Deep Dive

The Machine Economy

How AI + Robotics Rewrites Web3

How AI + Robotics Rewrites Web3

If you still think humanoid robots are a 2030 thing, you are already behind. The industry crossed a threshold in 2025 that most retail investors have not priced in.

Here is what actually happened in 2025. Humanoid robot shipments hit just under 14,000 units worldwide. Revenue crossed $500 million for the first time. China captured over 80% of installations. And then Figure AI did something that should have been front-page news in every financial publication on Earth.

They ramped production 24x in under 120 days. One Figure 03 per day in January. One per hour by April. Over 350 units shipped by late April. The Figure 03 runs Helix, a vision-language-action model that lets the robot walk into a space it has never seen before and adapt in real time. No reprogramming. No manual setup. Just a robot that figures it out. The $39 billion Series C valuation tells you that NVIDIA, Intel Capital, and Qualcomm are not speculating. They are buying infrastructure.

Tesla's Optimus Gen 3 launched at $20,000 to $30,000 and is already running inside the Fremont factory at scale. Boston Dynamics Atlas sold out its entire 2026 production run before the public announcement. 1X Technologies hit 10,000 pre-orders for its $20,000 Neo robot in five days. These are not concept cars. They are shipping products with committed buyers and confirmed deployments.

Three cost curves are collapsing at the same time. Hardware is falling from $35,000 per unit toward $13,000 to $17,000. Vision-language-action models are removing the need for environment-specific programming. And manufacturing scale is finally real. When three cost curves collapse simultaneously in a new technology, you get an inflection. This is that inflection.

UBS is forecasting 2 million workplace humanoids by 2035 and 300 million by 2050. That is a market expanding from $30 to $50 billion to $1.4 to $1.7 trillion. You can dismiss that forecast if you like. But Figure AI is already at one robot per hour. The question is not if this happens. It is who owns the infrastructure when it does.

You can train a language model on the entire internet. You cannot train a physical AI model on data you do not have. That is the entire argument for DePIN, and it is a good one.

Think about what a humanoid robot actually needs to work in the real world. It needs to know exactly where it is, down to the centimeter. It needs a 3D model of the space around it. It needs a wireless connection to send and receive data. And the engineers training the next version of its brain need footage of edge cases, the weird situations the robot has never seen before. None of that infrastructure exists in any hyperscaler's server farm.

A single autonomous vehicle data collection run in San Francisco covers one city in one climate on one set of roads. Building a robot that works globally requires data from everywhere. You need someone in rural Vietnam, a warehouse operator in Poland, a farmer in Brazil, all contributing data from their real environments. Token incentives are the only economic model that makes global decentralized data collection viable at speed.

Here is the honest market picture. By early 2026, the DePIN sector market cap sat between $9 billion and $10 billion. On-chain revenues hit $72 million in 2025. Roughly 40% of crypto VC in 2025 targeted AI-integrated blockchain projects. Over $400 million flowed into the Peaq ecosystem alone. This is not speculative froth. This is early-stage infrastructure capital.

There are five DePIN verticals that matter for physical AI. Precision positioning so robots know exactly where they are. Spatial mapping so they understand the space around them. Visual training data so future model generations get smarter. Wireless connectivity so autonomous fleets stay connected without paying carrier rates. And verifiable compute so the data robots generate can actually be trusted. Every robot needs all five.

The speculative era is over. Revenue multiples compressed from 1,000x to 10 to 25x for the leaders. Some people will read that as bearish. We read it the opposite way. Cheap narratives with real fundamentals underneath are how you find the next wave before everyone else does.

DePIN is not competing with centralized AI infrastructure. It is solving the problems centralized AI infrastructure structurally cannot solve.

Most L1 blockchains want to be everything to everyone. Peaq made the opposite bet: be the only thing that matters for machines. So far, that bet is working.

