Morgan Stanley MSBT Bitcoin ETF launched with a 0.14% fee, the lowest among spot Bitcoin ETFs. How it compares to BlackRock's IBIT and others.

Author: Sahil Thakur

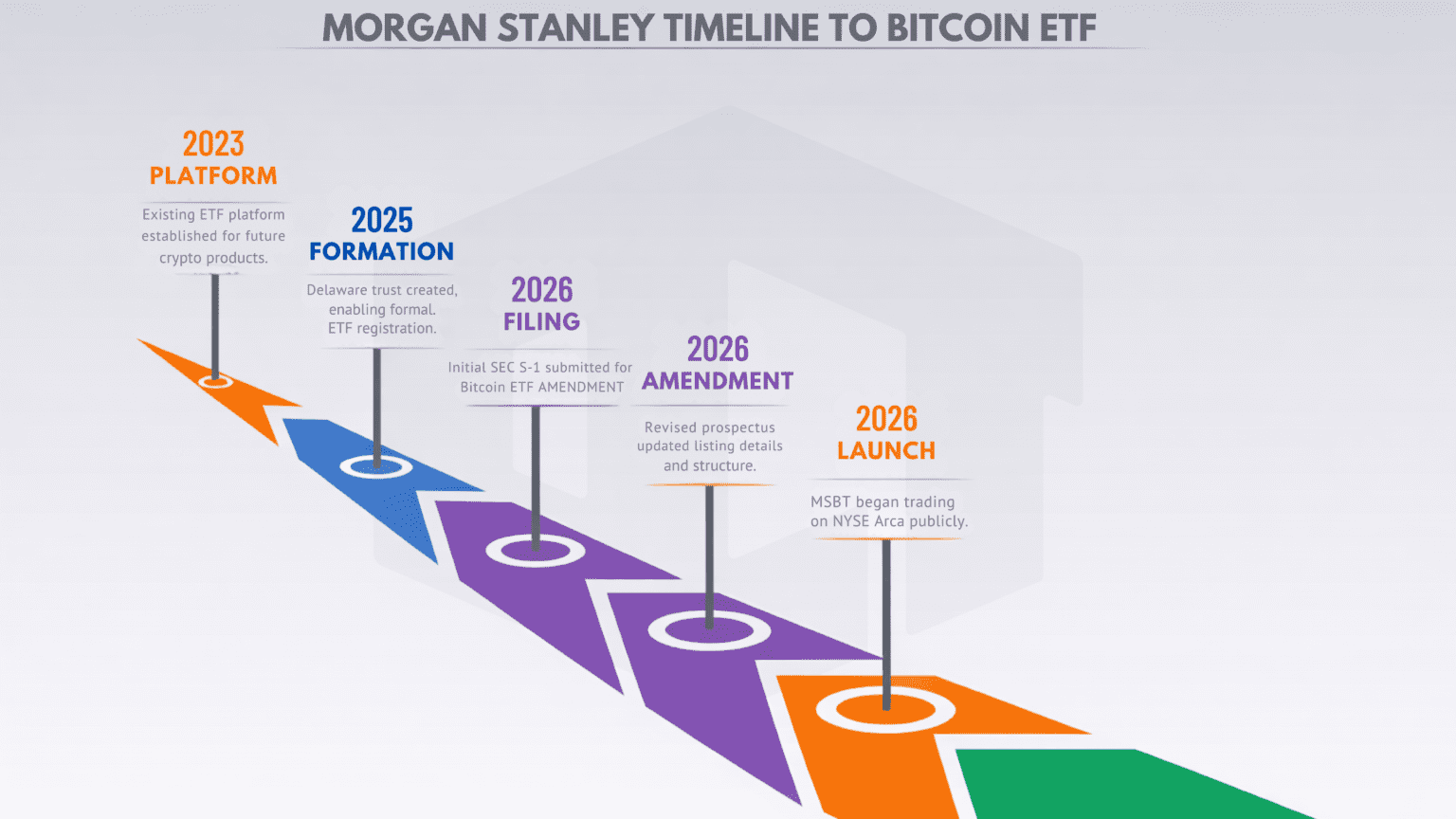

Morgan Stanley launched its spot Bitcoin ETF on April 8, 2026. The product, called Morgan Stanley Bitcoin Trust, trades on NYSE Arca under the ticker MSBT and charges a 0.14% annual fee. That’s nearly half what BlackRock’s iShares Bitcoin Trust (IBIT) charges at 0.25%. For a firm that manages trillions in client assets, the move puts real competitive pressure on the existing spot Bitcoin ETF field and opens a direct pipeline from one of Wall Street’s largest advisory networks into Bitcoin exposure.

