Learn how 3Jane is bringing unsecured credit onchain with USD3, sUSD3, real-world lending, and the JANE token ecosystem.

Author: Akshat Thakur

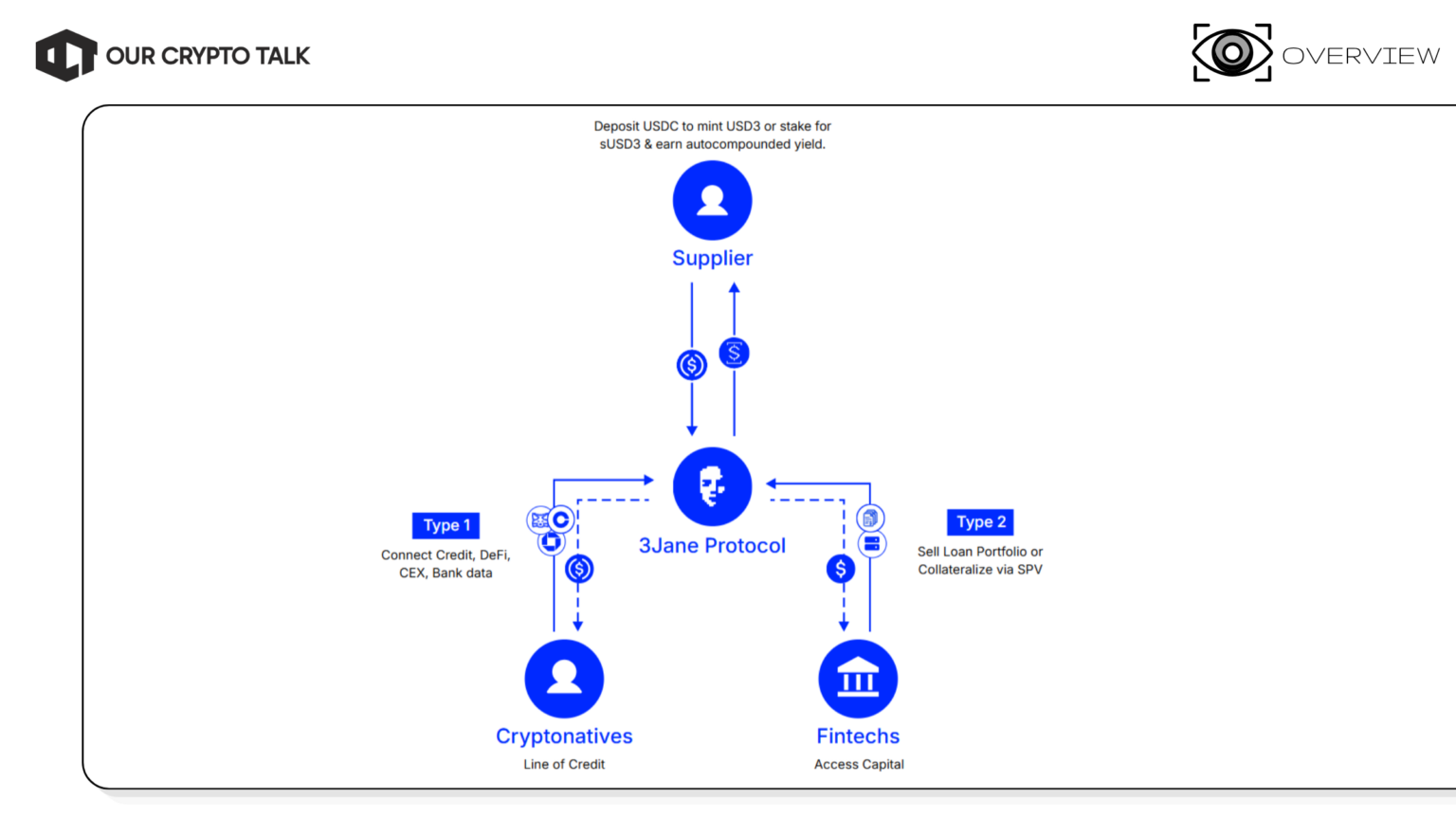

3Jane is building a permissionless credit-based money market on Ethereum that offers unsecured USDC credit lines backed by verifiable financial data rather than excess collateral. Instead of forcing users to deposit more value than they borrow, the protocol uses a combination of onchain assets, offchain financial information, and future cash flows to assess creditworthiness.

