RWA crypto tokens promise real-world backing, but what if the issuer goes bankrupt? We break down 7 risks of tokenized assets so you invest with eyes open.

Author: Kritika Gupta

RWA crypto tokens promise the stability of real-world assets on the speed of blockchain. But “backed by real assets” does not mean “risk-free.” Here’s what can actually go wrong, and is RWA crypto safe enough for your portfolio?

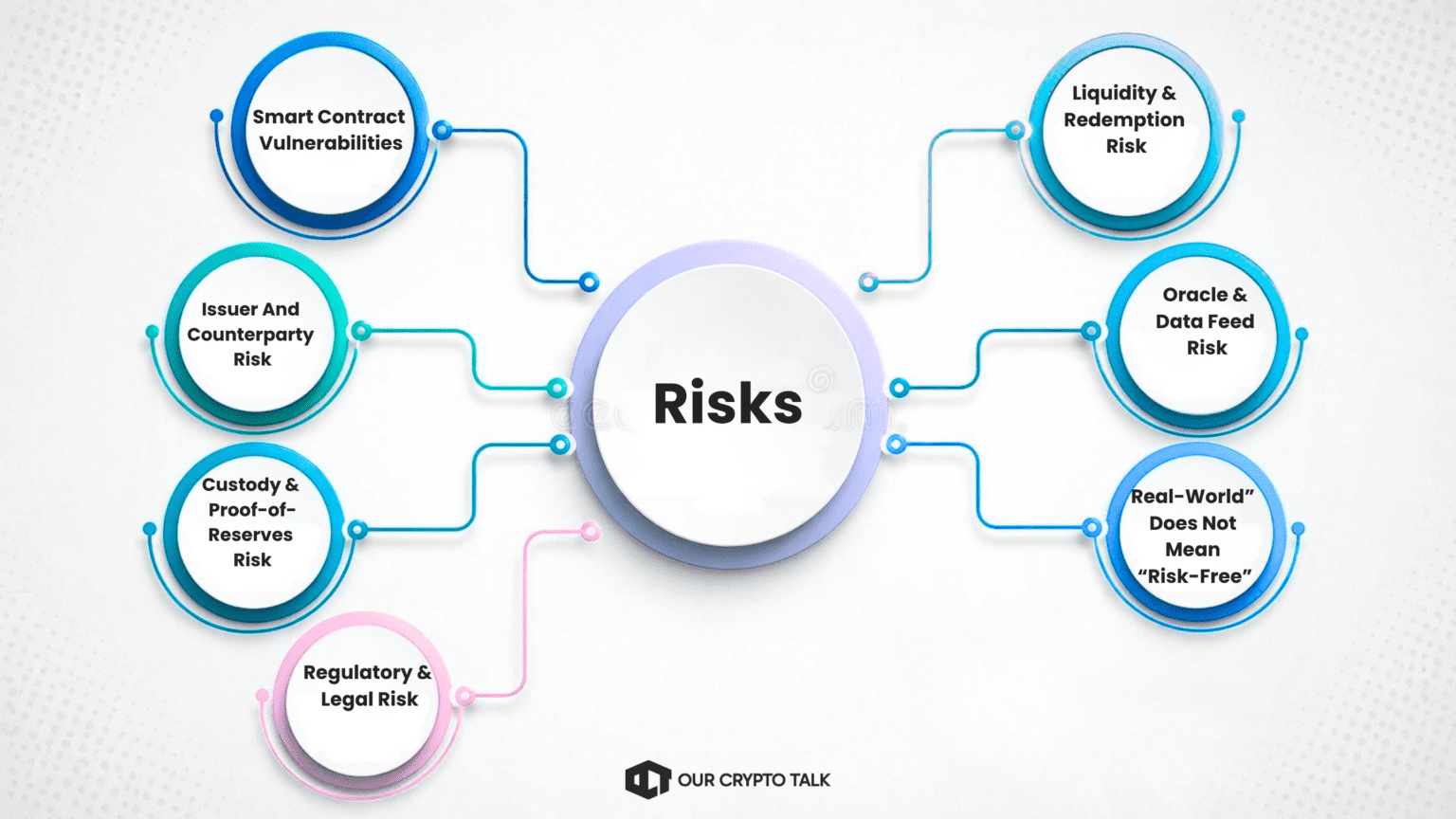

The RWA narrative has accelerated fast. Tokenized Treasuries, private credit, and real estate now drive billions in on-chain value. New entrants see familiar assets and assume familiar safety. We have seen this assumption break under stress before. RWAs introduce a layered risk model that blends smart contracts, legal structures, custodians, and off-chain counterparties. Each layer can fail independently.

