How did USD1 become a top 5 stablecoin in just one year of the launch? We explore in this article the growth to $4.5B market cap and its potential from here.

Author: Sahil Thakur

The USD1 stablecoin launched in March 2025. Fifteen months later, the token sits fourth on DefiLlama. Its market cap is about $4.57 billion. Only USDT, USDC, and Sky Dollar USDS sit ahead of it. CoinGecko shows a similar picture, with USD1 around $4.63 billion across a stablecoin category worth roughly $310.3 billion.

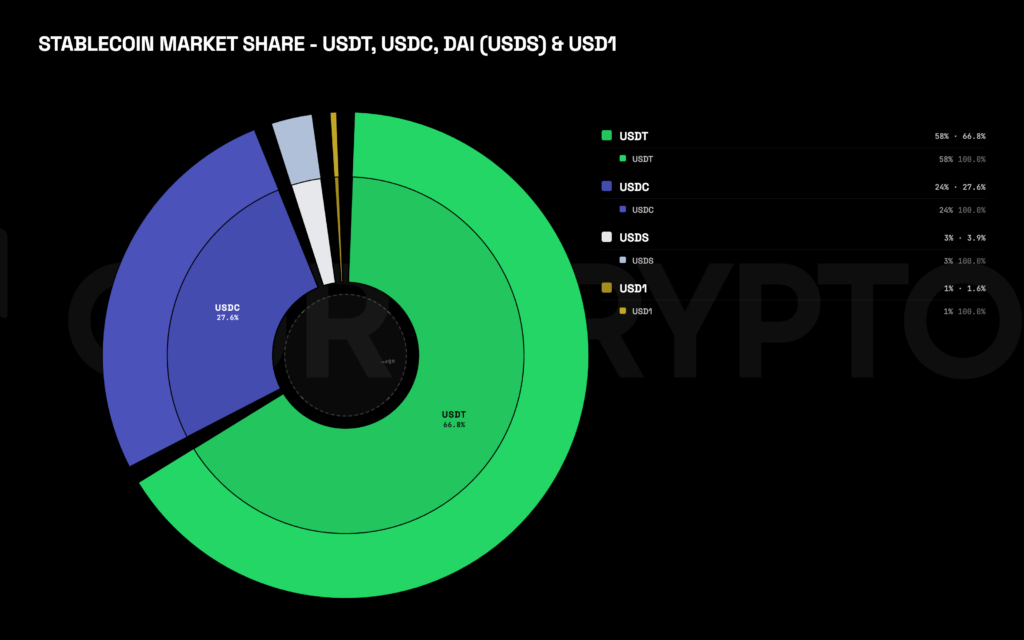

That makes USD1 about 1.45% to 1.5% of the market. The two giants don’t dominate quite as completely as they used to. On DefiLlama today, USDT and USDC together hold about 82.9% of the stablecoin market. That’s a drop from the ~88% figure that was making the rounds earlier this year.

The structural story is simple. A fiat-backed stablecoin entered the top five in fifteen months. It got there through distribution, not novelty. That’s worth understanding regardless of how you feel about the people behind it.

USD1 is a fiat-backed stablecoin issued by BitGo. World Liberty Financial USD1 is the long-form name. WLFI is the Trump-affiliated crypto venture most readers will already know. The token launched on Ethereum and BNB Chain in March 2025. It now lives across eleven blockchains.

The pitch is conventional. One USD1 redeems for one dollar. The reserves are cash and short-duration government instruments. BitGo holds them in a segregated trust.

The reason searches for the USD1 stablecoin keep climbing is the speed of the rise. Most new fiat-backed tokens spend years getting to a billion dollars in supply. USD1 did it in months. It’s now a $4.6 billion asset sitting in the top five of a $315 billion market. It overtook PYUSD and DAI along the way.

You should know the risk surface before the bullish framing. World Liberty Financial’s own docs say USD1 isn’t legal tender. It isn’t deposit-insured either. Direct redemption is limited to eligible BitGo customers. BitGo or WLFI parties can block or freeze addresses.

The peg held in February 2026 when the token briefly dipped. But the control surface around USD1 is highly centralized. That trade-off is baked into the design. The rest of this article assumes you’ve taken it on board.