That approach targets one of the largest inefficiencies in crypto lending. Today’s dominant lending protocols, such as Aave and Morpho, remain heavily overcollateralized. They move billions in liquidity but primarily serve users who already have significant crypto assets. Traditional credit markets solve this problem through underwriting, but they operate through slow, permissioned, and geographically restricted systems.

3Jane sits between those two worlds. The protocol uses zkTLS-verified financial data to evaluate borrowers while preserving privacy. It then combines that underwriting layer with onchain enforcement mechanisms such as credit slashing and non-performing credit line auctions.

The broader vision extends beyond retail borrowers. Capital supplied through the USD3 and sUSD3 system can also support fintech warehouse facilities and forward-flow agreements, creating a bridge between crypto liquidity and real-world credit demand.

The timing is notable. Ethena demonstrated significant demand for yield-bearing dollar assets beyond traditional DeFi lending. At the same time, zkTLS infrastructure has matured, onchain credit scoring has become more viable, and fintech lenders are actively seeking alternative sources of capital.

Rather than creating another synthetic yield product, 3Jane aims to build a scalable credit market powered by real economic activity. If successful, it could become one of the first protocols to make unsecured lending a native part of onchain finance.

3Jane operates in a category with clear leaders but very little direct competition.

Protocols such as Aave and Morpho dominate crypto lending. However, they rely almost entirely on overcollateralization. Users must lock up significant assets before accessing liquidity, which limits capital efficiency and excludes many potential borrowers.

On the real-world asset side, Maple, Goldfinch, and Centrifuge have brought institutional credit onchain. These platforms have proven demand for blockchain-based lending, but they remain largely permissioned and relationship-driven. Access depends on legal structures, institutional partnerships, and manual underwriting.

3Jane targets the gap between those models.

Its core proposition is a permissionless credit market that combines crypto-native infrastructure with real-world underwriting. Borrowers can access unsecured USDC credit lines using a mix of verifiable crypto assets, offchain bank and credit data, and projected cash flows. The protocol verifies much of this information through zkTLS, allowing risk assessment without exposing sensitive financial data.

The second differentiator is enforcement. Traditional DeFi relies on liquidations. Traditional finance relies on courts and collections. 3Jane combines both approaches through credit slashing and non-performing credit line auctions that transfer distressed debt to licensed recovery participants.

This creates a meaningful moat. Aave and Morpho lack the infrastructure to underwrite offchain credit data at scale. Permissioned RWA lenders deliberately avoid open-access credit markets because doing so introduces new regulatory and operational challenges.

The result is one of the few credible attempts at permissionless unsecured lending. Live facilities with partners such as LendSwift and Slope suggest the model is already moving beyond theory and into practical deployment.

