Pavel Durov is taking back TON six years after the SEC forced Telegram out. Inside the reversal arc, the MTONGA roadmap, and what comes next.

Author: Tanishq Bodh

In May 2020, Pavel Durov wrote a blog post announcing the death of the Telegram Open Network. The SEC had won. A federal judge in New York had blocked the distribution of Gram tokens worldwide. Telegram agreed to pay $18.5 million in penalties and return $1.22 billion to investors. The project Durov and his brother Nikolai had spent two years and $1.7 billion building was officially over.

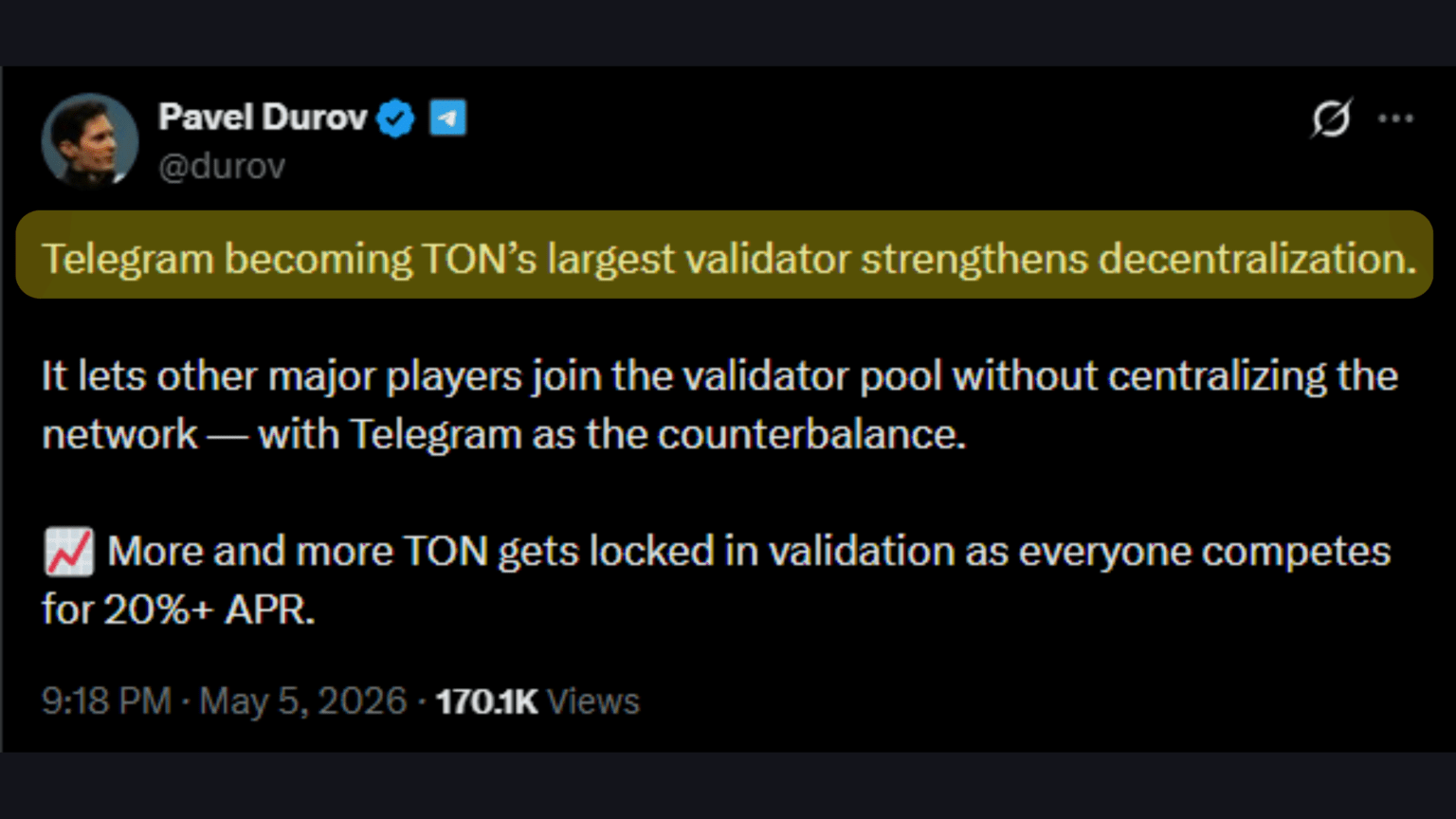

Six years later, on May 4, 2026, Durov posted on X that Telegram would replace the TON Foundation as the network’s primary driver and become its largest validator. The official ton.org now reads “ton.org is now controlled by MTONGA.” Toncoin jumped 30% in 24 hours. And the messaging app that was forced out of its own blockchain by US securities law walked back in through the front door.

This is not a routine governance shuffle. It is the closing of a six-year arc that started with one of the largest ICOs in crypto history, ran through a defining SEC enforcement action, survived as a community-led project for half a decade, and is now circling back to the founder who started it. The arc itself is the story, because what changes hands here is not just validator weight. It is the question of whether the SEC’s 2020 win actually killed Telegram’s blockchain ambitions, or just delayed them.

Telegram announced TON in 2017 with an ambition that read closer to a manifesto than a product roadmap. The Telegram Open Network was meant to be a sharded, scalable layer 1 capable of powering payments, decentralized storage, identity, and a broader services layer integrated directly into the messaging app. The native token was Gram, and Telegram intended to distribute 2.9 billion of them across an initial set of purchasers ahead of the network launch.

The fundraise itself was a record. Across two private rounds in early 2018, Telegram raised approximately $1.7 billion from 171 initial purchasers, including more than 1 billion Grams sold to 39 US-based investors. The structure was a Simple Agreement for Future Tokens, or SAFT, where accredited investors purchased rights to receive Grams once the network was operational. At the time, this was the second-largest token raise in history behind only EOS.

The thesis behind the TON model rested on a single assumption. Telegram believed that selling SAFTs to accredited investors qualified as an exempt private placement under Regulation D, and that the eventual delivery of Grams once the network was functional would not constitute a separate securities transaction. The legal theory mattered, because it underpinned the entire fundraising model that crypto projects had been using since 2017.

