Compare every Solana ETF by fees, staking rewards, and AUM. See how BSOL, SOEZ, and GSOL stack up, and whether an ETF or direct SOL is right for you.

Author: Chirag Sharma

The crypto ETF story did not stop with Bitcoin and Ethereum. In 2025, a new chapter opened when Solana ETFs began trading in the United States, giving traditional investors direct exposure to one of the fastest-growing blockchain ecosystems. As of March 2026, spot Solana ETFs have been trading for nearly five months across major U.S. exchanges. These funds allow investors to gain exposure to Solana (SOL) through ordinary brokerage accounts, retirement portfolios, and institutional investment platforms.

The response has been stronger than many expected. Despite SOL trading significantly below its peak levels around the time the first funds launched, Solana ETFs have still accumulated roughly $1.5 billion in cumulative inflows. Multiple issuers now offer competing products, including funds from VanEck, Fidelity Investments, Bitwise Asset Management, Franklin Templeton, Grayscale Investments, 21Shares, and others.

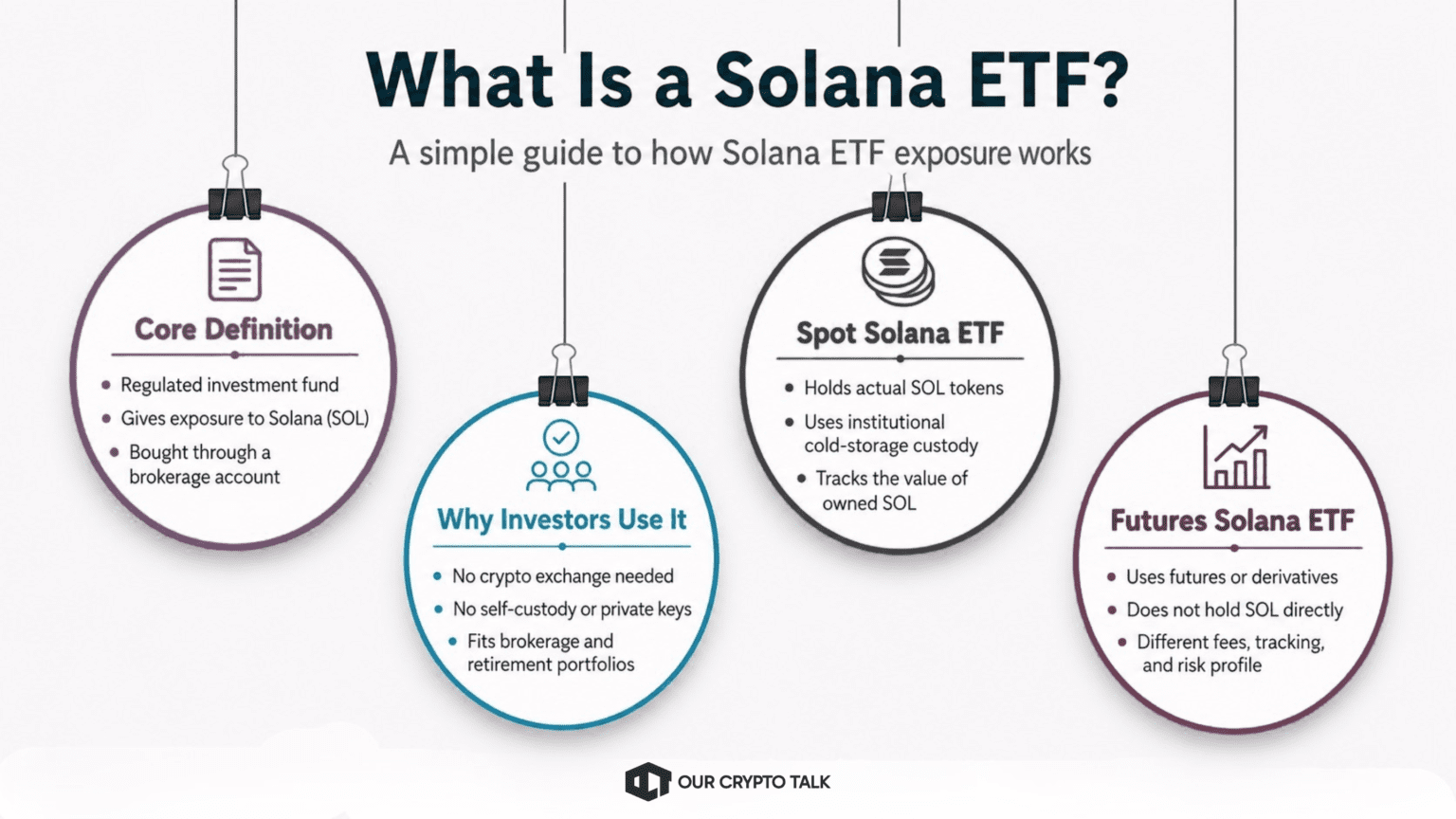

A Solana ETF is a regulated investment fund that gives investors exposure to Solana (SOL) through a normal brokerage account instead of a crypto exchange or self-custody wallet. Investors buy ETF shares on a stock exchange, and those shares are designed to track the fund’s net asset value (NAV), which reflects the value of the SOL or Solana-linked assets the fund holds.

A spot Solana ETF holds actual SOL tokens in institutional custody, usually through regulated custodians that secure the assets in cold storage. A futures-based Solana ETF, by contrast, does not need to hold SOL directly. It tracks Solana’s price through futures contracts or other derivatives tied to SOL. In plain English: a spot ETF owns the asset, while a futures ETF owns contracts that reference the asset’s price. For investors, both can provide Solana exposure, but fees, tracking accuracy, custody structure, and risk profile can differ.

Solana ETFs are now available in the U.S., with the market moving from regulatory filings to live exchange-traded products in 2025. The first major step came when REX-Osprey launched SSK, a Solana + staking ETF, on July 2, 2025, giving U.S. brokerage investors early access to SOL exposure with staking rewards through a 1940 Act ETF structure.

The bigger spot ETF breakthrough came on October 28, 2025, when Bitwise launched the Bitwise Solana Staking ETF (BSOL) on NYSE Arca. Reuters reported that BSOL was the first U.S. spot Solana ETF, launched during the SEC shutdown after Bitwise used the newer regulatory pathway created by generic crypto ETF listing standards.