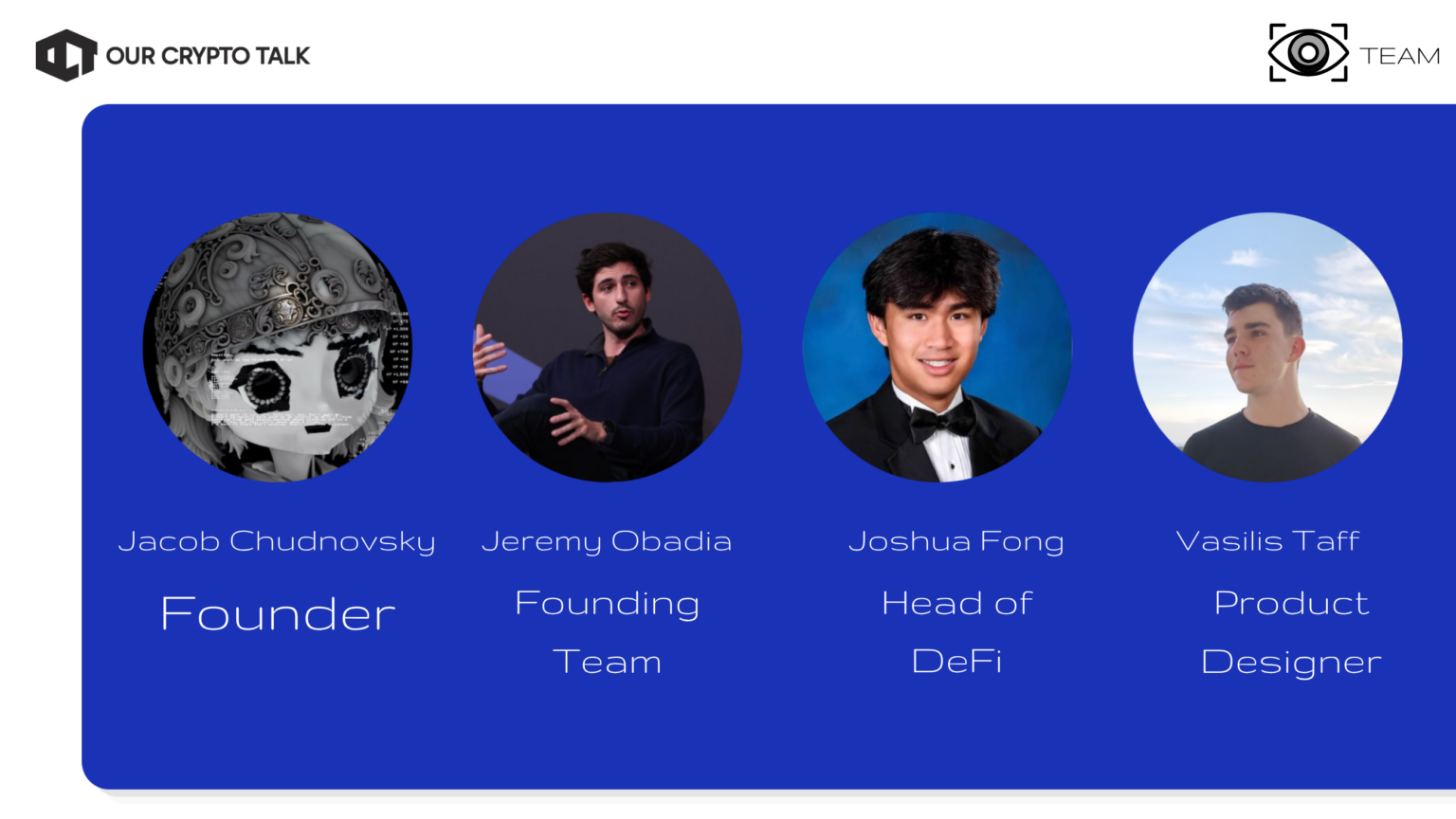

3Jane was founded by Jacob Chudnovsky, a DeFi builder with direct experience in derivatives, lending, and unsecured credit infrastructure.

Before launching 3Jane in October 2024, Chudnovsky spent more than three years at Aevo, one of crypto’s leading derivatives platforms. He joined as a Founding Engineer in 2021, where he helped build structured products and lending strategies that scaled to more than $300 million TVL. He also worked on an onchain options OTC desk that processed over $100 million in notional volume.

Jacob later became Head of Strategy at Aevo. During that period, he helped grow the exchange to more than $100 million in daily notional trading volume and led an onchain unsecured revolving credit facility business that reached approximately $75 million TVL and originated more than $50 million in loans. That experience is particularly relevant because unsecured lending is now the core problem 3Jane is trying to solve.

