SEC guidance clarifies when DeFi interfaces can avoid broker-dealer registration, outlining strict rules for self-custodial crypto apps.

Author: Akshat Thakur

Steady attention without excessive speculation.

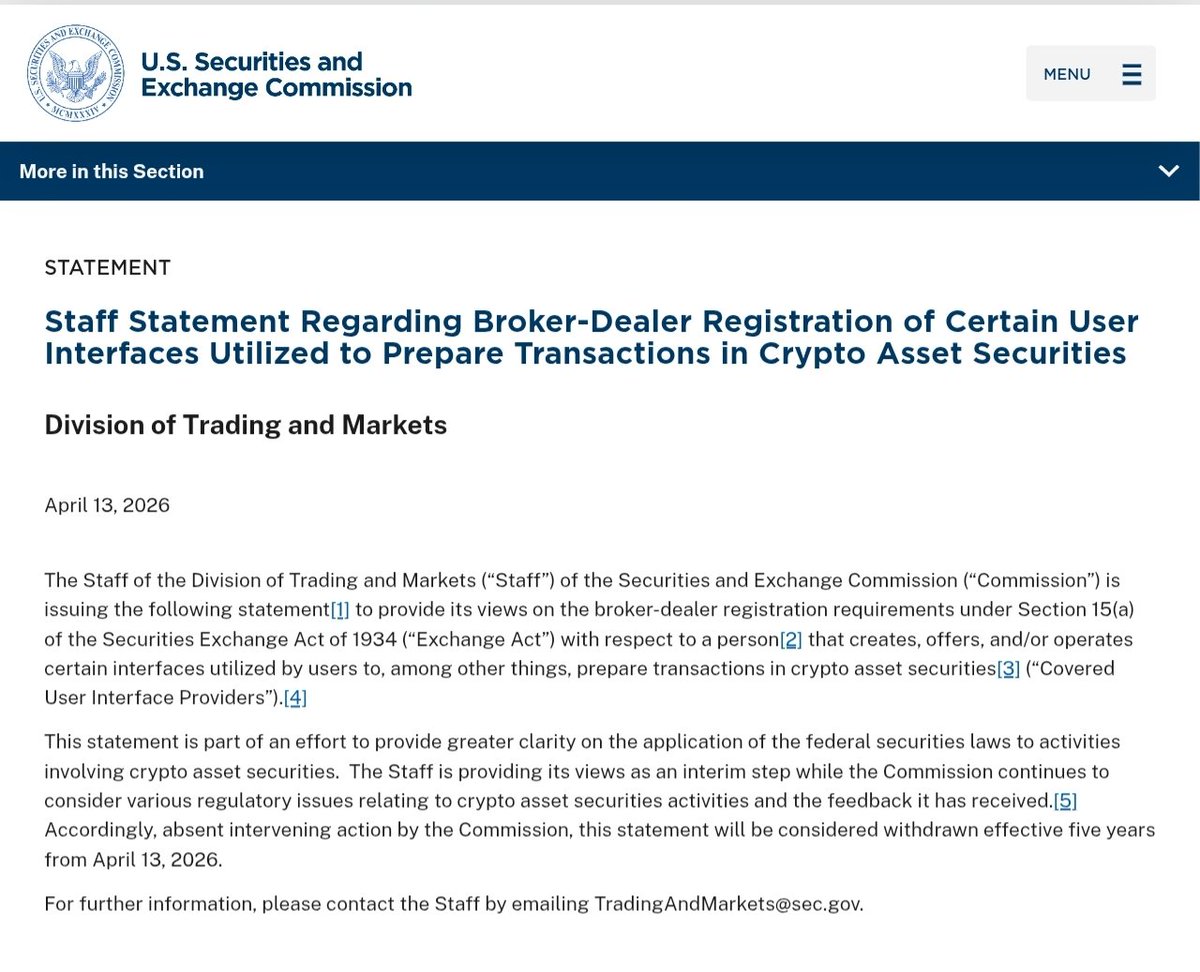

14th April 2026 – The SEC’s Division of Trading and Markets released a staff statement on April 13. It outlines when crypto trading interfaces can skip broker-dealer registration under Section 15 of the Exchange Act.