The cleanest way to see the climb is through the attested reserve reports. BitGo and Crowe published a year-end attestation. It showed $3.3135 billion of redeemable USD1 outstanding on December 31, 2025. A second BitGo/Crowe attestation showed $4.3928 billion on March 31, 2026. DefiLlama puts the current figure at about $4.571 billion. USD1 has grown roughly 38% from year-end 2025 to now. It’s also stayed close enough to its peg to remain a credible fiat-backed asset.

The USD1 market cap matters less than the rank shift. As USD1 expanded, the rivals just below the two giants stagnated. PYUSD and DAI either flatlined or shrank over the last month on DefiLlama. So when USD1 overtook them, it wasn’t just a function of USD1 minting harder. It captured relative share in the part of the stablecoin market sitting below USDT and USDC. That’s the more honest read.

The cleanest way to picture this is a simple supply line. Start with $3.31 billion at year-end 2025. Move to $4.39 billion at the end of Q1 2026. Land somewhere between $4.57 and $4.63 billion now, depending on the tracker. Add markers at the dates USD1 passed PYUSD and then DAI. The climb was steady, attested, and rank-altering, all in the same fifteen-month window.

USD1’s design isn’t unusual. It’s a fully reserved fiat-backed stablecoin with a vanilla treasury portfolio. The reason it grew so fast is distribution. It launched into rails that almost no new issuer ever gets. The pieces also stacked unusually quickly.

Binance is the central venue. Forbes reported in February that Binance-linked wallets held about 87% of USD1 supply at one point. Binance also ran multiple campaigns to seed liquidity. The flagship was a USD1 booster program offering up to 20% APR. That rate was later cut to 8% APR. Holders also got WLFI token airdrops. CoinGecko’s market page still shows Binance dominating the most active USD1 trading pairs. The bigger catalyst was structural. Reuters reported that Abu Dhabi’s MGX used USD1 to settle a $2 billion investment in Binance. That’s an institutional event no newly launched stablecoin usually gets.

The chain expansion happened fast. WLFI’s contract-address docs now list USD1 deployments across eleven networks. The list covers Ethereum, BNB Chain, Plume, AB Core, Monad, Mantle, Morph, XLayer, Solana, TRON, and Aptos. Cross-chain transfers run through Chainlink CCIP. Bridging support today spans nine of those chains. That breadth lets USD1 chase liquidity where users already are. A stablecoin that lives on one chain has to convince the rest of the market to come to it, that is not USD1. It just shows up.

USD1 BitGo is the institutional pipe. BitGo, not WLFI, issues, mints, and redeems the token. Institutional clients can mint and redeem through BitGo Mint. That gives USD1 immediate distribution into BitGo’s bank, exchange, asset-manager, and fintech base. The USD1 GENIUS Act alignment is the other half. Reuters confirmed the GENIUS Act became law in July 2025. The law created a federal stablecoin framework around liquid reserves and public disclosures. The March 2026 attestation shows reserves held in a segregated qualified trust at BitGo Bank & Trust, N.A. The mix is cash, cash equivalents, and government money market funds. It’s deliberately boring. In stablecoins, boring is what institutions want.

The USD1 vs USDC question is the one most readers actually want answered. The short version is that they’re not really fighting for the same dollar. USDC is the established compliance-first stablecoin. It’s issued by a US-based company. Its attestations are public and monthly. It carries the deepest CEX and DeFi integration of any non-USDT token.

USD1 is newer, more concentrated, and with a much smaller transparency track record. The reserve profile is similar in spirit. The disclosure cadence isn’t. So for a regulated institutional flow, USDC still wins on history. For tracking where the new growth is going, you can’t ignore USD1.

The duopoly remains the duopoly. USDT and USDC together hold about 82.9% of the market on DefiLlama. USDT alone sits at the top. Sky Dollar USDS now ranks third after the MakerDAO rebrand and its own growth run. The real contest is for the non-duopoly share. USD1 currently leads that pack. It’s ahead of USDe, DAI, and PYUSD on DefiLlama.

The DAI comparison is sharper. DAI is partially crypto-backed and historically less centralized in its control surface. USD1 sits at the other end. It’s fully fiat-reserved, fully centralized, and carries explicit freeze powers. Neither is a clean substitute for the other. They appeal to different stablecoin users with different priorities.

