simpler home, the Polkadot narrative can at least stabilize.

The cleanest way to frame what happened to Polkadot is this: the software isn’t dead, and the April 2026 exploit didn’t break native DOT. But the original public thesis has suffered a near-total collapse. The parachain-auction story was retired, treasury credibility was badly damaged by years of spending, flagship ecosystem tokens were annihilated, and several well-known builders either exited or repudiated the culture. What remains is a technically capable network trying to earn a second chance after burning through much of the goodwill that was supposed to carry its first one.

This article is for informational purposes only and does not constitute financial advice. Always do your own research before making investment decisions.