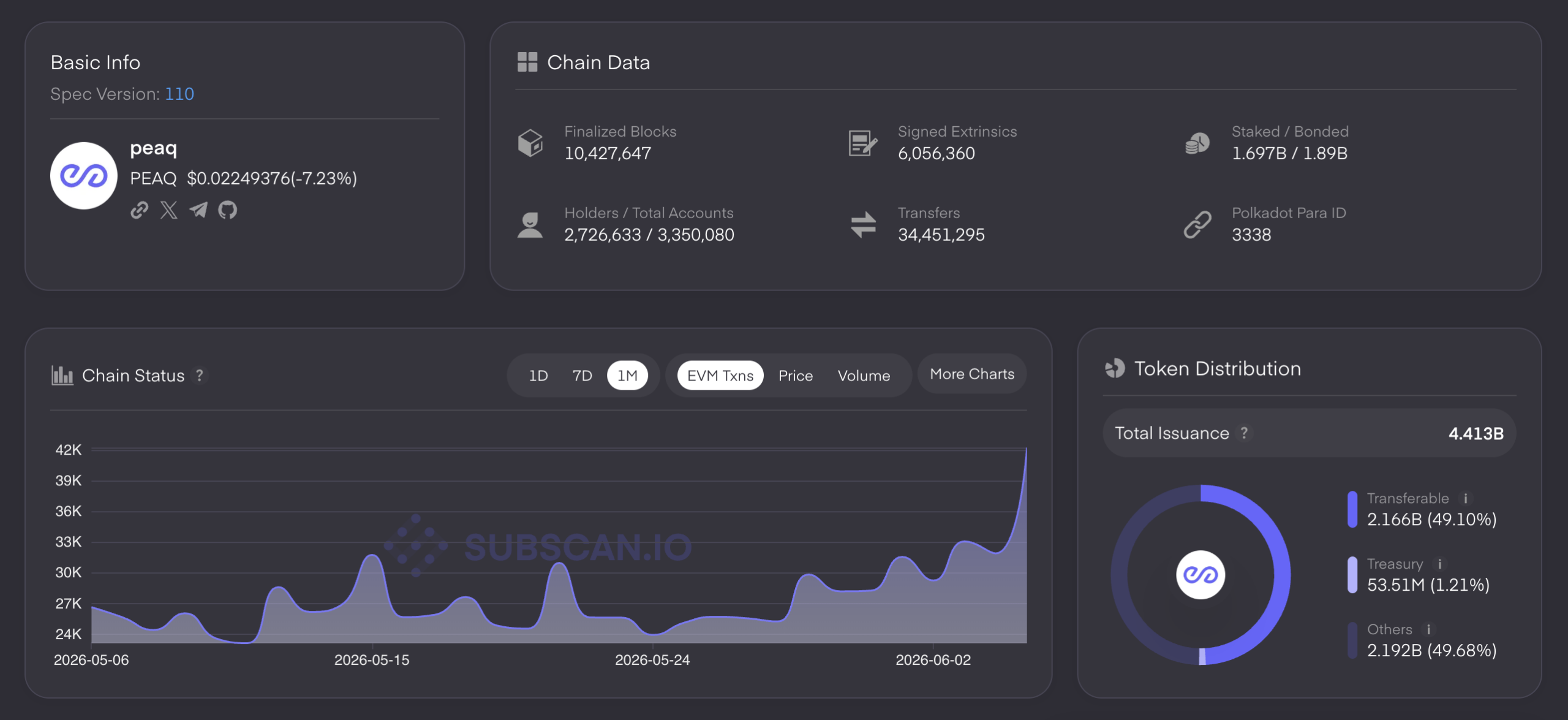

Let us start with what Peaq actually is, because most descriptions get it wrong. It is not a general-purpose Layer 1 trying to compete with Solana or Ethereum. It is a machine identity and settlement network. Every machine that wants to hold value, earn revenue, and transact autonomously needs an operating system. Peaq is building that OS. As of May 2026, 60 DePIN applications are live across 22 industries, and 6 million machines are connected on-chain. That is not a roadmap. That is a product.

peaqOS gives every connected machine four things: a self-sovereign identity (peaqID), a wallet to hold and transact value, cryptographic trust for its data outputs, and on-chain settlement for machine-to-machine payments. The thing that makes this interesting is that it is omnichain by design. A robot running peaqOS can settle a payment on Solana while keeping its identity and reputation on Peaq. The Serve Robotics delivery bot already does exactly this in Seoul.