At Our Crypto Talk, we focus on mapping these failure points before they surface. We have covered collapses where “real-world backing” unraveled quickly. A single external manager loss triggered a depeg, froze redemptions, and wiped confidence across the system. That pattern is not isolated. It repeats across smaller issuers, weaker custody setups, and poorly structured SPVs. This guide does not challenge the RWA thesis. It isolates where execution fails.

In traditional finance, safety comes from clear guarantees. You rely on deposit insurance, defined bankruptcy priority, and regulated custodians that operate within well-tested legal frameworks. In RWA crypto, that definition does not translate cleanly. Instead, safety compresses into a single, practical question. Can you actually get your money back when you want it?

RWA crypto tokens do not represent direct ownership of an asset. They represent a claim on an off-chain asset such as a Treasury bill, a loan, or a piece of real estate. That distinction matters more than most investors realize. The blockchain layer handles transfers, yield distribution, and settlement with precision. It records ownership, executes transactions, and enables 24/7 liquidity. From a technical standpoint, that layer works efficiently. We have not seen major failures at the token layer itself.

The real risk sits outside the chain. The asset exists in the traditional financial system, held by an issuer, structured through a special-purpose vehicle, and secured by a custodian. Legal agreements define your rights. Jurisdiction determines enforceability. This creates a split system. On-chain, everything appears transparent, fast, and reliable. Off-chain, the system depends on institutions, legal structures, and operational discipline.

If any of these off-chain layers fail, the token does not disappear. It continues to trade and exist on-chain, but it loses its economic meaning. You still hold a token in your wallet, but your ability to redeem it for the underlying asset becomes uncertain or completely broken.

That is the core misunderstanding in RWA crypto. The technology works. The structure determines whether your capital is actually safe.

Smart contracts form the execution layer of RWAs, and they introduce immediate technical risk. In fact, even audited contracts fail.

Most credible projects undergo audits by firms like CertiK, Trail of Bits, or OpenZeppelin. However, an audit reduces risk, it does not eliminate it. We have seen multiple DeFi exploits where audited code still failed in production. Attackers do not break the obvious logic. They target edge cases, integration gaps, and assumptions that auditors or developers overlook. Flash loan exploits, reentrancy bugs, and oracle manipulation continue to appear across protocols that were considered “secure.”

Upgradeability adds another layer of risk. Many RWA crypto protocols rely on proxy contracts or admin keys that allow teams to modify logic after deployment. This flexibility helps teams patch vulnerabilities and evolve the product. At the same time, it creates a central point of control. If those keys are compromised, misused, or poorly secured, the attacker does not need to exploit the contract. They simply take control of it. We have seen incidents where privileged access became the attack vector rather than the code itself.

We approach this layer with a simple filter. First, check for public audit reports from reputable firms, not just a generic “audit.pdf” hosted on a website. Second, confirm the presence of active bug bounty programs, ideally on platforms like Immunefi, which signal ongoing security testing. Third, review upgrade controls. Time-locked changes, multi-signature approvals, and transparent governance reduce the risk of sudden or malicious contract changes.

If a protocol lacks audits, restricts code visibility, or retains unrestricted admin control, the technical risk remains high regardless of the underlying asset.

This is the most important question in RWAs, and most beginners never ask it. What happens if the entity behind the token goes bankrupt?

When you hold an RWA crypto token, you rely on a legal issuer that controls the underlying asset. That issuer may operate through a special-purpose vehicle (SPV) or hold assets directly on its balance sheet. This distinction defines your risk.

We have seen this pattern play out repeatedly. The Stream Finance and XCHNG-style collapses followed the same structure. External managers lost funds, issuers lacked proper legal isolation, and redemptions froze. Token holders discovered that “real-world backing” did not translate into enforceable claims.

