Loading Search...

Author: Chirag Sharma

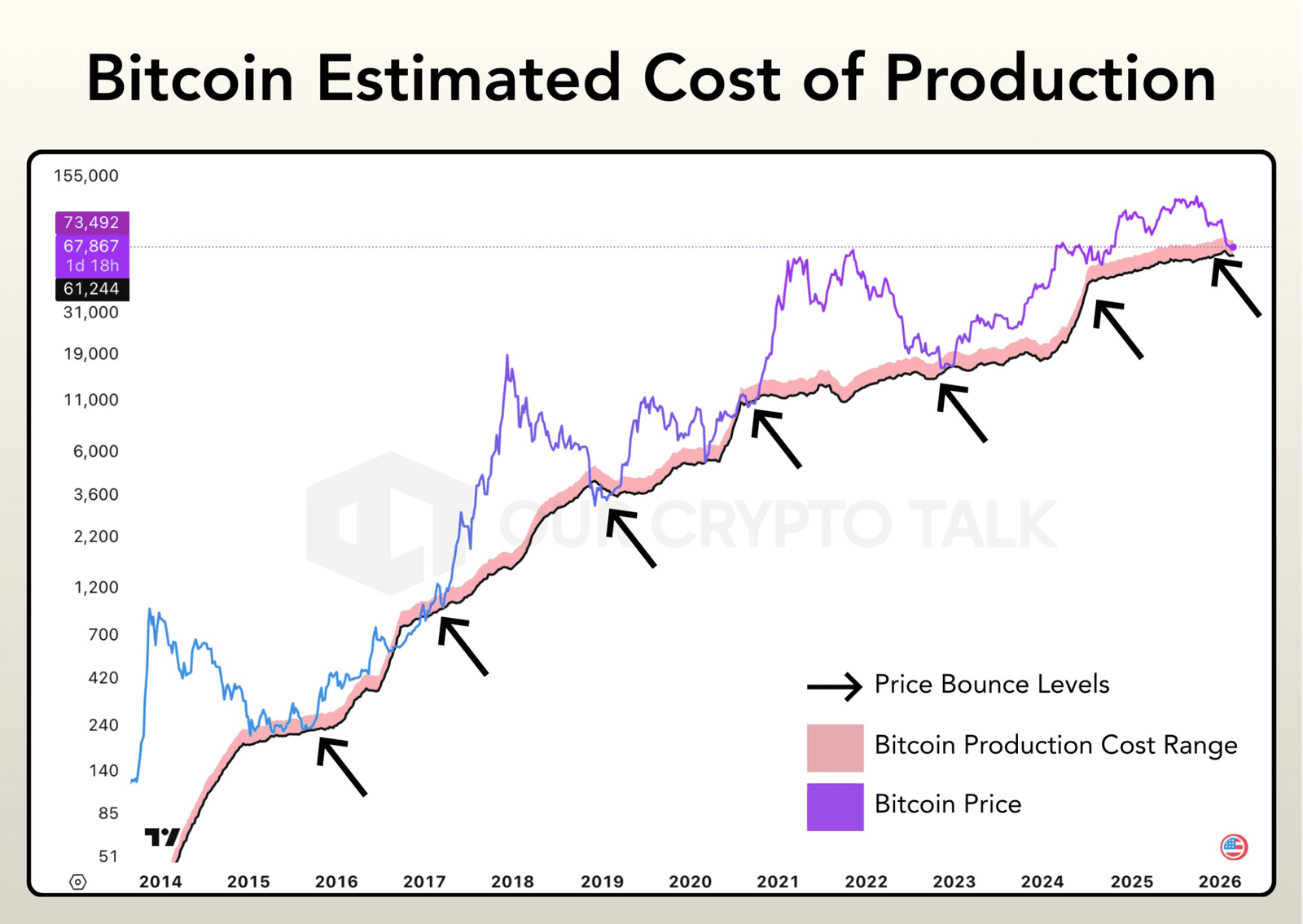

Bitcoin is trading near $68,800 as of March 2026. At the same time, the average cost to mine one coin sits between $83,000 and $87,000. That gap is not marginal. It means miners are losing roughly $19,000 per Bitcoin they produce. This is the core of the Bitcoin Miner Crisis.

It has already triggered one of the sharpest difficulty drops of the year, forced public miners to liquidate reserves, and pushed the sector into its most stressed phase since the 2022 bear market. Yet beneath this pressure lies a more important shift. This is not just a breakdown in mining economics. It is a structural reset that has historically preceded major market moves.