MSBT isn’t the first spot Bitcoin ETF in the United States. That wave started in January 2024, when IBIT, Fidelity’s FBTC, and several others began trading after years of regulatory delays. But Morgan Stanley entering the market with its own product shifts the dynamic. This isn’t just another asset manager launching a fund. It’s a bank-affiliated sponsor with roughly 16,000 financial advisors and a built-in distribution channel that could funnel significant assets into a single product. Day-one net inflows hit $34 million, according to Yahoo Finance, a solid opening for a brand-new fund in a market already dominated by incumbents.

MSBT is a Delaware statutory trust, formed on December 16, 2025. It continuously issues shares that represent a fractional interest in the trust’s bitcoin holdings. The product tracks bitcoin’s performance using the CoinDesk Bitcoin Benchmark 4PM NY Settlement Rate, adjusted for fees and expenses.

One structural point that matters: MSBT isn’t a ’40 Act ETF. It’s not registered under the Investment Company Act of 1940, which means investors don’t get the protections that come with traditional mutual funds or registered ETFs. This is the same structure most spot Bitcoin ETFs use, including IBIT, but it’s something investors should understand upfront.

The trust has a somewhat unusual governance setup with two trustees, one in Delaware and one in the Cayman Islands. The Cayman trustee delegates day-to-day responsibilities to the sponsor under delegation agreements. Morgan Stanley Investment Management acts as the sponsor, handling operational decisions and overseeing the service provider stack.

As for how MSBT got off the ground: Morgan Stanley filed initial registration statements with the SEC on January 6, 2026, for both a Bitcoin ETP and a separate Solana ETP. The MSBT prospectus, filed under Rule 424(b)(3), is dated April 6, 2026. Before listing, the sponsor purchased seed baskets to establish the trust’s initial bitcoin holdings. A $100 audit seed was created on March 9, 2026, and 50,000 shares were purchased as initial seed creation baskets with $1 million in proceeds to acquire bitcoin through a designated counterparty.

The fee is straightforward. MSBT charges a 0.14% annualized Delegated Sponsor Fee, accrued daily based on NAV. There are no additional management fees layered on top. That 0.14% covers operating costs through a unitary fee structure, making it one of the cheapest spot Bitcoin ETFs available.

The custody setup is where things get more interesting. MSBT uses what amounts to a dual-custody model for its bitcoin holdings. The Bank of New York Mellon and Coinbase Custody Trust Company both serve as bitcoin custodians. BNY also handles the traditional fund operations side: administrator, transfer agent, and cash custodian. So you get a systemically important bank managing the paperwork and holding bitcoin alongside a crypto-native custodian.

Then there’s the prime brokerage layer. Coinbase, Inc. acts as prime broker for MSBT, handling execution and facilitating bitcoin sales to pay the sponsor fee and other expenses. Foreside Fund Services serves as the marketing agent, reviewing materials for compliance.

The dual-custody approach is clearly designed to appeal to institutional investors and wealth platforms that want “big bank” controls without giving up crypto-native infrastructure. But it also concentrates critical dependencies. The MSBT prospectus explicitly flags this: a small number of providers handle custody, execution, and AP services, creating correlated failure modes if any one of them has a disruption. That’s a tradeoff, not a free lunch.