The launch opened the door for more U.S. Solana ETF products. Grayscale’s Solana vehicle followed by converting into the Grayscale Solana Staking ETF (GSOL), with ongoing share creation and redemption beginning on October 29, 2025.

The U.S. Solana ETF market now has two main product groups: spot Solana ETFs that aim to track SOL directly, and alternative Solana exposure products, including REX-Osprey’s staking-focused 1940 Act ETF and futures or leveraged products. For most investors, the main comparison comes down to fee, staking treatment, issuer credibility, liquidity, and tracking accuracy.

Solana ETF list: tickers, issuers, fees and staking

The lowest-fee Solana ETFs are currently clustered between 0.19% and 0.25%, which means issuers are already competing aggressively on cost. Franklin Templeton’s SOEZ has the lowest listed base fee at 0.19%, followed by Bitwise’s BSOL at 0.20%, 21Shares’ TSOL at 0.21%, and Invesco Galaxy’s QSOL and Fidelity’s FSOL at 0.25%. NerdWallet’s Solana ETF fee table also notes that some issuers are using temporary fee waivers, including SOEZ’s waiver until May 31, 2026, or the first $5 billion in assets.

Fee waivers matter, but investors should not treat them as permanent. A Solana ETF with a 0% promotional fee can become more expensive once the waiver expires, while a slightly higher-fee product may still be more attractive if it has deeper liquidity, tighter spreads, better staking mechanics, or stronger tracking. VanEck, for example, waived VSOL’s sponsor fee at launch until February 17, 2026, or until the fund reached $1 billion in assets, after which the normal 0.30% sponsor fee applies.

For long-term investors, the cleanest comparison is not just headline fee vs headline fee. The better test is net cost after waivers, trading spreads, tracking error, staking treatment, and fund liquidity. A low-fee ETF can still deliver weaker results if it trades with wide spreads or fails to track SOL closely.

Featured snippet: Solana ETF comparison table

Staking is the main feature that separates Solana ETFs from earlier Bitcoin ETF products. Because Solana runs on proof of stake, an ETF that holds SOL can potentially delegate some or all of its tokens to validators and earn protocol rewards. BSOL, VSOL, GSOL, SOLC, and REX-Osprey’s SSK are the most relevant products to watch for staking exposure, while other Solana ETFs may focus more on plain spot-price tracking.

