Hyperliquid processes $200B+ monthly with 70% DEX perp open interest. Explore the rise of Hyperliquid built by 11 people with zero VC funding.

Author: Tanishq Bodh

In 2010, crypto trading started on a website originally built for Magic: The Gathering cards. By 2014, 850,000 Bitcoin had vanished from that same platform. In 2022, FTX collapsed and took $8 billion in customer funds with it. Each era of centralized crypto trading solved real problems while creating catastrophic new ones. Then Hyperliquid changed everything.

In 2026, the most dominant derivatives exchange in crypto processes over $200 billion in monthly volume, holds 70%+ of all decentralized perpetual open interest, and generates roughly $700 million in annualized revenue. It was built by 11 people who never took a single dollar from venture capitalists. The rise of Hyperliquid is not just the story of one exchange. It is the story of how crypto trading evolved across four distinct eras, each one correcting the failures of the last, and how a physics Olympiad gold medalist from Palo Alto decided to build the thing everyone else said was impossible.

This article traces that full arc. From the early exchange era through the collapse of FTX, into the architecture and numbers behind Hyperliquid, and forward into what its roadmap means for the future of on-chain financial infrastructure.

Every generation of crypto exchange solved a real problem. Every single one also created a new one. Understanding this cycle is essential to understanding why Hyperliquid matters as much as it does.

Jed McCaleb launched Mt. Gox in 2010 as a marketplace for Magic: The Gathering cards, then pivoted it to Bitcoin and sold it to Mark Karpeles. Within three years, it handled roughly 70% of all BTC transactions on the planet. Then 850,000 Bitcoin vanished.

Mt. Gox proved that the demand for crypto trading was real, massive, and global. It also proved that centralized custody without accountability is a time bomb. The lesson was brutal but clear: holding user funds without transparent systems creates a single point of catastrophic failure.

Brian Armstrong took the opposite approach. Regulated, compliant, user-friendly. Coinbase became the first crypto exchange your parents could use without panicking. It eventually IPO’d at an $86 billion valuation and remains one of the most recognized brands in the industry.

However, Coinbase was always more bank than exchange and more compliance layer than trading infrastructure. It was crypto telling Wall Street “we can play by your rules.” The trade-off was performance, global access, and the aggressive innovation the space demanded.

CZ flipped the script entirely. Aggressive listings, razor-thin fees, the BNB utility loop, no fixed headquarters, and global by default. Binance became the undisputed volume king, processing more daily trades than most traditional stock exchanges combined.

Yet Binance also became the biggest regulatory target in the industry. A DOJ settlement followed, and CZ stepped down as CEO. Binance was crypto saying “we don’t need TradFi rules.” Regulators eventually disagreed.

Sam Bankman-Fried attempted to have it all. The institutional-grade interface, the celebrity endorsements, the stadium naming rights, the political donations, the $32 billion valuation. FTX looked like the future of crypto finance. Then $8 billion in customer funds disappeared overnight.

FTX was not an anomaly. It was the logical conclusion of a structural flaw that plagued every era of centralized crypto trading: someone controls the keys, and eventually, someone abuses that trust. After FTX collapsed, the question changed. It was no longer whether decentralized trading could compete. It was whether anyone could actually build a DEX that matched CEX performance.

Post-FTX, decentralized exchanges had their shot. But the infrastructure was not ready.

dYdX was constrained by StarkEx. GMX was innovative but bottlenecked by Arbitrum’s throughput. Uniswap dominated spot trading but lacked the architecture for perpetual derivatives. The tools existed in fragments. Nobody had assembled them into a single, purpose-built machine that could rival Binance on speed, depth, and UX while keeping everything on-chain and self-custodial.

That gap persisted until 11 people decided to build one from scratch.

The founder behind the rise of Hyperliquid is almost comically different from the man whose collapse inspired it.

Jeff Yan grew up in Palo Alto. He won a gold medal representing the United States at the 2013 International Physics Olympiad, graduated from Harvard with degrees in mathematics and computer science. He joined Hudson River Trading, one of the most elite high-frequency trading firms in the world, with a brief stint at Google after that.

In early 2020, he pivoted to crypto by founding Chameleon Trading, a market-making firm that quickly became one of the largest on centralized exchanges. He saw the inefficiencies firsthand. Then FTX collapsed and everything changed.

Yan made a decision that defied every convention in crypto. He would build a decentralized exchange from scratch. Not on Ethereum, Not on Arbitrum. Not on any existing chain. He would build the entire blockchain himself and fund it entirely from Chameleon Trading’s profits. Zero dollars from venture capitalists.

