Stablecoins are a category of crypto created to maintain a consistent value, typically by linking their price to a real-world asset. Unlike Bitcoin or Ethereum, which are highly volatile, stablecoins are designed to reduce price fluctuations. This feature makes them useful in everyday transactions, trading, and decentralized finance.

At their core, stablecoins serve as a bridge between the traditional financial system and the fast-paced world of crypto. By mimicking the price stability of fiat currencies like the US dollar, they offer a digital alternative for storing and transferring value without the unpredictability found in most cryptocurrencies.

Over the years, stablecoins have become a critical component of the crypto market. Traders use them to move funds between exchanges quickly. Developers use them to build decentralized finance platforms. Individuals in unstable economies rely on them to preserve purchasing power. But the real question remains—how do stablecoins work, and why have they become so essential in digital finance?

This article will break down the different types of stablecoins, how they function, why they matter, and which ones dominate the market. Let’s start with the foundation: how these tokens maintain stability.

Working of Stablecoins

Stablecoins achieve price stability by linking their value to external assets, like fiat currencies, commodities, or even other cryptocurrencies. To keep their prices consistent, they use one of four main mechanisms. Each method comes with its own structure, benefits, and risks.

Fiat-backed stablecoins

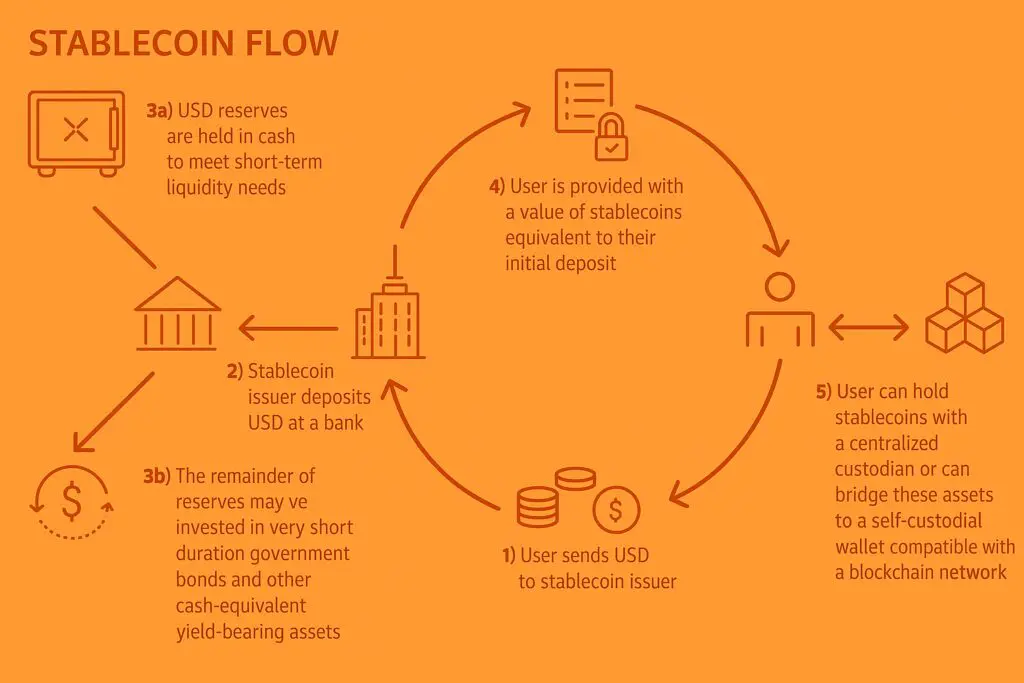

These are the most common and widely used type of stablecoin. Each token is backed 1:1 by a real-world currency, usually the US dollar. For example, if a company issues one million stablecoins, it should have one million dollars stored in reserves to support them. The reserves are often held in banks or money market instruments.

Two leading examples in this category are Tether (USDT) and USD Coin (USDC). USDC, issued by Circle, emphasizes transparency with regular third-party audits. Tether, on the other hand, has faced criticism in the past over unclear disclosures about its reserve composition. Still, both dominate trading volume and provide fast liquidity across platforms.

Fiat-backed stablecoins rely on the trust that the issuing entity actually holds sufficient reserves. If users lose confidence in this backing, the peg could break, leading to devaluation.