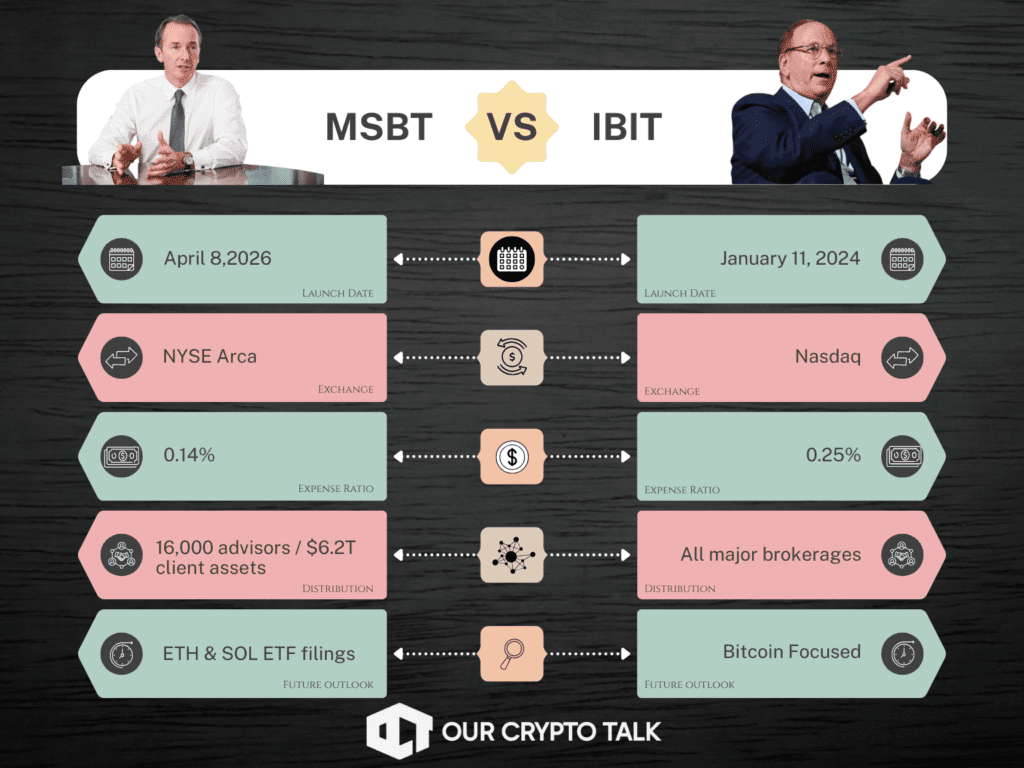

The comparison most investors want is MSBT against IBIT, BlackRock’s iShares Bitcoin Trust, which is the largest and most liquid spot Bitcoin ETF by a wide margin. Here’s how they stack up across the dimensions that actually matter.

On fees, MSBT wins on paper. Its 0.14% Delegated Sponsor Fee undercuts IBIT’s 0.25% expense ratio. Over time, in a commodity-like beta product where everyone holds the same underlying asset, fee is one of the few durable differentiators. A $100,000 allocation would save roughly $110 per year in MSBT versus IBIT. That’s small in absolute terms but compounds over years, and it matters at scale for advisors running model portfolios across thousands of accounts.

Benchmarks differ slightly. MSBT uses the CoinDesk Bitcoin Benchmark 4PM NY Settlement Rate, while IBIT tracks the CME CF Bitcoin Reference Rate, New York Variant. Both are institutional-grade pricing methodologies designed for NAV marking. In normal market conditions the difference is negligible, but during stressed liquidity or exchange outage scenarios, the two benchmarks could diverge briefly.

Custody architecture is where the design philosophies split. MSBT runs dual bitcoin custodians (BNY and Coinbase Custody), with BNY also handling cash and fund admin. IBIT custodies bitcoin primarily at Coinbase Custody, with Anchorage Digital Bank as an available alternative, and uses BNY for cash and administration. MSBT’s pitch is that having a major bank actively custodying bitcoin alongside a crypto-native firm adds a layer of institutional trust. The counterargument is that more custodians means more governance and handoff complexity.

Basket size is a mechanical difference that affects AP arbitrage granularity. MSBT uses 10,000-share baskets for creations and redemptions, while IBIT uses 40,000-share baskets. Smaller baskets can lower the minimum block size for arbitrage trades and improve price-to-NAV alignment in theory. In practice, realized liquidity depends more on AUM, spreads, and AP engagement.