Prior to Aevo, Chudnovsky worked as a Software Engineer Intern at Credit Karma, giving him exposure to consumer credit systems before entering crypto full-time.

The broader 3Jane team combines expertise across protocol engineering, product design, credit risk, and DeFi infrastructure. Public team members include Jeremy Obadia, Joshua Fong (Head of DeFi), Vasilis Taff (Product Design), and Evgeny Boxer (Senior Frontend Engineer).

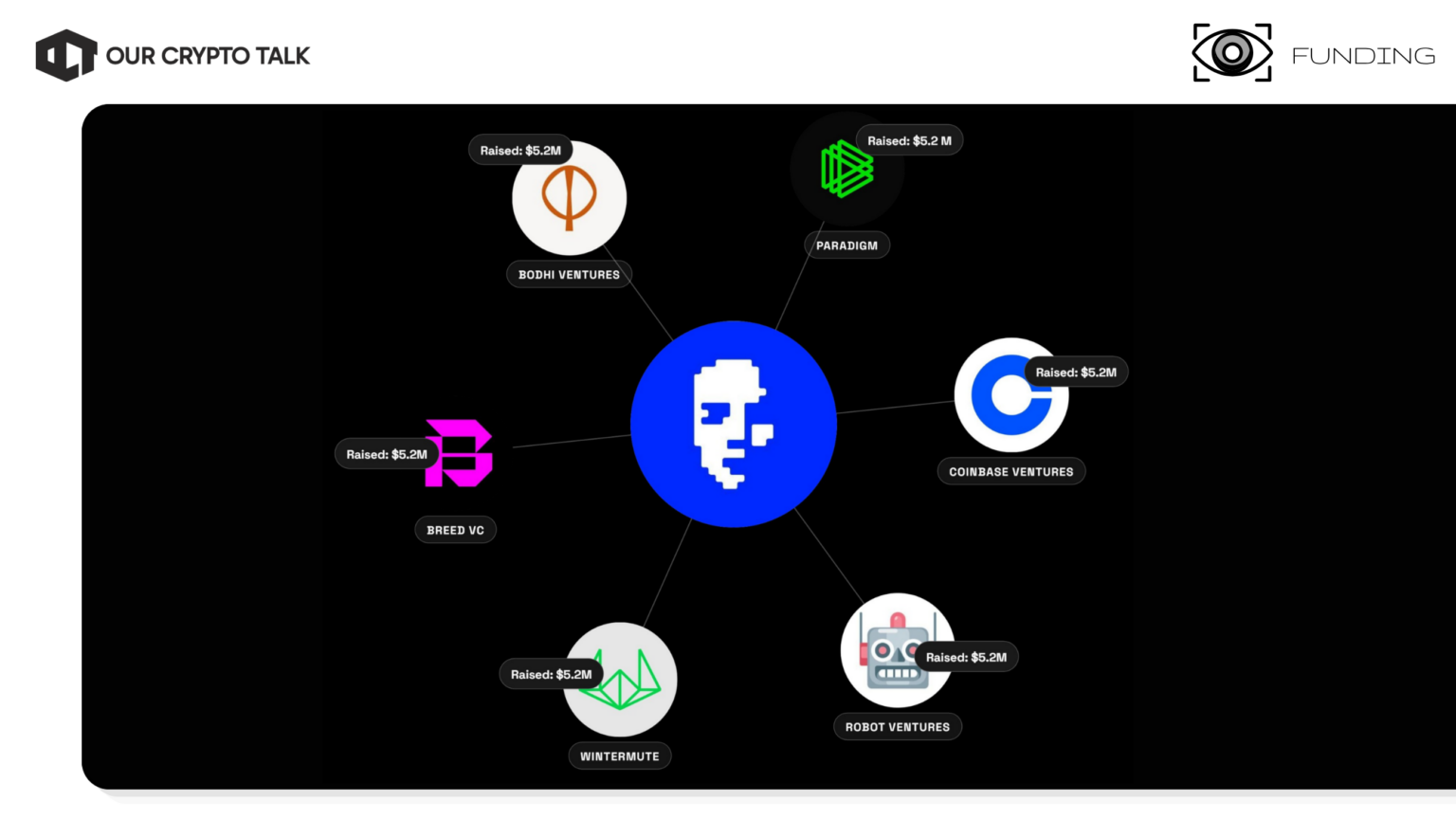

3Jane raised a $5.2 million seed round led by Paradigm in June 2025, with participation from Robot Ventures and Coinbase Ventures.

The headline investor is Paradigm. The firm has built a reputation for backing technically ambitious crypto infrastructure projects and remains one of the most respected investors in the industry. Its involvement provides a strong signal that experienced investors believe the unsecured credit opportunity is worth pursuing.

The size of the round is also appropriate for the stage of development. It provides sufficient runway to build underwriting systems, expand lending facilities, and reach meaningful adoption without creating unrealistic valuation expectations.

The investor mix adds credibility from multiple angles. Paradigm contributes deep protocol expertise. Coinbase Ventures offers ecosystem reach and strategic relationships. Robot Ventures has a strong track record of identifying early-stage infrastructure projects before they become mainstream.

Perhaps the most important signal is timing. The round arrived before unsecured credit became a major narrative within crypto markets. Investors backed the underlying thesis rather than chasing a trend.

For a project attempting one of the most difficult challenges in crypto finance, institutional support matters. Capital alone does not guarantee success, but it significantly improves the odds that 3Jane can build, iterate, and prove whether permissionless unsecured credit can work at scale.

Yes. 3Jane has a live mainnet product that users can access today.

The protocol opened public deposits and launched its liquidity mining program in June 2026. Through the app, users can mint USD3, stake into sUSD3, provide liquidity across partner protocols, and participate in the broader credit ecosystem.

Unlike many pre-token projects, 3Jane is not operating on a testnet. The protocol is live on Ethereum mainnet with real capital deployed into real credit facilities.

The strongest proof comes from its lending partnerships. 3Jane has already funded a $10 million senior warehouse facility with LendSwift, backed by approximately 15,000 U.S. consumer installment loans. It has also completed an $8.5 million whole-loan purchase facility with Slope covering SMB credit lines and BNPL receivables.

These are not pilot programs or future commitments. Capital is already deployed and generating yield.