Crypto-backed stablecoins

Instead of being tied to fiat, these stablecoins use other cryptocurrencies as collateral. Because cryptocurrencies are volatile, these coins are often overcollateralized. That means you might need to deposit $150 worth of ETH to mint $100 worth of a stablecoin.

A popular example is Dai (DAI), which runs on the Ethereum blockchain and is managed by the MakerDAO protocol. Users lock their collateral into smart contracts, which maintain the peg through automated liquidation and risk mechanisms. If the value of the collateral falls below a set threshold, it gets sold off to ensure that the stablecoin remains backed.

Crypto-backed models aim for decentralization and transparency, but they are also exposed to the volatility of the assets backing them. A rapid drop in crypto prices could lead to mass liquidations and risk the stability of the system.

Commodity-backed stablecoins

These coins are tied to physical assets like gold, oil, or real estate. One token equals a set amount of the asset, often stored in secure vaults. Pax Gold (PAXG) is one such stablecoin, where each token is backed by one fine troy ounce of gold.

Commodity-backed stablecoins allow people to invest in tangible assets without holding them physically. They also open up markets for those who otherwise couldn’t access commodities due to regulatory or geographic limitations. However, they come with their own challenges—verifying reserves and ensuring proper custody are crucial for long-term trust.

Algorithmic stablecoins

This model takes a different approach. Rather than relying on collateral, algorithmic stablecoins attempt to control price through supply and demand. When prices rise above the peg, the system increases supply to bring it down. If the price falls, it reduces supply.

This mechanism is built into the code using smart contracts. It sounds elegant in theory, but the reality has been rough. The collapse of TerraUSD (UST) in 2022 exposed the fragility of algorithmic systems. Once confidence breaks, there’s often no collateral to absorb the impact.

While developers continue to experiment with improved models, most algorithmic stablecoins today face high risk and limited adoption.

Across all these types, the core idea remains the same: keep the token’s value stable. Whether through reserves, overcollateralization, or algorithms, stablecoins must maintain their peg to function effectively.

Top Stablecoins in the Market

The stablecoin landscape has grown rapidly, with several key players dominating the market by volume, adoption, and integration across protocols. Understanding these stablecoins and how they operate gives deeper insight into how stablecoin ecosystems actually function.

Tether (USDT)

Tether remains the most traded cryptocurrency in the world by volume. It’s pegged to the US dollar and issued by Tether Limited, which claims to back every token with reserves, including cash, cash equivalents, and other assets. Despite early criticism over transparency, Tether has held its peg remarkably well in practice.

Its dominance is partly due to early-mover advantage and deep liquidity on almost every exchange. It is widely used in crypto-to-crypto trading pairs and has become the default settlement token in many centralized and decentralized platforms.

USD Coin (USDC)

USDC is issued by Circle in partnership with Coinbase. It’s a regulated stablecoin, with reserves held in US bank accounts and short-term government securities. What sets USDC apart is its emphasis on transparency — it undergoes monthly attestations from third-party accounting firms.

USDC is widely used in the U.S. and integrated into hundreds of DeFi applications. It’s often the stablecoin of choice for those seeking regulatory clarity and audited backing.

Dai (DAI)

DAI is a decentralized stablecoin governed by MakerDAO. It’s pegged to the US dollar but backed by crypto assets, primarily ETH and other tokens like USDC. Users mint DAI by locking up collateral in smart contracts, and the system adjusts variables like fees and collateral ratios to help maintain the peg.

Its decentralization makes it unique. There’s no central authority holding reserves. Instead, the peg is maintained algorithmically and through community governance. DAI plays a critical role in DeFi protocols where decentralization is a must.

Binance USD (BUSD)

BUSD was launched by Binance in collaboration with Paxos, a regulated financial institution. It’s backed 1:1 with US dollars and approved by the New York State Department of Financial Services. While Binance recently phased out some support for BUSD following regulatory developments, it remains a significant stablecoin in terms of past volume and usage.

TrueUSD (TUSD), FRAX, and Others

TUSD offers real-time attestations of its reserves, aiming for maximum transparency. FRAX, once a semi-algorithmic stablecoin, has shifted toward a fully collateralized model in response to the collapse of algorithmic designs like UST.

Other region-specific stablecoins like EURC (Euro Coin) and XSGD (Singapore Dollar) are emerging as localized options, widening the use of stablecoins beyond the US dollar.