USDe is the other interesting comparison point. Ethena’s USDe is yield-bearing. It runs on a delta-neutral basis trade. That’s a different product category entirely. The USD1 stablecoin positions closer to “compliant fiat dollar on more chains,” not yield instrument. That clarity is part of why USD1 sits above USDe today. A treasury team holding USD1 isn’t running synthetic-dollar risk. It’s holding a fiat-backed token with a public attestation cadence.

USD1 vs USDC vs USDT vs DAI across the metrics that matter

A lot of USD1 supply still sits on exchanges. The fair question is whether the token is starting to do work outside that. As of mid-2026, the answer is yes, but unevenly. Some of the visible use is brand advertising. Some looks like infrastructure.

The UFC Freedom 250 fighter bonus is the most public example. World Liberty paid out a $250,000 bonus pool in USD1 on the White House lawn in June. CoinDesk cited Klaros Group’s Todd Phillips on the framing. He called the payout “economically similar to paying by cheque.” But its real value was as advertising. That reading is fair. It wasn’t transformative payment volume. It was a marketing event that put USD1 on every sports-news feed for a week.

The payment surface is broader than that one event. Oobit markets USD1 spending anywhere Visa is accepted. It includes Apple Pay and Google Pay support. World Liberty has separately discussed a debit-card pilot. Reuters has reported a World Swap foreign-exchange and remittance platform. World Swap is meant to connect users to debit cards and bank accounts at lower fees. That’s still early. It does show the token is being attached to spend rails, not just to exchange books.

The DeFi side is building too. BitGo’s USD1 page markets the token for payments, lending, borrowing, and trading. WLFI Markets docs describe supplied USD1 collateral securing borrowed positions. Eco’s explainer notes that USD1 now appears as a borrowable or supplied asset in selected lending markets. None of this is at the scale of USDC’s DeFi presence yet. But the direction of travel is more use cases, not fewer.

Tempo is the other thread worth flagging. BitGo expanded institutional wallet support for Tempo in April 2026. WLFI’s AgentPay docs reference a Tempo payment path. Eco reports that USD1 added a native Tempo deployment in May 2026. The USD1 stablecoin is being positioned as part of a broader payments stack. That stack spans cross-chain transfers, enterprise payment rails, and machine payments. None of these threads are mass-market today. All of them point in the same direction.

Every stablecoin gets one bad day eventually. USD1 had its first one on February 23, 2026. Reuters reported that the token briefly fell to about $0.994. WLFI described it as a coordinated attack. The peg recovered to around $0.9994 within hours. Some deviation is normal for stablecoins. USD1 returned to its historical trading range in the same session.

That isn’t a USDC-style 2023 bank-shock stress test. That episode involved a real funding question about reserves held at Silicon Valley Bank. The USD1 dip didn’t involve a balance-sheet question at all. It was a market-mechanics event. So the lesson is narrower than the USDC episode. The peg held. The market quickly absorbed the dip. The redemption gate wasn’t tested.

That last point is worth pausing on. A real stress test for USD1 would mean a wave of redemption requests routed through the eligible-BitGo-customer process. February didn’t produce that. Until something does, the redemption rail remains untested at scale. Spot peg behavior isn’t the same as redemption-side liquidity.

The honest caveat is broader. Peg stability isn’t the same as decentralization or censorship resistance. WLFI’s own risk disclosures say redemption is limited to eligible BitGo customers. Reserve liquidity could come under pressure in a redemption spike. BitGo or WLFI parties can block transfers or freeze addresses. For institutional users running compliance-sensitive flows, that’s a feature. For users who value the censorship-resistance property of a stablecoin, it’s a deal-breaker. February showed USD1 can handle a normal stress event. It didn’t tell you anything about the centralization concerns. Those are a separate question.

Src: Coingecko

From here, three forward catalysts will shape whether USD1 keeps gaining share or hits a ceiling. None is fully baked. Each is moving.

Reuters reported in January that WLTC Holdings applied to the OCC. The application is for a national trust charter to launch World Liberty Trust Company. The new entity would issue, redeem, and custody USD1 under a national trust-bank structure. The OCC’s current digital-asset licensing page still lists World Liberty Trust Company, N.A. as pending. The application was received on January 6, 2026. So the catalyst is real but not yet banked. If the charter goes through, issuance, custody, and conversion could sit inside a single federally supervised vehicle. That would reduce USD1’s dependence on third-party rails. If it doesn’t, USD1 keeps relying on the existing BitGo arrangement.