He viewed VCs holding large token allocations as a permanent “scar on the network.” Fortune profiled him as the anti-SBF, and the comparison writes itself. Both quant traders. Both saw the same market. One chose fraud, celebrity endorsements, and a $135 million stadium deal. The other chose to build quietly with 11 people and no marketing department.

His X handle is @chameleon_jeff because he genuinely finds chameleons fascinating. He barely tweets. In 2023, he launched Hyperliquid with zero press releases, zero KOL partnerships, and zero billboards.

The core insight behind Hyperliquid was deceptively simple: no existing blockchain was built for high-frequency trading. Every previous DEX was constrained by the chain it sat on. Yan’s team eliminated that constraint by building a custom Layer 1 from the ground up.

HyperCore is the native L1 trading engine powering Hyperliquid. It runs a fully on-chain central limit order book and achieves roughly 200,000 transactions per second through a proprietary consensus mechanism called HyperBFT, which was inspired by HotStuff and built in Rust. Sub-second finality clocks in at approximately 0.2-second median latency. Gas fees are zero.

HyperEVM sits on top of HyperCore as an Ethereum-compatible layer, allowing Solidity developers to build natively on Hyperliquid infrastructure. Lending protocols, CDP platforms, automated vaults, and structured products all compose directly with the trading engine’s liquidity. Since February 2025, more than 175 teams have deployed on HyperEVM.

The practical effect is that Hyperliquid feels like Binance. Deep order book, fast execution, clean interface. But every trade settles on-chain. Users custody their own assets. No intermediary holds funds, no opaque backend exists, and no one can freeze withdrawals or disappear with deposits.

Hyperliquid is what happens when someone with real quant experience builds the exchange they wished existed, rather than the one that raises the most money.