The choice between these stablecoins often depends on the user’s need—liquidity, transparency, decentralization, or regional fiat exposure.

Use Cases of Stablecoins

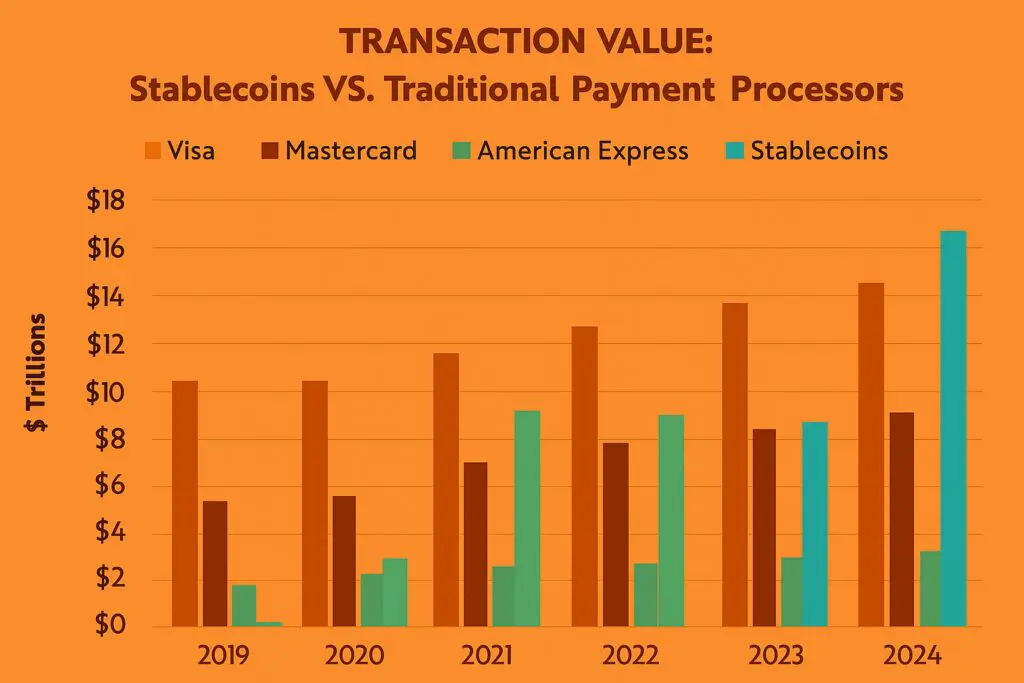

Stablecoins aren’t just tools for crypto traders. They’ve unlocked a wide range of real-world applications. Their ability to stay stable while operating on open blockchain networks makes them one of the most versatile tools in the digital economy. In 2024 the surge of stablecoin payments is enough to know the trend shift.

Trading and arbitrage

Most trading pairs on exchanges now involve stablecoins. Traders use them to move between assets quickly without going back into fiat. Arbitrage traders also use stablecoins to exploit price differences across platforms, executing trades within seconds.

Having a stable base asset means traders can sit in cash positions when needed, avoid slippage, and deploy capital across multiple platforms with less risk.

Lending and borrowing

Stablecoins are the lifeblood of decentralized lending markets. Platforms like Aave and Compound allow users to deposit stablecoins and earn interest, or borrow against their holdings.

This system provides both sides of the credit equation—borrowers gain access to liquidity, while lenders earn yield on idle assets. The use of stablecoins minimizes the volatility risk, making these platforms more usable and sustainable.

Payments and remittances

Stablecoins offer a faster, cheaper alternative to traditional money transfers. A stablecoin transaction can settle globally in seconds with minimal fees, compared to the multi-day, high-cost experience of SWIFT or wire transfers.

For cross-border workers sending money home, stablecoins provide more value to recipients. Even small businesses are beginning to explore crypto invoices and payroll using stablecoins for their global teams.

E-commerce and digital spending

Some online platforms and fintechs now accept stablecoins for digital purchases. Because stablecoins hold their value, they are suitable for online shopping, tipping, or subscription payments without worrying about volatility.

Integrations with debit cards and digital wallets are increasing, making it easier to spend stablecoins just like traditional currency.

