Avici Review ( $AVICI )

Avici Review: A crypto-native neobank offering self-custodial wallets, stablecoin payments, and Visa cards to bring everyday banking onchain.

Author: Akshat Thakur

Avici Review Introduction

Global finance is still dominated by centralized banking systems that control custody, payments, and credit infrastructure. While cryptocurrencies introduced self-custody and permissionless value transfer, the ecosystem still lacks the everyday banking tools people rely on: credit cards, fiat accounts, and payment rails accepted by millions of merchants. In this Avici Review, we examine how global finance is still dominated by centralized banking systems that control custody, payments, and credit infrastructure.

Most crypto users still depend on traditional banks to convert fiat, make payments, or access credit. This dependency creates friction and contradicts the original vision of decentralized finance.

This Avici Review examines Avici, a crypto-native financial platform attempting to build an internet-native neobank. The project connects fiat infrastructure with self-custodial crypto wallets, enabling users to spend, receive, and manage funds without giving up ownership of their assets. Instead of forcing users to abandon traditional financial rails entirely, Avici integrates them with blockchain infrastructure. The platform provides crypto credit cards, fiat onramps, smart wallets, and payment tools designed to make stablecoins usable for everyday financial activity.

Problem Statement

- Crypto Still Lacks Everyday Banking Infrastructure: Despite rapid growth, most cryptocurrencies are still primarily used for trading or speculation rather than daily financial activity. Essential banking tools such as credit, payment cards, and salary deposits remain tied to traditional financial institutions.

- Self-Custody Creates Usability Challenges: Managing private keys and wallet security can be complex for mainstream users. Losing keys or making mistakes during transactions often results in irreversible loss of funds.

- Fiat and Crypto Systems Remain Fragmented: Moving between fiat currencies and digital assets often requires multiple intermediaries such as exchanges or payment providers. These steps create delays, fees, and friction for users trying to interact with both systems.

- Merchant Acceptance of Crypto Is Limited: Even though stablecoins are growing rapidly, most merchants still operate entirely on traditional payment rails. This means crypto holders cannot easily spend their assets in everyday situations.

- Onchain Credit Infrastructure Is Still Underdeveloped: Traditional financial systems rely heavily on credit scoring and lending infrastructure. Crypto ecosystems currently lack mature systems for underwriting loans or tracking creditworthiness onchain.

Solutions Provided by Avici

- Crypto-Powered Credit Cards: Avici provides Visa credit cards that allow users to spend using their crypto holdings while merchants receive fiat payments through traditional payment networks.

- Self-Custodial Wallet Infrastructure: The platform uses a smart contract wallet architecture that replaces traditional private keys with passkeys and multi-factor authentication. This design improves usability while maintaining self-custody.

- Integrated Fiat Onramps Users can open virtual USD and EUR accounts to receive bank transfers via traditional payment rails such as ACH, SEPA, or wire transfers. Incoming fiat is automatically converted into stablecoins and credited to the wallet.

- Stablecoin Spending Infrastructure: Funds held in crypto can be used directly through credit card spending balances, enabling stablecoins to function as practical payment instruments across global merchants.

- Cross-Chain Wallet Support: The wallet supports multiple blockchain networks including EVM chains and Solana, enabling transfers, swaps, and payments across different ecosystems.