BSOL is the clearest staking-first product. Bitwise says the fund targets 100% of assets staked, with 100% currently staked as of May 10, 2026. It also listed a 6.53% gross staking reward rate and 6.13% net staking reward rate, while making clear that rewards can change and are not guaranteed.

VSOL also includes staking mechanics. VanEck says staking rewards are not paid as a separate shareholder distribution. Instead, any staking rewards or losses affect the fund’s NAV and performance. That distinction matters because investors should not expect staking rewards to work like a fixed dividend or bond coupon.

GSOL is another staking-enabled product. Grayscale describes the fund as giving investors Solana exposure with potential staking rewards and notes that Solana staking rewards have historically averaged 6% to 8% per year. However, historical staking yields do not guarantee future returns, and ETF-level fees, validator performance, liquidity needs, and market-price discounts or premiums can all affect shareholder outcomes.

In plain English, staking rewards usually flow through the ETF structure by increasing the fund’s SOL holdings or improving NAV, not by giving every shareholder a separate staking payout. The final result depends on the fund’s prospectus, validator setup, expenses, and reward-sharing policy. Yield is not guaranteed because Solana reward rates fluctuate, validators can underperform, staking can create liquidity constraints, and SOL price volatility can easily outweigh staking income.

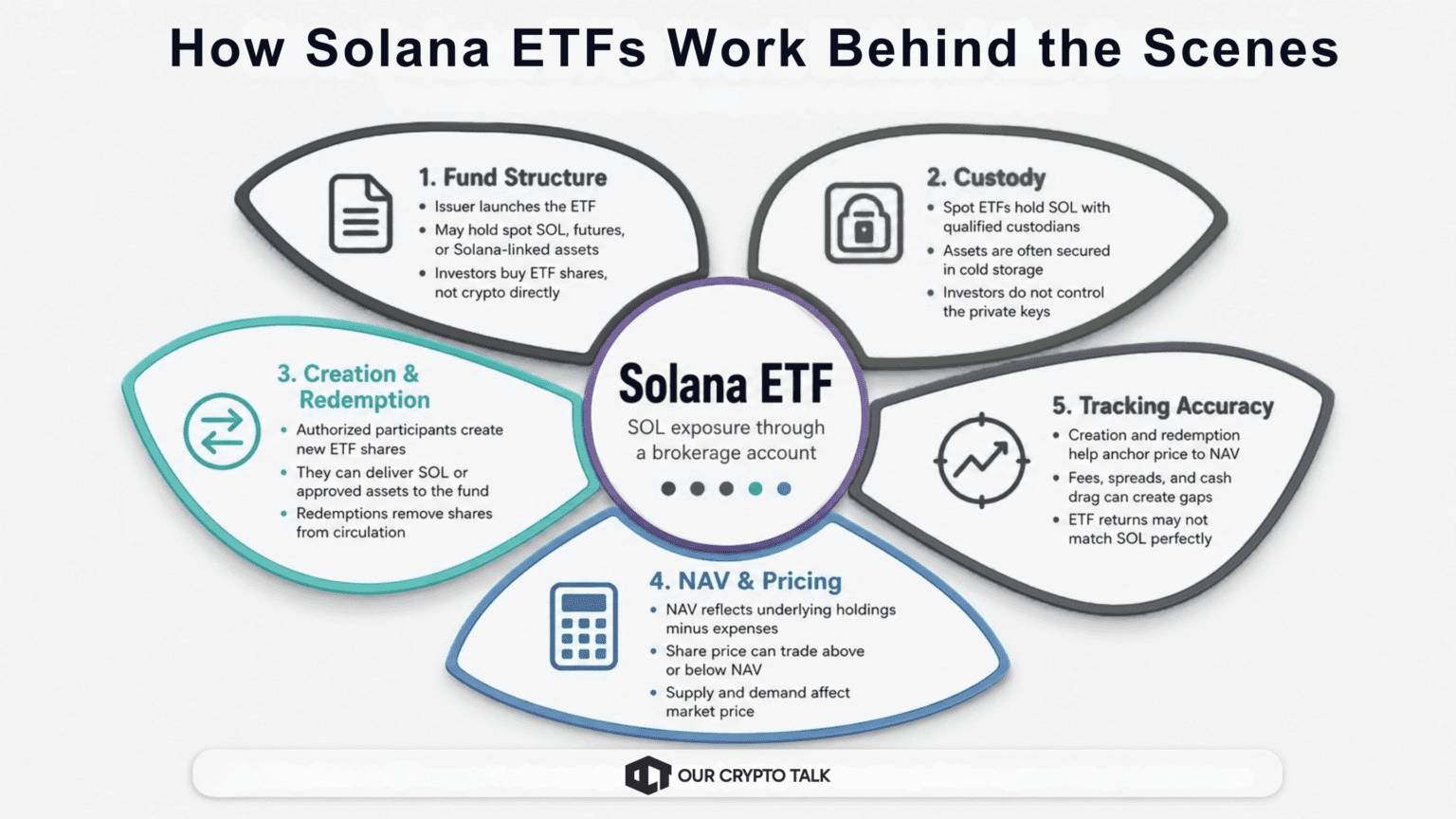