Reuters also reported that Pakistan signed an MoU with SC Financial Technologies. The firm is a World Liberty affiliate. The MoU is exploratory. It covers integrating USD1 into a regulated digital-payments structure for cross-border payments. The work would happen alongside the central bank. That doesn’t make Pakistan a guaranteed success case. It does push USD1 past the “speculative exchange instrument” framing. The token becomes a candidate settlement layer for emerging-market payment corridors. The total addressable market there is much larger than meme-driven retail flow.

This catalyst is the least covered and possibly the most asymmetric. WLFI’s docs describe AgentPay SDK as an open-source toolkit. It lets AI agents hold, move, and govern USD1 under policy. The use-case docs even show manual approval thresholds for larger USD1 transfers. Stablecoins now compete on programmability, not just on reserves. If agentic commerce becomes real over the next 12 to 24 months, the right issuer wins. That issuer combines multichain liquidity with spend controls and approval logic. It matters more than the issuer with the best marketing campaign. USD1 is positioning for that bet now.

Centralization is the biggest one. WLFI and BitGo retain the ability to block or freeze addresses. The redemption gate also runs through BitGo’s eligible-customer process. So you don’t redeem USD1 the way you redeem USDC. You hold it, use it, or sell it on a venue. That’s a real constraint for some user profiles.

Concentration is the second. The fact that Binance-linked wallets historically held around 87% of supply is a structural risk worth tracking. If that concentration falls as multichain distribution deepens, the float looks more like a normal stablecoin. If it doesn’t, USD1 stays exposed to single-venue dynamics.

Reserve disclosure cadence is the third. BitGo/Crowe attestations are useful but episodic, not real-time. A monthly attestation rhythm would close the trust gap further. A Chainlink Proof-of-Reserve feed would go even further. Until then, holders rely on quarterly snapshots and good faith between them.

Political risk doesn’t disappear because you ignore it. The USD1 stablecoin’s brand is permanently linked to World Liberty Financial. That cuts both ways. It accelerated distribution. It also creates a reputational vector. Institutional treasurers may or may not be comfortable with it, depending on the jurisdiction and the moment.

Regulatory risk is the fifth layer. The GENIUS Act provides a framework, but the rule-making process around stablecoins is still active. Future rule changes on reserves, audits, or issuer structure could affect how USD1 operates. The OCC charter application is one signal that WLFI is moving toward more direct federal supervision. The flip side is that the application could also be denied or delayed. Either outcome shapes the next phase.

USDT and USDC still own the top tier of the stablecoin market. That isn’t changing in the next twelve months. The more actionable fight is for the non-duopoly share. That’s where the USD1 stablecoin has been winning fastest. None of this erases concentration risk, redemption limits, or governance concerns. It also doesn’t change a key fact about the original distribution. Most of it came from a machine. That machine included Binance, BitGo, and a once-in-a-category settlement event.

Three things to watch. First, the OCC charter decision. Second, the next BitGo/Crowe attestation. Pay attention to whether the supply growth continues and whether Binance-wallet concentration falls. Third, whether AgentPay produces meaningful transaction volume, or stays a demo. None of these on their own decides USD1’s trajectory. Together, they tell you whether USD1 is consolidating its top-five slot or starting to push higher.

None of this is financial advice. Stablecoin holders should always understand the reserve composition, redemption mechanics, and control surface of any token they use, USD1 included. The takeaway is structural, not directional. USD1 isn’t a curiosity anymore. It’s a live contender in tier two of the stablecoin market. And it got there in a remarkably short window.

Are Exchange Tokens a Good Investment in 2026? CEX vs DEX

Zcash vs Monero vs Dash: Best Privacy Coin in 2026?

Helium Worked in America. Can Dabba Win India?

Where to Earn Yield on Stablecoin in 2026 (After the Yield Ban)

Are Exchange Tokens a Good Investment in 2026? CEX vs DEX

Zcash vs Monero vs Dash: Best Privacy Coin in 2026?

Helium Worked in America. Can Dabba Win India?

Where to Earn Yield on Stablecoin in 2026 (After the Yield Ban)