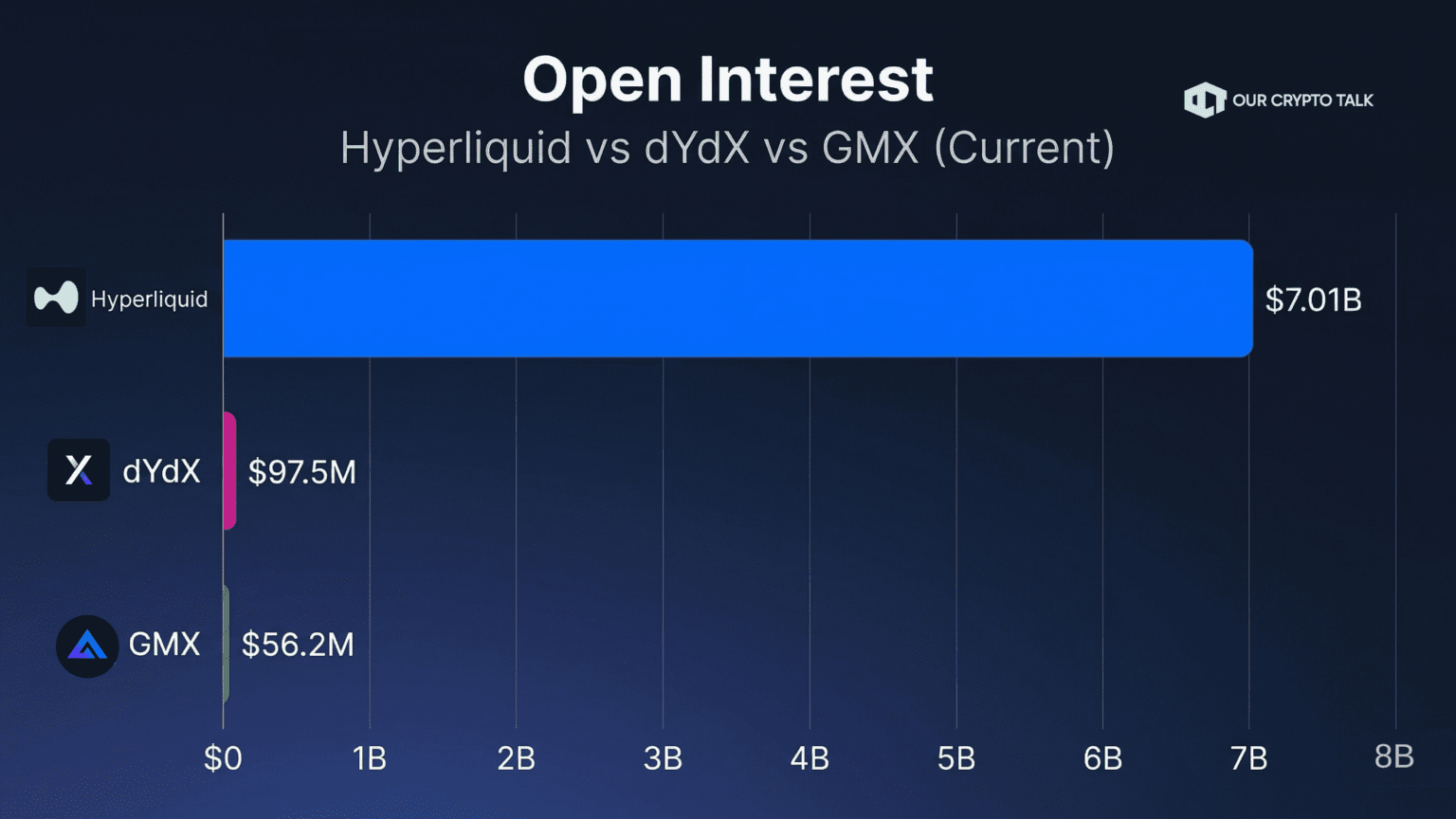

The data behind Hyperliquid does not need embellishment. In 2025, Hyperliquid processed $2.6 trillion in trading volume. For comparison, Coinbase did $1.4 trillion in the same period, nearly half.