On October 11, 2019, weeks before Telegram planned to deliver Grams to initial purchasers, the SEC filed an emergency action in the Southern District of New York. The complaint argued that Telegram had conducted an unregistered public offering of securities, that Grams were investment contracts under the Howey test, and that the SAFT framework Telegram had relied on was an attempted workaround rather than a legitimate exemption.

The SEC’s argument was direct. The agency contended that the SAFT structure could not be analyzed in isolation. The initial sale to accredited investors and the eventual public distribution of Grams were part of one continuous scheme, designed to move tokens into secondary markets without registration. The court agreed.

On March 24, 2020, Judge P. Kevin Castel granted the SEC’s preliminary injunction. The decision held that Telegram’s SAFTs and the planned Gram distribution constituted a single integrated offering of securities, and that registration was required. The injunction blocked Telegram from distributing Grams not just in the United States but globally, on the reasoning that a US citizen might still access the network from anywhere in the world.

Telegram filed an appeal but ultimately settled. On June 11, 2020, the SEC announced that Telegram would pay an $18.5 million civil penalty, return $1.22 billion to initial purchasers, and submit any future digital asset issuance for SEC review for the next three years. Earlier, on May 12, Durov had published the blog post discontinuing the project, framing the decision as a forced surrender.

Durov’s exit statement was unusually pointed for a settlement context. He wrote that the US judge was right about one thing, that countries outside America remained dependent on the United States for finance and technology, and that this dependency stripped other nations of full sovereignty over what to allow on their own territory. The framing mattered, because it preserved a narrative thread Durov could return to later. Telegram did not abandon TON because the technology failed. Telegram abandoned TON because the regulatory environment forced it to.

The SEC injunction barred Telegram from distributing Grams. It did not bar anyone else from launching a similar network. Within weeks of Telegram’s exit, an independent group of developers picked up the codebase, renamed Gram to Toncoin, rechristened the Telegram Open Network as The Open Network, and quietly relaunched the chain. The TON Foundation, a Swiss-based nonprofit, emerged as the most prominent coordinating body in this new community structure.