On-chain savings and yield

Many users park their stablecoins in DeFi protocols to earn passive income. Yield farming strategies, liquidity provision, and staking pools offer returns on stablecoin holdings.

While these strategies vary in risk, the idea of earning real yield on stable dollar-pegged assets has attracted both retail and institutional capital.

Crisis and capital control resistance

In countries with strict capital controls, unstable fiat currencies, or financial repression, stablecoins offer an exit route. Citizens in places like Argentina, Venezuela, and Nigeria have increasingly turned to USDT and USDC to preserve wealth and conduct international transactions.

They allow people to operate outside of fragile financial systems without needing a foreign bank account.

The flexibility of stablecoins makes them usable for both everyday consumers and institutional power users. As the technology matures, use cases continue to evolve.

Benefits of Stablecoins

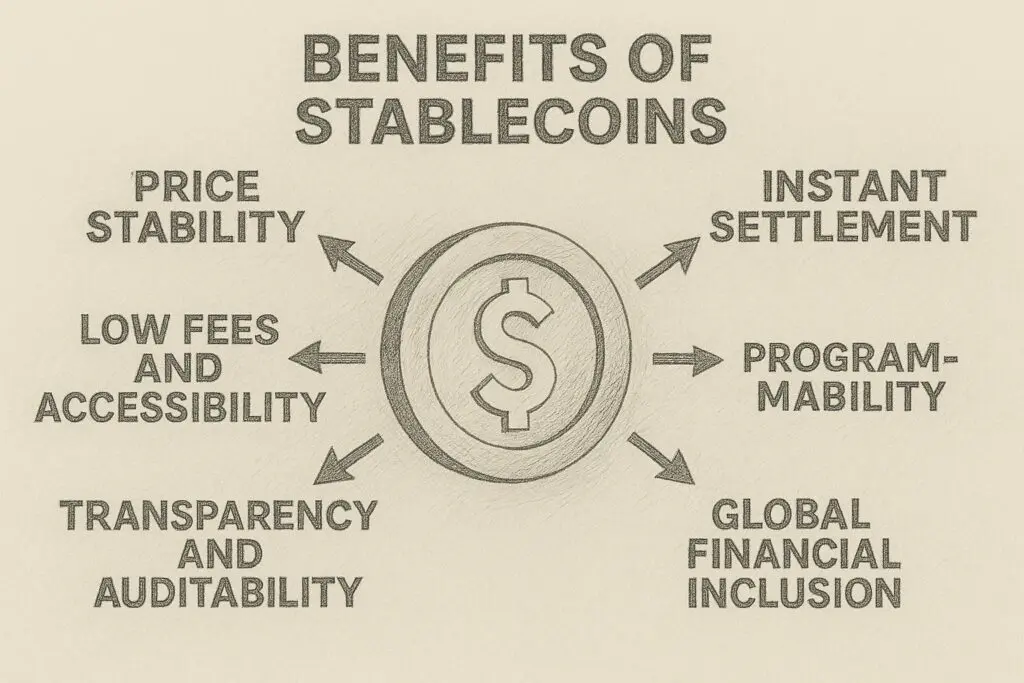

Stablecoins provide practical benefits that solve some of the key issues in both traditional finance and crypto. These aren’t just theoretical advantages but they’re shaping how digital finance functions today.

Price stability

This is the core advantage. Stablecoins remove volatility, making them suitable for savings, transactions, and accounting. Whether used in a DeFi strategy or to pay for services, users know what their assets are worth.

This predictability builds trust and usability in ways that Bitcoin or ETH can’t easily match. In a bear market you will find a big increase of stablecoins being held in wallets during price uncertainties. Investors find stablecoins as a better way to store crypto.

Instant settlement

Stablecoins move at the speed of blockchain. Transactions settle in seconds, regardless of borders, banking hours, or geographic location. This enables faster financial flows across the globe.

Instant settlement is particularly beneficial for exchanges, marketplaces, and money transfer services that need liquidity and responsiveness.

Low fees and accessibility

Most stablecoin transactions cost a fraction of a cent, especially on networks like Solana or Polygon. This makes them a strong choice for microtransactions or peer-to-peer transfers.

They also remove the need for intermediaries. Anyone with a smartphone and internet connection can use stablecoins, regardless of banking status or nationality.

Programmability

Because they’re digital and blockchain-native, stablecoins can interact with smart contracts. This enables automated payments, escrow, lending logic, yield optimization, and countless DeFi strategies.