A Solana ETF turns SOL exposure into a stock-market product. The fund holds SOL, Solana futures, or a mix of Solana-linked assets, then issues ETF shares that trade through normal brokerage accounts. Behind the ticker, the key mechanics are custody, NAV calculation, creation and redemption, market pricing, and tracking accuracy.

A Solana ETF and direct SOL ownership both give investors exposure to Solana, but they are not the same trade. A Solana ETF is cleaner for brokerage users, advisors, and retirement-account investors who want regulated access without managing wallets. Buying SOL directly gives crypto-native users more control, including self-custody, direct staking, DeFi access, and full on-chain utility.

Solana ETF vs buying SOL directly

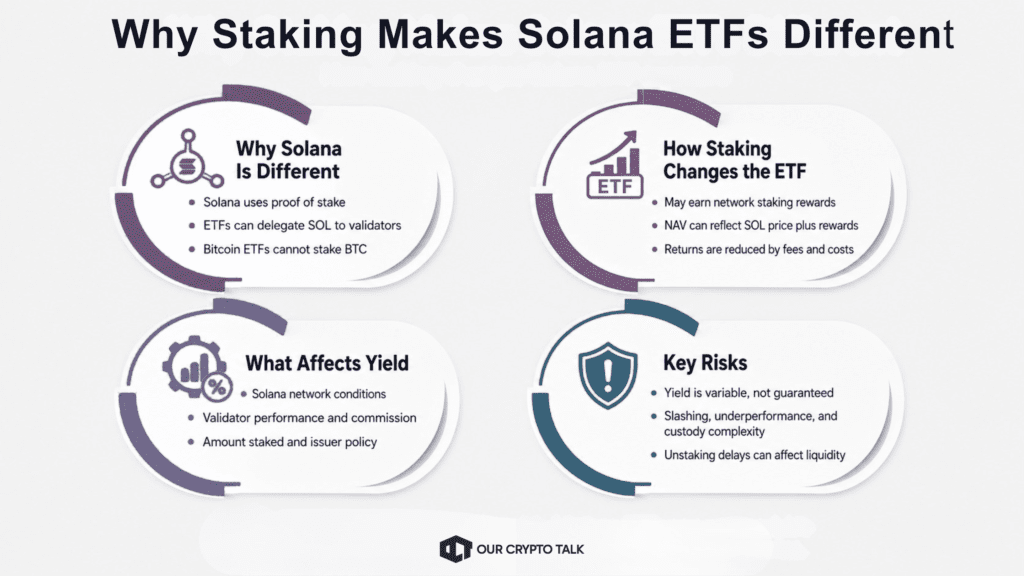

Staking makes Solana ETFs different because Solana is a proof-of-stake network, while Bitcoin is not. A Bitcoin ETF can only hold BTC and track its price because Bitcoin has no native staking system. A Solana ETF, by contrast, can potentially delegate some or all of its SOL to validators, help secure the network, and earn protocol rewards. VanEck says its VSOL trust delegates a portion of its SOL to help secure Solana and earn staking rewards, while staking levels may vary over time depending on fund operations.

That changes the ETF structure. A staking-enabled Solana ETF is not just tracking SOL’s spot price. It may also reflect staking rewards, validator performance, fund-level expenses, custody costs, and liquidity needs. VanEck’s S-1 says its trust seeks to reflect the price performance of SOL and rewards from staking a portion of the trust’s SOL, minus operating expenses, when the sponsor determines staking can be done without undue legal or regulatory risk.