High Signal Summary For A Quick Glance

CryptosRus

@CryptosR_Us

SEC'S NEW GUIDELINES JUST HANDED CRYPTO A WIN. The SEC's Division of Trading and Markets says apps & wallets can now operate without broker-dealer registration if they meet specific conditions. This is the clarity institutions have been waiting for. Regulatory tailwind https://t.co/gcmW07BVyZ

05:39 PM·Apr 13, 2026

Crypto India

@CryptooIndia

JUST IN: 🇺🇸 SEC says DeFi apps and wallets can operate without broker registration if they: • don’t route or execute trades • don’t give investment advice • don’t hold user funds • don’t take trade-based fees or incentives https://t.co/hwFOx7gn5Y

01:58 PM·Apr 13, 2026

Cointelegraph

@Cointelegraph

🇺🇸 JUST IN: SEC says certain crypto interfaces, including DeFi front-ends, wallet extensions, and apps, may operate without broker-dealer registration under conditions: • No custody of user funds (self-custodial only) • No investment advice or recommendations • No order https://t.co/0LcMhKlMPE

01:46 PM·Apr 13, 2026

The guidance applies narrowly. It addresses only SEC DeFi broker-dealer registration obligations under Section 15 of the Exchange Act. It does not touch exchange registration, ATS rules, anti-fraud provisions, or state-level requirements.

The framework covers only crypto asset securities transactions. Interfaces that stay within the guardrails can operate without registering. Those that step outside the conditions still face potential enforcement.

A Covered User Interface Provider must meet strict operational requirements. Users must retain full control of their private keys and assets. The interface cannot custody funds, give investment advice, or exercise any discretion over execution.

Routing is another critical area. The interface cannot route orders on the user’s behalf. It can display market data, estimate gas fees, and format transaction code. The user alone decides parameters and signs from their own wallet.

Fees must remain fixed and neutral. Providers can charge either a flat amount or a consistent percentage. That fee applies uniformly regardless of asset, venue, or counterparty. No hidden order-flow payments or variable incentives are allowed.

When multiple execution routes appear, the interface must offer objective sorting tools. Sorting by price or speed is acceptable. Labeling any route as “best” or “most reliable” is not.

Default settings are permitted only if users can override them. Providers must also supply educational material about available choices. On top of that, each provider must maintain policies for selecting connected protocols based on measurable factors like liquidity depth and security audits.

Full disclosures are mandatory under the framework. The interface must prominently explain the provider’s role and any affiliations with trading venues. All fees and their structure must be visible.

Material conflicts, cybersecurity practices, and asset limitations also require disclosure. Affiliations with any trading venue must receive equal treatment alongside unaffiliated options. As a result, interfaces cannot quietly steer users toward connected platforms.

This guidance draws a workable line between passive software and traditional brokerage activity. For years, the threat of broker-dealer registration hung over every DeFi front-end. Uniswap’s interface, wallet swap screens, and browser extensions all sat in a regulatory gray zone.

Full registration brings net-capital rules, SIPC membership, and extensive compliance overhead. That uncertainty chilled legitimate UX improvements. It also pushed many projects offshore or into legal limbo.

According to the staff statement, domestic developers now have a concrete compliance path. The 2023 Coinbase Wallet lawsuit set the legal precedent for this approach. A federal court dismissed claims that the non-custodial wallet acted as a broker by connecting users to decentralized exchanges.

The mechanics keep the interface as a passive translator. A user opens the app or extension, selects an asset and amount, and reviews displayed data. They adjust any defaults and click to sign.

The software then generates the calldata. The user’s wallet broadcasts the transaction. Settlement happens directly on-chain with no off-chain matching or discretionary routing. Compensation flows only through the disclosed fixed fee.

The entire position expires five years from April 13, 2026. Without further Commission action, the framework disappears in 2031. The staff described this as an interim measure.

That sunset clause creates urgency for the industry. Projects must demonstrate that the model works without investor harm. If gaps appear around aggregator routing or MEV protections, the Commission could tighten conditions before expiration.

Wallet providers and DeFi front-ends will likely update their documentation and fee disclosures. Teams that previously hesitated on U.S.-facing features may now accelerate consumer-facing improvements. Better default settings and objective route comparators are likely priorities.

Enforcement risk drops for compliant interfaces. The statement also feeds into the SEC’s ongoing Crypto Task Force work. It could influence parallel CFTC guidance on derivatives interfaces as well.

For now, the SEC staff has handed DeFi builders a practical blueprint. It validates the core architecture of permissionless interfaces. At the same time, it insists they stay true to the self-custodial promise that defined the space from the start.

This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

Our Crypto Talk is committed to unbiased, transparent, and true reporting to the best of our knowledge. This news article aims to provide accurate information in a timely manner. However, we advise the readers to verify facts independently and consult a professional before making any decisions based on the content since our sources could be wrong too. Check our Terms and conditions for more info.