In May 2026, Peaq launched robotic.sh. This is where the thesis gets real. Machines running peaqOS can now buy AI inference, geospatial correction data, and cloud analytics from other machines on-chain, autonomously, without a human in the loop. Most people are still debating whether machine-to-machine commerce is possible. Peaq shipped a marketplace for it.

The Machine RWA angle is the part retail investors should pay attention to. Peaq's Initial Machine Offering framework lets operators tokenize the cash flows from productive robots, not the machine itself, but the revenue it generates. The first tokenized robot farm in Hong Kong distributed $3,820 USDT to an early holder in January 2026 at roughly 18% APY. CoinList is confirmed as a launchpad partner for future offerings.

The on-chain numbers are early-stage but directional. Market cap $62.1M. TVL up 55.7% in 30 days. App fees up 5,152% in 30 days, which is a low-base effect but the direction is clear. Peaq is in active regulatory dialogue with Dubai's VARA for machine RWA licensing. If that clears, it changes the addressable market considerably.

Robots are purchasing AI inference from other robots, on-chain, in real time. That is not a 2030 roadmap item. robotic.sh launched in May 2026.— OCT Research, June 2026

Standard GPS is accurate to about 3 to 5 meters. A warehouse aisle is 3.5 meters wide. Do the math. That is why Geodnet exists, and that is why it matters.

RTK GNSS sounds technical but the concept is simple. You take GPS, add a reference station on the ground that knows exactly where it is, and you use that station to correct the satellite signals in real time. The result is 1 to 2 centimeter horizontal accuracy. For robots, drones, surgical systems, and autonomous vehicles, the difference between 3 meters and 1.5 centimeters is the difference between a product that works and one that kills people.

Trimble and Hexagon have been building centralized RTK networks for decades. Their subscriptions run $1,200 to $3,500 per device per year. And they still have almost no coverage in Southeast Asia, Sub-Saharan Africa, or agricultural interiors globally. These are exactly the regions where autonomous farming robots and delivery drones are being deployed first. Geodnet's decentralized model simply outcompetes them everywhere it counts.

Community operators deploy stations using sub-$1,000 hardware, earn GEOD rewards for uptime and coverage quality, and the network scales to wherever stations are deployed. Geodnet now has 20,000 active stations across 140+ countries. Trimble and Hexagon had decades and billions of dollars. Geodnet built this in a few years with token incentives. That is worth sitting with.

The GEODASH Aerosystems joint venture with DroneDash Technologies is the commercial proof point that changes the narrative from network builder to revenue generator. Their system eliminates the pre-mapping flight that agricultural drones need before every deployment. The drone maps and sprays simultaneously using Geodnet's live RTK correction feed. Commercial target is Q3 2026, starting with Southeast Asian oil palm and sugarcane plantations.

The financials make sense at current prices. $67.4M market cap against roughly $10M in annualized revenue is a 6.7x P/S ratio. That is not cheap, but it is reasonable for a network with 19% quarterly revenue growth and real enterprise contracts. The risk to model is the FDV overhang but quarterly burns are there to regularly make this deflationary

Trimble and Hexagon had decades and billions. Geodnet built the largest decentralized RTK network on Earth in years, using token incentives. That gap is not closing.— OCT Research, June 2026

Everyone in robotics is obsessed with manipulation. Picking things up, moving things around. Auki thinks that is the wrong problem to solve first, and they are probably right.

Before a robot can pick anything up, it needs to know where it is, what surrounds it, and how the space is organized. That is perception. And right now, every robot company is solving perception from scratch, building proprietary systems for every new deployment. Auki's argument is that this is massively inefficient and that a shared, decentralized perception layer would unlock the entire industry. They are building it.

