Discover the rise of yield-bearing stablecoins and the five key models driving crypto yield, from T-bills and DeFi to lending.

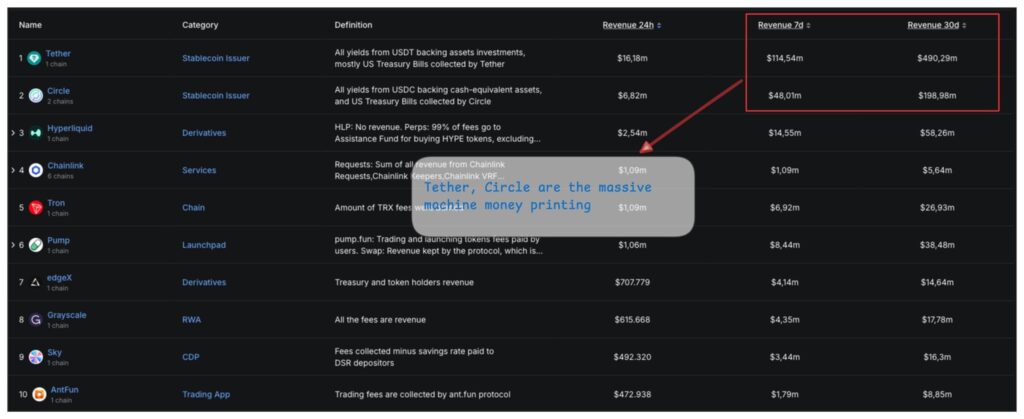

The rise of yield-bearing stablecoins has changed how many DeFi users think about idle capital. For years, I held USDT and USDC like most traders do. Meanwhile, Tether and Circle were quietly pocketing billions in reserve yield from T-bills while holders earned nothing.

Meanwhile, Tether and Circle were quietly pocketing $3–5 billion a year in reserve yield from T-bills. My dollars but their profit.

I always knew it, but the alternative didn’t exist at scale. So I accepted it.

Looking at the data now, I don’t think that era is coming back.

So I spent a day going deep on the Yield-Bearing Stablecoin (YBS) landscape – mapping every major model, the numbers behind each, and what actually breaks when market conditions shift.

Whether you’re a conservative capital allocator, a DeFi power user, or somewhere in between – there are things in here you probably didn’t know existed.

I’ll walk you through all five models with data, so you can allocate with conviction instead of guessing.

—

Let’s get into it.

—

For the better part of a decade, Circle and Tether held a near-monopoly on stablecoins, commanding 90–95% of the market. The business model was simple and brutally effective: take user dollars, invest them in short-term US T-bills, and keep the yield. Holders got nothing. The rise of yield-bearing stablecoins is challenging that model by returning a share of reserve income directly to users rather than issuers.

At $3–5B in annual reserve income, it was one of the most profitable models in crypto. And it worked because there was no real alternative – USDC and USDT had the liquidity, the integrations, and the trust. Switching costs were high.

That structural advantage is now being competed away.

Yield-Bearing Stablecoins flip the model: instead of the issuer retaining reserve income, the yield flows directly back to the holder – with comparable liquidity, no lock-up, and increasingly institutional-grade infrastructure behind it.

The question is no longer whether this model wins. The question is which engine you want exposure to.

—

The numbers already tell the story. YBS has found clear PMF:

Zoom in on just the last 6 months and the divergence becomes stark:

—

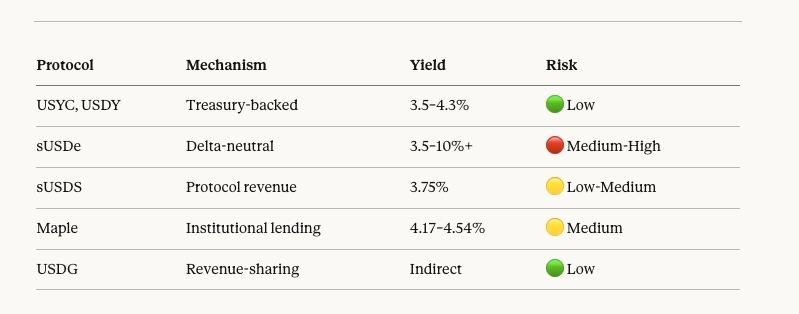

These numbers are just the surface. The rise of yield-bearing stablecoins is being driven by very different yield engines beneath the hood. Before you move capital, you need to understand which engine is producing that yield and, more importantly, what breaks when market conditions change.

There are 5 fundamentally different models running under the hood.

The simplest model: your dollar buys short-term US T-bills

—

You deposit crypto. Ethena opens an equal short futures position. Net market exposure = zero. Yield comes from three sources simultaneously:

The model is elegant. The risk is regime-dependent.

In a bull market, funding rates run hot and yields can hit 10%+. In a bear market, rates compress hard and the product’s value proposition narrows. We saw this directly: TVL dropped from $14.8B to $7.6B in two months when sentiment shifted in 2025. As the rise of yield-bearing stablecoins continues, this highlights an important reality: not all yield is created equal, and some models are far more sensitive to market regimes than others.

—

The OG model, running since 2017 as MakerDAO. Sky has been distributing yield to stablecoin holders longer than most DeFi protocols have existed.

Yield sources are diversified:

Mechanic: Deposit USDS -> receive sUSDS -> exchange rate rises as the protocol distributes revenue back to holders.

—

Maple deploys USDC and USDT into overcollateralized loans to vetted institutional borrowers, primarily trading firms and market makers. Yield is higher because you’re taking on credit exposure rather than market or protocol risk.

—

USDG takes a different approach. Reserve yield doesn’t flow to holders directly – it flows to network partners (exchanges and platforms), who then distribute it to users through their own reward structures.

The model is indirect, but the growth validates it: +170% in 6 months to .

The incentive alignment is clever: exchanges benefit from distributing a yield-bearing stablecoin, which keeps users on-platform and improves capital efficiency for both sides.

—

The era of holding zero-yield stablecoins because there’s no alternative is over. The infrastructure is here, the models are battle-tested, and the growth numbers confirm adoption isn’t slowing.

The only remaining question is which engine you trust with your capital and that depends on understanding what’s actually under the hood.