For investors, the key point is that staking yield is variable, not guaranteed. Rewards can change based on Solana network conditions, validator performance, commission rates, the amount of SOL staked, and issuer policy. Staking can also introduce operational risks, including validator underperformance, slashing or penalty risk, custody complexity, and unstaking delays if the fund needs liquidity for redemptions. Any staking benefit usually flows through the ETF’s NAV and performance, not as a fixed dividend-style payout.

A Solana ETF differs from a Bitcoin ETF because Solana uses proof of stake. A staking-enabled Solana ETF can delegate SOL to validators, earn variable network rewards, and reflect those rewards in NAV after fees. Yield is not guaranteed because validator performance, slashing risk, unstaking delays, custody costs, and fund expenses can affect returns.

Solana ETF demand should be measured through flows, AUM, volume, and product concentration, not just issuer announcements. It had accumulated roughly $1.5 billion in cumulative inflows by March 2026, even as SOL traded far below peak levels.

The first clear institutional signal came from Bitwise’s BSOL launch. Bitwise said BSOL began trading on October 28, 2025, with a 0.20% management fee and a temporary 0% fee on the first $1 billion in assets for the first three months. Reuters later reported that BSOL attracted $420 million in its first week, giving Bitwise a first-mover advantage in the U.S. spot Solana ETF market during the SEC shutdown period. CoinDesk reported that BSOL saw $55.4 million in first-day volume and $217.2 million in AUM after launch, while other market reports put first-day inflows near $69.5 million.

That launch changed the Solana ETF race from a filing story into a live asset-gathering story. Once BSOL proved that brokerage investors would buy spot SOL exposure with staking mechanics, other issuers had to compete on fees, staking policy, liquidity, and distribution access.

Solana ETF inflows can support SOL price by increasing regulated demand for the asset. When spot Solana ETFs receive new money, issuers or authorized participants may need to acquire more SOL or allocate more exposure to SOL-linked holdings, depending on the fund structure. That can tighten available supply, deepen institutional liquidity, and strengthen the market’s perception of Solana as an investable asset.

However, ETF inflows do not guarantee price appreciation. SOL can still fall if broader crypto liquidity weakens, leverage unwinds, macro conditions turn risk-off, or traders sell into ETF-driven demand. The better way to frame inflows is this: strong ETF demand can create a structural bid for SOL, but it does not override market cycles, token volatility, derivatives positioning, or network-specific risks.

Flat or negative Solana ETF flows would not automatically mean the Solana thesis is broken. However, they would signal that institutional demand is becoming more cautious. If inflows slow after a strong launch period, it may show that wealth managers, advisors, and ETF buyers are waiting for clearer SOL price momentum, stronger market conditions, or more proof that staking-enabled ETFs can deliver consistent net benefits after fees.

Persistent outflows would be more serious. They could suggest that investors are reducing altcoin exposure, rotating back into Bitcoin or Ethereum ETFs, reacting to Solana network-risk concerns, or losing confidence in the ETF’s tracking, liquidity, or staking economics. A single weak week is noise. Several weak months would be a trend.