The Posemesh works through three layers. Domain Servers hold persistent 3D spatial maps of physical venues. Reconstruction Servers convert raw camera scans into point cloud data. The Hagall Layer coordinates real-time spatial data exchange between any device visiting that space. A robot walks into a warehouse and immediately knows the layout because the Domain Server already has it. No setup required.

The privacy architecture is what makes enterprise deployment actually possible. Devices do not upload raw camera feeds to a central server. They exchange processed spatial data only with the specific domain they are visiting. For any company deploying robots in sensitive environments, hospitals, government buildings, financial facilities, this is not a bonus feature. It is the feature that makes a yes decision possible.

The CTRL+R supermarket partnership reveals the business model. Auki owns the deployed robots and the spatial perception layer. Third-party manipulation AIs license onto that hardware. Auki provides the eyes and the map. Partners provide the hands. Auki captures the infrastructure rent on every single deployment without needing to solve the manipulation problem itself.

The near-term revenue vehicle is Cactus, an AI-assisted store inventory management product. The moat is the posemesh itself. As it scales, the spatial index of the physical world becomes the most valuable queryable dataset in the physical AI stack. Think of it as Google Maps for the interior of every building on Earth, updated in real time, owned by nobody.

Google and Apple are surveillance infrastructure by design. The Posemesh is the privacy-preserving alternative that enterprises can actually deploy without calling their legal team first.

Most DePIN projects talk about real revenue. Helium has it. That one sentence should tell you everything about why it belongs at the top of this list.

Let us be direct about why the Solana migration in April 2023 mattered. The original Helium chain could not settle hundreds of thousands of daily micro-reward transactions at sub-cent economics. It was technically impossible on the original architecture. Moving to Solana removed that ceiling, and within the same year, the Helium Mobile cellular product launched. That sequence matters. Fix the infrastructure, ship the product.

The T-Mobile MVNO partnership is what made Helium Mobile usable. You cannot sell a mobile plan with coverage gaps. T-Mobile filled them. But the AT&T Passpoint integration is the more interesting story. AT&T subscribers can automatically authenticate to Helium hotspots without touching their phone. AT&T is not just providing backup coverage. It is integrating Helium into its Wi-Fi convergence architecture as a genuine component.

Here is the part that most retail analysis misses. AT&T and Telefonica are paying per-gigabyte to the Helium protocol for carrier offload at stadiums, airports, and dense urban nodes. Every megabyte of offloaded data burns Data Credits, which burns HNT. Traditional telco B2B revenue is creating on-chain deflation. This is the closed-loop demand driver most DePIN protocols are still trying to design. Helium already built it.

The physical AI angle for Helium is LoRaWAN. Low-power, long-range, low-cost wireless for autonomous sensor fleets, agricultural IoT, and warehouse robot coordination. These are exactly the use cases that macro cell towers are too expensive for. Helium fills that gap at a price point that makes the economics of large autonomous deployments actually work.

The numbers hold up at current prices. $130.3M market cap against roughly $17.5M annualized fees is a 7.4x P/S ratio. By April 2026, 3.5 million people in the U.S. alone were being served daily. 600,000 Helium Mobile subscribers. 4,388 TB of data offloaded in Q4 2025, up 60.7% quarter on quarter. If you need one DePIN protocol with the clearest path to durable revenue, this is the one.

Every AT&T gigabyte offloaded through a Helium hotspot burns HNT. Traditional corporate revenue is driving on-chain token deflation. That is the closed loop most DePIN protocols are still chasing.— OCT Research, June 2026

IoTeX is the most technically rigorous project in this report. It is also the most frustrating to cover, because the adoption has not caught up to the architecture yet.