Decentralization was not just a technical choice for the new TON. It was a legal shield. Under the Howey framework, a sufficiently decentralized network with no single promoter responsible for value generation falls outside the SEC’s enforcement perimeter. By distributing development across a community of independent builders, validators, and an arms-length foundation, the new TON could operate in ways the original project never could.

For the first three years, TON functioned as a small layer 1 with limited adoption. The shift came in 2023 and 2024, when Telegram began rebuilding its connection to the network through product integrations rather than direct ownership. Toncoin became the payment rail for Telegram Premium subscriptions, advertising, and creator monetization. The wallet feature inside Telegram was rebuilt around TON. Mini Apps, Telegram’s in-chat application layer, were architected to use TON as the underlying blockchain.

By January 2025, TON Foundation announced that TON would become the exclusive blockchain infrastructure for Telegram’s Mini App ecosystem, an environment supporting more than 950 million monthly active users. Toncoin became the only cryptocurrency accepted for non-fiat payments across Telegram Stars, Premium, Ads, and Gateway. The integration was deep enough that, in practical terms, TON had become Telegram’s blockchain in everything but name. Reported holder counts climbed from 2.9 million to 32 million over the past year alone.

This is the structural setup that made the May 2026 announcement possible. The Foundation had spent five years building a chain that was technically independent but operationally inseparable from Telegram. What Durov did on May 4 was not a hostile takeover. It was the formalization of a relationship that already existed.

Durov did not announce the validator takeover in isolation. It arrived as the third visible step in a roadmap he has been calling MTONGA, short for “Make TON Great Again,” a seven-step plan focused on technical superiority and product integration. Each step has landed publicly with measurable network effects.

The sequencing matters. Durov did not start with the validator takeover. He started with the technical case. Catchain 2.0 reduced confirmation times by an order of magnitude, which made TON viable as the settlement layer for Telegram’s high-frequency consumer activity. The fee cut on May 1 made micropayments economically viable. By the time Durov posted the validator announcement on May 4, the technical foundation for “tech superiority” was already in place. The takeover was the operational consequence of upgrades that had already shipped.

Validators on TON produce blocks, verify transactions, and earn staking rewards proportional to their stake. The largest validator does not control the network outright. Block production is still distributed across the validator set, and consensus requires participation from multiple parties. But the largest validator carries the largest weight in governance votes, has the most influence over network parameters, and earns the largest share of validation rewards.

In practical terms, Telegram becoming the largest validator means three things. First, the company captures a meaningful share of TON’s annual issuance through staking rewards. Second, it gains the loudest single voice in any future governance question, including the upcoming June 2026 inflation vote. Third, it formalizes Telegram’s responsibility for network uptime and security, which previously sat informally with the TON Foundation and a distributed set of community validators.

Toncoin’s response to the announcement was immediate and clean. The token climbed from roughly $1.35 to $1.80 within 24 hours, a move of approximately 30%, and re-entered the top 20 cryptocurrencies by market capitalization during the rally. By the time the dust settled on May 5, TON was trading at $1.806.

The on-chain follow-through carried more signal than the price move alone. According to Token Terminal data, TON closed April with roughly 67 million transactions, the network’s strongest monthly performance of 2026 so far. Following Durov’s post, the staking ratio jumped 18.36% in a single day, and net staking inflows hit $191.83 million, the largest single-day staking inflow in nearly four months. Capital was not just buying the token. It was locking it up.

The combination of price action, transaction volume, and staking flows points to a coordinated thesis among holders. Lower fees mean more on-chain activity. More activity means more validation rewards. A larger validator stake from Telegram compresses the available rewards pool for smaller validators, but it also signals long-term commitment from the network’s most strategically important counterparty. Holders are pricing in execution.

The reversal arc closes one chapter but opens several others. None of these questions have settled answers, and each one will shape how the next phase of TON plays out.