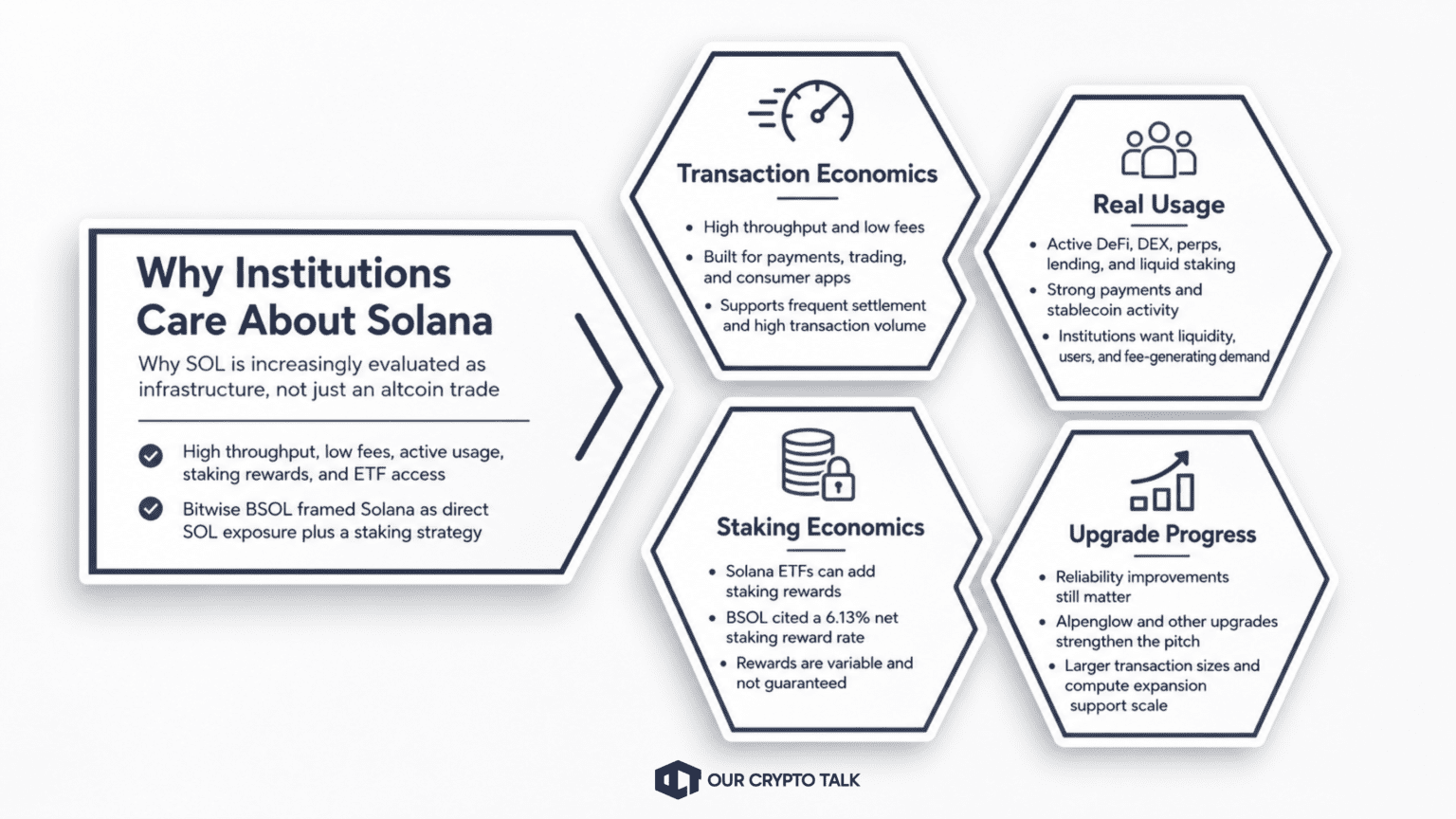

Institutions care about Solana because it offers a rare mix of high throughput, low fees, active on-chain usage, staking rewards, and improving market access through ETFs. That combination makes Solana easier to evaluate as infrastructure, not just as an altcoin trade.

Bitwise made this thesis explicit when it launched BSOL, describing the fund as the first U.S. ETP with 100% direct SOL exposure plus a staking strategy designed to capture Solana’s average staking rewards. Bitwise also highlighted Solana’s role as a fast, low-cost network with real application demand, which gives institutions a clearer reason to underwrite SOL exposure beyond short-term price momentum.

The first institutional draw is transaction economics. Solana is built for low-cost, high-volume activity, which matters for payments, trading, consumer apps, stablecoins, and tokenized assets. Unlike networks where high gas fees can price out smaller transfers, Solana’s design supports frequent settlement and high transaction counts.

The second draw is real usage across DeFi and payments. Institutions do not only want a chain with a fast narrative. They want liquidity, users, applications, and fee-generating activity. Solana’s DeFi stack now supports DEX trading, perpetuals, lending, liquid staking, payments, and stablecoin settlement.

The third draw is staking economics. Bitcoin ETFs are price-only products because Bitcoin has no native staking yield. Solana ETFs can add another layer by staking SOL through validator delegation. Bitwise’s BSOL page lists a 6.13% net staking reward rate, with 100% of assets currently staked as of May 10, 2026, while warning that rewards can change and are not guaranteed.

The fourth draw is network upgrade progress. Solana’s institutional pitch still carries a reliability discount because of its earlier outage history. That is why upgrades such as Alpenglow, larger transaction sizes, compute-unit expansion, and other network-level improvements matter.