To understand the Bitcoin Miner Crisis, the starting point is the 2024 halving. When block rewards dropped from 6.25 BTC to 3.125 BTC, miner revenue was cut in half overnight. Costs did not adjust alongside it.

Electricity prices remained elevated across key mining regions. Hardware costs continued rising as newer, more efficient ASICs became necessary to stay competitive. Cooling infrastructure, maintenance, and operational overhead also increased. The combination created a situation where revenue fell sharply while expenses stayed relatively constant.

The result is a broken equation.

Today, even efficient miners operating at around $0.06 per kWh struggle to remain profitable when Bitcoin trades below $75,000. Older machines are in far worse shape. Many legacy ASIC fleets now operate at a consistent loss, with some machines losing $20 to $30 per day. Transaction fees, once expected to offset the halving impact, have not provided sufficient relief. Network activity has slowed during this consolidation phase, keeping fees relatively low. This has removed a key revenue buffer that miners relied on in previous cycles.

As a result, survival has replaced accumulation as the primary objective. Major players such as Marathon Digital Holdings, Riot Platforms, and Core Scientific have already adjusted strategy. Instead of holding mined Bitcoin, they are increasingly selling it to maintain liquidity. When production costs exceed market prices by over 20 percent, ideology takes a back seat to balance sheet management.