Relative positioning across RWA issuer and counterparty risk structures

Custody answers a simple but critical question. Who actually holds the underlying asset?

In a strong RWA crypto structure, a regulated third-party custodian holds the assets. This typically includes banks or licensed trust companies that maintain segregated accounts on behalf of investors. Segregation matters because it ensures the assets do not sit on the issuer’s balance sheet.

In weaker setups, the issuer controls custody directly. This often means self-custody wallets, internal treasury accounts, or reliance on a single entity without external oversight. That structure introduces a single point of failure. Apart from this we have seen custody failures wipe out otherwise viable products.

Proof-of-reserves attempts to address this risk. These reports aim to show that the on-chain token supply matches the off-chain assets held in custody. However, not all verification carries equal weight. An attestation confirms balances at a specific point in time.

Regulatory fragmentation creates one of the most unpredictable risks in RWAs. Different jurisdictions apply different rules, and those rules continue to evolve.

A core issue is classification. Regulators may treat an RWA token as a utility today and reclassify it as a security tomorrow. That shift can trigger immediate consequences such as forced delistings, trading restrictions, or compliance requirements that most platforms cannot meet quickly. We have seen liquidity disappear almost instantly after regulatory action.

In the European Union, the Markets in Crypto-Assets Regulation framework imposes strict licensing, disclosure, and reserve requirements on asset-referenced tokens. Projects that fail to comply risk removal from exchanges and wallets.

For retail investors, the implication is direct. You may hold a token that you can legally trade today but cannot access tomorrow. Jurisdiction also matters. However, offshore issuers may operate within one legal framework while restricting users from another.

Regulatory risk does not affect the asset itself. It affects your ability to access, trade, and redeem it.

RWA tokens often appear liquid because they trade on-chain, but real liquidity depends on redemption, not just price discovery.

Secondary markets for most RWAs remain thin. You may see activity on a DEX, but depth is limited and large orders can move price significantly. In normal conditions, this may not matter. Therefore, under stress, it becomes critical. We have seen spreads widen sharply and liquidity disappear during volatility spikes.

Redemption mechanics add another constraint. Many RWA issuers do not offer instant redemption. Instead, they operate through daily or weekly windows, minimum size thresholds, or manual approval processes. Some require KYC or off-chain settlement steps before releasing funds.

During market stress, these systems tighten. Issuers may pause redemptions to manage liquidity or protect remaining assets. At the same time, secondary markets diverge from NAV, and tokens can trade at a discount.

Blockchains do not natively understand real-world data. They rely on external systems called oracles to feed in prices, yields, and net asset values.

This creates a critical dependency. If an oracle delivers incorrect, delayed, or manipulated data, the entire RWA system can misprice assets. A stale Treasury yield or incorrect bond price can distort valuations, trigger faulty liquidations, or enable overleveraged borrowing against inflated collateral.

We have seen oracle issues amplify losses in DeFi before. RWAs inherit the same dependency. At the same time, attack vectors include manipulated data sources, delayed updates, and weak oracle infrastructure. If the data layer fails, the financial logic built on top of it fails with it.

The underlying asset still carries risk. Tokenization does not eliminate it.

Bonds fall when interest rates rise. Real estate prices decline during weak demand cycles. Private credit faces defaults when borrowers fail to repay. As a result, RWA tokens simply wrap these exposures in a blockchain format.

We see a recurring mistake. Investors assume “real-world” equals stability. In practice, these assets still move with macro conditions. Net asset value can fluctuate, yields can compress, and redemption timelines can extend under stress. The token improves accessibility, liquidity, and settlement speed. It does not remove market risk. If the underlying asset loses value, the token follows.