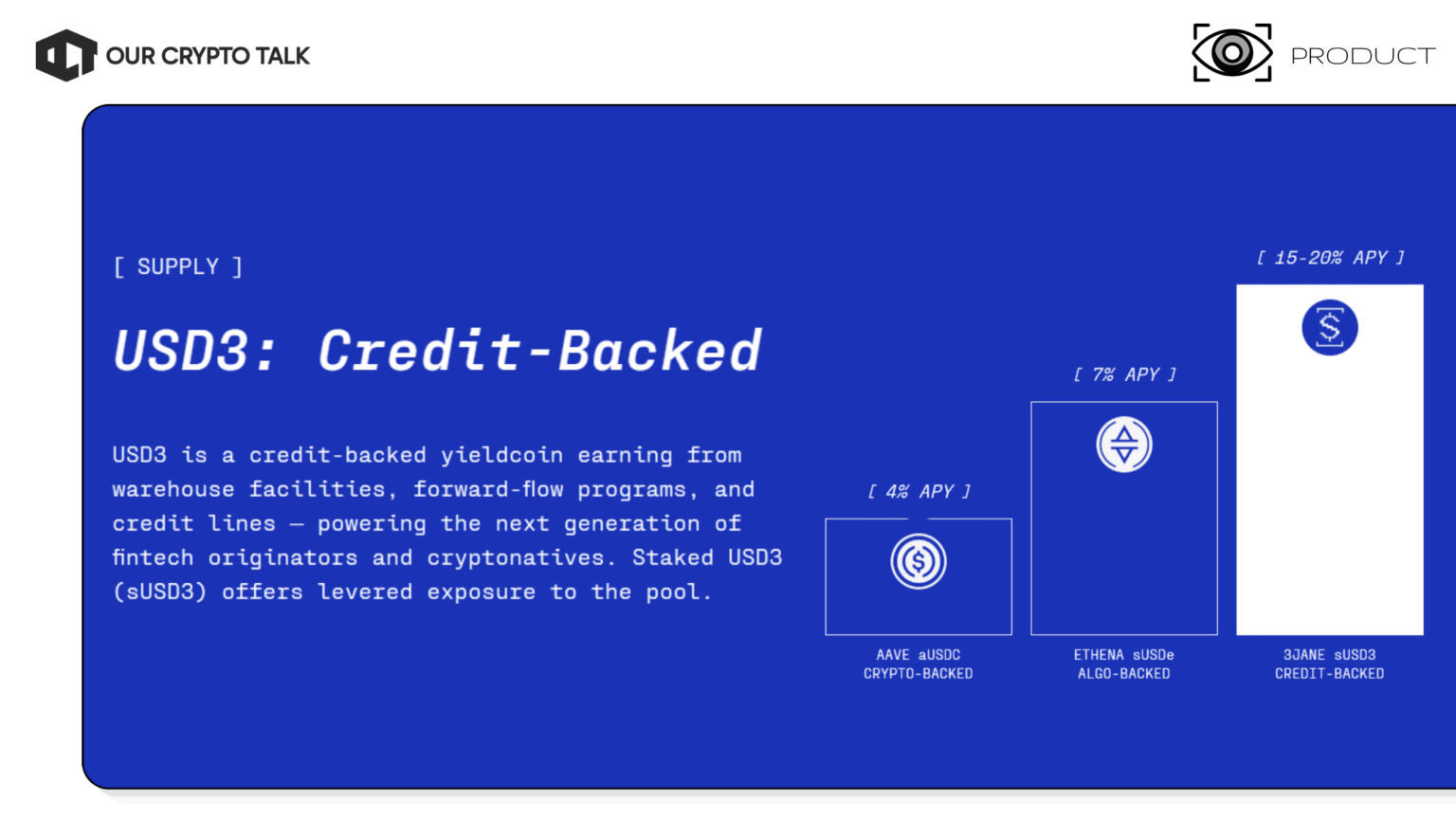

At launch, USD3 carried a $50 million supply cap to manage risk while the protocol scales. Yield rates have remained competitive versus other stablecoin strategies, with USD3 targeting senior credit-backed returns and sUSD3 offering higher-risk, higher-yield exposure.

The liquidity mining program is also live. Users earn locked JANE tokens by minting USD3, staking into sUSD3, borrowing through the protocol, or providing liquidity on supported venues.

The bottom line is simple. 3Jane has moved beyond the whitepaper stage. Users can interact with the protocol, deploy capital, earn yield, and participate in the token ecosystem today.

The most important traction metrics are the ones that cost participants real money.

For 3Jane, that starts with deployed credit.

The protocol has already funded a $10 million warehouse facility with LendSwift and an additional $8.5 million facility with Slope. Together, these facilities represent more than $18 million in live credit exposure backed by real-world borrowers and real repayment activity.

That matters because these assets generate the yield that supports USD3 and sUSD3 holders.

The protocol also launched with a controlled USD3 supply cap of $50 million. Rather than chasing rapid TVL growth, the team has prioritized measured expansion while testing underwriting and risk systems under real market conditions.

The liquidity mining program provides another meaningful signal. The first rewards epoch distributed roughly 1.35 million JANE tokens across core protocol activities, including USD3 deposits, sUSD3 staking, and partner liquidity pools.