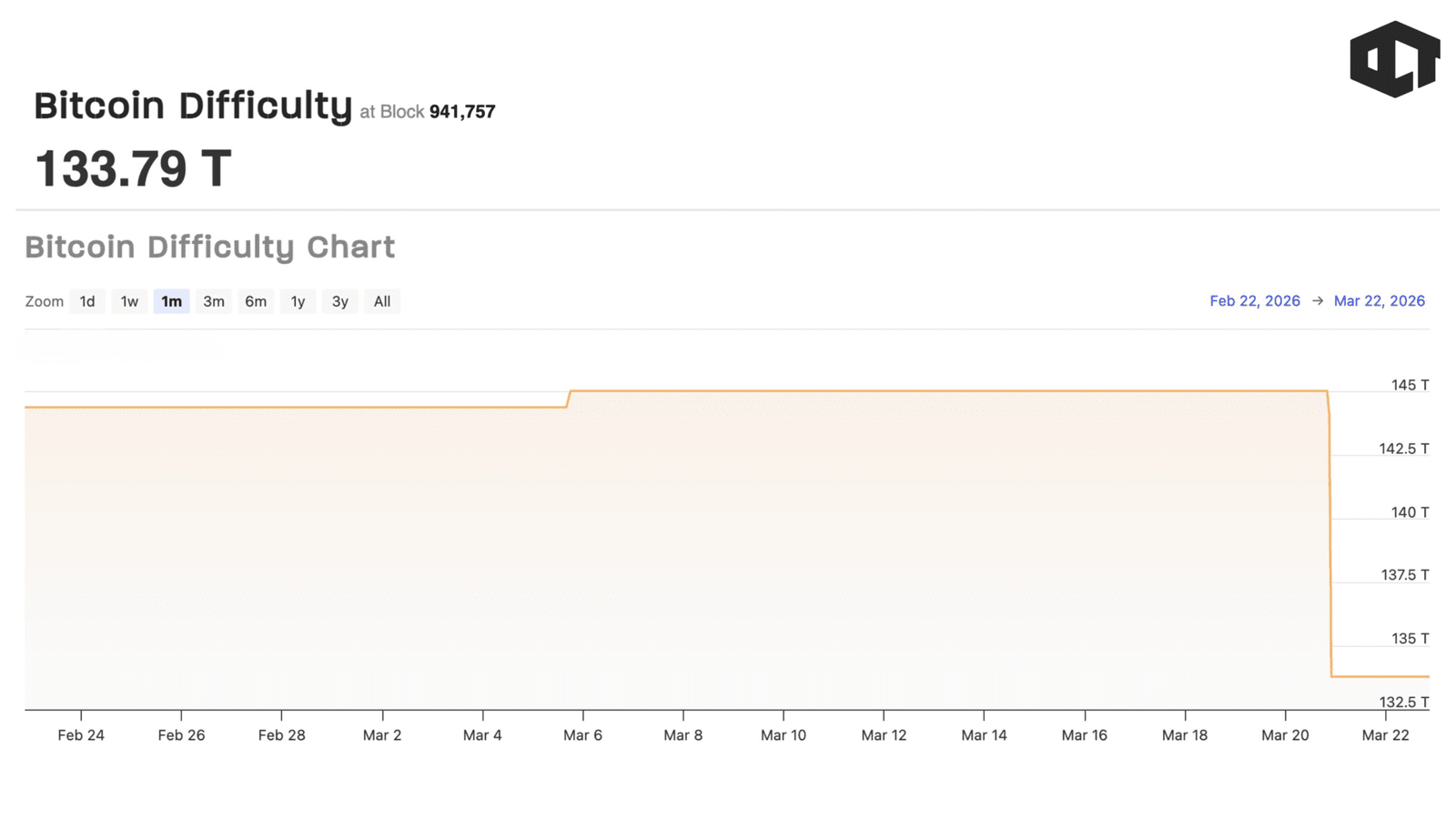

On March 21, 2026, Bitcoin’s mining difficulty dropped by 7.76 percent. This marked one of the largest adjustments since the 2022 bear market and immediately signaled that miners were shutting down unprofitable operations.

At first glance, such a drop appears negative. In reality, it reflects Bitcoin’s built-in self-correction mechanism.

As miners exit the network, total hash rate declines. The protocol responds by lowering difficulty so that block production remains consistent. This adjustment redistributes rewards among the remaining miners, improving their profitability.

Following the drop, hashprice increased by approximately 8 to 9 percent. Surviving miners saw an immediate improvement in revenue per unit of hash rate. Machines that were previously deep in the red moved closer to breakeven levels.

However, the context matters. This adjustment did not occur in isolation. Average block times had stretched beyond 12 minutes in the previous cycle, indicating that miners were already unplugging machines at scale. The difficulty drop simply confirmed what was already happening behind the scenes.

The Bitcoin Miner Crisis is therefore both a distress signal and a cleansing process. It removes inefficient participants and allows stronger operators to consolidate market share. Historically, these moments have been critical inflection points.

While miners are under pressure, institutional demand is moving in the opposite direction.

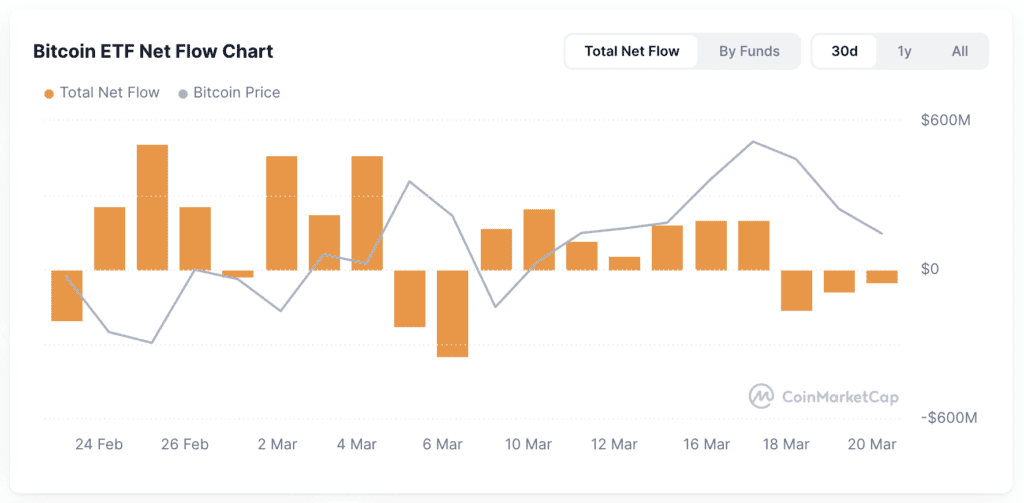

Spot Bitcoin ETFs have continued to attract strong inflows throughout early 2026. Products from BlackRock and Fidelity Investments are consistently absorbing large volumes of Bitcoin from the market. Over recent weeks, ETF inflows have exceeded $2 billion. On peak days, inflows have crossed $500 million. This demand significantly outweighs the daily supply of newly mined Bitcoin.

This creates a direct supply conflict.Miners are selling nearly all of their production to stay operational. Public companies alone have offloaded tens of thousands of BTC over recent months. At the same time, ETFs are accumulating aggressively, reducing available supply on exchanges. This dynamic forms the core of the Bitcoin Miner Crisis: forced selling versus structural demand.

The price action reflects this tension. Bitcoin tested resistance near $74,000 but failed to break through, largely due to continuous miner selling. At the same time, ETF demand has prevented deeper downside, keeping price supported near current levels. If ETF inflows remain consistent, they can absorb miner selling entirely. This would tighten supply and potentially trigger upward momentum. If inflows slow, miner selling could dominate, pushing prices lower. The balance between these two forces will define Bitcoin’s next major move.