Problem–Solution Overview

Technology & Architecture

Technology & Architecture

Smart Contract Wallet Design

User Experience Layer

Multi-Chain Infrastructure

Fintech-Style Self-Custody

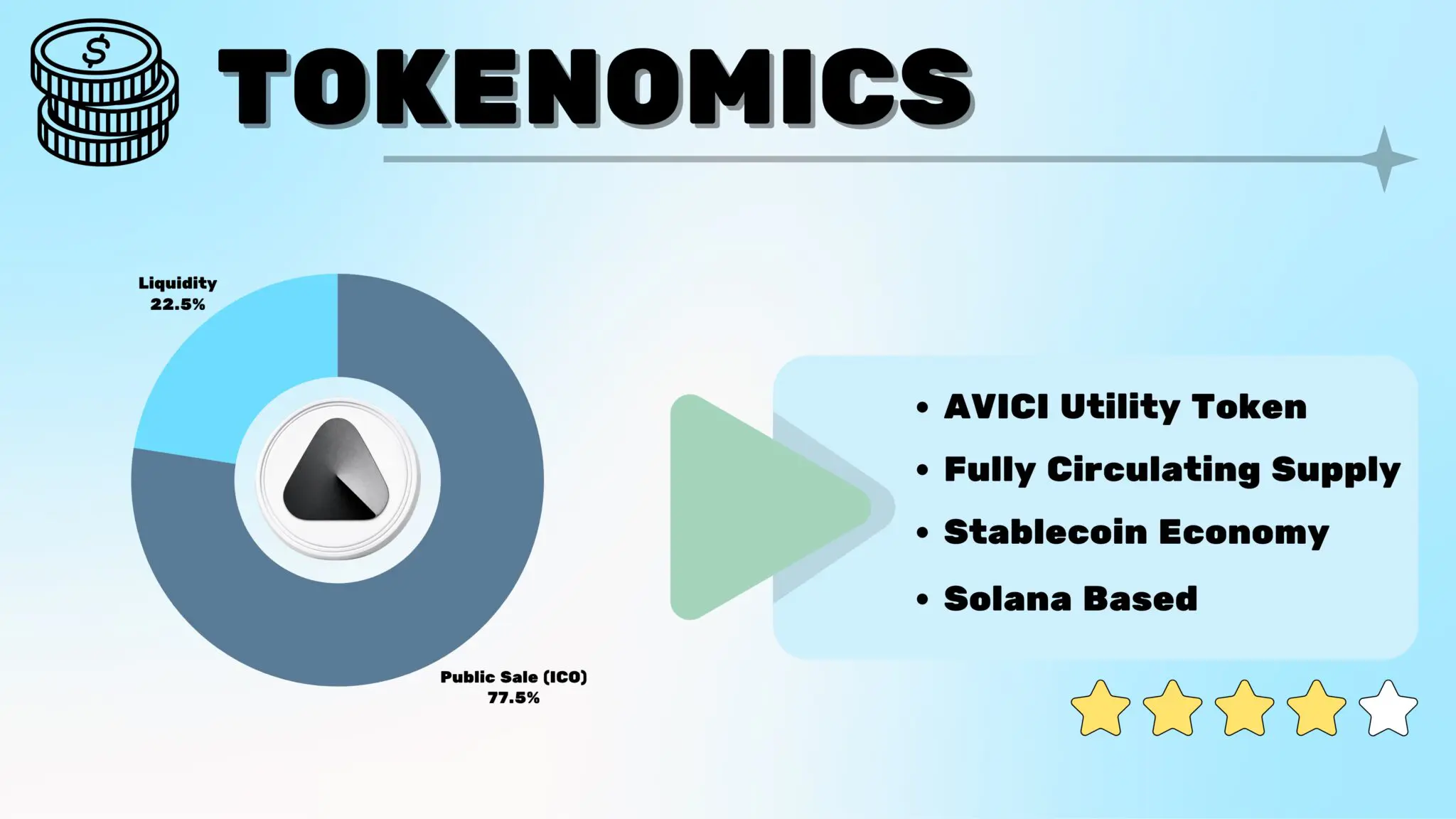

Tokenomics

Avici introduces the AVICI token as the utility and economic coordination asset of the Avici ecosystem. The protocol operates on a Solana-native environment, enabling seamless interoperability for crypto payments and credit while aligning incentives with long-term protocol growth, sustainability, and bridging fiat and crypto markets.

Token Overview

- Symbol: AVICI

- Total Supply: 12,900,000 AVICI (as of March 2026)

- Standard: SPL (Solana-native)

- Decimals: 6

The AVICI token functions as the utility, coordination, and value accrual asset of the Avici protocol. It enables ecosystem participation, payments, and access to incentives and rewards.

Token Allocation

- Public Sale (ICO): 77.52% (10,000,000 AVICI, allocated through public sale with no vesting).

- Liquidity: 22.48% (Allocated to provide initial liquidity on exchanges).

- Released / Circulating Supply: ~100% (Freely circulating supply, as nearly all tokens are in circulation with no locked allocations).

Avici currently focuses primarily on product infrastructure rather than speculative token economics. The ecosystem is built around stablecoin usage and financial services rather than a traditional utility token model.

Stablecoins such as USDC are used for card balances, spending, and transfers within the platform. Deposits made to card escrow contracts generate corresponding fiat credit balances that can be used for payments.

This design positions stablecoins as the core economic layer of the ecosystem, aligning with the platform’s goal of enabling everyday crypto-based banking.

Market Performance

📊 Market Performance

Exchange Listings:

Liquidity:

Team & Governance

- Co-Founder: Sitaram Kakarlamudi

- Co-Founder & CTO: Abhishek Tiwari

- Product Growth: Yash Kapur

- Blockchain Developer: Arpit Singh Bhatia

Avici operates with a product-driven approach focused on building infrastructure for internet-native banking. The project positions itself as part of a broader movement toward decentralized financial systems where users retain full control of their assets.