What does not matter?

Follower counts. Discord memberships. Testnet wallet numbers. None of those metrics require capital, risk, or commitment.

3Jane has largely avoided those vanity metrics. There was no heavily marketed presale, no node sale campaign, and no inflated testnet participation narrative.

The strongest signal remains the same: the protocol is already deploying capital into real credit facilities. In a market filled with narrative-driven projects, funded credit exposure provides a far more reliable measure of progress than social media growth.

JANE serves as the protocol’s governance and incentive token.

The current structure differs from many traditional token launches because the final token supply has not yet been fixed. During the ongoing liquidity mining phase, participants earn locked JANE rewards that become transferable after the final mint event scheduled for 2026.

The current design heavily favors active participants. During the liquidity mining phase, 100% of token emissions flow to users providing liquidity, minting USD3, staking into sUSD3, or otherwise contributing capital to the protocol.

The first reward epoch distributed approximately 1.35 million JANE across core pools.

However, several important questions remain unanswered.

The team has not yet published a complete allocation breakdown covering founders, employees, investors, advisors, treasury reserves, or ecosystem incentives. Vesting schedules and unlock timelines also remain undisclosed.

That makes FDV analysis difficult.

Investors are effectively underwriting both protocol growth and future token supply. Until the final tokenomics framework is released, participants face uncertainty around dilution and long-term ownership structure.

The current design is relatively community-friendly because emissions flow directly to active users. However, the absence of a full allocation table and vesting schedule remains the biggest tokenomics risk.

The simplest way to get early exposure is to use the protocol itself.

Users can mint USD3 through the application and stake into sUSD3 to begin earning yield and accumulating locked JANE rewards. These actions currently represent the highest-signal participation because they require real capital deployment.

A second option is providing liquidity through supported platforms such as Curve, Morpho, Pendle, and Frax. These pools are included in the liquidity mining program and receive JANE emissions alongside protocol-native activities.

Rewards accrue continuously and become claimable every seven days. However, all rewards remain locked until the final token mint event expected in 2026.

That distinction matters.

This is not a social quest campaign where users complete simple tasks for speculative points. Meaningful participation requires deploying capital and accepting both credit risk and token risk.

The upside is that participants earn real yield while accumulating governance tokens. The downside is that rewards remain illiquid until transferability is enabled.

The biggest advantage for early users is timing. The protocol remains in its capped growth phase, and all emissions currently flow toward active participants. As TVL expands, competition for rewards will likely increase.

For investors who already believe in the onchain credit thesis, the most direct strategy is straightforward: use the product, earn yield, accumulate JANE, and monitor future tokenomics announcements closely.

3Jane offers one of the more compelling risk-reward setups in the current RWA and credit category, but it is not a passive airdrop farm.

Participants deploy real stablecoin capital into a live credit protocol that is already funding real-world lending facilities. In return, they earn yield from those facilities while accumulating locked JANE rewards through the liquidity mining program.

That combination matters. Most farming opportunities force users to choose between yield and token incentives. 3Jane offers both. USD3 currently targets senior credit-backed returns, while sUSD3 provides higher-risk, higher-yield exposure. At the same time, all current JANE emissions flow to active participants.

The quality of the rewards is also higher than typical points programs. Users are earning governance tokens tied to a live protocol with funded lending facilities rather than speculative points attached to a future product.

The trade-off is duration. JANE remains locked until the final mint event in 2026. Participants therefore take protocol risk, credit risk, and token risk simultaneously.

There is also no public token sale. The only way to gain exposure today is through the protocol itself.

For investors already comfortable allocating capital to credit-backed yield strategies, the expected value looks attractive. The protocol has real lending activity, meaningful institutional backing, and a rewards structure that favors early users.

For investors seeking quick liquidity or short-term speculation, the opportunity is less compelling.