This makes stablecoins more than just digital dollars—they are programmable money that integrates seamlessly with on-chain applications.

Transparency and auditability

Stablecoins issued by reputable companies offer real-time or monthly proof of reserves. Even decentralized versions like DAI are fully transparent on-chain. Users can verify balances and track flows.

This level of openness stands in contrast to traditional banking, where funds and liabilities are opaque to end users.

Global financial inclusion

For people locked out of stable financial systems, stablecoins offer an alternative. They allow access to dollars or other stable assets without needing a bank account. This is particularly powerful in unstable economies or regions with underdeveloped banking infrastructure.

They also lower the barrier to global investment, making it easier for individuals to participate in opportunities worldwide.

In short, stablecoins combine the best of both worlds: the reliability of fiat and the innovation of crypto. These advantages are why they’re not just surviving, but thriving in a volatile market.

Risks and Challenges of Stablecoins

Despite their rapid adoption and real-world utility, stablecoins aren’t immune to risks. Some are inherent to the way they’re structured. Others stem from the evolving regulatory and financial environment they operate in. Understanding these challenges is crucial for users, developers, and regulators alike.

Centralization risk

Fiat-backed stablecoins like USDT and USDC are issued by centralized entities. They hold the reserves and have full control over issuance and blacklisting of addresses. This level of control runs contrary to the ethos of decentralization and opens the door to censorship.

In some past cases, issuers have frozen specific wallet addresses. While this is sometimes used to comply with regulations or prevent fraud, it’s also a reminder that users don’t fully control these assets.

Reserve transparency

Stablecoin issuers claim to back every token with real-world assets. But the degree of transparency varies. Tether, for example, has long faced criticism over its reserve disclosures. Even with periodic attestations, full independent audits remain rare.

Without real-time verification or third-party audits, there’s always uncertainty. A loss of trust in reserves can trigger mass redemptions or cause the stablecoin to depeg — a scenario that could ripple through the broader crypto market.

Regulatory uncertainty

As stablecoins begin to compete with traditional banking products, they attract regulatory scrutiny. Governments are now asking tough questions about whether stablecoins are securities, how reserves are managed, and what risks they pose to financial stability.

Recent U.S. proposals seek to place fiat-backed stablecoins under federal oversight, possibly requiring them to hold reserves in insured institutions or register as banks. These changes could affect how projects operate or which coins are accessible to users.

In the EU, the Markets in Crypto-Assets (MiCA) regulation will impose caps and reserve requirements. This will likely raise operational costs and limit the use of non-compliant stablecoins in Europe.

Algorithmic failure

Decentralized stablecoins come with their own set of risks. Algorithmic models, especially under-collateralized ones, have proven to be fragile. The collapse of TerraUSD (UST) in 2022 was a stark reminder. A massive depeg event wiped out over $40 billion in market value.

Even overcollateralized stablecoins like DAI can be tested during market crashes. If collateral assets plunge in value or liquidity dries up, the system can struggle to maintain the peg.

Smart contract vulnerabilities

Stablecoins running on smart contracts are exposed to bugs or exploits. A flaw in the code could allow an attacker to mint excess tokens, drain reserves, or break peg mechanisms. Security audits help, but they don’t eliminate all risks.

DeFi integrations using stablecoins can also be compromised, leading to cascading failures across protocols. Users relying on smart contract-backed stablecoins must factor in this technical layer of risk.

Market liquidity and slippage

Not all stablecoins have equal liquidity. Outside the top three or four, lower-cap stablecoins may have limited exchange support and deeper spreads. In high-volatility periods, these tokens can experience slippage or struggle to maintain their peg.

For investors and institutions, this liquidity risk can translate into real financial loss, especially when moving large amounts of capital.

Stablecoins are not “risk-free crypto dollars.” They represent a balance between usability and trust — and that balance depends on design, governance, and external events.

The Future of Stablecoins

Stablecoins are evolving from a trading tool into a foundational layer of the new financial system. Their future will be shaped by regulation, innovation, and expanding demand — both inside and outside the crypto world.

Integration with traditional finance

Traditional institutions are beginning to explore stablecoins for payments and settlement. Visa and Mastercard have already tested stablecoin integrations. Fintech platforms now offer stablecoin deposits and withdrawals, bridging the gap between banking and blockchain.