The long-term governance vision involves expanding the ecosystem toward decentralized coordination while maintaining compliance where required for payment infrastructure.

Avici Review Project Analysis

Comparative Overview

- Avici vs Traditional Neobanks: Traditional neobanks provide convenient digital banking but retain custody of user funds and rely entirely on centralized financial infrastructure. Avici attempts to replicate similar usability while allowing users to maintain control of their assets onchain.

- Avici vs Crypto Exchanges: Exchanges offer onramps and trading but are not designed to function as everyday financial platforms. Avici focuses instead on payments, banking functionality, and financial infrastructure.

- Avici vs DeFi Platforms: Most DeFi protocols focus on trading, liquidity, or lending markets. Avici positions itself closer to a financial operating system that combines banking services with blockchain infrastructure.

Strengths

- Integrated fiat and crypto financial rails

- Self-custodial wallet architecture

- Global merchant compatibility through Visa

- Cross-chain asset support

- Focus on real-world financial utility

Challenges

- Reliance on traditional payment infrastructure partners

- Regulatory complexity around global financial services

- Competition from fintech neobanks and crypto wallets

- User education required for self-custodial systems

Avici vs Crypto Neobank & DeFi Banking Protocols

| Project | Core Focus | Execution Architecture | Programmability | Token Utility | Notes |

|---|---|---|---|---|---|

|

| Decentralized neobank on Solana for self-custodial crypto banking | Smart contracts on Solana | Full (Rust-based) | Governance via DAO with futarchy | Raised $3.5M and refunded 90%; app live on iOS and Android; revenue from fees; partnership with MoonPay; virtual accounts plus physical and virtual cards; launched Oct 2025 |

|

| Liquid restaking and yield-bearing stablecoin infrastructure | Smart contracts on Ethereum and multichain deployments | Full (EVM) | Governance, staking (ETHFI) | Strong monthly spend metrics; yield-focused product suite; multichain strategy |

|

| Modular Layer-2 for DeFi and real-world assets | Mantle Network on Ethereum Layer-2 | Full (EVM) | Governance, staking (MNT) | Leads the neobank category narrative; compliance-focused; supports RWA vault structures |

|

| Decentralized lending and borrowing | Smart contracts on Algorand | Full (TEAL) | Governance (FOLKS) | Non-custodial design with focus on emerging market credit access |

|

| Yield optimization and DeFi tooling | Smart contracts on multichain networks | Full (EVM) | Governance (LMTS) | Auto-compounding vault strategies with ongoing multichain expansion |

|

| High-throughput Layer-1 for payments | Plasma consensus with Proof-of-Stake | Full (EVM-compatible) | Fees, staking (XPL) | Low-fee payment focus; enterprise adoption narrative; supply-chain-oriented integrations |

Avici Review Conclusion

The emergence of crypto-native financial platforms reflects a broader shift in how people think about money, custody, and financial access. While blockchain technology introduced the concept of self-sovereign assets, the surrounding financial infrastructure has remained incomplete. Everyday financial tools such as payment cards, bank accounts, and credit systems are still largely controlled by traditional institutions.

Avici attempts to address this gap by combining self-custodial blockchain infrastructure with familiar fintech-style services. Through smart contract wallets, crypto-backed credit cards, and fiat onramp accounts, the platform aims to make stablecoins and digital assets usable for everyday financial activity rather than limiting them to trading or speculation.

Rather than forcing users to abandon traditional financial systems entirely, Avici integrates with existing payment rails such as Visa and bank transfers. This hybrid approach allows crypto holders to interact with the global financial system while maintaining ownership of their assets onchain. If executed effectively, it could lower the barriers that currently prevent crypto from functioning as practical money.

Ultimately, Avici represents an experiment in building a new form of internet-native banking infrastructure. By blending decentralized custody with global payment compatibility, the project aims to move crypto closer to fulfilling its original promise: a financial system where individuals can spend, save, and manage wealth without relying on centralized banks.

TL;DR

- Internet-native crypto neobank.

- Self-custodial smart wallet infrastructure.

- Crypto credit cards usable at global Visa merchants.

- Fiat onramps convert bank transfers into stablecoins.

- Built for spending, saving, lending, and onchain banking.

- Vision to replace traditional banking rails.

In this article

Avici Review IntroductionProblem StatementSolutions Provided by AviciProblem–Solution OverviewTechnology & ArchitectureTokenomicsMarket PerformanceTeam & GovernanceAvici Review Project AnalysisAvici Review Conclusion