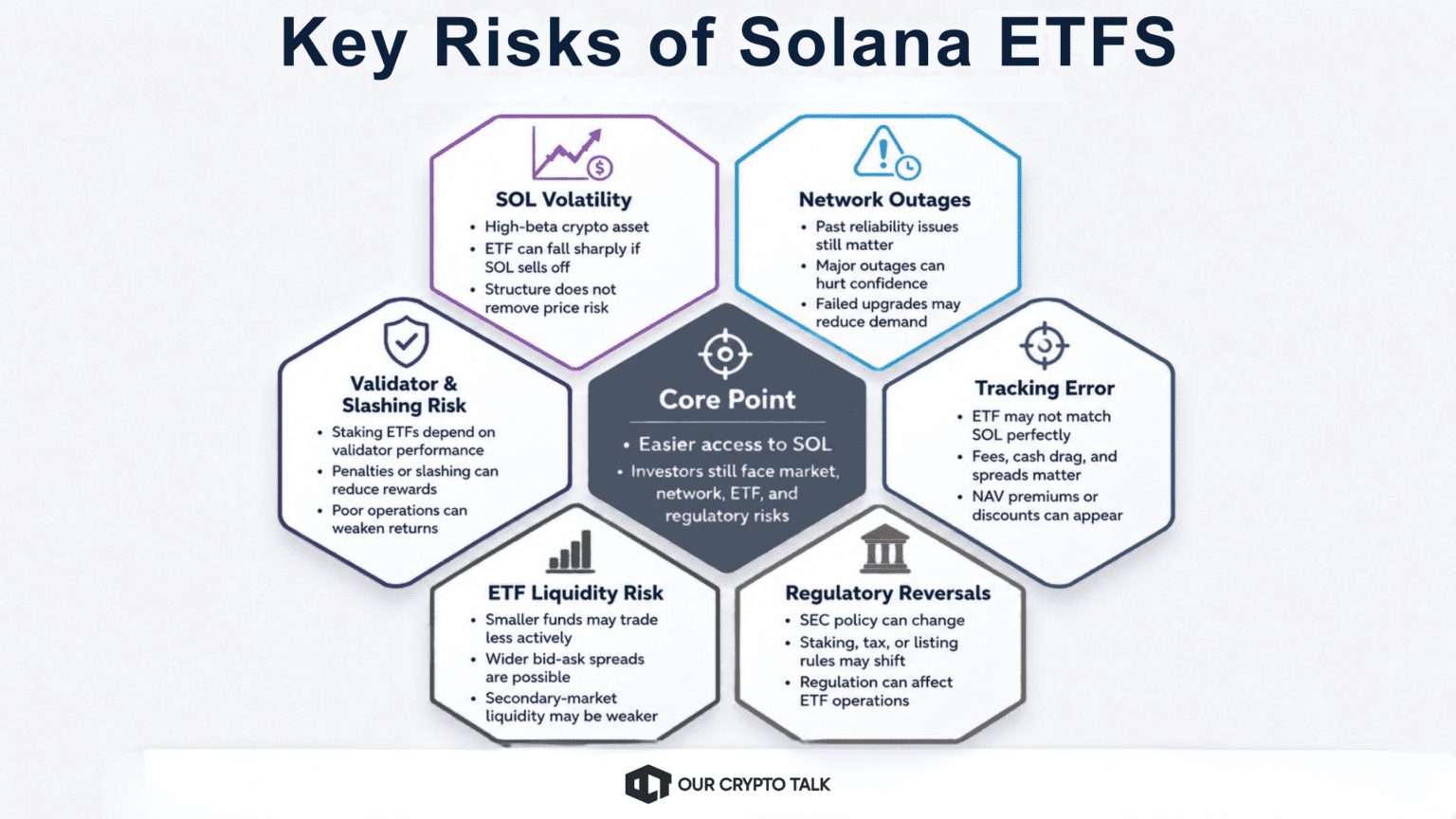

Solana ETFs make SOL easier to buy through traditional brokerage accounts, but they do not remove the core risks of the underlying asset. Investors still face SOL volatility, network reliability concerns, staking execution risk, ETF tracking gaps, regulatory uncertainty, and product-level liquidity risk.

The key point for readers: a Solana ETF reduces custody friction, not investment risk. It removes the need to manage wallets and private keys, but investors still take exposure to SOL’s price swings, Solana’s network execution, ETF structure, issuer operations, and regulatory decisions.

A Solana ETF is best suited for investors who want SOL exposure inside a traditional investment account without managing wallets, seed phrases, exchanges, or direct staking. It is less useful for users who want full on-chain control, DeFi access, or 24/7 crypto-native execution.

This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making investment decisions.