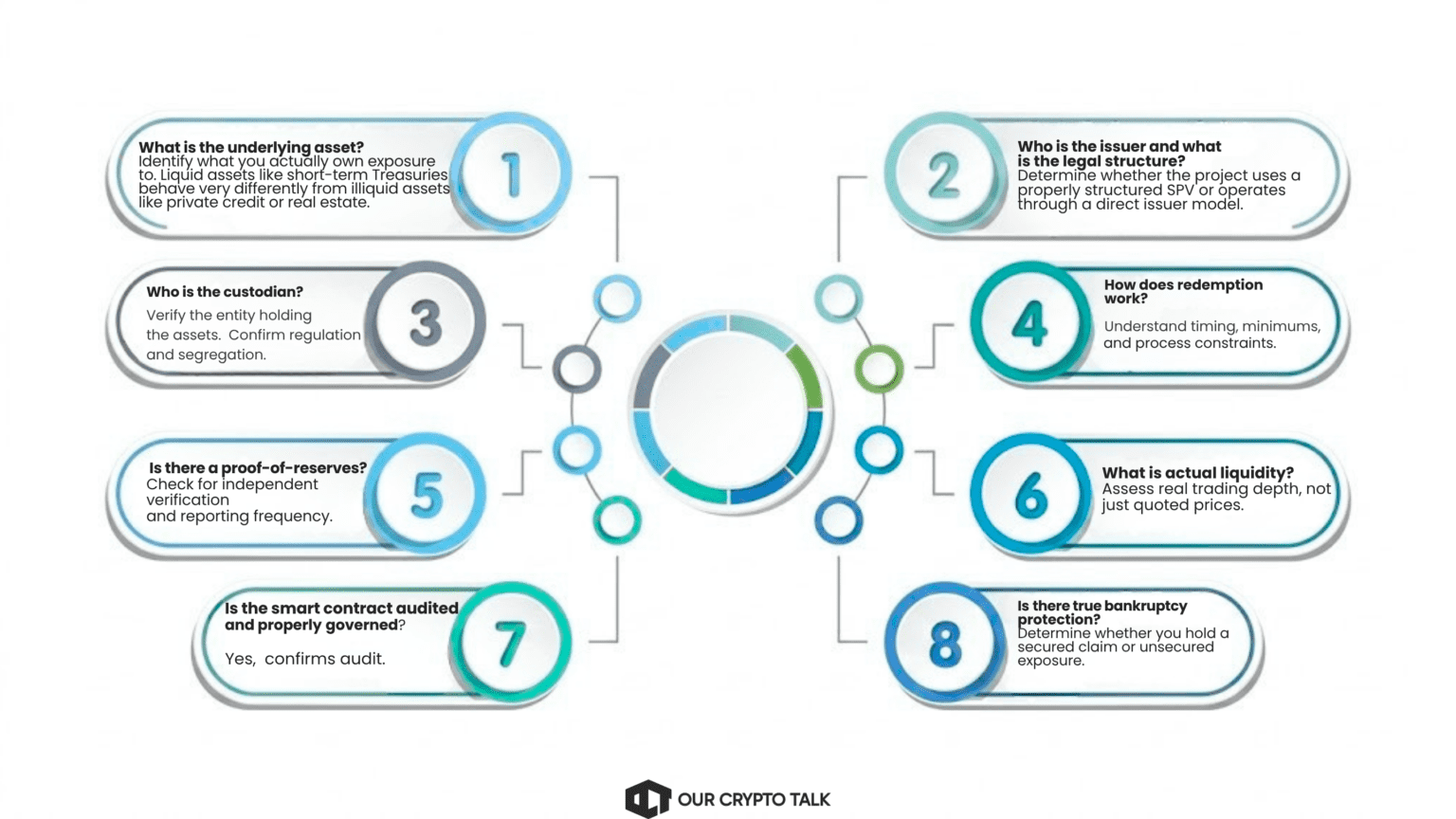

Treat RWAs like structured financial products, not simple tokens. Therefore, you need to evaluate multiple layers before allocating capital. Use this checklist to assess risk:

If you cannot verify these points quickly through public disclosures, the risk is not priced in.

RWAs are not inherently unsafe, but “backed by real assets” does not mean guaranteed. The structure behind the token determines the outcome, not the narrative.

The strongest projects, such as BlackRock BUIDL, Franklin Templeton BENJI, and Ondo Finance, operate with institutional-grade custody, clear legal frameworks, and transparent proof-of-reserves. They mirror traditional finance standards while leveraging blockchain efficiency.

The weakest projects follow patterns we have documented repeatedly. Opaque issuers, weak custody, unclear legal claims, and overreliance on marketing narratives create the same failure conditions seen in past collapses.

The difference is structural.

Do your own research. This article is for informational purposes only and does not constitute financial advice.