The current Bitcoin Miner Crisis closely resembles previous market cycles. In 2018, after the ICO bubble collapsed, Bitcoin fell from $20,000 to $3,200. Mining became unprofitable, hash rate declined sharply, and miners were forced to liquidate holdings. That period marked the cycle bottom.

A similar pattern emerged in 2022 following the FTX collapse. Bitcoin dropped to around $16,000, mining margins turned negative, and difficulty experienced one of its largest downward adjustments. Miners again sold aggressively.

In both cases, the peak of miner capitulation coincided with the market bottom.

The current cycle shows comparable signals. The hash ribbon indicator, which measures miner stress, has remained inverted for months. This suggests prolonged capitulation, similar to previous cycles.However, there is one major difference in 2026.

Spot ETFs now exist. Previous cycles lacked this level of institutional demand. Today, ETFs provide a consistent source of capital that can absorb supply during periods of stress. This introduces a structural support mechanism that did not exist in earlier bear markets. While history does not guarantee outcomes, the parallels are difficult to ignore.

The current environment is forcing a reset across the mining industry.

Not all participants will survive. The sector is entering a consolidation phase where only the most efficient operators remain competitive. Surviving miners will likely share three key characteristics.

First, access to low-cost energy is critical. Operators with electricity costs below $0.05 per kWh maintain a significant advantage. Regions with abundant hydroelectric power or access to flared gas continue to offer favorable conditions.

Second, hardware efficiency is becoming increasingly important. New-generation ASIC machines deliver better performance per unit of energy. Older equipment is rapidly becoming obsolete and unprofitable.

Third, diversification is emerging as a strategic necessity. Some mining companies are repurposing infrastructure for AI data centers or high-performance computing workloads. These alternative revenue streams provide stability during periods of mining stress.

Larger players with strong balance sheets are also better positioned to survive. They can absorb short-term losses and expand market share as smaller competitors exit.

This process ultimately strengthens the network by concentrating hash rate among more efficient operators.

Despite the immediate challenges, the Bitcoin Miner Crisis carries long-term positive implications. The protocol is functioning as intended. Inefficient miners are forced out, reducing excess competition and lowering selling pressure over time.

As weaker players exit, the remaining miners operate with improved margins. This allows them to hold a greater portion of their production instead of selling everything to cover costs. At the same time, ETF demand continues to absorb available supply.

This combination creates the potential for a supply shock. If demand remains strong while selling pressure declines, price can move rapidly upward. This pattern has repeated across previous cycles.

Periods of extreme miner stress have historically preceded strong recoveries. The current environment shows similar characteristics, with the added factor of institutional demand.

Several key indicators will determine how the Bitcoin Miner Crisis evolves. Bitcoin price levels remain critical. A sustained move above $75,000 would significantly improve mining profitability and reduce forced selling. ETF inflows are equally important. Consistent daily inflows above $150 million could absorb all new supply, creating upward pressure on price. Future difficulty adjustments will provide insight into miner health. Continued declines indicate ongoing stress, while stabilization suggests recovery. Hash rate trends will also signal whether miners are returning to the network. These metrics together will define the transition from stress to recovery.

The Bitcoin Miner Crisis in 2026 represents one of the most challenging environments for miners in recent history. Production costs exceed market prices, forcing widespread selling and triggering significant difficulty adjustments.

Yet this is not an anomaly. It is a recurring phase in Bitcoin’s economic cycle. The difference today lies in structural demand. ETFs are absorbing supply at scale, providing a stabilizing force that previous cycles lacked. This creates a unique setup. While miners are under pressure, the broader market is supported by institutional inflows.

The result is a transition phase rather than a collapse. Historically, such phases have marked the foundation for the next bull run. The current crisis may follow the same path.

Qubic Dogecoin Mining Explained: What It Is and Why It Matters

Bitcoin Miner Crisis: Trigger for the Next BTC Move

Meta Metaverse Failure Explained: How $80 Billion Burned on a Future That Never Arrived

Biggest Crypto Hacks of All Time : $6B+ Stolen and Counting

Qubic Dogecoin Mining Explained: What It Is and Why It Matters

Bitcoin Miner Crisis: Trigger for the Next BTC Move

Meta Metaverse Failure Explained: How $80 Billion Burned on a Future That Never Arrived

Biggest Crypto Hacks of All Time : $6B+ Stolen and Counting