Before the announcement, the TON Foundation had been pursuing a $400 million treasury raise through a Kingsway Capital-led PIPE structure. The transaction was framed as a long-term capitalization vehicle for the Foundation’s operations and ecosystem grants. Durov’s announcement did not address what happens to this initiative under the new arrangement, and the Foundation has not publicly clarified its status. If the PIPE proceeds, the Foundation retains an independent treasury that could fund operations parallel to Telegram’s validator role. If it does not, the Foundation’s ongoing relevance becomes a more open question.

Catchain 2.0’s faster block production created a side effect. Annual inflation projections jumped from approximately 0.6% to roughly 3.6%, because more blocks per year means more block rewards distributed per year. Validators are scheduled to vote in June 2026 on reducing block rewards to stabilize issuance. Proposed changes include cutting masterchain rewards from 1.7 TON to 0.35 TON per block, and main network rewards from 1 TON to 0.2 TON per block. As the largest validator, Telegram will hold the largest single voting weight in this decision, which makes the vote a meaningful early test of how the new governance arrangement actually functions.

The strongest critique of the announcement is structural. A 950-million-user platform becoming the largest validator on its own blockchain compresses the distinction between application layer and infrastructure layer in a way that few crypto networks have attempted. Supporters argue this is exactly what TON needs to deliver on its consumer thesis. Critics argue it reintroduces the single-point-of-failure problem that decentralization was meant to solve. The legal angle is also worth flagging. The SEC’s 2020 case rested partly on the argument that Telegram was the central promoter of TON’s value. By formally taking the largest validator seat in 2026, Telegram is, in some readings, walking back into that exact position, just under different regulatory conditions.

The current US regulatory environment is materially different from the one Telegram faced in 2020. The Biden-era SEC’s aggressive enforcement posture has softened under the current administration, and the broader policy direction has shifted toward clearer rules for digital assets rather than enforcement-driven precedent. Whether that holds, and whether it holds specifically for a chain whose original founder is now operationally back in control, is unproven. Durov’s three-year notice obligation to the SEC from the 2020 settlement has long since expired. But the underlying questions about who controls value generation on TON have not gone away. They have just been answered differently.

The TON reversal arc has implications beyond a single chain. Three points stand out.

First, the case demonstrates that SEC enforcement actions do not necessarily kill projects. They redirect them. Telegram lost its case in 2020 and abandoned the network. The network survived through community ownership, rebuilt distribution through Telegram product integrations, and ultimately returned operational control to its original founder. The five-year detour was costly, but it was not terminal. Other projects working through unresolved enforcement questions will read this carefully.

Second, the integration of a 950-million-user consumer app with a single chain creates a different kind of competitive moat than the typical layer 1 thesis. Most chains compete on technical performance, developer experience, or capital incentives. TON’s moat is distribution. The validator takeover deepens that moat, because Telegram now has direct control over how the chain evolves to serve its product roadmap.

Third, the centralization question is no longer hypothetical for major chains. TON’s structure makes the tradeoff explicit. Other large networks have similar dynamics in practice but rarely formalize them. Whether TON’s approach becomes a model or a cautionary tale depends on what gets shipped over the next 12 to 18 months and how the network handles its first real governance stress test.

In May 2020, Pavel Durov wished luck to all those striving for decentralization, balance, and equality in the world. The post read like a farewell. It was not.

Six years later, the network Telegram was forced to abandon has 32 million holders, 67 million monthly transactions, integration with 950 million users, sub-second finality, near-zero fees, and a founder who just took back operational control. The SEC won the 2020 case. The network won the longer game.

What happens next depends on execution. Durov has promised new dev tools, a redesigned ton.org, and further performance upgrades within two to three weeks. The June inflation vote will test the new governance model. The fate of the Foundation’s PIPE will signal whether the old structure retains independent leverage or quietly winds down. And the centralization question will keep producing critics and defenders for as long as the chain matters.

But the arc itself is finished. Telegram built TON, lost TON, watched TON survive without it, and walked back in to lead it again. Few stories in crypto have closed loops this clean, and fewer still have done it at this scale.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.