Here is the problem W3bstream solves, and it is a real problem. Raw sensor data from a DePIN device is trivially spoofable. A GPS tracker can broadcast fake coordinates. A weather sensor can relay manipulated readings. If the data robots and sensors generate cannot be cryptographically proven to be real, then every downstream decision that relies on that data is built on sand. W3bstream solves this with ZK proofs that verify device identity, sensor state, and timestamp simultaneously. This matters enormously.

The GEODNET-IoTeX integration is the best example of this in practice. GEO-PULSE dash-mounted devices record lane-level GPS data, W3bstream attests it cryptographically, and the device owner earns both IOTX and GEOD rewards simultaneously. Two verified revenue streams from one device. That dual-mining model is compelling for hardware manufacturers and should drive ioID adoption at the device level if IoTeX executes on distribution.

ioID is the identity layer: devices registered as NFTs on-chain with transferable ownership, composable across DePIN projects. 399 ecosystem projects and 25 million DePIN devices already on the network. The DePINscan analytics dashboard launched May 2025 gives the ecosystem a unified view. The infrastructure is genuinely there.

So why is this section titled the wrong moment? The numbers. $41.4M market cap. $1.92M TVL. 30-day fees of $1,064. Not $1 million. One thousand and sixty-four dollars. The architecture is excellent. The enterprise integrations are real. But consumer adoption is thin and the token price reflects that honestly. IoTeX is not a bad project. It is an early one that has not found its breakout use case at scale yet.

If you are a patient investor, the thesis is that W3bstream becomes critical infrastructure once one large physical AI project validates it publicly. That could change the picture significantly. But you are waiting for a catalyst that has not arrived yet. Size your position accordingly. Do not bet on architecture alone.

In 2026, Natix made one product decision that could define the next five years for the project. They stopped competing in dashcam mapping and pivoted to something much more interesting.

The VX360 pivot is the story. Instead of asking people to buy a dedicated dashcam, Natix targeted the four cameras already in millions of Tesla vehicles sitting in driveways right now. VX360 is a dongle that captures 360-degree footage from all four Tesla cameras, backs it up to personal cloud storage, and lets owners contribute anonymized driving events to the data marketplace in exchange for NATIX tokens. Hardware already in the field. Existing behavior monetized. That is good product thinking.

Here is the business context that makes this move brilliant. Tesla, Waymo, and Mobileye collect proprietary training data that they keep entirely to themselves. That data moat is the reason incumbents stay incumbents. But the robotics companies building humanoids, the agricultural AI companies building field robots, the logistics companies building warehouse systems, they do not have access to any of that. They are data-starved. Natix is building the marketplace that solves their problem.

The data buyers are real. OEMs, AI labs, and mapping companies subscribe to data types and receive flagged clips in standardized formats, including edge- case extraction via VLMs and 4D simulation scenarios in OpenDrive format. The $NATIX burn mechanism links token value directly to marketplace demand. More AI labs buying data means more token burns. April 2026 hit a record 110 million $NATIX burned in a single month.

The enterprise validation is hard to argue with. The Autoware Foundation partnership puts Natix data into the training pipeline for the leading open- source autonomous driving stack. The Valeo collaboration places Natix data into the World Foundation Model of one of the largest global automotive suppliers. These are not crypto companies. These are serious industrial partners choosing Natix data for production research.

The honest risk is that Natix is not tracked on DefiLlama, which makes independent verification of metrics harder for retail investors. Always verify numbers directly from official sources before making a decision. That said, 269,000 contributing drivers, 247 million kilometers mapped, and two tier-one enterprise partnerships in six months is a real track record. This is one of the more underrated setups in the DePIN space.