The biggest gap is scale. IBIT holds approximately $54.76 billion in assets as of April 2026 and has accumulated $63.3 billion in cumulative net inflows since January 2024, per Farside Investors. MSBT started from zero. IBIT’s liquidity and tight bid-ask spreads are hard to match for any new entrant. But MSBT doesn’t necessarily need to beat IBIT on the open market. Its competitive edge is distribution: Morgan Stanley’s advisory platform, where “house brand” preferences, model portfolio inclusion, and platform economics influence which ETFs get shelf space.

MSBT enters a market that’s structurally concentrated but still attracting meaningful flows. As of April 2026, the landscape looks roughly like this:

IBIT leads with around $54.76 billion in AUM and a 0.25% fee. Fidelity’s FBTC sits at about $13.2 billion with the same 0.25% expense ratio. The original Grayscale Bitcoin Trust (GBTC) still holds roughly $10.62 billion, though it charges 1.50% and has seen massive cumulative outflows of $26.1 billion as investors rotate into cheaper alternatives. Grayscale’s Mini Trust (BTC) holds about $3.59 billion at 0.15%. Bitwise’s BITB and ARK 21Shares’ ARKB each manage around $2.5 billion with fees in the 0.20-0.21% range.

The flow picture tells the story of a market that’s still growing but rotating internally. Cumulative net flows across all U.S. spot Bitcoin ETFs reached approximately $56.2 billion through April 8, 2026, according to Farside Investors. IBIT captured the lion’s share, while GBTC bled assets consistently. So the total pie is expanding, but the money is moving toward lower-cost, higher-liquidity products.

Daily flows remain volatile. Total U.S. spot Bitcoin ETF net flows hit +$471.4 million on April 6, 2026, then swung to -$159.1 million the next day, before landing at a more moderate positive figure on April 8 when MSBT debuted. That kind of day-to-day choppiness is normal for the asset class and reflects tactical allocator behavior mixed with momentum trading.

If you’re evaluating MSBT or any spot Bitcoin ETF, it helps to understand the plumbing. A spot Bitcoin ETF is essentially a share wrapper around pooled bitcoin holdings. You buy shares on a stock exchange, and those shares represent a fractional claim on the bitcoin held in the trust’s custody accounts. You never touch or self-custody the bitcoin.

The mechanism that keeps the share price aligned with the value of the underlying bitcoin is the creation and redemption process. Authorized Participants, which are registered broker-dealers and DTC participants, can create new shares by delivering cash or bitcoin to the trust in large blocks called baskets. They can also redeem baskets to pull bitcoin or cash back out. When shares trade at a premium to NAV, APs create new shares (adding supply until the premium shrinks). When shares trade at a discount, APs redeem shares (reducing supply until the discount closes).

MSBT supports both cash and in-kind creation and redemption pathways. The cash pathway has a specific design worth noting: when an AP creates shares using cash, the sponsor instructs a designated “Bitcoin Counterparty” to purchase bitcoin and deposit it into the trust’s custody. The AP doesn’t pick the counterparty. The prospectus is clear that pricing slippage in cash transactions is borne by the AP, not the trust, which protects existing shareholders but can affect AP economics.

Tracking error, the gap between the ETF’s return and the underlying bitcoin price, exists even with this arbitrage mechanism. Fees create a constant small drag. Cash creation and redemption frictions add execution-level costs. And in stressed markets, if AP capacity gets constrained or balance sheets tighten, premiums and discounts can widen more than usual. MSBT’s prospectus acknowledges all of these as risks.

On taxes, both MSBT and IBIT stress that investors should consult advisors. A few high-level points from the prospectus disclosures: shareholders could incur tax liability without receiving any distribution, the tax treatment of bitcoin transactions isn’t fully settled in all contexts, and events like forks or airdrops can create complications. None of this is unique to MSBT, but it’s part of the product reality.

Rather than predict prices, it’s more useful to think in scenarios that connect MSBT’s mechanics to plausible market states.

If risk appetite stays strong and U.S. spot Bitcoin ETFs return to sustained positive daily inflows, the entire complex acts as a “beta transmission” mechanism. Inflows create immediate spot purchasing needs, either directly or through counterparty pathways, which tightens available supply and can reinforce upside momentum. Repeat inflow spikes like the +$471.4 million day on April 6 suggest this channel is still very much active.