The conclusion is straightforward. The strongest reason to participate is the yield. JANE should be viewed as additional upside rather than the primary investment thesis.

Credit protocols fail for practical reasons, not narrative reasons.

The largest risk is credit performance. 3Jane generates yield from real consumer and business loans. If default rates rise or lending partners underperform, returns can fall and losses can increase. Junior capital in sUSD3 absorbs that risk first.

Competition is another challenge. Aave and Morpho dominate crypto lending, while Maple, Goldfinch, and Centrifuge already operate in the RWA credit sector. If 3Jane struggles to scale loan origination or maintain attractive yields, growth could slow significantly.

Regulation remains a meaningful uncertainty. The protocol relies on access to credit data, underwriting infrastructure, and collections processes tied to traditional financial systems. Changes in lending regulations or data-access requirements could affect growth.

Tokenomics also deserve attention. The final JANE supply remains variable, and the team has not yet published a complete allocation breakdown, vesting schedule, or unlock timeline. Until those details arrive, participants face uncertainty around future dilution.

Execution risk should not be ignored either. Scaling unsecured credit is far more difficult than scaling collateralized crypto lending. A major default event, underwriting mistake, legal challenge, or smart contract exploit could damage confidence quickly.

The technology is differentiated. The risk lies in proving that the model can scale safely over time.

The most important catalyst is the final JANE mint event expected in 2026.

That event will determine the final token supply, activate transferability, and clarify the long-term ownership structure of the protocol. It is also likely to coincide with expanded governance functionality and broader market participation.

Before then, the market still needs several key pieces of information.

The biggest missing variable is tokenomics transparency. Investors are waiting for a complete allocation table, vesting schedules, investor unlocks, and team lockups. Those details will have a major impact on how the market values JANE.

Business growth is the second major catalyst. Additional lending facilities, new originator partnerships, and growth beyond the initial USD3 cap would provide evidence that demand exists beyond the first deployment phase.

Performance matters as well. The protocol must demonstrate that it can maintain attractive yields while managing credit risk across multiple lending partners.

Investors therefore face a simple choice.

Participate now if the goal is earning yield and accumulating JANE while emissions remain concentrated among early users. Wait if tokenomics transparency and long-term supply certainty matter more than early positioning.

FARM

3Jane has already cleared the most important hurdle facing early-stage crypto projects: it shipped a real product.

The protocol operates on mainnet, funds real-world credit facilities, generates real yield, and has institutional backing from one of the strongest investor groups in crypto. That immediately separates it from projects that remain dependent on future promises.

The investment case is strongest for users already interested in credit-backed yield. Those participants earn returns today while accumulating exposure to a future governance token.

The structure also favors conviction. Meaningful rewards require real capital deployment, which limits speculative participation and reduces the impact of low-quality farming activity.

The biggest unanswered question remains tokenomics.

The team has not yet released a complete allocation breakdown, insider vesting schedule, or unlock timeline. Those details will ultimately determine whether JANE launches with healthy long-term incentives or excessive dilution risk.

For now, the protocol earns a FARM rating because the product exists, the yield is real, and the core thesis is already being tested in production.

The milestone that could change the rating is simple: the release of full tokenomics and vesting details.

If those numbers are reasonable, the thesis strengthens. If they are not, the rating should be revisited regardless of how strong the underlying protocol appears.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.

10 Crypto Skills Quietly Printing Money While Everyone Else Gets Liquidated

Are Exchange Tokens a Good Investment in 2026? CEX vs DEX

Zcash vs Monero vs Dash: Best Privacy Coin in 2026?

Helium Worked in America. Can Dabba Win India?

10 Crypto Skills Quietly Printing Money While Everyone Else Gets Liquidated

Are Exchange Tokens a Good Investment in 2026? CEX vs DEX

Zcash vs Monero vs Dash: Best Privacy Coin in 2026?

Helium Worked in America. Can Dabba Win India?