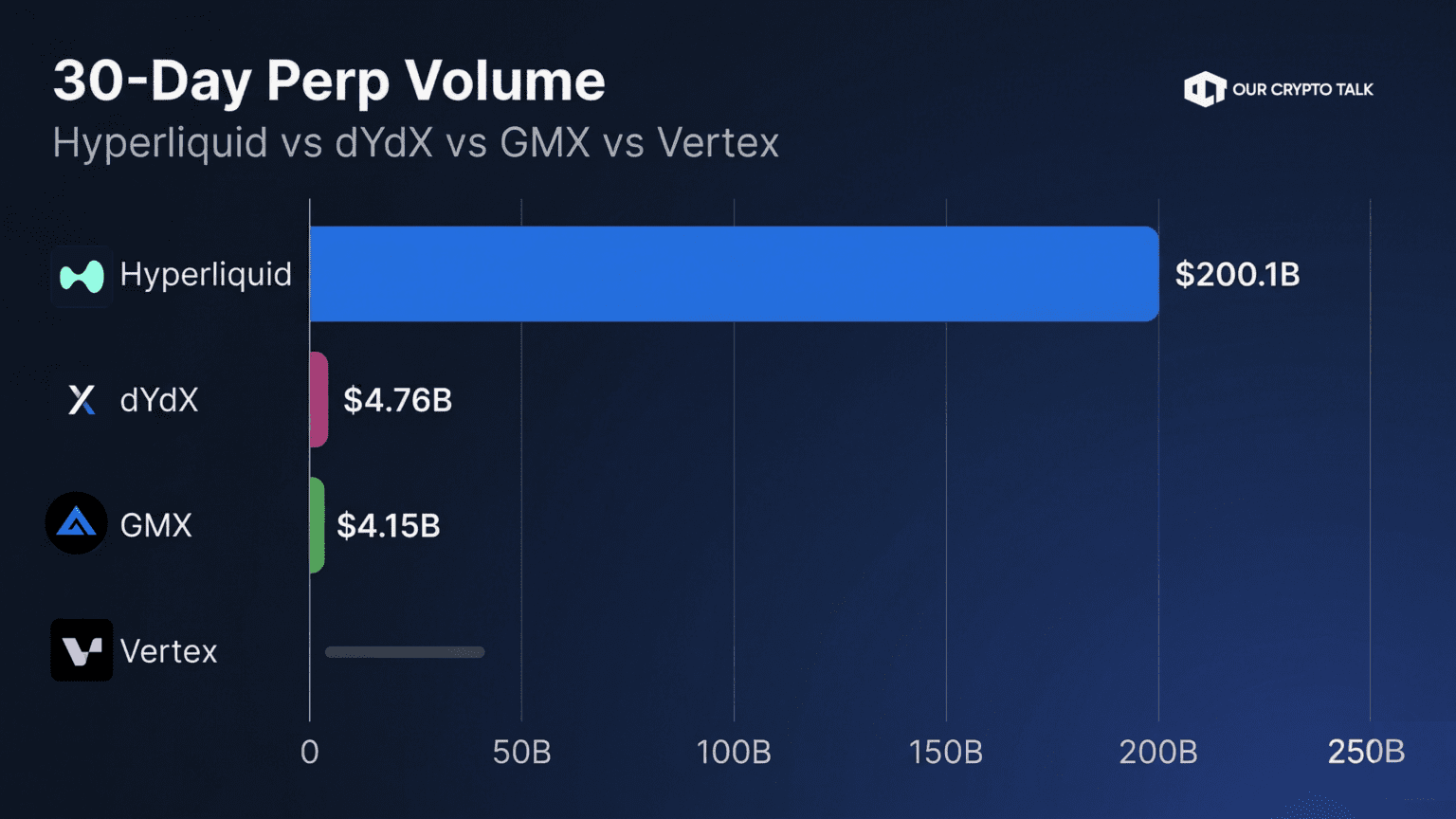

Daily volume regularly ranges between $5 billion and $12 billion. The March 23, 2026 spike hit $12.3 billion in a single day. The most recent 30-day window recorded $200.1 billion in perpetual contract volume alone.

That is 42x more volume than dYdX and 48x more than GMX. The competitive gap is not a gap. It is a chasm.

Over 70% of all open interest across every decentralized perpetual exchange on earth sits on Hyperliquid.