A choppier base case looks like alternating flow days: positive bursts followed by outflow sessions. This is what the data shows around MSBT’s launch week. In that environment, the largest funds with the tightest spreads and deepest liquidity tend to attract the most capital, while challengers like MSBT compete on fee and distribution. It’s not a bad setup for a new product with a built-in advisory channel, but it’s not a windfall either.

The bearish scenario involves a macro shock or sharp risk-off move. In a drawdown, several frictions can widen premiums and discounts: APs reduce balance sheet deployment, cash redemption execution slippage increases, and operational concentration risks become more visible. MSBT’s prospectus explicitly warns that limited AP capacity and cash creation mechanics can cause the share price to diverge from NAV during stress.

On a longer horizon, the medium-term story for MSBT hinges on whether wealth platforms formalize bitcoin allocations. If advisor-approved model portfolios start including a standard 1-3% Bitcoin sleeve, the fund that sits on the platform with the lowest fee and the sponsor’s brand gets a structural advantage. Morgan Stanley’s day-one positioning suggests they’re building for exactly that scenario.

Fee compression is also coming for the broader market. MSBT’s 0.14% sets a new low-fee benchmark. Over time, that pressure likely pushes the market toward a small number of ultra-liquid “core beta” products and a longer tail of niche offerings. The wide fee dispersion that still exists across the Bitcoin ETF space, ranging from 0.14% up to 1.50%, won’t last indefinitely.

The regulatory variable cuts both ways. Clearer U.S. rules for spot crypto ETPs would support deeper institutional adoption, making the “wrapper” a more durable bridge for pension governance, RIA compliance, and standardized reporting. But MSBT’s prospectus repeatedly warns that regulation is evolving and potentially inconsistent. An adverse regulatory shift, whether on custody rules, market surveillance, or intermediary requirements, could raise costs and operational burdens across the entire product category.

MSBT carries risks that go beyond normal stock-market volatility. Bitcoin is a single-asset exposure with extreme price swings. The MSBT prospectus cites wide multi-year price ranges to illustrate how quickly the trust’s value can move in either direction.

Operational concentration is a specific concern. The number of custodians, prime brokers, and authorized participants capable of servicing spot Bitcoin ETFs is small. If Coinbase or BNY experienced a significant disruption, it wouldn’t just affect MSBT. It would ripple across multiple products simultaneously. That’s a correlated failure mode the prospectus explicitly acknowledges.

Regulatory risk is real and ongoing. Bitcoin’s regulatory treatment in the U.S. is still evolving, with potentially conflicting rules across agencies. The prospectus warns this could alter the nature of an investment in the trust or affect its ability to continue operating.

And because MSBT isn’t a ’40 Act fund, investors don’t get the protections of the Investment Company Act. The trust’s bitcoin custody also carries irreversibility risk: if private keys are compromised or lost, the bitcoin can’t be recovered. Insurance coverage at the custodians exists but isn’t necessarily sufficient and is shared across customers.

None of these risks are unique to MSBT. They apply across the spot Bitcoin ETF category. But they’re qualitatively different from what investors face in a broad-market equity or bond ETF, and they deserve attention.

The Morgan Stanley Bitcoin ETF matters less as a product innovation and more as a competitive signal. The mechanics are solid: low fee, dual custody, support for cash and in-kind flows. But the real story is distribution. When a bank with 16,000 advisors launches its own spot Bitcoin ETF, the question shifts from “will advisors recommend Bitcoin exposure” to “which product gets the default allocation.” For investors already in IBIT or another spot product, the fee savings from switching are real but modest. For those working with a Morgan Stanley advisor, MSBT may simply become the path of least resistance.

The competitive dynamic it introduces, bank-affiliated sponsors versus crypto-native issuers, is what’s worth watching over the next 12 to 18 months. If more wirehouses follow Morgan Stanley’s lead, fee compression will accelerate and the market will consolidate further around a few dominant products. MSBT may not dethrone IBIT on liquidity anytime soon, but it doesn’t need to. It just needs to capture its own channel.

This article is for informational purposes only and does not constitute financial advice. Always do your own research before making investment decisions.