The protocols that build the largest, most cryptographically attested physical datasets in the next 24 months will be infrastructure monopolies or acquisition targets. Either outcome is good for holders.— OCT Research, June 2026

| # | MV | Asset | Price | 24h % | 7d % | Volume | Cap |

|---|---|---|---|---|---|---|---|

| 01 | | $130.3M mcap | -2% | -1% | $1.44M 30d | 7.4x P/S - Most defensible | |

| 02 | | $67.4M mcap | -2% | -1% | $825K 30d | 6.7x P/S - Stable in downtrend | |

| 03 |  | $62.1M mcap | -9% | -1% | $35K 30d | Early - Watch robotic.sh | |

| 04 |  | $41.4M mcap | -2% | -24% | $1K 30d | Dev infra - Needs breakout | |

| 05 |  | Verify directly | -10% | -20% | 110M burns | Verify - Not on DefiLlama |

The DePIN narrative in 2026 is no longer speculative. That is the headline. The details matter more than the headline.

Revenue multiples compressed from 1,000x to 6 to 7x for the leaders. That sounds bad. It is not. It means the easy money is gone and the smart money is now buying on fundamentals. Helium at 7.4x P/S with $17.5M in annualized carrier revenue is a different kind of investment from Helium at 1,000x speculative multiple with no revenue. The former requires more work to evaluate. It is a better bet.

The clear pattern: revenue generators outperform. Helium and Geodnet are leading because they have enterprise buyers paying real money. Peaq and IoTeX are trailing because they are still in the bootstrap phase where token rewards are doing most of the economic work. That gap will close as machine-to-machine commerce volume scales, but it has not closed yet.

Institutional money is moving in more quietly than the headlines suggest. Grayscale weighting conversations, corporate treasury exposure, and the UAE's $500 million Digital Energy Infrastructure fund targeting AI-DePIN convergence are all signals that the next buyer cohort is not retail. Retail investors who understand this sector now are positioned ahead of that institutional wave.

Let us cut to it. The physical AI wave is real. The infrastructure question is which protocols will still be executing in 2028 when deployment velocity peaks. Here is our honest take.

Start with the macro. Humanoid robots are going from thousands of units to tens of thousands in 2026, then hundreds of thousands after that. Every single one of those robots needs precise positioning, a spatial model of its environment, wireless connectivity, verifiable sensor data, and training data for the next model generation. You are not speculating on whether this market exists. You are choosing which infrastructure protocols will capture the most value from it.

The cold-start problem is already solved. Geodnet bootstrapped 20,000 stations. Helium bootstrapped 800,000 daily active users. Both did it with token incentives at a fraction of the cost of traditional capex. The existential question is whether revenue can sustain those networks after token inflation subsidies wind down. Helium's carrier offload revenue says yes. Geodnet's enterprise contracts say yes. The others are still proving it.

Our verdict on each project. Helium: the most defensible valuation in the sector at 7.4x against real telco revenue. Buy the dip. Geodnet: the largest decentralized RTK network on Earth with a GEODASH enterprise catalyst in Q3. Model the FDV dilution before sizing. Peaq: the right architecture for the machine economy with early but directional revenue. Watch robotic.sh volume as the leading indicator. Natix: the right pivot at the right time with two tier-one enterprise validations. Undervalued relative to its data moat. IoTeX: genuinely important infrastructure waiting for its breakout moment. Smaller position until W3bstream gets validated at scale. Auki: the most underappreciated thesis in the group. Pre-revenue but solving the hardest problem. A speculative allocation with real upside if co-embodiment scales.

The acquisition thesis is the one most retail investors are not pricing. NVIDIA, Google, and Microsoft cannot build decentralized physical infrastructure with capital alone. They cannot bootstrap a global RTK network. They cannot incentivize 270,000 drivers. The protocols building the most defensible physical datasets and networks are either the infrastructure monopolies of the machine economy, or acquisition targets. Either outcome creates value for token holders. That is an asymmetric setup worth paying attention to.

One more thing worth saying clearly. Every protocol in this report is high-risk. Token dilution, execution risk, regulatory uncertainty, and timing risk are all real. Do your own research. Verify every metric independently. This report is a starting point, not financial advice. But the physical AI infrastructure layer is being built right now, and the window to own it at current valuations will not stay open forever.

The machine economy is not a 2030 prediction. It is a 2026 deployment. The infrastructure underneath it is being built in public, on-chain, with metrics you can verify yourself.