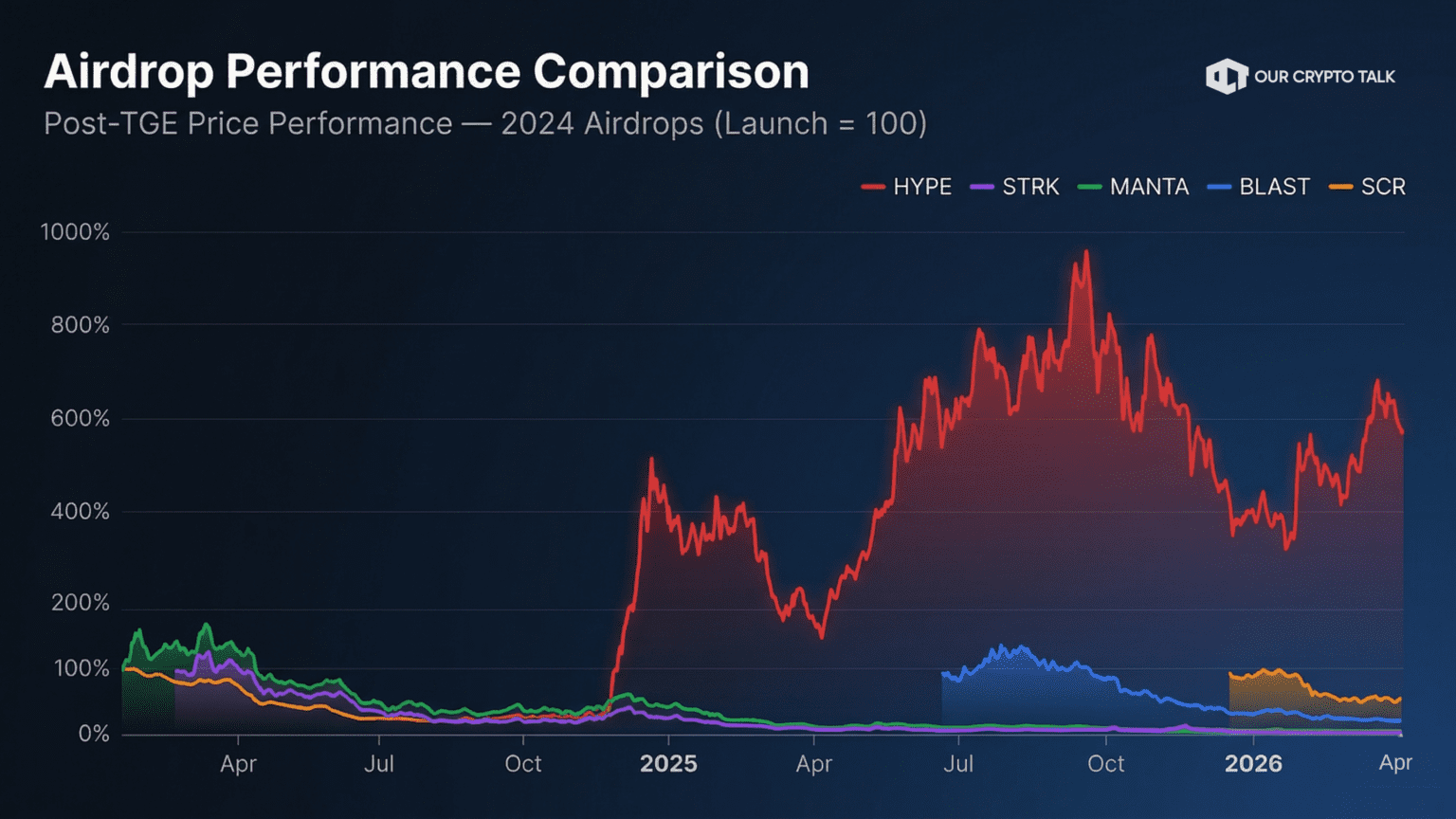

On November 29, 2024, Hyperliquid distributed 310 million HYPE tokens to approximately 94,000 eligible users. That represented 31% of total supply. The average allocation was worth roughly $45,000. One address claimed 970,000 tokens valued at $9.56 million.

The VC allocation was zero. Because there were no VCs.

The standard playbook in 2024 said this should have been a disaster. Every major airdrop that year followed the same script: VCs take 20%+, community gets 5%, token launches, everyone dumps. Scroll, Blast, Starknet, and Manta all saw massive outflows post-TGE. The consensus on Crypto Twitter was that greedy VC allocations had killed the airdrop model entirely.

HYPE defied every expectation. It opened at roughly $3.90, did not dump, and climbed to an all-time high of $59.30 by September 2025. The lesson was immediate: build a genuinely superior product, give the tokens to the people who actually use it instead of the institutions that flip it, and the market rewards you.

Hyperliquid’s airdrop did not just distribute wealth. It created a community of aligned holders who believed they owned a piece of the future of financial infrastructure.

Hyperliquid is no longer just a perps DEX. The HIP framework is systematically expanding it into something much larger. HIP-1 and HIP-2 laid the foundation with token standards and liquidity mechanisms. The real inflection points came after.

HIP-3 introduced permissionless perpetual markets. Anyone can now create a new market by staking 500,000 HYPE. This unlocked 24/7 on-chain trading of S&P 500 futures, Nasdaq 100, gold, silver, crude oil, and forex for the first time on a decentralized exchange.

The S&P 500 market hit $100 million in volume on day one. Weekend volume reached $720 million in a single day when traditional markets were closed and oil prices were spiking. Traders came to Hyperliquid because it was the only venue open. Within four months, HIP-3 was contributing approximately 10% of total revenue.

HIP-4 introduced outcome contracts in February 2026. These are fully collateralized instruments that settle between 0 and 1 based on real-world events. No leverage. No liquidation risk. They were designed for prediction markets and options-style instruments.

Kalshi’s head of crypto co-authored the proposal. In March 2026, the two formally announced a partnership to build on-chain prediction markets together, bridging the CFTC-regulated world and DeFi directly. Prediction markets did $63.5 billion in volume during 2025, a 302.7% increase year-over-year. HIP-4 positions Hyperliquid to capture a share of that rapidly growing market.

The trajectory is clear. Perps exchange, then real-world asset trading, then prediction markets, then everything. Jeff Yan’s own framing describes it as the “AWS of financial infrastructure” – an open, permissionless layer on which all financial products can be built, traded, and settled on-chain.

HYPE is not a governance token that sits idle. It is the engine of a self-reinforcing flywheel.

97% of all trading fees flow into the Assistance Fund. The Assistance Fund buys HYPE on the open market and permanently removes it from circulation. Roughly $795 million worth of HYPE has already been burned through this mechanism.

The loop works as follows: more volume generates more fees, which fund more buybacks, which reduce supply, which drives price higher, which attracts more attention, which brings more users, which drives more volume. Repeat.

HYPE commands a 104x market cap premium over dYdX and 131x over GMX. The market is not simply pricing dominance. It is pricing a fundamentally different category of financial infrastructure.

The tension is real though. Only 24.8% of supply currently circulates. Core contributor tokens vest until 2027-2028. Monthly distributions of approximately 1.2M HYPE add steady sell pressure. Whether buybacks can consistently outpace unlocks is the central question for holders going forward.

HYPE commands a 104x market cap premium over dYdX and 131x over GMX. The market is not simply pricing dominance. It is pricing a fundamentally different category of financial infrastructure.

The tension is real though. Only 24.8% of supply currently circulates. Core contributor tokens vest until 2027-2028. Monthly distributions of approximately 1.2M HYPE add steady sell pressure. Whether buybacks can consistently outpace unlocks is the central question for holders going forward.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.