Banks are also experimenting with their own tokenized dollars or stablecoin-like assets for internal transfers and cross-border settlements.

As these systems mature, stablecoins could become the default medium for digital cash transactions — not only in crypto but across mainstream finance.

Rise of non-USD stablecoins

Currently, most stablecoins are pegged to the U.S. dollar. But the demand for euro-, yen-, and rupee-pegged stablecoins is growing. As crypto adoption spreads globally, region-specific stablecoins will likely rise.

Projects like EURC, XSGD, and BRZ are early examples. They could reduce dollar dominance in DeFi and make localized on-chain economies more practical.

Regulatory clarity and new rules

Regulations are coming. In the U.S., stablecoin legislation is being debated that could require 100% cash reserves, audits, and issuance through insured institutions. MiCA in Europe will enforce strict reserve and reporting requirements starting in 2025.

These changes may reduce risk but could also reduce innovation. Some projects may exit regulated markets or shift to more decentralized models to stay competitive.

In the long run, regulatory clarity might legitimize stablecoins further, leading to broader adoption in traditional financial infrastructure.

Expansion in DeFi and tokenization

Stablecoins will remain the primary liquidity layer in DeFi. As more real-world assets (RWA) like bonds and real estate become tokenized, stablecoins will serve as the settlement currency.

This expansion ties directly into the DePIN and RWA tokenization narratives — where stablecoins act as the glue between crypto-native applications and off-chain value.

Central Bank Digital Currencies (CBDCs)

CBDCs are state-issued digital currencies. Some view them as competitors to stablecoins, others see them as complementary. In reality, the two may coexist. CBDCs could be used in local economies, while stablecoins remain dominant in cross-border DeFi environments.

Stablecoins also offer innovation that CBDCs can learn from — especially when it comes to programmability, composability, and user experience.

Stablecoins are no longer a niche product. They’re becoming a global infrastructure — programmable, borderless, and instantly transferable.

Final Thoughts

Stablecoins solve one of crypto’s biggest problems: volatility. By pegging to real-world currencies like the US dollar, they provide a stable unit of account while keeping all the benefits of blockchain — speed, transparency, and global access.

There are multiple types:

- Fiat-backed like USDT and USDC, held by companies with dollar reserves.

- Crypto-collateralized like DAI, using overcollateralized smart contracts.

- Algorithmic models, though risky and often unstable.

They’re used for trading, lending, payments, remittances, and savings. They power most of DeFi and are expanding into fintech and traditional finance.

But they also carry risks — regulatory uncertainty, transparency issues, algorithmic failures, and smart contract vulnerabilities. Understanding how each stablecoin is designed is essential before trusting it with your capital.

Looking ahead, stablecoins will play a central role in the tokenized economy. They’ll be used to buy real-world assets on-chain, settle transactions in global trade, and drive liquidity into emerging crypto narratives like DePIN and RWA.

In many ways, stablecoins are the infrastructure layer quietly powering the future of money — programmable, fast, and always on.

TL;DR – 20 Key Points (One-liner Bullets)

- Stablecoins are cryptocurrencies pegged to stable assets like the US dollar.

- Their goal is to reduce volatility while retaining crypto’s benefits.

- USDT, USDC, and DAI are the most widely used stablecoins today.

- Fiat-backed stablecoins hold real-world reserves in banks.

- Crypto-backed stablecoins rely on overcollateralized digital assets.

- Algorithmic stablecoins use code to maintain their peg, often riskier.

- They are widely used in DeFi for lending, trading, and saving.

- Stablecoins simplify on-chain payments and remittances.

- They’re essential for cross-border crypto transactions.

- Smart contracts can automate stablecoin use in dApps.

- Centralized stablecoins have blacklisting and censorship risks.

- Reserve transparency varies — not all are equally trustworthy.

- Regulatory pressure on stablecoins is rising worldwide.

- Failures like UST have made users more cautious.

- Smart contract bugs can cause systemic damage.

- USD dominance may give way to local currency stablecoins.

- Tokenization and RWA use stablecoins as payment rails.

- DePIN ecosystems rely on stablecoins for liquidity and scale.

- Stablecoins may coexist with CBDCs in future economies.

- They are evolving into foundational layers of global finance.